Key Insights

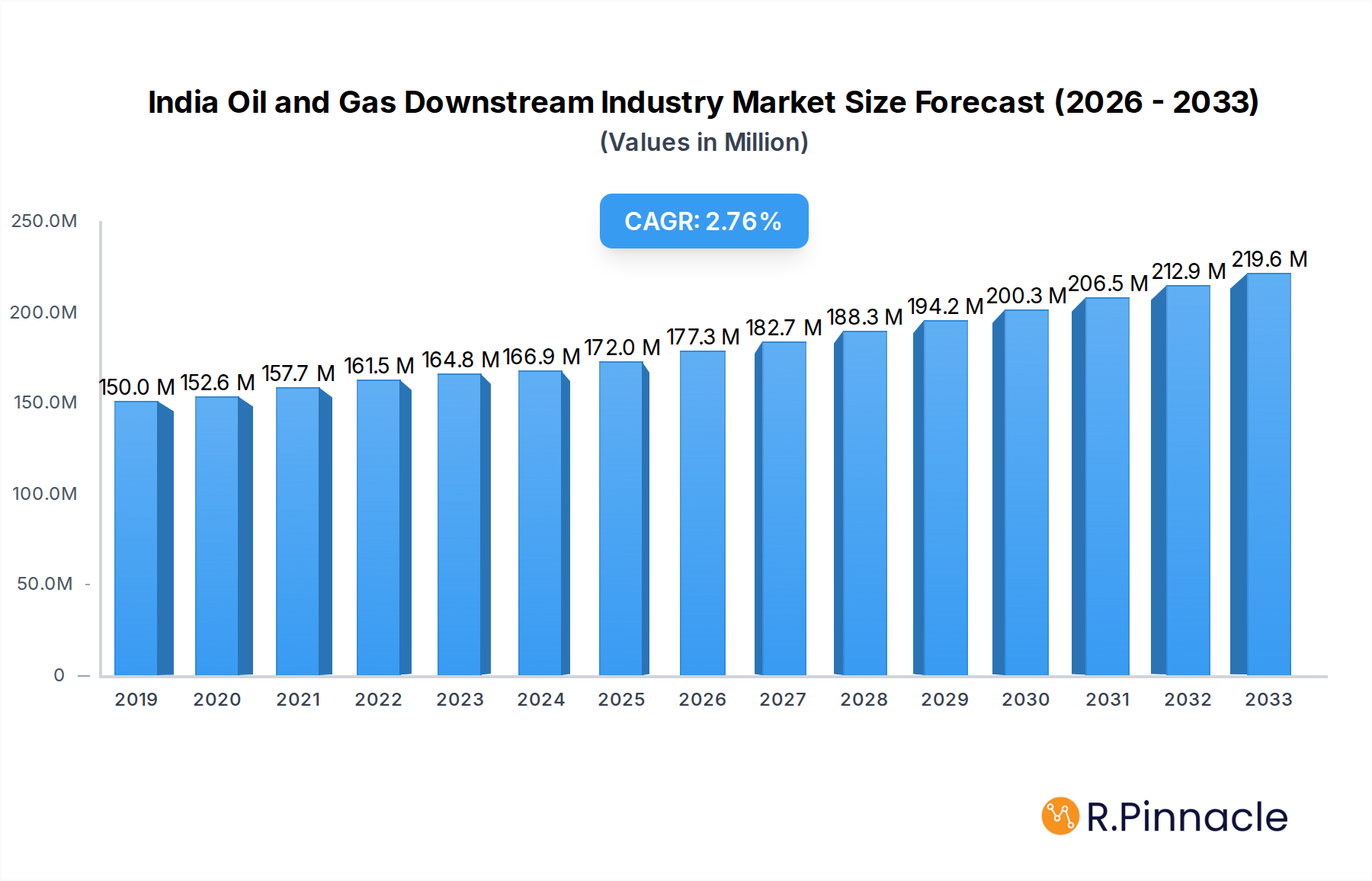

The Indian Oil and Gas Downstream Industry is poised for robust growth, with an estimated market size of $166.93 million in 2024. The sector is projected to expand at a Compound Annual Growth Rate (CAGR) of 3.5% from 2019 to 2033, indicating sustained momentum driven by increasing domestic energy demand and strategic government initiatives. This growth trajectory is primarily fueled by the nation's expanding economy, burgeoning middle class, and the continuous need for refined petroleum products and petrochemical derivatives. Key drivers include substantial investments in refining capacity expansion and modernization, alongside the development of new petrochemical complexes to meet the rising demand for polymers, chemicals, and other downstream products. The government's focus on enhancing energy security and promoting domestic manufacturing further supports this expansion.

India Oil and Gas Downstream Industry Market Size (In Million)

The market's expansion is further characterized by significant investments in upgrading existing refineries and establishing new, technologically advanced petrochemical plants. Companies like Indian Oil Corporation Limited, Bharat Petroleum Corporation Limited, and Reliance Industries Limited are at the forefront of these developments, investing heavily in projects aimed at increasing production efficiency, product diversification, and environmental compliance. Emerging trends such as the adoption of cleaner fuels, the development of specialty chemicals, and a greater emphasis on operational efficiency through digital transformation are shaping the industry landscape. While the sector benefits from strong demand, it also navigates challenges such as price volatility of crude oil, stringent environmental regulations, and the need for continuous technological upgrades to remain competitive. Nonetheless, the outlook remains exceptionally positive, driven by India's integral role in the global energy market and its unwavering commitment to energy self-sufficiency and economic development.

India Oil and Gas Downstream Industry Company Market Share

Here is an SEO-optimized, reader-centric report description for the India Oil and Gas Downstream Industry:

India Oil and Gas Downstream Industry Market Analysis: Navigating Growth and Innovation (2019–2033)

This comprehensive report delivers an in-depth analysis of the India Oil and Gas Downstream Industry, providing critical insights for stakeholders seeking to capitalize on burgeoning opportunities and navigate evolving market dynamics. Covering a study period from 2019 to 2033, with a base and estimated year of 2025, this report offers an unparalleled view of market concentration, innovation trends, regulatory landscapes, and the competitive forces shaping the sector. Essential for industry professionals, investors, and policymakers, this report equips you with the actionable intelligence needed to drive strategic decision-making in one of the world's fastest-growing energy markets.

India Oil and Gas Downstream Industry Market Structure & Innovation Trends

The Indian Oil and Gas Downstream Industry is characterized by a moderate market concentration, with a few dominant players holding significant market share. Key companies like Indian Oil Corporation Limited, Bharat Petroleum Corporation Limited, and Hindustan Petroleum Corporation Limited lead the refining segment, while GAIL (India) Limited and Reliance Industries Limited are pivotal in petrochemicals. Innovation is primarily driven by the pursuit of advanced refining technologies, the development of higher-value petrochemical products, and increasing investments in sustainable and cleaner fuel alternatives. Regulatory frameworks, while evolving, continue to emphasize energy security and environmental compliance. Product substitutes, such as renewable energy sources and electric mobility, are emerging as long-term competitive pressures. End-user demographics are shifting towards a larger middle class with increasing disposable incomes, driving demand for refined fuels and petrochemical derivatives. Mergers and acquisitions (M&A) activities are strategically focused on enhancing capacity, expanding product portfolios, and gaining market share. Recent M&A deal values are estimated to be in the range of several hundred million to over a billion dollars for significant transactions, indicating consolidation and strategic growth plays within the sector.

India Oil and Gas Downstream Industry Market Dynamics & Trends

The Indian Oil and Gas Downstream Industry is poised for robust growth, driven by a confluence of factors including rising energy demand from a rapidly expanding economy and a growing population. The market is projected to experience a Compound Annual Growth Rate (CAGR) of approximately 6-7% over the forecast period (2025–2033). Technological disruptions are playing a crucial role, with advancements in refining processes leading to improved efficiency and the production of cleaner fuels. The adoption of digital technologies, artificial intelligence, and automation in refineries and petrochemical plants is enhancing operational excellence and safety. Consumer preferences are evolving, with an increasing demand for high-quality fuels, specialty chemicals, and environmentally friendly products. The push towards cleaner energy is also influencing demand patterns, although conventional fuels will remain dominant for the foreseeable future. Competitive dynamics are intensifying, with both public sector undertakings and private players vying for market leadership through capacity expansion, product diversification, and strategic partnerships. Market penetration for refined products and petrochemicals is expected to deepen, especially in tier-2 and tier-3 cities, as infrastructure development continues to improve access and distribution networks. The downstream sector is also witnessing a trend towards greater integration, with companies seeking to optimize their value chains from refining to petrochemical production and marketing. The ongoing energy transition presents both challenges and opportunities, pushing companies to invest in sustainability initiatives and explore new avenues like biofuels and green hydrogen. The government's policy initiatives, such as the Pradhan Mantri Ujjwala Yojana, have significantly boosted LPG consumption and are indicative of the focus on increasing energy access and affordability. Furthermore, the increasing use of petrochemicals in various industries, including automotive, construction, and packaging, underpins sustained demand growth. The evolving global energy landscape, including geopolitical shifts and the push for decarbonization, will continue to shape the strategic direction of the Indian downstream sector.

Dominant Regions & Segments in India Oil and Gas Downstream Industry

The Indian Oil and Gas Downstream Industry exhibits distinct regional dominance and segment leadership.

Refineries: Market Overview

- Dominant Region: Western India, particularly states like Gujarat and Maharashtra, are the nerve centers of refining operations. This dominance is attributed to a confluence of factors:

- Proximity to Ports: These regions have extensive coastal access, facilitating the import of crude oil and the export of refined products. Major ports like Kandla, Mundra, and JNPT provide critical logistical advantages.

- Established Infrastructure: Decades of investment have led to the development of robust pipeline networks, storage facilities, and transportation infrastructure supporting refining operations.

- Industrial Hubs: These states are major industrial and economic hubs, creating significant domestic demand for refined fuels and petrochemical feedstocks.

- Government Support & Policy: Favorable state government policies and incentives have historically attracted and supported the growth of the refining sector.

Key Project Information: The refining segment is characterized by large-scale, integrated refinery complexes. Key projects include expansions and upgrades of existing facilities by major players like Indian Oil Corporation Limited (IOCL), Bharat Petroleum Corporation Limited (BPCL), and Hindustan Petroleum Corporation Limited (HPCL). Reliance Industries Limited's Jamnagar refinery remains a global benchmark in terms of scale and complexity. Recent and ongoing projects focus on increasing capacity, enhancing complexity to process heavier crudes, and upgrading to meet stringent fuel specifications like BS-VI. Project investments are often in the multi-billion dollar range for greenfield expansions and significant upgrades.

Petrochemical Plants: Market Overview

- Dominant Segment: The petrochemical segment is experiencing rapid growth, driven by increasing demand from sectors like packaging, textiles, automotive, and construction.

- Polymer Production: This is the largest sub-segment, with significant production of polyethylene (PE), polypropylene (PP), and polyvinyl chloride (PVC), essential for various industrial and consumer applications.

- Aromatics and Olefins: These are key building blocks for a wide array of downstream chemical products and are witnessing steady demand growth.

Key Project Information: Petrochemical projects are often integrated with refineries to optimize feedstock utilization. Reliance Industries Limited is a major player in this segment with its integrated refinery-petrochemical complexes. GAIL (India) Limited is also a significant contributor through its petrochemical plants and gas processing facilities. New investments are focused on expanding capacities for high-demand polymers and exploring the production of specialty chemicals. Projects include the development of new crackers, polymer units, and downstream chemical facilities, with investments ranging from hundreds of millions to billions of dollars.

India Oil and Gas Downstream Industry Product Innovations

Product innovations in the India Oil and Gas Downstream Industry are increasingly focused on enhancing product quality and environmental performance. Refiners are investing in technologies to produce ultra-low sulfur diesel and gasoline, aligning with stricter emission norms. Petrochemical companies are developing advanced polymers with improved strength, durability, and recyclability, catering to the evolving needs of industries like automotive and packaging. There's a growing emphasis on specialty chemicals that offer enhanced performance characteristics for niche applications. These innovations are driven by a desire for competitive advantage, regulatory compliance, and a response to growing consumer demand for sustainable and high-performance products, ensuring market fit and broader application potential.

Report Scope & Segmentation Analysis

This report meticulously analyzes the India Oil and Gas Downstream Industry, segmenting the market into Refineries and Petrochemical Plants.

Refineries: This segment encompasses the refining of crude oil into various petroleum products. The market size is projected to reach over $200 billion by 2033, with steady growth driven by increasing fuel demand. Key project information highlights ongoing expansions and upgrades aimed at enhancing capacity and complexity. Competitive dynamics involve major PSUs and private players focusing on operational efficiency and meeting evolving fuel standards.

Petrochemical Plants: This segment focuses on the production of chemicals derived from petroleum and natural gas. The market is expected to witness robust growth, exceeding $100 billion by 2033, fueled by demand from end-use industries. Key project information indicates investments in expanding polymer and specialty chemical capacities. Competitive dynamics are characterized by integration with refining operations and a growing focus on high-value products.

Key Drivers of India Oil and Gas Downstream Industry Growth

The growth of the India Oil and Gas Downstream Industry is propelled by several key drivers. Economic expansion and a burgeoning middle class are fueling an insatiable demand for transportation fuels and petrochemical-based products. Government initiatives like 'Make in India' and policies promoting energy security further bolster domestic production and consumption. Technological advancements in refining and petrochemical processes enhance efficiency, product quality, and environmental compliance, enabling companies to meet stricter regulations and evolving market needs. The increasing use of plastics and polymers in various sectors like packaging, automotive, and construction significantly drives demand for petrochemical derivatives. For instance, the government's push for infrastructure development directly translates to higher consumption of petrochemicals in construction materials.

Challenges in the India Oil and Gas Downstream Industry Sector

Despite robust growth, the India Oil and Gas Downstream Industry faces significant challenges. Regulatory hurdles and evolving environmental norms necessitate continuous investment in upgraded technologies and processes, increasing capital expenditure. Crude oil price volatility and dependence on imports create supply chain risks and impact profitability. Intensifying competition, both domestic and international, pressures margins and requires constant innovation and cost optimization. Infrastructure bottlenecks, particularly in logistics and transportation, can hinder efficient product distribution. Public perception and the increasing focus on decarbonization present long-term challenges to the demand for fossil fuels, necessitating diversification strategies.

Emerging Opportunities in India Oil and Gas Downstream Industry

The India Oil and Gas Downstream Industry is ripe with emerging opportunities. The increasing demand for specialty chemicals and advanced materials presents lucrative avenues for value addition. The growth of the electric vehicle (EV) ecosystem, while posing a long-term shift, also creates opportunities for producing advanced battery materials and lightweight plastics. The government's focus on biofuels and renewable energy integration opens doors for hybrid business models and investments in sustainable alternatives. Digital transformation and the adoption of Industry 4.0 technologies offer significant potential for operational efficiency, predictive maintenance, and cost reduction. Furthermore, the expansion into new geographical markets and downstream integration into consumer-facing segments can unlock further growth.

Leading Players in the India Oil and Gas Downstream Industry Market

- Oil and Natural Gas Corporation

- Bharat Petroleum Corporation Limited

- Haldia Petrochemicals Ltd

- Hindustan Petroleum Corporation Limited

- Reliance Industries Limited

- GAIL (India) Limited

- Nayara Energy Limited

- Indian Oil Corporation Limited

- Oman Oil Company

Key Developments in India Oil and Gas Downstream Industry Industry

- 2023/2024: Indian Oil Corporation Limited announces significant capacity expansion plans for its refineries to meet rising fuel demand.

- 2023/2024: Reliance Industries Limited continues to invest heavily in its integrated petrochemical complexes, focusing on specialty polymers.

- 2023: Bharat Petroleum Corporation Limited announces new projects to upgrade its refining capabilities and enhance product quality.

- 2022/2023: GAIL (India) Limited focuses on expanding its petrochemical production capacity and exploring gas-based chemical opportunities.

- Ongoing: Increased adoption of digital technologies and automation across major refineries and petrochemical plants for improved operational efficiency.

- Ongoing: Focus on developing and producing BS-VI compliant fuels and higher-value petrochemical derivatives.

Future Outlook for India Oil and Gas Downstream Industry Market

The future outlook for the India Oil and Gas Downstream Industry is exceptionally bright, characterized by sustained demand growth and strategic diversification. While conventional fuels will remain a cornerstone for the medium term, the industry is increasingly pivoting towards higher-value petrochemicals and specialty products. Significant investments are anticipated in expanding refining capacities and petrochemical production, driven by domestic consumption and export potential. The integration of cleaner technologies and a gradual exploration of biofuels and hydrogen are expected to shape the long-term trajectory. Companies that can effectively navigate regulatory landscapes, leverage technological advancements, and adapt to evolving consumer preferences will be best positioned for sustained success and growth in this dynamic market. The strategic importance of the downstream sector to India's economic development ensures continued focus and investment.

India Oil and Gas Downstream Industry Segmentation

-

1. Refineries

- 1.1. Market Overview

- 1.2. Key Project Information

-

2. Petrochemical Pants

- 2.1. Market Overview

- 2.2. Key Project Information

India Oil and Gas Downstream Industry Segmentation By Geography

- 1. India

India Oil and Gas Downstream Industry Regional Market Share

Geographic Coverage of India Oil and Gas Downstream Industry

India Oil and Gas Downstream Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Refineries

- 5.1.1. Market Overview

- 5.1.2. Key Project Information

- 5.2. Market Analysis, Insights and Forecast - by Petrochemical Pants

- 5.2.1. Market Overview

- 5.2.2. Key Project Information

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. India

- 5.1. Market Analysis, Insights and Forecast - by Refineries

- 6. India Oil and Gas Downstream Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Refineries

- 6.1.1. Market Overview

- 6.1.2. Key Project Information

- 6.2. Market Analysis, Insights and Forecast - by Petrochemical Pants

- 6.2.1. Market Overview

- 6.2.2. Key Project Information

- 6.1. Market Analysis, Insights and Forecast - by Refineries

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Oil and Natural Gas Corporation

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Bharat Petroleum Corporation Limited

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Haldia Petrochemicals Ltd

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Hindustan Petroleum Corporation Limited

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Reliance Industries Limited

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 GAIL (India) Limited

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Nayara Energy Limited

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Indian Oil Corporation Limited

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Oman Oil Company

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.1 Oil and Natural Gas Corporation

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: India Oil and Gas Downstream Industry Revenue Breakdown (million, %) by Product 2025 & 2033

- Figure 2: India Oil and Gas Downstream Industry Share (%) by Company 2025

List of Tables

- Table 1: India Oil and Gas Downstream Industry Revenue million Forecast, by Refineries 2020 & 2033

- Table 2: India Oil and Gas Downstream Industry Revenue million Forecast, by Petrochemical Pants 2020 & 2033

- Table 3: India Oil and Gas Downstream Industry Revenue million Forecast, by Region 2020 & 2033

- Table 4: India Oil and Gas Downstream Industry Revenue million Forecast, by Refineries 2020 & 2033

- Table 5: India Oil and Gas Downstream Industry Revenue million Forecast, by Petrochemical Pants 2020 & 2033

- Table 6: India Oil and Gas Downstream Industry Revenue million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the India Oil and Gas Downstream Industry?

The projected CAGR is approximately 3.5%.

2. Which companies are prominent players in the India Oil and Gas Downstream Industry?

Key companies in the market include Oil and Natural Gas Corporation, Bharat Petroleum Corporation Limited, Haldia Petrochemicals Ltd, Hindustan Petroleum Corporation Limited, Reliance Industries Limited, GAIL (India) Limited, Nayara Energy Limited, Indian Oil Corporation Limited, Oman Oil Company.

3. What are the main segments of the India Oil and Gas Downstream Industry?

The market segments include Refineries, Petrochemical Pants.

4. Can you provide details about the market size?

The market size is estimated to be USD 166.93 million as of 2022.

5. What are some drivers contributing to market growth?

4.; Increasing Investments in Renewable Energy Generation 4.; Supportive Government Policies Towards Green Energy.

6. What are the notable trends driving market growth?

Refineries to Dominate the Market.

7. Are there any restraints impacting market growth?

4.; Challenges In Installing Renewable Power in the Circulated Structure.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "India Oil and Gas Downstream Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the India Oil and Gas Downstream Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the India Oil and Gas Downstream Industry?

To stay informed about further developments, trends, and reports in the India Oil and Gas Downstream Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence