Key Insights

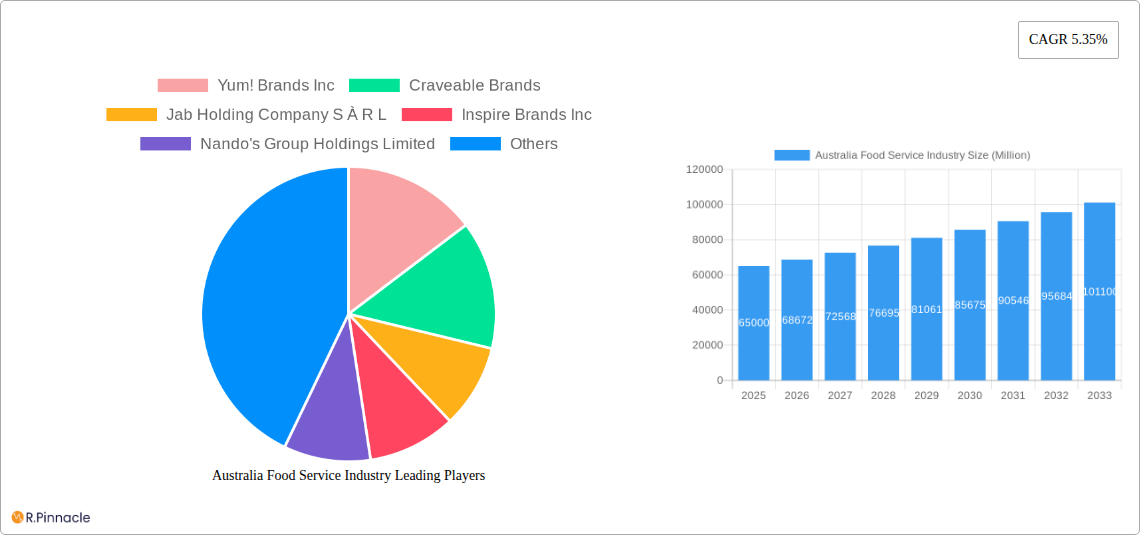

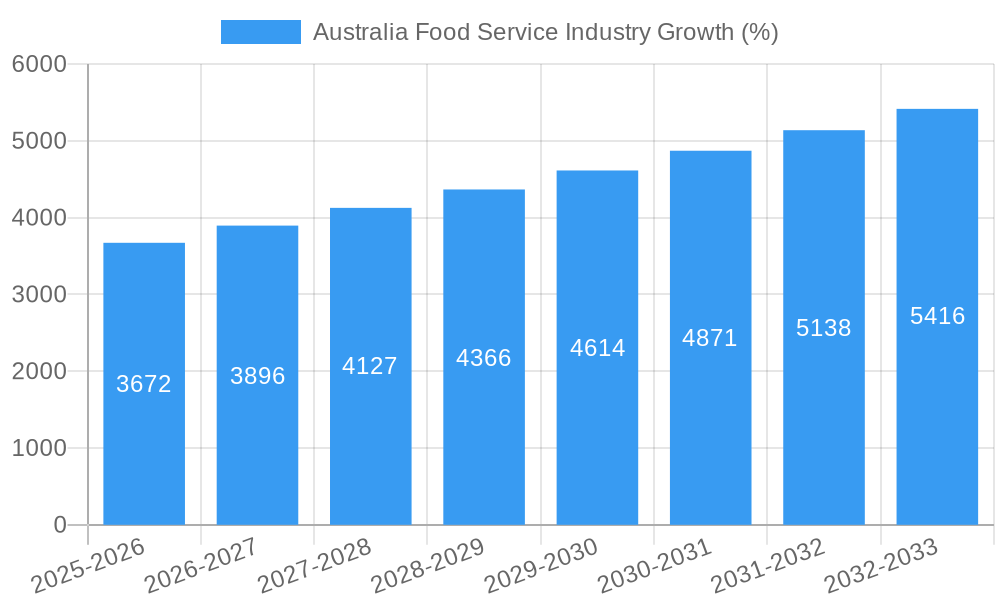

The Australian food service industry, exhibiting a Compound Annual Growth Rate (CAGR) of 5.35% between 2019 and 2024, is a dynamic and expanding sector. This growth is fueled by several key drivers: a rising population with increased disposable incomes leading to higher spending on dining out, a growing preference for convenience and diverse culinary experiences, and the continued expansion of both independent and chain outlets catering to various preferences. The industry is segmented by foodservice type (Cafes & Bars, Other QSR Cuisines), outlet type (Chained Outlets, Independent Outlets), and location (Leisure, Lodging, Retail, Standalone, Travel). While precise market size figures for specific years are not provided, we can infer substantial growth based on the CAGR. Assuming a 2024 market size of approximately $60 billion (an educated estimate considering Australia’s economy and the global food service market), the market would be projected to exceed $80 billion by 2033, continuing its upward trajectory. This expansion is further supported by ongoing trends such as the increasing popularity of delivery services, the integration of technology for improved efficiency and customer engagement, and a rising demand for sustainable and ethically sourced food options. However, challenges remain, including rising input costs, labor shortages, and the impact of economic fluctuations on consumer spending. This necessitates strategic adaptation and innovation within the sector to maintain and further accelerate growth.

The competitive landscape is intensely populated, encompassing both large multinational corporations like McDonald's and Yum! Brands, along with numerous smaller, independent operators. The success of individual companies will depend on their ability to effectively address consumer preferences, manage operational costs, and adapt to evolving market dynamics. The strong growth trajectory indicates significant opportunities for investment and expansion within the Australian food service industry, particularly in areas focused on catering to diverse culinary tastes, embracing technological advancements, and prioritizing sustainability initiatives. Further segmentation analysis, including detailed revenue breakdowns across different types of outlets and locations, would offer a more comprehensive understanding of the opportunities and challenges across this expansive market.

Australia Food Service Industry Market Report: 2019-2033

This comprehensive report provides an in-depth analysis of the Australian food service industry, offering invaluable insights for industry professionals, investors, and strategic planners. Covering the period 2019-2033, with a base year of 2025, this report forecasts robust growth and highlights key trends shaping the sector's future. The report meticulously examines market dynamics, competitive landscapes, and emerging opportunities, providing actionable intelligence to navigate this dynamic market. The total market size is estimated at AU$XX Billion in 2025.

Australia Food Service Industry Market Structure & Innovation Trends

The Australian food service industry is characterized by a diverse range of players, from multinational corporations to independent outlets. Market concentration is moderate, with several key players holding significant market share but not dominating the entire landscape. Yum! Brands Inc., McDonald's Corporation, and Domino's Pizza Enterprises Ltd. represent prominent examples of large chained players. However, a significant portion of the market comprises independent outlets and smaller chains, contributing to a relatively competitive environment. The estimated market share of the top 5 players in 2025 is approximately 35%, indicating significant opportunities for smaller players.

Innovation is driven by evolving consumer preferences, technological advancements, and increasing competition. Regulatory frameworks, including food safety regulations and labor laws, significantly impact operational costs and strategies. Product substitutes, such as meal kits and home-cooked meals, pose a competitive challenge, while demographic shifts influence demand patterns and menu offerings. M&A activities have been significant, with deal values exceeding AU$XX Billion in the past five years, reflecting consolidation and expansion strategies within the industry. Key M&A activities include:

- Retail Food Group's acquisition of several smaller cafe chains.

- Domino's Pizza Enterprises Ltd.'s expansion through strategic acquisitions.

- Consolidation within the pub and bar sector, leading to the formation of larger groups like PubCo Group.

Australia Food Service Industry Market Dynamics & Trends

The Australian food service industry exhibits strong growth potential, driven by several key factors. Rising disposable incomes, increasing urbanization, and changing lifestyles are fueling demand for convenience and out-of-home dining experiences. The market has demonstrated robust growth, with a Compound Annual Growth Rate (CAGR) of XX% during the historical period (2019-2024), and is projected to maintain a CAGR of XX% during the forecast period (2025-2033). Technological disruptions, including online ordering, delivery platforms, and digital marketing, are transforming the industry's operational efficiency and customer engagement strategies. Consumer preferences are evolving towards healthier options, personalized experiences, and sustainable practices, creating both challenges and opportunities for food service businesses. Competitive dynamics are intense, with businesses constantly innovating to attract and retain customers. Market penetration of online ordering platforms is estimated to be at XX% in 2025.

Dominant Regions & Segments in Australia Food Service Industry

The Australian food service industry shows significant variations across regions and segments. Key factors influencing dominance include population density, economic activity, tourism, and local preferences.

- Leading Region: New South Wales and Victoria consistently dominate the market due to higher population densities and strong economic activity.

- Leading Foodservice Type: QSR (Quick Service Restaurants) continues to be the largest segment, driven by convenience and affordability. Cafes and Bars also represent a substantial and growing segment, fuelled by lifestyle trends and social dynamics.

- Leading Outlet Type: Chained outlets hold a significant market share due to brand recognition and economies of scale. However, independent outlets also contribute substantially to the overall market size, appealing to consumers seeking unique culinary experiences.

- Leading Location: Standalone outlets are the most prevalent, followed by retail locations that benefit from high foot traffic. Travel locations and lodging segments are experiencing growth as travel recovers.

Key Drivers:

- Strong economic growth in major cities.

- Developed infrastructure supporting efficient logistics and operations.

- Supportive government policies promoting business development.

Australia Food Service Industry Product Innovations

Recent product innovations focus on healthier options, customized meals, and technological integrations. The introduction of plant-based alternatives, customizable bowls, and loyalty programs reflects a response to consumer demand for healthier choices and personalized experiences. Technological advancements in kitchen automation and online ordering systems are streamlining operations and enhancing customer service. These innovations are aimed at improving efficiency, customer engagement, and creating competitive advantages.

Report Scope & Segmentation Analysis

This report segments the Australian food service industry based on foodservice type (Cafes & Bars, Other QSR Cuisines), outlet type (Chained Outlets, Independent Outlets), and location (Leisure, Lodging, Retail, Standalone, Travel). Each segment displays unique growth projections, market sizes, and competitive dynamics. For example, the QSR segment is projected to grow at a higher rate than the cafes and bars segment due to its price point and convenience. Chained outlets generally benefit from economies of scale and brand recognition, while independent outlets cater to niche markets.

Key Drivers of Australia Food Service Industry Growth

Several factors fuel growth in the Australian food service industry. Economic growth boosts consumer spending on dining out. Technological advancements, such as online ordering and delivery platforms, expand market reach and improve efficiency. Favorable regulatory environments supporting business development further contribute to growth. The rise of innovative business models, including ghost kitchens and cloud kitchens, optimizes operations and reduces overhead costs.

Challenges in the Australia Food Service Industry Sector

The Australian food service industry faces challenges, including rising labor costs, supply chain disruptions impacting ingredient availability and pricing, and intense competition. Regulatory compliance costs can be significant, posing barriers to entry for smaller players. Fluctuations in commodity prices and the increasing cost of energy add to operational difficulties. These factors can significantly affect profit margins and competitiveness.

Emerging Opportunities in Australia Food Service Industry

Emerging opportunities include the expansion of specialized cuisines, the growth of the delivery market, and the adoption of sustainable practices. Health-conscious consumers drive the demand for organic and plant-based options. Technological innovations, including AI-powered menu recommendations and personalized customer experiences, create significant opportunities for differentiation.

Leading Players in the Australia Food Service Industry Market

- Yum! Brands Inc.

- Craveable Brands

- Jab Holding Company S À R L

- Inspire Brands Inc.

- Nando's Group Holdings Limited

- Doctor's Associate Inc

- PubCo Group

- Zambrero Pty Lt

- Retail Food Group

- Domino's Pizza Enterprises Ltd

- Guzman Y Gomez Restaurant Group Pty Limited

- Starbucks Corporation

- Pacific Hunter Group Pty Ltd

- Ribs and Burgers

- McDonald's Corporation

- Competitive Foods Australia

- Bloomin' Brands Inc.

Key Developments in Australia Food Service Industry Industry

- December 2022: KFC Australia partnered with Wing for drone delivery services, enhancing customer convenience.

- January 2023: Zambrero announced a partnership with Cronulla Sharks and SurfAid, increasing brand visibility.

- April 2023: Subway launched the Bizarre Creme Egg Sandwich, adding novelty to its menu.

Future Outlook for Australia Food Service Industry Market

The Australian food service industry is poised for continued growth, driven by evolving consumer preferences and technological advancements. The focus on health, sustainability, and personalized experiences will shape future market trends. Strategic partnerships, technological integration, and innovative business models will be crucial for success in this dynamic market. The industry's future potential remains significant, offering substantial opportunities for both established and emerging players.

Australia Food Service Industry Segmentation

-

1. Foodservice Type

-

1.1. Cafes & Bars

-

1.1.1. By Cuisine

- 1.1.1.1. Bars & Pubs

- 1.1.1.2. Juice/Smoothie/Desserts Bars

- 1.1.1.3. Specialist Coffee & Tea Shops

-

1.1.1. By Cuisine

- 1.2. Cloud Kitchen

-

1.3. Full Service Restaurants

- 1.3.1. Asian

- 1.3.2. European

- 1.3.3. Latin American

- 1.3.4. Middle Eastern

- 1.3.5. North American

- 1.3.6. Other FSR Cuisines

-

1.4. Quick Service Restaurants

- 1.4.1. Bakeries

- 1.4.2. Burger

- 1.4.3. Ice Cream

- 1.4.4. Meat-based Cuisines

- 1.4.5. Pizza

- 1.4.6. Other QSR Cuisines

-

1.1. Cafes & Bars

-

2. Outlet

- 2.1. Chained Outlets

- 2.2. Independent Outlets

-

3. Location

- 3.1. Leisure

- 3.2. Lodging

- 3.3. Retail

- 3.4. Standalone

- 3.5. Travel

Australia Food Service Industry Segmentation By Geography

- 1. Australia

Australia Food Service Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 5.35% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Growing Inclination Towards Vegan/Plant-based Protein Sources; Increasing Demand for Functional Protein Beverages

- 3.3. Market Restrains

- 3.3.1. Competition from Substitute Products

- 3.4. Market Trends

- 3.4.1. The number if restaurant visits per month grew as a result of the national spread of fast food companies.

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Australia Food Service Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Foodservice Type

- 5.1.1. Cafes & Bars

- 5.1.1.1. By Cuisine

- 5.1.1.1.1. Bars & Pubs

- 5.1.1.1.2. Juice/Smoothie/Desserts Bars

- 5.1.1.1.3. Specialist Coffee & Tea Shops

- 5.1.1.1. By Cuisine

- 5.1.2. Cloud Kitchen

- 5.1.3. Full Service Restaurants

- 5.1.3.1. Asian

- 5.1.3.2. European

- 5.1.3.3. Latin American

- 5.1.3.4. Middle Eastern

- 5.1.3.5. North American

- 5.1.3.6. Other FSR Cuisines

- 5.1.4. Quick Service Restaurants

- 5.1.4.1. Bakeries

- 5.1.4.2. Burger

- 5.1.4.3. Ice Cream

- 5.1.4.4. Meat-based Cuisines

- 5.1.4.5. Pizza

- 5.1.4.6. Other QSR Cuisines

- 5.1.1. Cafes & Bars

- 5.2. Market Analysis, Insights and Forecast - by Outlet

- 5.2.1. Chained Outlets

- 5.2.2. Independent Outlets

- 5.3. Market Analysis, Insights and Forecast - by Location

- 5.3.1. Leisure

- 5.3.2. Lodging

- 5.3.3. Retail

- 5.3.4. Standalone

- 5.3.5. Travel

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Australia

- 5.1. Market Analysis, Insights and Forecast - by Foodservice Type

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2024

- 6.2. Company Profiles

- 6.2.1 Yum! Brands Inc

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 Craveable Brands

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 Jab Holding Company S À R L

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Inspire Brands Inc

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 Nando's Group Holdings Limited

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 Doctor's Associate Inc

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 PubCo Group

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 Zambrero Pty Lt

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 Retail Food Group

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 Domino's Pizza Enterprises Ltd

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.11 Guzman Y Gomez Restaurant Group Pty Limited

- 6.2.11.1. Overview

- 6.2.11.2. Products

- 6.2.11.3. SWOT Analysis

- 6.2.11.4. Recent Developments

- 6.2.11.5. Financials (Based on Availability)

- 6.2.12 Starbucks Corporation

- 6.2.12.1. Overview

- 6.2.12.2. Products

- 6.2.12.3. SWOT Analysis

- 6.2.12.4. Recent Developments

- 6.2.12.5. Financials (Based on Availability)

- 6.2.13 Pacific Hunter Group Pty Ltd

- 6.2.13.1. Overview

- 6.2.13.2. Products

- 6.2.13.3. SWOT Analysis

- 6.2.13.4. Recent Developments

- 6.2.13.5. Financials (Based on Availability)

- 6.2.14 Ribs and Burgers

- 6.2.14.1. Overview

- 6.2.14.2. Products

- 6.2.14.3. SWOT Analysis

- 6.2.14.4. Recent Developments

- 6.2.14.5. Financials (Based on Availability)

- 6.2.15 McDonald's Corporation

- 6.2.15.1. Overview

- 6.2.15.2. Products

- 6.2.15.3. SWOT Analysis

- 6.2.15.4. Recent Developments

- 6.2.15.5. Financials (Based on Availability)

- 6.2.16 Competitive Foods Australia

- 6.2.16.1. Overview

- 6.2.16.2. Products

- 6.2.16.3. SWOT Analysis

- 6.2.16.4. Recent Developments

- 6.2.16.5. Financials (Based on Availability)

- 6.2.17 Bloomin' Brands Inc

- 6.2.17.1. Overview

- 6.2.17.2. Products

- 6.2.17.3. SWOT Analysis

- 6.2.17.4. Recent Developments

- 6.2.17.5. Financials (Based on Availability)

- 6.2.1 Yum! Brands Inc

List of Figures

- Figure 1: Australia Food Service Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Australia Food Service Industry Share (%) by Company 2024

List of Tables

- Table 1: Australia Food Service Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Australia Food Service Industry Revenue Million Forecast, by Foodservice Type 2019 & 2032

- Table 3: Australia Food Service Industry Revenue Million Forecast, by Outlet 2019 & 2032

- Table 4: Australia Food Service Industry Revenue Million Forecast, by Location 2019 & 2032

- Table 5: Australia Food Service Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 6: Australia Food Service Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 7: Australia Food Service Industry Revenue Million Forecast, by Foodservice Type 2019 & 2032

- Table 8: Australia Food Service Industry Revenue Million Forecast, by Outlet 2019 & 2032

- Table 9: Australia Food Service Industry Revenue Million Forecast, by Location 2019 & 2032

- Table 10: Australia Food Service Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Australia Food Service Industry?

The projected CAGR is approximately 5.35%.

2. Which companies are prominent players in the Australia Food Service Industry?

Key companies in the market include Yum! Brands Inc, Craveable Brands, Jab Holding Company S À R L, Inspire Brands Inc, Nando's Group Holdings Limited, Doctor's Associate Inc, PubCo Group, Zambrero Pty Lt, Retail Food Group, Domino's Pizza Enterprises Ltd, Guzman Y Gomez Restaurant Group Pty Limited, Starbucks Corporation, Pacific Hunter Group Pty Ltd, Ribs and Burgers, McDonald's Corporation, Competitive Foods Australia, Bloomin' Brands Inc.

3. What are the main segments of the Australia Food Service Industry?

The market segments include Foodservice Type, Outlet, Location.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Growing Inclination Towards Vegan/Plant-based Protein Sources; Increasing Demand for Functional Protein Beverages.

6. What are the notable trends driving market growth?

The number if restaurant visits per month grew as a result of the national spread of fast food companies..

7. Are there any restraints impacting market growth?

Competition from Substitute Products.

8. Can you provide examples of recent developments in the market?

April 2023: Subway added the latest item in its subs range, the Bizarre Creme Egg Sandwich, a combination of chocolate creme egg stuffed in Italian bread.January 2023: Zambrero announced its partnership with Cronulla Sharks and SurfAid for 2023.December 2022: KFC Australia teamed up with drone service provider, Wing, to pilot a delivery service of hot and fresh menu items in Australia to provide more convenience to customers.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Australia Food Service Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Australia Food Service Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Australia Food Service Industry?

To stay informed about further developments, trends, and reports in the Australia Food Service Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence