Key Insights

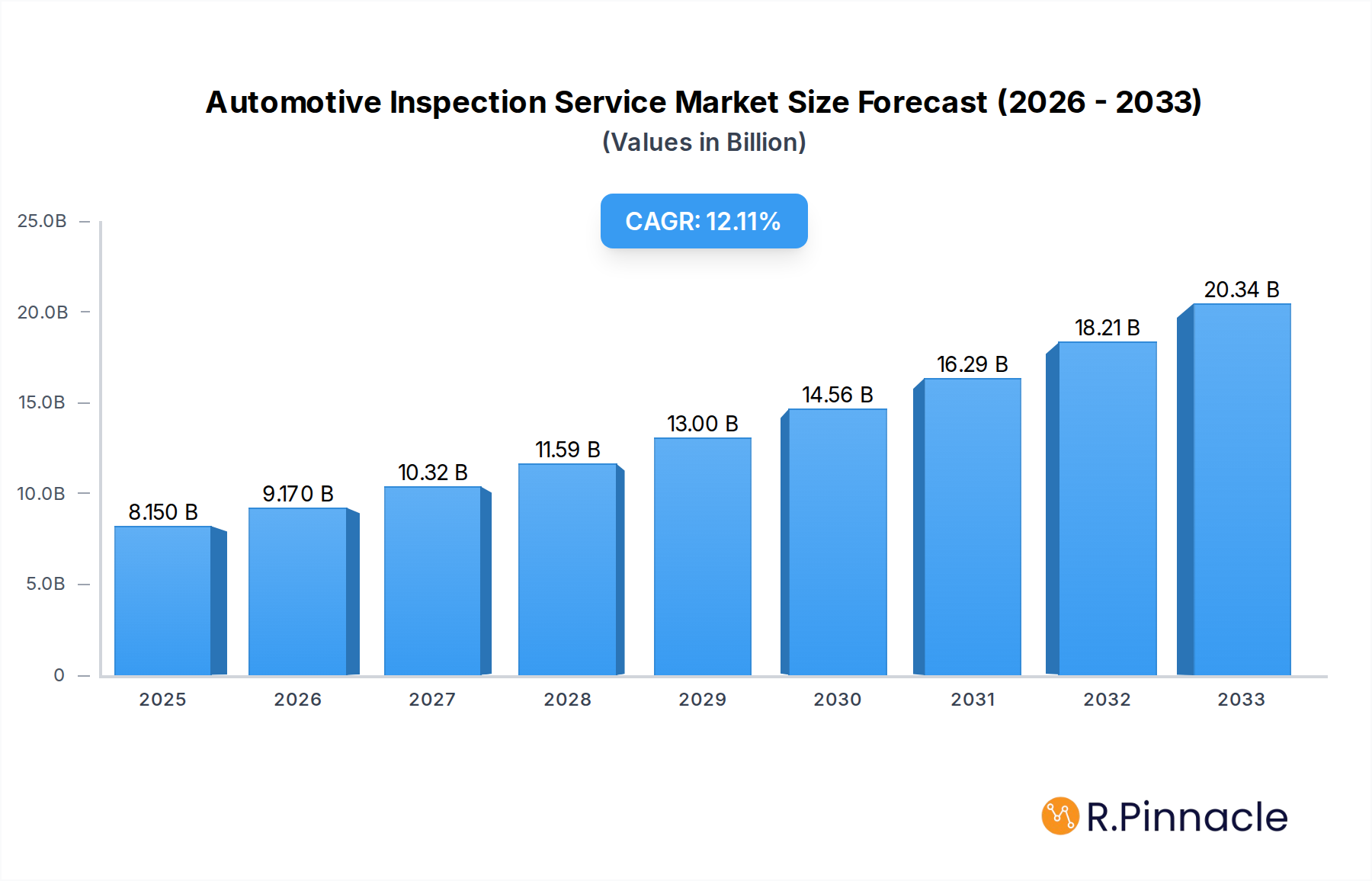

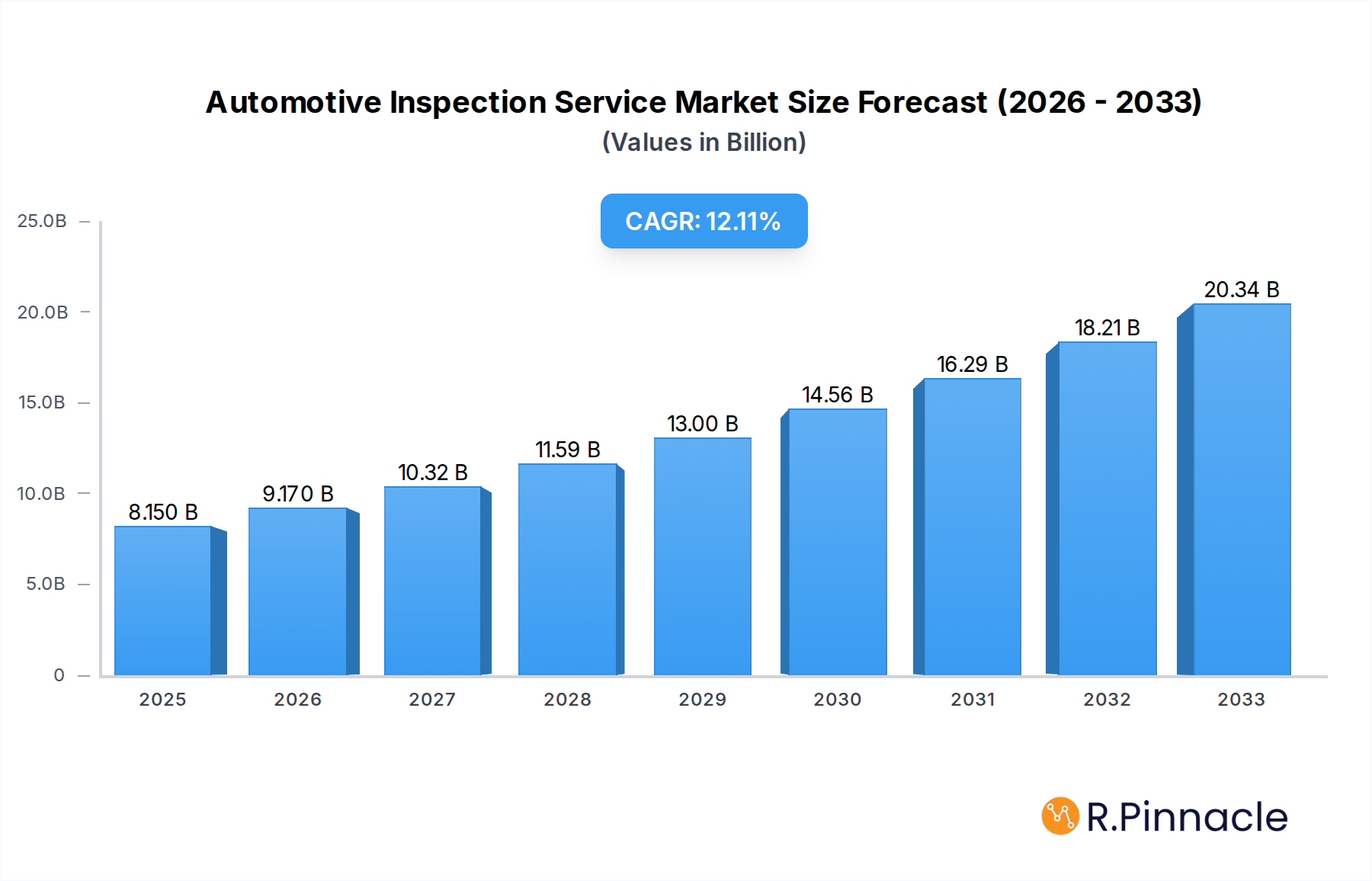

The global Automotive Inspection Service market is poised for substantial growth, projected to reach $8.15 billion by 2025, driven by a robust CAGR of 12.08% through 2033. This expansion is fueled by a confluence of factors including increasingly stringent vehicle safety and emissions regulations worldwide, the growing complexity of automotive technology demanding specialized testing, and a heightened consumer awareness regarding vehicle reliability and environmental impact. The burgeoning demand for electric and autonomous vehicles, with their unique testing requirements, further acts as a significant catalyst. Moreover, the persistent need for pre-purchase inspections, routine maintenance checks, and regulatory compliance for both passenger cars and commercial vehicles underpins the market's sustained upward trajectory. Leading the charge in market dynamics are key players like DEKRA, TUV Group, and Bureau Veritas, actively shaping the competitive landscape through strategic acquisitions, technological innovations, and expanded service offerings. The market's segmentation into Vehicle Testing and Vehicle Check, across both Passenger Car and Commercial Vehicle applications, highlights the diverse service needs being addressed.

Automotive Inspection Service Market Size (In Billion)

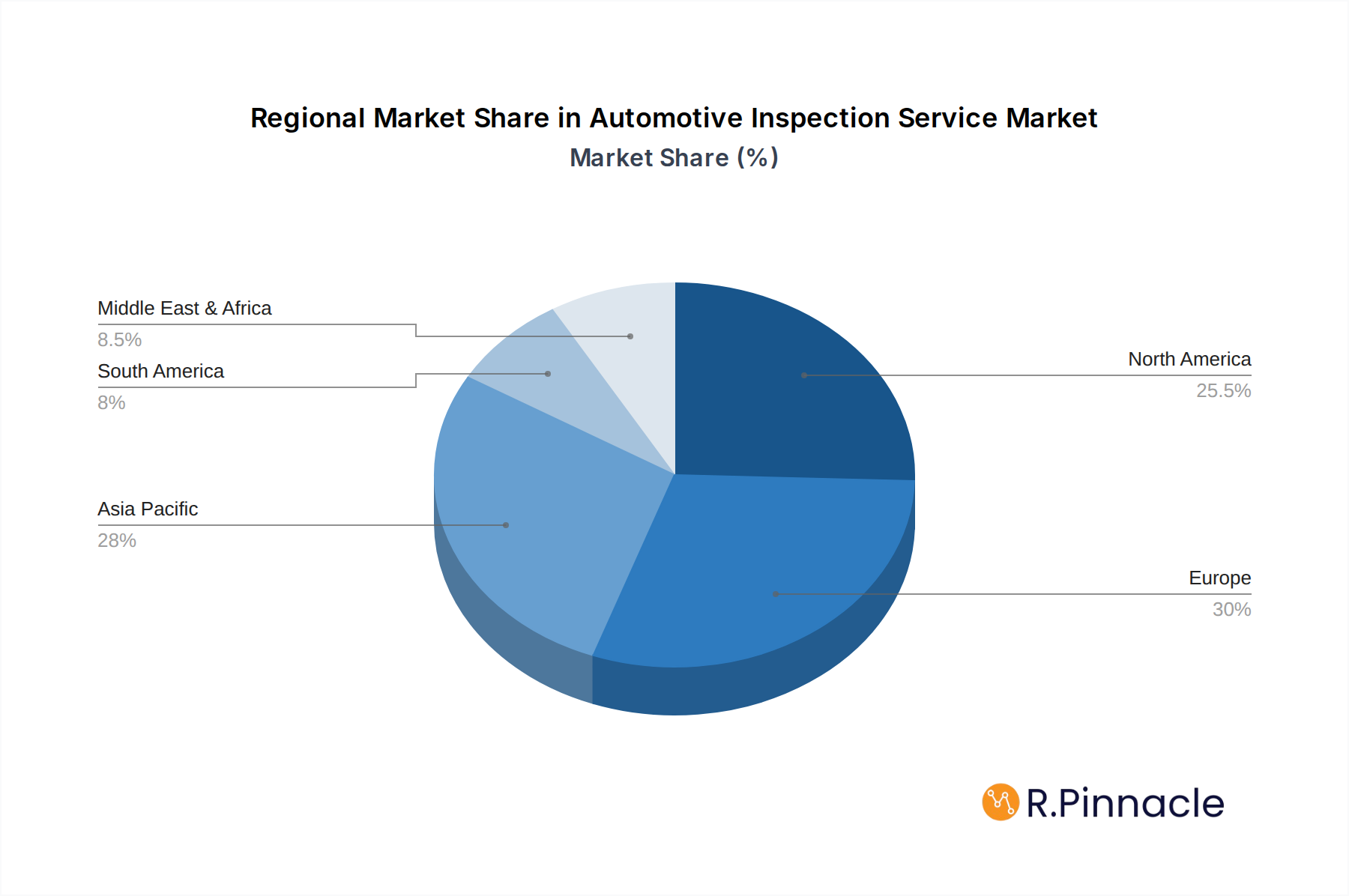

Looking ahead, the automotive inspection service sector is characterized by several key trends. The integration of advanced digital technologies, such as AI-powered diagnostics and remote inspection capabilities, is revolutionizing efficiency and accuracy. Furthermore, the increasing emphasis on sustainability and the circular economy is driving demand for services focused on extending vehicle lifespan and promoting eco-friendly practices. Geographically, North America and Europe are established leaders, but the Asia Pacific region, particularly China and India, is emerging as a high-growth area due to rapid vehicle market expansion and evolving regulatory frameworks. While the market benefits from strong drivers, potential restraints include the high initial investment required for sophisticated testing equipment and the fluctuating economic conditions that could impact consumer spending on non-essential vehicle services. Despite these challenges, the overarching trend points towards a dynamic and expanding market, crucial for ensuring vehicle safety, regulatory compliance, and environmental responsibility.

Automotive Inspection Service Company Market Share

Automotive Inspection Service Market: Comprehensive Analysis and Future Projections (2019-2033)

This in-depth report offers a definitive analysis of the global Automotive Inspection Service Market, providing critical insights for industry stakeholders. Covering the historical period from 2019 to 2024, the base year of 2025, and extending through an extensive forecast period of 2025–2033, this research meticulously examines market structures, dynamics, dominant regions, and cutting-edge innovations. Leveraging high-ranking SEO keywords such as "automotive inspection," "vehicle testing," "vehicle check," and "automotive compliance," this report is engineered to maximize search visibility and deliver actionable intelligence to professionals in the automotive sector, including those at DEKRA, TUV Group, Bureau Veritas, Applus Services, SGS Group, Intertek Group, NTS, ATS Lab, Intertek, UL, MET Labs, Tata Elxsi, Mobile Power Solutions, Chroma ATE, and Element.

Automotive Inspection Service Market Structure & Innovation Trends

The Automotive Inspection Service Market exhibits a moderate to high concentration, with major global players like DEKRA and TUV Group dominating significant market shares, estimated at over 25 billion USD collectively. Innovation is primarily driven by the increasing complexity of vehicle electronics, the rise of autonomous driving technologies, and stringent emission control regulations. These factors necessitate advanced diagnostic tools and specialized inspection procedures, pushing service providers to invest billions in R&D. Regulatory frameworks, such as Euro VI emissions standards and NHTSA safety mandates, continue to shape the market landscape, ensuring compliance and driving demand for rigorous vehicle checks. Product substitutes, while present in the form of DIY diagnostic tools, lack the comprehensive scope and certified validation offered by professional automotive inspection services, limiting their impact on the overall market. End-user demographics span both individual vehicle owners seeking pre-purchase inspections and fleet operators prioritizing safety and operational efficiency, representing a market valued in the hundreds of billions. Mergers and acquisitions (M&A) activity remains robust, with recent deals totaling over 10 billion USD as larger entities seek to expand their service portfolios and geographic reach.

Automotive Inspection Service Market Dynamics & Trends

The Automotive Inspection Service Market is poised for substantial growth, projected to expand at a Compound Annual Growth Rate (CAGR) of approximately 7.5% from 2025 to 2033, reaching a colossal market size exceeding 800 billion USD. This robust expansion is fueled by a confluence of escalating global vehicle parc, increasingly stringent safety and environmental regulations, and a heightened consumer awareness regarding vehicle reliability and performance. Technological disruptions are at the forefront, with the integration of Artificial Intelligence (AI) and Machine Learning (ML) in diagnostic equipment revolutionizing the speed and accuracy of vehicle checks. The proliferation of Electric Vehicles (EVs) and the anticipated surge in connected and autonomous vehicles introduce new complexities, demanding specialized inspection protocols and recalibrations, further solidifying the need for expert automotive inspection services. Consumer preferences are shifting towards proactive maintenance and preventative inspections, driven by the desire to prolong vehicle lifespan and avoid costly repairs. This trend is amplified by the increasing cost of vehicles and the growing emphasis on resale value. Competitive dynamics are characterized by a blend of established global players and regional specialists, all vying for market share through service differentiation, technological adoption, and strategic partnerships. The market penetration of specialized automotive inspection services is expected to climb significantly, especially in developed economies with mature automotive sectors and a strong regulatory enforcement apparatus. The ongoing transition towards sustainable mobility solutions also presents unique inspection challenges and opportunities, including battery health assessments and emissions testing for alternative powertrains, contributing to the market's dynamic evolution. The estimated market value in the base year 2025 is projected to be around 500 billion USD.

Dominant Regions & Segments in Automotive Inspection Service

North America and Europe currently stand as the dominant regions in the Automotive Inspection Service Market, driven by well-established automotive industries, stringent regulatory oversight, and high consumer spending power. In North America, the Passenger Car segment, representing over 60% of the market, is a primary driver, fueled by a vast existing vehicle fleet and a strong emphasis on consumer safety. Key drivers include economic policies that support vehicle ownership, robust infrastructure for automotive repair and maintenance, and stringent federal and state regulations mandating regular vehicle inspections, particularly for emissions and safety. The United States alone accounts for a significant portion of this regional dominance, with projected market revenues in the hundreds of billions.

In Europe, the Vehicle Testing type, encompassing mandatory technical inspections, holds substantial sway. Stringent EU directives on roadworthiness and emissions standards, such as those related to CO2 emissions and particulate matter, ensure consistent demand for these services. The presence of major automotive manufacturers and a highly regulated aftermarket further bolsters the market. Economic policies in Europe, aimed at promoting cleaner transportation and ensuring road safety, directly translate into a continuous need for comprehensive vehicle inspections.

The Commercial Vehicle segment, while smaller in volume than passenger cars, represents a high-value niche due to the critical nature of fleet operations and the severe economic repercussions of vehicle downtime. Countries with substantial logistics and transportation industries, such as Germany and France in Europe, and the United States in North America, exhibit higher demand for commercial vehicle inspections. The implementation of specific regulations for commercial vehicle safety and emissions, alongside advanced fleet management technologies, are key growth accelerators in this segment. The overall market segmentation analysis indicates a continued dominance of Passenger Car and Vehicle Testing types, with Commercial Vehicle inspections showing strong growth potential driven by fleet modernization and regulatory compliance.

Automotive Inspection Service Product Innovations

Product innovations in the Automotive Inspection Service Market are rapidly evolving, focusing on enhanced diagnostic capabilities and streamlined workflows. Advanced OBD-II scanners with cloud connectivity, capable of accessing real-time vehicle data and manufacturer-specific diagnostic trouble codes (DTCs), are becoming standard. The integration of AI-powered visual inspection tools, utilizing high-resolution cameras and machine learning algorithms to detect subtle damages or wear on vehicle components, offers a significant competitive advantage. Furthermore, specialized testing equipment for Electric Vehicles (EVs), such as battery health analyzers and charging system testers, are gaining traction. These innovations translate into faster, more accurate, and more comprehensive inspections, improving customer satisfaction and operational efficiency for service providers, contributing to a market valued in the tens of billions.

Report Scope & Segmentation Analysis

This report meticulously segments the Automotive Inspection Service Market across key parameters. The Passenger Car application segment is projected to maintain its leadership, driven by the sheer volume of vehicles, with an estimated market share exceeding 65% and a projected growth rate of 7% annually, reaching hundreds of billions by 2033. The Commercial Vehicle segment, while smaller, is expected to witness robust growth at a CAGR of 8.5%, driven by fleet modernization and increasing regulatory compliance, with a projected market size in the tens of billions. In terms of service type, Vehicle Testing, encompassing statutory inspections and diagnostics, is anticipated to account for over 55% of the market, with a steady growth trajectory aligned with regulatory mandates. Vehicle Check, covering pre-purchase inspections and routine maintenance checks, will represent a significant portion, demonstrating strong growth due to increasing consumer awareness and the desire to maintain vehicle value, with a projected market size in the hundreds of billions.

Key Drivers of Automotive Inspection Service Growth

Several pivotal factors are propelling the growth of the Automotive Inspection Service Market. Technological advancements, including the adoption of AI in diagnostics and the increasing complexity of modern vehicles with advanced driver-assistance systems (ADAS) and electrification, necessitate specialized inspection expertise. Economic factors such as rising disposable incomes in emerging economies and the increasing cost of new vehicles are encouraging consumers to maintain their existing vehicles longer, thereby boosting demand for inspection and maintenance services. Regulatory mandates are a significant catalyst; governments worldwide are continuously strengthening vehicle safety and environmental regulations, making regular inspections a legal requirement. For instance, evolving emissions standards and enhanced safety protocols for autonomous features directly drive the need for compliant inspection services, contributing billions to the market.

Challenges in the Automotive Inspection Service Sector

Despite the promising growth trajectory, the Automotive Inspection Service Market faces several significant challenges. Regulatory hurdles can be complex and vary significantly across different regions and countries, requiring service providers to navigate a labyrinth of compliance requirements. Supply chain disruptions, particularly concerning specialized diagnostic equipment and spare parts, can impact operational efficiency and lead to delays in service delivery. Intense competitive pressure from both established global players and a growing number of independent workshops puts pressure on pricing and margins. Furthermore, the lack of standardized training and certification for technicians handling advanced vehicle technologies, such as EVs and ADAS, presents a significant barrier to consistent service quality and market expansion, potentially costing billions in lost opportunities.

Emerging Opportunities in Automotive Inspection Service

The Automotive Inspection Service Market is ripe with emerging opportunities. The rapid expansion of the Electric Vehicle (EV) market presents a substantial new avenue for inspection services, focusing on battery health diagnostics, charging infrastructure checks, and specialized powertrain inspections. The increasing sophistication of Autonomous Driving Systems (ADAS) creates a demand for specialized calibration and validation services post-inspection. Furthermore, the growing trend of vehicle subscriptions and mobility-as-a-service (MaaS) models necessitates robust fleet management and regular, reliable inspections to ensure optimal vehicle uptime and safety. The development of predictive maintenance solutions, leveraging AI and IoT data from vehicles, offers an opportunity for proactive service offerings and enhanced customer retention, promising billions in future revenue.

Leading Players in the Automotive Inspection Service Market

- DEKRA

- TUV Group

- Bureau Veritas

- Applus Services

- SGS Group

- Intertek Group

- NTS

- ATS Lab

- Intertek

- UL

- MET Labs

- Tata Elxsi

- Mobile Power Solutions

- Chroma ATE

- Element

Key Developments in Automotive Inspection Service Industry

- 2023 Q4: DEKRA acquired a significant stake in a leading EV charging infrastructure inspection company, expanding its service portfolio for the electric mobility sector.

- 2023 Q3: TUV Group launched an AI-powered diagnostic platform for advanced driver-assistance systems (ADAS) calibration, enhancing inspection accuracy.

- 2023 Q2: Bureau Veritas partnered with a major automotive manufacturer to develop standardized inspection protocols for connected vehicles.

- 2023 Q1: Applus Services acquired a specialized automotive testing firm focusing on cybersecurity for connected cars, addressing a growing industry concern.

- 2022 Q4: SGS Group expanded its global network of automotive testing facilities, with a particular focus on emerging markets in Asia.

- 2022 Q3: Intertek Group introduced a new service line for battery health diagnostics for electric vehicles, anticipating a surge in demand.

- 2022 Q2: NTS introduced advanced functional safety testing services for automotive electronics, crucial for autonomous vehicle development.

- 2022 Q1: ATS Lab expanded its emissions testing capabilities to include the latest Euro VII standards.

- 2021 Q4: UL announced new certification programs for automotive cybersecurity, a critical aspect of vehicle safety.

- 2021 Q3: MET Labs invested heavily in its electromagnetic compatibility (EMC) testing capabilities for automotive components.

- 2021 Q2: Tata Elxsi showcased its innovative solutions for in-vehicle infotainment system testing.

- 2021 Q1: Mobile Power Solutions launched specialized inspection services for commercial vehicle fleets, focusing on efficiency and compliance.

- 2020 Q4: Chroma ATE introduced new dynamic testing solutions for electric vehicle powertrains.

- 2020 Q3: Element acquired a niche automotive homologation service provider, broadening its regulatory compliance offerings.

Future Outlook for Automotive Inspection Service Market

The future outlook for the Automotive Inspection Service Market is exceptionally positive, with sustained growth projected through 2033 and beyond. The escalating complexity of automotive technology, particularly the pervasive shift towards electrification and autonomous driving, will continue to drive demand for specialized and highly skilled inspection services. Anticipated advancements in AI, IoT, and data analytics will further revolutionize the sector, enabling more predictive and proactive maintenance strategies. Investments in infrastructure for EV charging and servicing, coupled with stricter global safety and environmental regulations, will act as significant growth accelerators. Strategic partnerships and potential consolidation among key players will likely shape the competitive landscape, fostering innovation and expanding service offerings to meet evolving market needs, promising a market value in the trillions.

Automotive Inspection Service Segmentation

-

1. Application

- 1.1. Passenger Car

- 1.2. Commercial Vehicle

-

2. Type

- 2.1. Vehicle Testing

- 2.2. Vehicle Check

Automotive Inspection Service Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Automotive Inspection Service Regional Market Share

Geographic Coverage of Automotive Inspection Service

Automotive Inspection Service REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 12.08% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Automotive Inspection Service Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Passenger Car

- 5.1.2. Commercial Vehicle

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Vehicle Testing

- 5.2.2. Vehicle Check

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Automotive Inspection Service Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Passenger Car

- 6.1.2. Commercial Vehicle

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Vehicle Testing

- 6.2.2. Vehicle Check

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Automotive Inspection Service Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Passenger Car

- 7.1.2. Commercial Vehicle

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Vehicle Testing

- 7.2.2. Vehicle Check

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Automotive Inspection Service Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Passenger Car

- 8.1.2. Commercial Vehicle

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Vehicle Testing

- 8.2.2. Vehicle Check

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Automotive Inspection Service Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Passenger Car

- 9.1.2. Commercial Vehicle

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Vehicle Testing

- 9.2.2. Vehicle Check

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Automotive Inspection Service Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Passenger Car

- 10.1.2. Commercial Vehicle

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Vehicle Testing

- 10.2.2. Vehicle Check

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 DEKRA

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 TUV Group

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Bureau Veritas

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Applus Services

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 SGS Group

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Intertek Group

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 NTS

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 ATS Lab

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Intertek

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 UL

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 MET Labs

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Tata Elxsi

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Mobile Power Solutions

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Chroma ATE

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Element

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.1 DEKRA

List of Figures

- Figure 1: Global Automotive Inspection Service Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Automotive Inspection Service Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Automotive Inspection Service Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Automotive Inspection Service Revenue (billion), by Type 2025 & 2033

- Figure 5: North America Automotive Inspection Service Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Automotive Inspection Service Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Automotive Inspection Service Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Automotive Inspection Service Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Automotive Inspection Service Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Automotive Inspection Service Revenue (billion), by Type 2025 & 2033

- Figure 11: South America Automotive Inspection Service Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Automotive Inspection Service Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Automotive Inspection Service Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Automotive Inspection Service Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Automotive Inspection Service Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Automotive Inspection Service Revenue (billion), by Type 2025 & 2033

- Figure 17: Europe Automotive Inspection Service Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Automotive Inspection Service Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Automotive Inspection Service Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Automotive Inspection Service Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Automotive Inspection Service Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Automotive Inspection Service Revenue (billion), by Type 2025 & 2033

- Figure 23: Middle East & Africa Automotive Inspection Service Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Automotive Inspection Service Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Automotive Inspection Service Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Automotive Inspection Service Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Automotive Inspection Service Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Automotive Inspection Service Revenue (billion), by Type 2025 & 2033

- Figure 29: Asia Pacific Automotive Inspection Service Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Automotive Inspection Service Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Automotive Inspection Service Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Automotive Inspection Service Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Automotive Inspection Service Revenue billion Forecast, by Type 2020 & 2033

- Table 3: Global Automotive Inspection Service Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Automotive Inspection Service Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Automotive Inspection Service Revenue billion Forecast, by Type 2020 & 2033

- Table 6: Global Automotive Inspection Service Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Automotive Inspection Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Automotive Inspection Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Automotive Inspection Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Automotive Inspection Service Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Automotive Inspection Service Revenue billion Forecast, by Type 2020 & 2033

- Table 12: Global Automotive Inspection Service Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Automotive Inspection Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Automotive Inspection Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Automotive Inspection Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Automotive Inspection Service Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Automotive Inspection Service Revenue billion Forecast, by Type 2020 & 2033

- Table 18: Global Automotive Inspection Service Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Automotive Inspection Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Automotive Inspection Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Automotive Inspection Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Automotive Inspection Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Automotive Inspection Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Automotive Inspection Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Automotive Inspection Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Automotive Inspection Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Automotive Inspection Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Automotive Inspection Service Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Automotive Inspection Service Revenue billion Forecast, by Type 2020 & 2033

- Table 30: Global Automotive Inspection Service Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Automotive Inspection Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Automotive Inspection Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Automotive Inspection Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Automotive Inspection Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Automotive Inspection Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Automotive Inspection Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Automotive Inspection Service Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Automotive Inspection Service Revenue billion Forecast, by Type 2020 & 2033

- Table 39: Global Automotive Inspection Service Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Automotive Inspection Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Automotive Inspection Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Automotive Inspection Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Automotive Inspection Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Automotive Inspection Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Automotive Inspection Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Automotive Inspection Service Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Automotive Inspection Service?

The projected CAGR is approximately 12.08%.

2. Which companies are prominent players in the Automotive Inspection Service?

Key companies in the market include DEKRA, TUV Group, Bureau Veritas, Applus Services, SGS Group, Intertek Group, NTS, ATS Lab, Intertek, UL, MET Labs, Tata Elxsi, Mobile Power Solutions, Chroma ATE, Element.

3. What are the main segments of the Automotive Inspection Service?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 8.15 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Automotive Inspection Service," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Automotive Inspection Service report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Automotive Inspection Service?

To stay informed about further developments, trends, and reports in the Automotive Inspection Service, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence