Key Insights

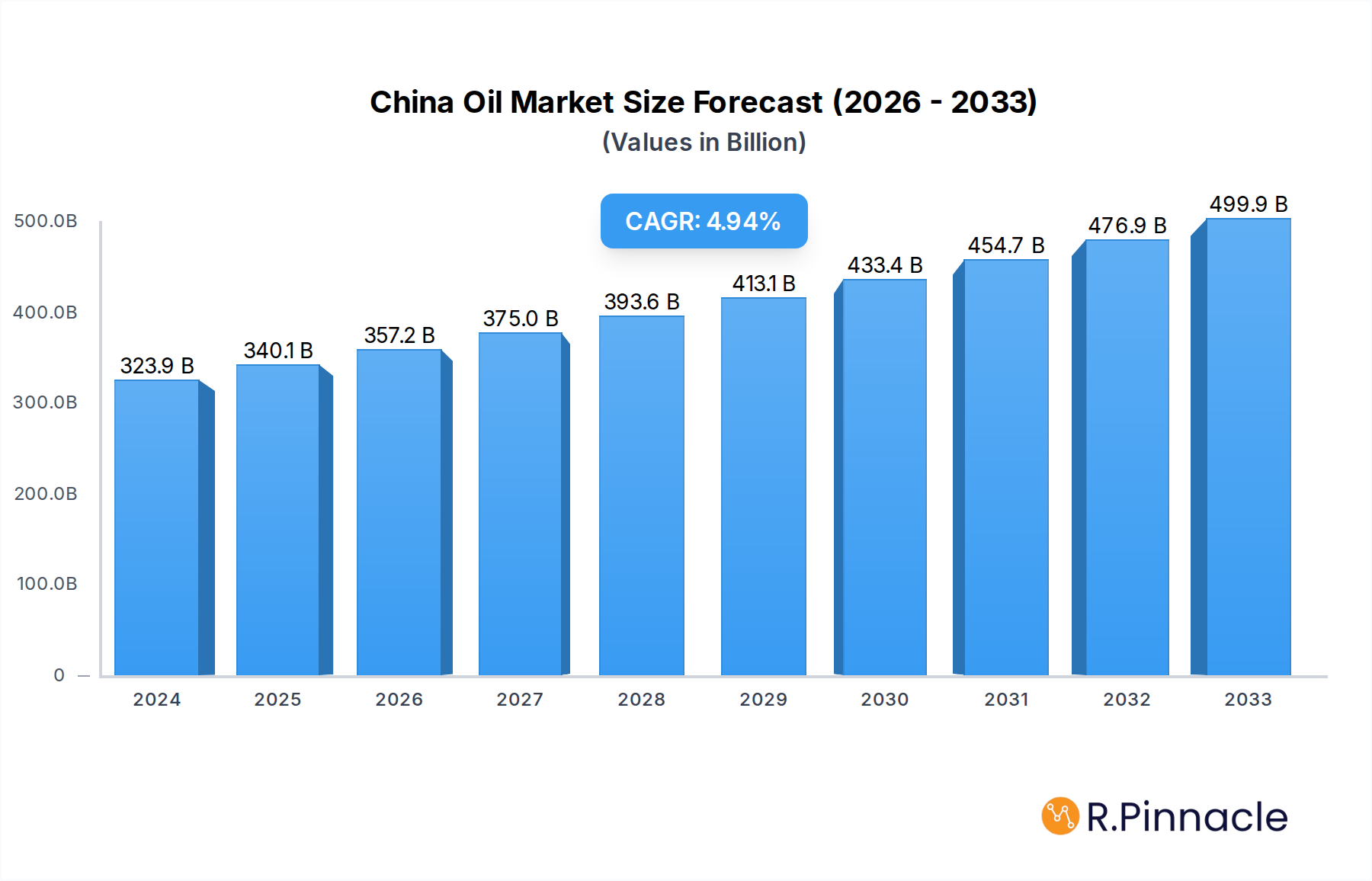

The China Oil & Gas Downstream Industry is poised for substantial growth, with the market size projected to reach $323.95 billion in 2024, driven by a healthy compound annual growth rate (CAGR) of 5%. This robust expansion is largely fueled by escalating domestic energy demand, rapid industrialization, and significant investments in refining and petrochemical infrastructure. Key drivers include the government's focus on energy security, increasing consumption of refined petroleum products, and the growing importance of the petrochemical sector in supplying raw materials for a wide range of industries, from plastics and textiles to automotive and construction. The industry is witnessing a transformation, with a clear trend towards the development of advanced, high-value petrochemical products and cleaner fuel alternatives. Furthermore, strategic expansions and upgrades in existing refinery capacities, coupled with the establishment of new integrated complexes, are set to bolster market performance. The ongoing shift towards more sustainable energy practices and stricter environmental regulations also presents both opportunities and challenges, prompting a focus on efficiency improvements and the adoption of greener technologies within the downstream oil and gas value chain.

China Oil & Gas Downstream Industry Market Size (In Billion)

The market dynamics are shaped by significant investments from major players like Sinopec, PetroChina, and CNPC, alongside international giants such as Shell and Total, who are actively participating in the development and modernization of China's downstream sector. The industry is segmented into Refinery and Petrochemical Plants, both experiencing robust demand. While growth is strong, certain restraints, such as fluctuating crude oil prices, intense competition, and evolving regulatory landscapes concerning emissions and environmental impact, require strategic navigation. However, the sheer scale of China's economy and its sustained appetite for energy and petrochemical derivatives provide a powerful underlying momentum. The forecast period from 2025 to 2033 anticipates continued, steady expansion, underscoring the enduring significance of the oil and gas downstream sector in supporting China's economic objectives and industrial progress.

China Oil & Gas Downstream Industry Company Market Share

This comprehensive report provides an in-depth analysis of the China Oil & Gas Downstream Industry, a sector pivotal to global energy markets. Spanning from 2019 to 2033, with a base and estimated year of 2025 and a forecast period of 2025–2033, this study leverages detailed historical data (2019–2024) to offer unparalleled insights into market dynamics, competitive landscapes, and future trajectory. With a focus on high-ranking keywords and reader-centric content, this report is essential for industry professionals seeking to navigate the complexities and capitalize on the opportunities within China's burgeoning downstream oil and gas sector.

China Oil & Gas Downstream Industry Market Structure & Innovation Trends

The China Oil & Gas Downstream Industry exhibits a moderately concentrated market structure, driven by the presence of national oil companies and a growing number of international players. Innovation is a key determinant of success, fueled by significant R&D investments in advanced refining techniques and the development of high-value petrochemicals. Regulatory frameworks, including stringent environmental policies and evolving fuel standards, are shaping operational strategies and product development. Product substitutes, such as renewable energy sources, are gaining traction but have yet to significantly disrupt the core demand for refined petroleum products and petrochemicals in the medium term. End-user demographics are increasingly sophisticated, demanding higher quality fuels and specialized chemical products. Merger and acquisition (M&A) activities are strategic, focusing on consolidating market share and acquiring advanced technological capabilities. For instance, M&A deal values in the sector are estimated to reach billions, reflecting the strategic importance of these transactions. Key market share percentages are held by major state-owned enterprises, with international players actively expanding their footprint through partnerships and direct investments.

China Oil & Gas Downstream Industry Market Dynamics & Trends

The China Oil & Gas Downstream Industry is poised for robust growth, with a projected Compound Annual Growth Rate (CAGR) of approximately xx% during the forecast period. This expansion is primarily propelled by China's insatiable demand for energy to fuel its continued economic development, industrialization, and a growing middle class with increasing disposable income. The market penetration of refined products and petrochemical derivatives remains high, underpinning the essential role of the sector. Technological disruptions are playing a transformative role, with a strong emphasis on digitalization, advanced process control, and the adoption of cleaner production methods. Companies are investing heavily in developing catalysts that enhance refinery efficiency and reduce emissions, alongside innovations in petrochemical processes to produce specialized polymers and advanced materials. Consumer preferences are evolving, with a rising demand for cleaner-burning fuels, such as ultra-low sulfur diesel and gasoline, driven by government mandates and public environmental awareness. Petrochemical demand is shifting towards higher-value products used in sectors like automotive, construction, and consumer goods, reflecting a move up the value chain. Competitive dynamics are intensifying, with both domestic giants and international energy majors vying for market leadership. Strategic alliances, joint ventures, and targeted investments in capacity expansion and technological upgrades are defining the competitive landscape. The development of integrated refining and petrochemical complexes is a significant trend, allowing for greater operational synergy and product diversification, thereby optimizing feedstock utilization and maximizing profitability. The sector's resilience is further bolstered by government policies aimed at ensuring energy security and promoting self-sufficiency in key chemical feedstocks.

Dominant Regions & Segments in China Oil & Gas Downstream Industry

The China Oil & Gas Downstream Industry is dominated by a few key regions, with East China and North China emerging as the most significant hubs due to their extensive industrial infrastructure and proximity to major consumption centers. The Petrochemical Plants segment holds a prominent position, contributing significantly to the overall market value and growth.

- East China: This region benefits from a highly developed transportation network, including major ports and extensive pipeline infrastructure, facilitating the import of crude oil and the distribution of refined products and petrochemicals. Major economic zones and industrial clusters within East China, such as the Yangtze River Delta, are characterized by high demand for chemical feedstocks and finished products. Economic policies favoring industrial development and foreign investment have further cemented East China's dominance.

- North China: Home to some of the country's largest refining and petrochemical complexes, North China plays a crucial role in meeting national energy and material needs. Proximity to key oil-producing regions and a robust industrial base contribute to its strategic importance. Government initiatives to upgrade existing facilities and build new, world-scale plants are actively shaping the sector's growth here.

Within the Segments, Petrochemical Plants are experiencing accelerated growth. This dominance is driven by:

- Surging Demand for Derivatives: China's rapidly growing manufacturing sector, particularly in automotive, electronics, and construction, creates an insatiable appetite for a wide range of petrochemical derivatives like plastics, synthetic fibers, and specialty chemicals.

- Technological Advancements: Significant investments in advanced petrochemical technologies are enabling the production of higher-value, specialized products, moving China up the global chemical value chain. This includes innovations in polymers, elastomers, and fine chemicals.

- Integrated Refining and Petrochemical Complexes: The trend towards integrating refining and petrochemical operations allows for greater feedstock flexibility and cost efficiencies, making these complexes highly competitive and driving the growth of the petrochemical segment. The construction of new, state-of-the-art complexes is a recurring theme, often backed by billions in capital investment.

- Government Support for Industrial Upgrading: Policies aimed at fostering domestic production of essential chemicals and reducing reliance on imports are providing a strong impetus for the expansion and modernization of petrochemical facilities.

The Refinery segment, while foundational, is increasingly focused on upgrading to produce higher-quality fuels and to serve as feedstock providers for the burgeoning petrochemical industry.

China Oil & Gas Downstream Industry Product Innovations

Product innovations in the China Oil & Gas Downstream Industry are characterized by a dual focus on enhancing existing product performance and developing novel chemical compounds. Companies are actively launching advanced lubricants with extended drain intervals and improved fuel efficiency properties, catering to evolving automotive demands. In the petrochemical arena, there's a significant push towards high-performance polymers for lightweight automotive components, advanced packaging solutions, and sustainable materials. The competitive advantage lies in proprietary catalyst technologies that enable more efficient production of these specialty chemicals, coupled with a keen understanding of market needs for tailored solutions.

Report Scope & Segmentation Analysis

This report meticulously analyzes the China Oil & Gas Downstream Industry, segmented by Type: Refinery and Petrochemical Plants. The Refinery segment, projected to reach market sizes in the billions, is characterized by ongoing upgrades to meet stringent environmental standards and optimize feedstock conversion for higher-value products. The Petrochemical Plants segment is expected to witness robust growth in the coming years, with market sizes also in the billions, driven by escalating demand for plastics, synthetic fibers, and other chemical intermediates across various end-use industries. Competitive dynamics within each segment are shaped by technological capabilities, operational efficiencies, and strategic market positioning.

Key Drivers of China Oil & Gas Downstream Industry Growth

The growth of the China Oil & Gas Downstream Industry is underpinned by several critical factors. Technological advancements are paramount, with ongoing R&D in catalysis, process optimization, and digitalization enhancing efficiency and enabling the production of higher-value products. Economic growth in China remains a primary driver, fueling demand for fuels and petrochemicals across diverse sectors. Government policies supporting energy security, industrial modernization, and environmental protection also play a crucial role, encouraging investments in cleaner technologies and capacity expansions, often involving billions in planned capital expenditures.

Challenges in the China Oil & Gas Downstream Industry Sector

The China Oil & Gas Downstream Industry Sector faces several significant challenges. Regulatory hurdles, particularly concerning environmental compliance and carbon emissions, necessitate substantial investment in cleaner technologies and emission control systems, impacting operational costs. Supply chain volatility, including fluctuations in crude oil prices and disruptions in global logistics, can affect profitability and feedstock availability. Intensifying competitive pressures, both from domestic and international players, demand continuous innovation and efficiency improvements to maintain market share. The increasing global focus on energy transition and the rise of renewable energy sources also present a long-term strategic challenge, requiring adaptation and diversification.

Emerging Opportunities in China Oil & Gas Downstream Industry

Emerging opportunities within the China Oil & Gas Downstream Industry are centered on sustainable solutions and high-value product development. The increasing global and domestic emphasis on decarbonization presents opportunities for investments in green hydrogen production, carbon capture utilization and storage (CCUS) technologies, and the development of sustainable aviation fuels (SAFs) and biofuels. The growing demand for specialty chemicals and advanced materials, driven by sectors like electric vehicles, renewable energy infrastructure, and high-tech manufacturing, offers significant growth potential. Furthermore, the digital transformation of operations, through AI-driven process optimization and predictive maintenance, promises to unlock new levels of efficiency and cost savings, potentially impacting billions in operational expenditures.

Leading Players in the China Oil & Gas Downstream Industry Market

- Shell Energy (China) Limited

- Total SA

- Sinopec Shanghai Petrochemical Company Limited

- China National Petroleum Corporation

- Chevron Corporation

- PetroChina Company Limited

- SABIC (Saudi Basic Industries Corporation)

- Sinochem International Corporation

- China National Chemical Corporation (ChemChina)

- Huaqiang Chemical Group

Key Developments in China Oil & Gas Downstream Industry Industry

- The construction of new refineries and petrochemical plants: Numerous large-scale projects are underway or have been completed, significantly increasing production capacity. For example, the construction of a new xx billion petrochemical complex in Guangdong province was announced in 2023.

- The development of new technologies to improve operational efficiency: Companies are investing in advanced catalysis and digital twin technologies to optimize refinery operations and reduce energy consumption. Sinopec Shanghai Petrochemical Company Limited announced a xx% improvement in energy efficiency through a new digitalization initiative in 2022.

- The launch of new products and services: There's a growing emphasis on high-value petrochemicals and cleaner fuels. In 2024, PetroChina launched a new line of high-performance polymers for the automotive industry, representing a significant market expansion.

Future Outlook for China Oil & Gas Downstream Industry Market

The future outlook for the China Oil & Gas Downstream Industry Market remains robust, albeit with a transformative shift towards sustainability and higher value creation. Continued economic expansion, coupled with China's ambition to become a leader in advanced manufacturing, will sustain demand for refined products and petrochemicals. Strategic investments in green technologies, such as hydrogen production and CCUS, will become increasingly crucial for long-term growth and regulatory compliance. The market is expected to see a greater emphasis on specialty chemicals and advanced materials, moving beyond commodity products. Companies that successfully integrate digitalization and sustainability into their core strategies will be best positioned to thrive, capitalizing on evolving market needs and navigating the global energy transition, with potential market value reaching trillions in the coming decade.

China Oil & Gas Downstream Industry Segmentation

-

1. Type

- 1.1. Refinery

- 1.2. Petrochemical Plants

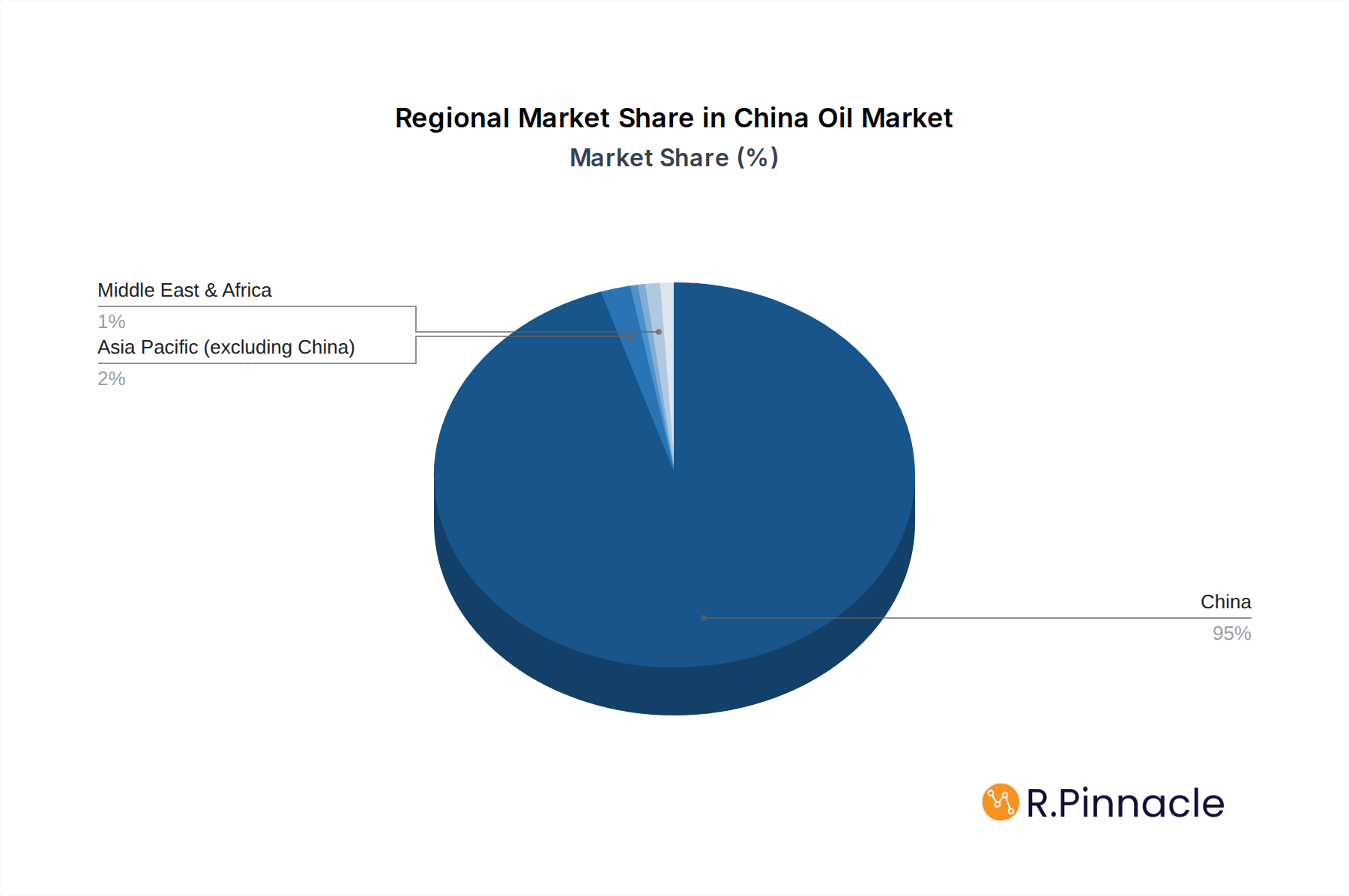

China Oil & Gas Downstream Industry Segmentation By Geography

- 1. China

China Oil & Gas Downstream Industry Regional Market Share

Geographic Coverage of China Oil & Gas Downstream Industry

China Oil & Gas Downstream Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Refinery

- 5.1.2. Petrochemical Plants

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. China

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. China Oil & Gas Downstream Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Refinery

- 6.1.2. Petrochemical Plants

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Shell Energy (China) Limited

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Total SA

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Sinopec Shanghai Petrochemical Company Limited

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 China National Petroleum Corporation

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Chevron Corporation*List Not Exhaustive

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 PetroChina Company Limited

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 SABIC (Saudi Basic Industries Corporation)

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Sinochem International Corporation

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 China National Chemical Corporation (ChemChina)

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Huaqiang Chemical Group

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Shell Energy (China) Limited

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: China Oil & Gas Downstream Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: China Oil & Gas Downstream Industry Share (%) by Company 2025

List of Tables

- Table 1: China Oil & Gas Downstream Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 2: China Oil & Gas Downstream Industry Volume K Tons Forecast, by Type 2020 & 2033

- Table 3: China Oil & Gas Downstream Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: China Oil & Gas Downstream Industry Volume K Tons Forecast, by Region 2020 & 2033

- Table 5: China Oil & Gas Downstream Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 6: China Oil & Gas Downstream Industry Volume K Tons Forecast, by Type 2020 & 2033

- Table 7: China Oil & Gas Downstream Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 8: China Oil & Gas Downstream Industry Volume K Tons Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the China Oil & Gas Downstream Industry?

The projected CAGR is approximately 5%.

2. Which companies are prominent players in the China Oil & Gas Downstream Industry?

Key companies in the market include Shell Energy (China) Limited, Total SA, Sinopec Shanghai Petrochemical Company Limited, China National Petroleum Corporation, Chevron Corporation*List Not Exhaustive, PetroChina Company Limited , SABIC (Saudi Basic Industries Corporation) , Sinochem International Corporation , China National Chemical Corporation (ChemChina) , Huaqiang Chemical Group.

3. What are the main segments of the China Oil & Gas Downstream Industry?

The market segments include Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 323.95 billion as of 2022.

5. What are some drivers contributing to market growth?

4.; Increasing Electricity Demand4.; Rsing Investments in the Coal Industry.

6. What are the notable trends driving market growth?

Refinery Capacity Expansion is Expected to Drive the Market.

7. Are there any restraints impacting market growth?

4.; Increasing Installation of Renewable Energy Sources.

8. Can you provide examples of recent developments in the market?

The construction of new refineries and petrochemical plants

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K Tons.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "China Oil & Gas Downstream Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the China Oil & Gas Downstream Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the China Oil & Gas Downstream Industry?

To stay informed about further developments, trends, and reports in the China Oil & Gas Downstream Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence