Key Insights

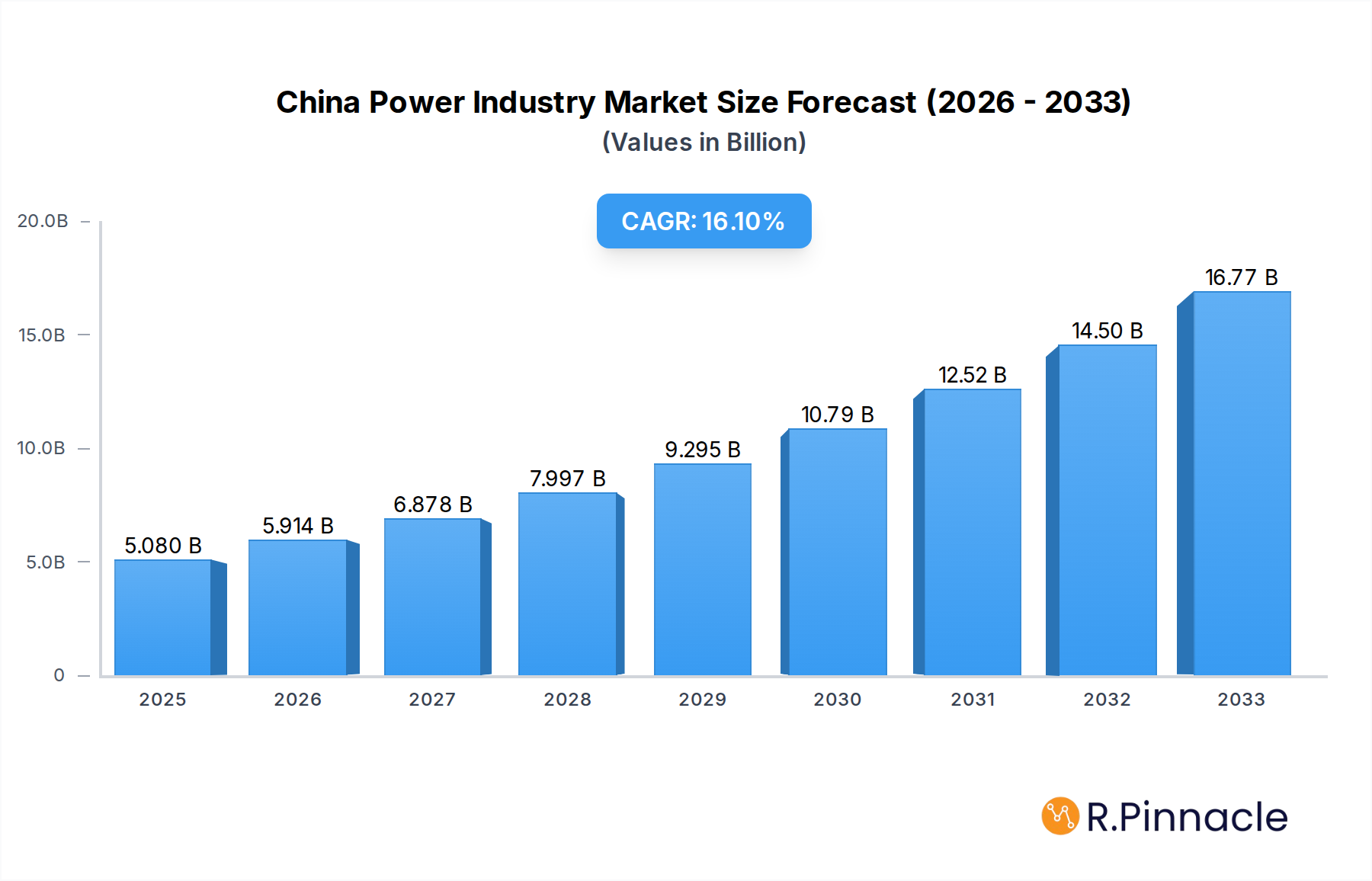

The China Power Industry is poised for substantial growth, with a current market size estimated at $4.36 billion and a projected Compound Annual Growth Rate (CAGR) of 16.39% through 2033. This robust expansion is primarily driven by the nation's escalating energy demands fueled by rapid industrialization, urbanization, and a burgeoning middle class. A significant catalyst for this growth is the government's strong commitment to renewable energy development. Investments in solar, wind, and other green technologies are surging, aimed at decarbonizing the energy mix and achieving ambitious environmental targets. This transition is further supported by advancements in smart grid technologies and the expansion of power transmission and distribution (T&D) infrastructure, ensuring efficient delivery of electricity across the vast country. The increasing integration of advanced technologies, such as artificial intelligence and IoT, into power generation and distribution networks is also playing a crucial role in optimizing operations and enhancing grid reliability.

China Power Industry Market Size (In Billion)

Despite the overwhelmingly positive outlook, certain restraints could temper this growth. While renewable energy sources are booming, the intermittency of these sources and the challenges associated with energy storage remain significant hurdles. Furthermore, the substantial capital expenditure required for upgrading and modernizing existing power infrastructure, coupled with evolving regulatory landscapes and the need for robust grid management systems to handle distributed energy resources, presents ongoing challenges. However, the sheer scale of investment in new power generation capacity, particularly in renewable sectors, and the continuous technological innovation are expected to outweigh these restraints. Key players are actively engaged in expanding their portfolios, focusing on both traditional and renewable energy generation, as well as bolstering their T&D capabilities to meet the ever-increasing power needs of the Chinese economy.

China Power Industry Company Market Share

Unlock comprehensive insights into China's dynamic power sector with this in-depth market analysis. Covering the period from 2019 to 2033, with a base and estimated year of 2025, this report provides critical data and actionable intelligence for industry professionals navigating the world's largest and most rapidly evolving energy market.

China Power Industry Market Structure & Innovation Trends

China's power industry is characterized by a blend of state-controlled giants and increasingly competitive private enterprises, exhibiting moderate market concentration. Innovation is primarily driven by the government's ambitious renewable energy targets, smart grid development, and the pursuit of energy efficiency. Regulatory frameworks, such as national energy plans and environmental protection mandates, significantly shape market dynamics. Product substitutes are emerging, particularly in distributed energy generation and energy storage solutions, challenging traditional grid-dependent models. End-user demographics are increasingly sophisticated, demanding reliable, affordable, and increasingly sustainable power. Mergers and acquisition (M&A) activities are ongoing, though largely driven by state-led consolidations and strategic partnerships aimed at technological advancement and market expansion. While specific M&A deal values are not readily available, the scale of investment in national energy projects indicates substantial financial flows within the sector. Key market participants, including State Grid Corporation of China and China Yangtze Power Co Ltd, hold significant market shares, influencing overall industry structure.

China Power Industry Market Dynamics & Trends

The China power industry is experiencing robust growth, fueled by escalating electricity demand from industrialization, urbanization, and the burgeoning electric vehicle sector. The compound annual growth rate (CAGR) is projected to be substantial, driven by strategic government investments in clean energy technologies and grid modernization. Technological disruptions are profound, with the rapid expansion of renewable energy sources like solar and wind power, alongside advancements in energy storage solutions and the deployment of ultra-high voltage transmission technologies. Consumer preferences are shifting towards cleaner energy options and greater grid reliability, influenced by environmental awareness and the increasing adoption of smart home technologies. The competitive landscape is intense, with established state-owned enterprises coexisting with emerging private players and international technology providers. Market penetration of advanced grid technologies and smart metering solutions is increasing, enhancing operational efficiency and enabling more sophisticated demand-side management. The ongoing transition from coal-fired power to cleaner alternatives presents both a challenge and a significant opportunity for market participants to invest in sustainable power generation.

Dominant Regions & Segments in China Power Industry

The Power Transmission and Distribution (T&D) segment is a dominant force within China's power industry, intrinsically linked to the nation's vast geographical expanse and ongoing economic development. Key drivers for its dominance include substantial government investment in infrastructure to connect remote resource-rich regions with major demand centers, and the continuous expansion of the national grid to accommodate increasing power generation capacity, particularly from renewable sources. Economic policies prioritizing energy security and the equitable distribution of power across all provinces further bolster T&D’s importance.

Renewable Power Generation is another critically dominant segment, driven by China's unwavering commitment to its ambitious decarbonization goals and its leadership in manufacturing solar panels and wind turbines. The segment's growth is accelerated by supportive government subsidies, favorable regulatory frameworks, and increasing global demand for clean energy. The sheer scale of installed capacity for solar and wind power positions this segment as a future cornerstone of China's energy mix.

Within Power Generation Sources, Thermal power remains a significant, albeit declining, segment due to its historical role in meeting base-load demand. However, its dominance is being challenged by the rapid rise of renewables. Hydroelectric power plays a crucial role, particularly in the southwestern regions, leveraging abundant water resources. Nuclear power is also a growing segment, driven by the pursuit of low-carbon, reliable energy sources for densely populated areas.

China Power Industry Product Innovations

Product innovations in the China power industry are predominantly focused on enhancing the efficiency, reliability, and sustainability of energy generation and transmission. Advancements in high-efficiency solar panels, such as those from Wuxi Suntech Power Co Ltd, and the development of larger, more efficient wind turbines by companies like Xinjiang Goldwind Science & Technology Co Ltd and Sinovel Wind Group Co Ltd, are transforming renewable energy generation. In transmission, ultra-high voltage (UHV) technology, exemplified by projects connecting Sichuan to Hubei, significantly reduces energy loss over long distances. Innovations in grid-scale battery storage systems are crucial for balancing the intermittency of renewables, while advancements in smart grid technologies enable better demand response and grid management.

Report Scope & Segmentation Analysis

This report segments the China Power Industry into key areas for comprehensive analysis. Power Generation Sources are categorized into Thermal, Hydroelectric, Nuclear, and Renewable. Each of these sub-segments is analyzed for its current market size, projected growth trajectory (2025-2033), and the competitive dynamics within. Power Transmission and Distribution (T&D) represents another distinct segment, focusing on the infrastructure and technologies that deliver electricity. Growth projections and competitive landscapes within T&D are also detailed, considering investments in grid modernization and expansion.

Key Drivers of China Power Industry Growth

The growth of China's power industry is propelled by several key factors. Firstly, the sustained economic expansion and industrial demand for electricity remains a primary driver. Secondly, the government's ambitious renewable energy targets, aimed at achieving carbon neutrality, are spurring massive investments in solar, wind, and other clean energy technologies. Thirdly, technological advancements in areas like ultra-high voltage transmission, smart grids, and energy storage are enhancing efficiency and expanding grid capabilities. Finally, urbanization and rising living standards are increasing per capita electricity consumption, further contributing to market growth.

Challenges in the China Power Industry Sector

Despite its robust growth, the China power industry faces several challenges. Grid integration of renewable energy sources presents technical hurdles due to their intermittency. Environmental concerns and the phase-out of coal-fired power plants require significant investment in alternative, cleaner generation. Supply chain disruptions for critical components, particularly in the context of global geopolitical shifts, can impact project timelines and costs. Furthermore, regulatory complexities and evolving market policies can create uncertainty for investors. Finally, intense competition and price pressures within certain segments can affect profitability.

Emerging Opportunities in China Power Industry

Emerging opportunities in China's power sector are abundant and diverse. The decentralized energy generation market, driven by rooftop solar and microgrids, offers significant potential. The expansion of electric vehicle charging infrastructure is creating new demand and opportunities for grid services. Green hydrogen production, powered by renewable electricity, represents a future frontier for decarbonization. Investments in energy efficiency technologies and smart grid solutions continue to offer avenues for innovation and market penetration. The increasing demand for energy storage solutions to support grid stability and renewable integration is also a rapidly growing market.

Leading Players in the China Power Industry Market

- Datang International Power Generation Company Limited

- China National Electric Wire & Cable I/E Corp

- State Grid Corporation of China

- Xinjiang Goldwind Science & Technology Co Ltd

- Sinovel Wind Group Co Ltd

- China National Electric Engineering Co Ltd

- China Yangtze Power Co Ltd

- Wuxi Suntech Power Co Ltd

- Sinohydro Corporation

- Shandong energy group co Ltd

Key Developments in China Power Industry Industry

- February 2023: China commenced work on the world's biggest ultrahigh-voltage energy transmission project, connecting Southwest China's Sichuan Province and Xizang Autonomous Region to Central China's Hubei Province. The project will transmit approximately 40 billion kWh of electricity annually, including hydroelectricity from the Jinsha River's upper stream, equivalent to one-sixth of Hubei Province's annual power demand, significantly boosting energy distribution efficiency.

- January 2023: China Three Gorges (CTG) announced the commencement of construction for a massive 16 GW integrated solar, wind, and coal project. This ambitious undertaking includes 8 GW of solar power capacity, 4 GW of wind power, and 4 GW of coal-fired generation, alongside crucial energy storage components, signaling a strategic approach to balancing diverse energy sources.

- March 2022: GE Gas Power and Harbin Electric reported that Shenzhen Energy Group Corporation Co. ordered equipment for its Guangming combined cycle power plant. The order includes three GE 9HA.01 gas turbines for a new 2-GW natural gas-fired power plant, a move designed to support the retirement of a large regional coal-fired complex and transition towards cleaner fuel sources.

Future Outlook for China Power Industry Market

The future outlook for China's power industry is exceptionally promising, marked by sustained growth and a profound transformation towards sustainability. Key growth accelerators include the continued aggressive expansion of renewable energy capacity, driven by national climate goals and technological advancements that are making solar and wind power increasingly cost-competitive. Investments in smart grid infrastructure and energy storage will be crucial for managing the complexities of a high-renewable energy system, ensuring grid stability and reliability. The electrification of transportation and industrial processes will create new demand paradigms. Strategic opportunities lie in further developing green hydrogen, enhancing energy efficiency across all sectors, and leveraging digital technologies for optimized energy management. The industry is poised for continued innovation and significant contributions to global energy transition efforts.

China Power Industry Segmentation

-

1. Power Generation Source

- 1.1. Thermal

- 1.2. Hydroelectric

- 1.3. Nuclear

- 1.4. Renewable

- 1.5. Other Power Generation Sources

- 2. Power Transmission and Distribution (T&D)

China Power Industry Segmentation By Geography

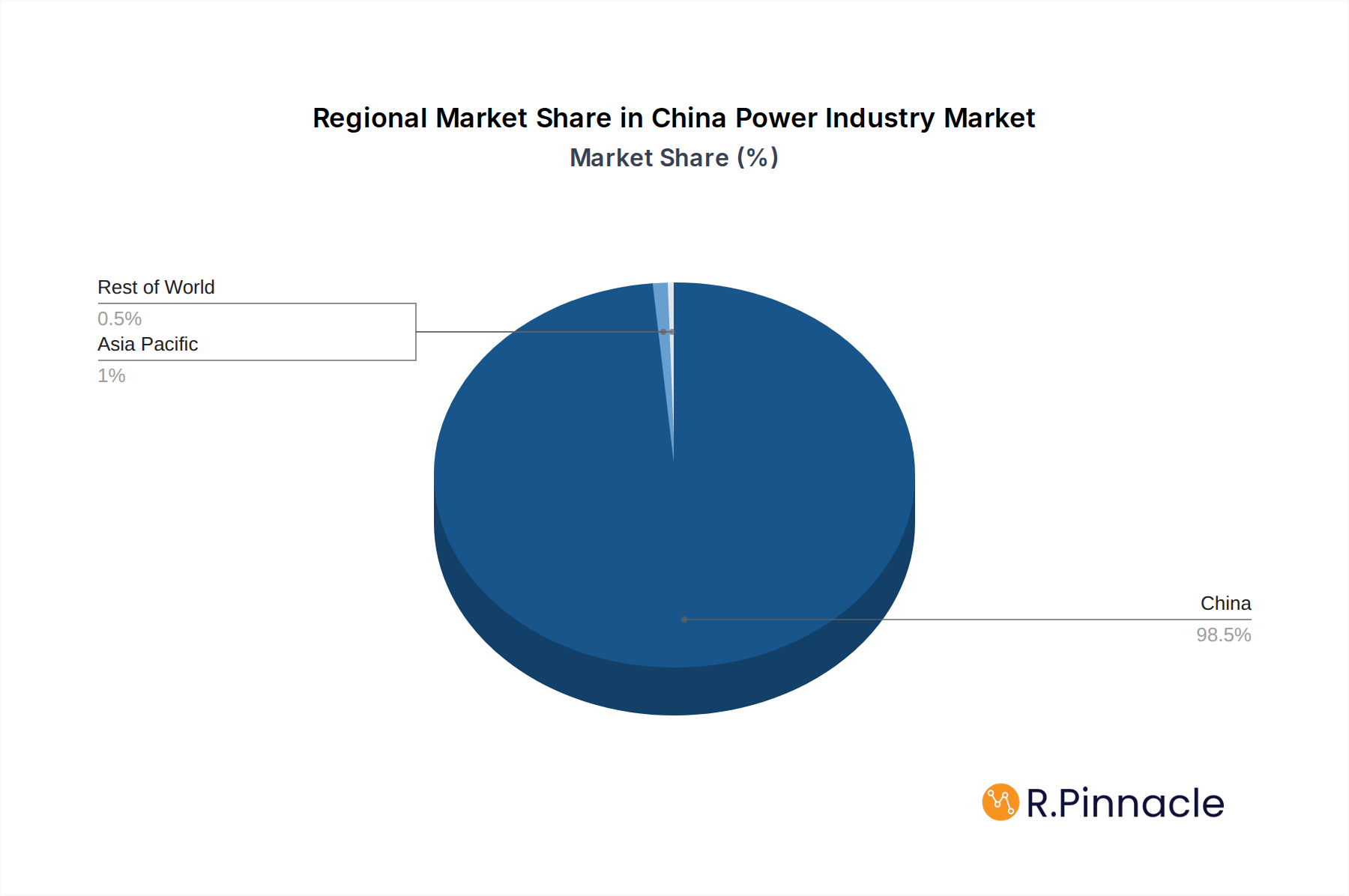

- 1. China

China Power Industry Regional Market Share

Geographic Coverage of China Power Industry

China Power Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 16.39% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Power Generation Source

- 5.1.1. Thermal

- 5.1.2. Hydroelectric

- 5.1.3. Nuclear

- 5.1.4. Renewable

- 5.1.5. Other Power Generation Sources

- 5.2. Market Analysis, Insights and Forecast - by Power Transmission and Distribution (T&D)

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. China

- 5.1. Market Analysis, Insights and Forecast - by Power Generation Source

- 6. China Power Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Power Generation Source

- 6.1.1. Thermal

- 6.1.2. Hydroelectric

- 6.1.3. Nuclear

- 6.1.4. Renewable

- 6.1.5. Other Power Generation Sources

- 6.2. Market Analysis, Insights and Forecast - by Power Transmission and Distribution (T&D)

- 6.1. Market Analysis, Insights and Forecast - by Power Generation Source

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Datang International Power Generation Company Limited

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 China National Electric Wire & Cable I/E Corp

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 State Grid Corporation of China

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Xinjiang Goldwind Science & Technology Co Ltd

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Sinovel Wind Group Co Ltd

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 China National Electric Engineering Co Ltd

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 China Yangtze Power Co Ltd

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Wuxi Suntech Power Co Ltd

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Sinohydro Corporation

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Shandong energy group co Ltd *List Not Exhaustive

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Datang International Power Generation Company Limited

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: China Power Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: China Power Industry Share (%) by Company 2025

List of Tables

- Table 1: China Power Industry Revenue Million Forecast, by Power Generation Source 2020 & 2033

- Table 2: China Power Industry Revenue Million Forecast, by Power Transmission and Distribution (T&D) 2020 & 2033

- Table 3: China Power Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: China Power Industry Revenue Million Forecast, by Power Generation Source 2020 & 2033

- Table 5: China Power Industry Revenue Million Forecast, by Power Transmission and Distribution (T&D) 2020 & 2033

- Table 6: China Power Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the China Power Industry?

The projected CAGR is approximately 16.39%.

2. Which companies are prominent players in the China Power Industry?

Key companies in the market include Datang International Power Generation Company Limited, China National Electric Wire & Cable I/E Corp, State Grid Corporation of China, Xinjiang Goldwind Science & Technology Co Ltd, Sinovel Wind Group Co Ltd, China National Electric Engineering Co Ltd, China Yangtze Power Co Ltd, Wuxi Suntech Power Co Ltd, Sinohydro Corporation, Shandong energy group co Ltd *List Not Exhaustive.

3. What are the main segments of the China Power Industry?

The market segments include Power Generation Source, Power Transmission and Distribution (T&D).

4. Can you provide details about the market size?

The market size is estimated to be USD 4.36 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Upcoming Investments in Renewable Energy Sector4.; Growing Manufacturing Sector Increases Demand For Power.

6. What are the notable trends driving market growth?

The Renewable Energy Segment Expected to Dominate the Market.

7. Are there any restraints impacting market growth?

Rising Phase Out of Coal-based Power Plants.

8. Can you provide examples of recent developments in the market?

February 2023: China announced that it had started work on the world's biggest ultrahigh-voltage energy transmission project, which will connect Southwest China's Sichuan Province and the Xizang Autonomous Region to Central China's Hubei Province. The transmission project will carry around 40 billion KW hours of electricity, including hydroelectricity from the Jinsha River's upper stream, comparable to one-sixth of Hubei Province's annual power demand.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "China Power Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the China Power Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the China Power Industry?

To stay informed about further developments, trends, and reports in the China Power Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence