Key Insights

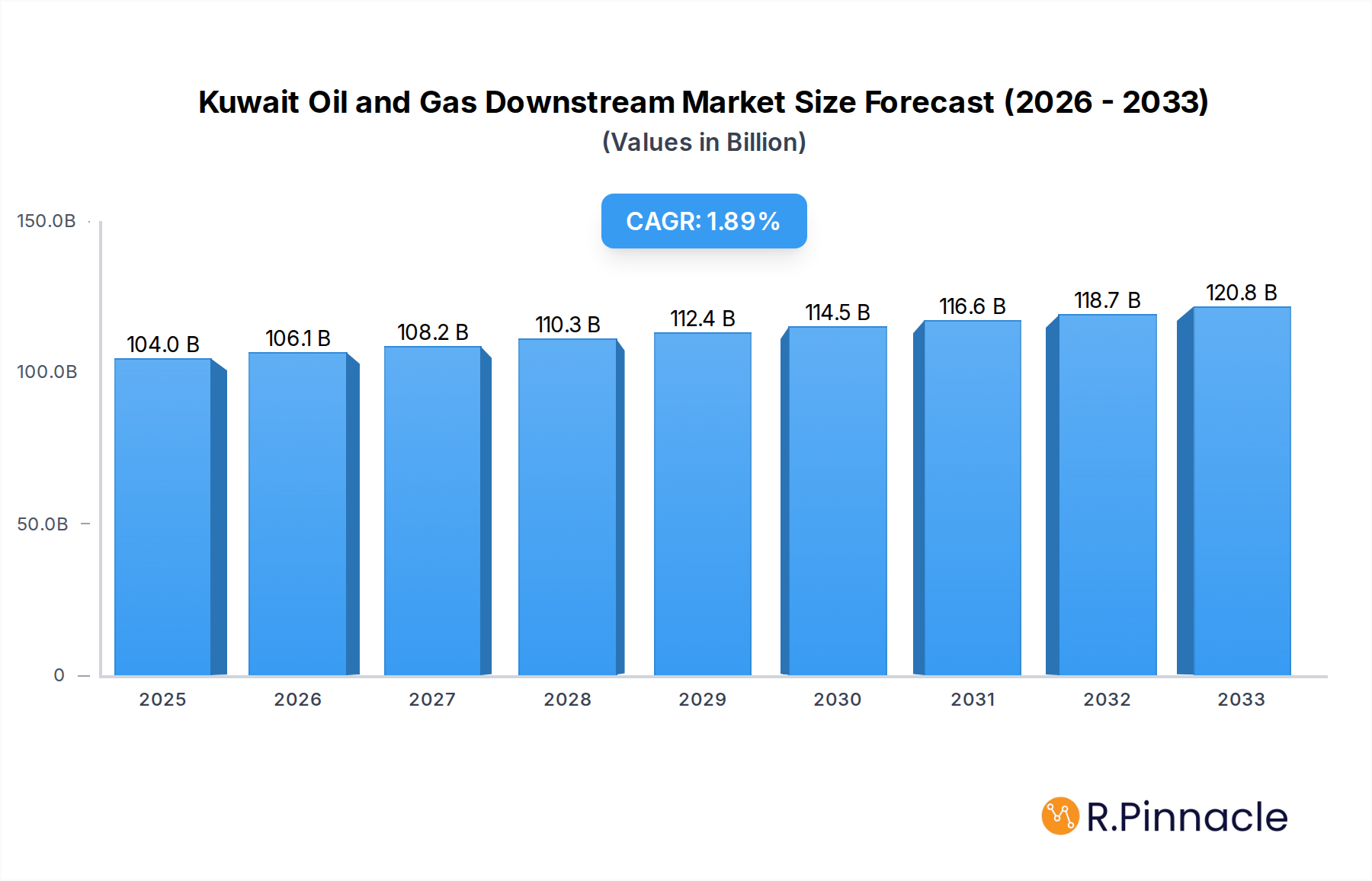

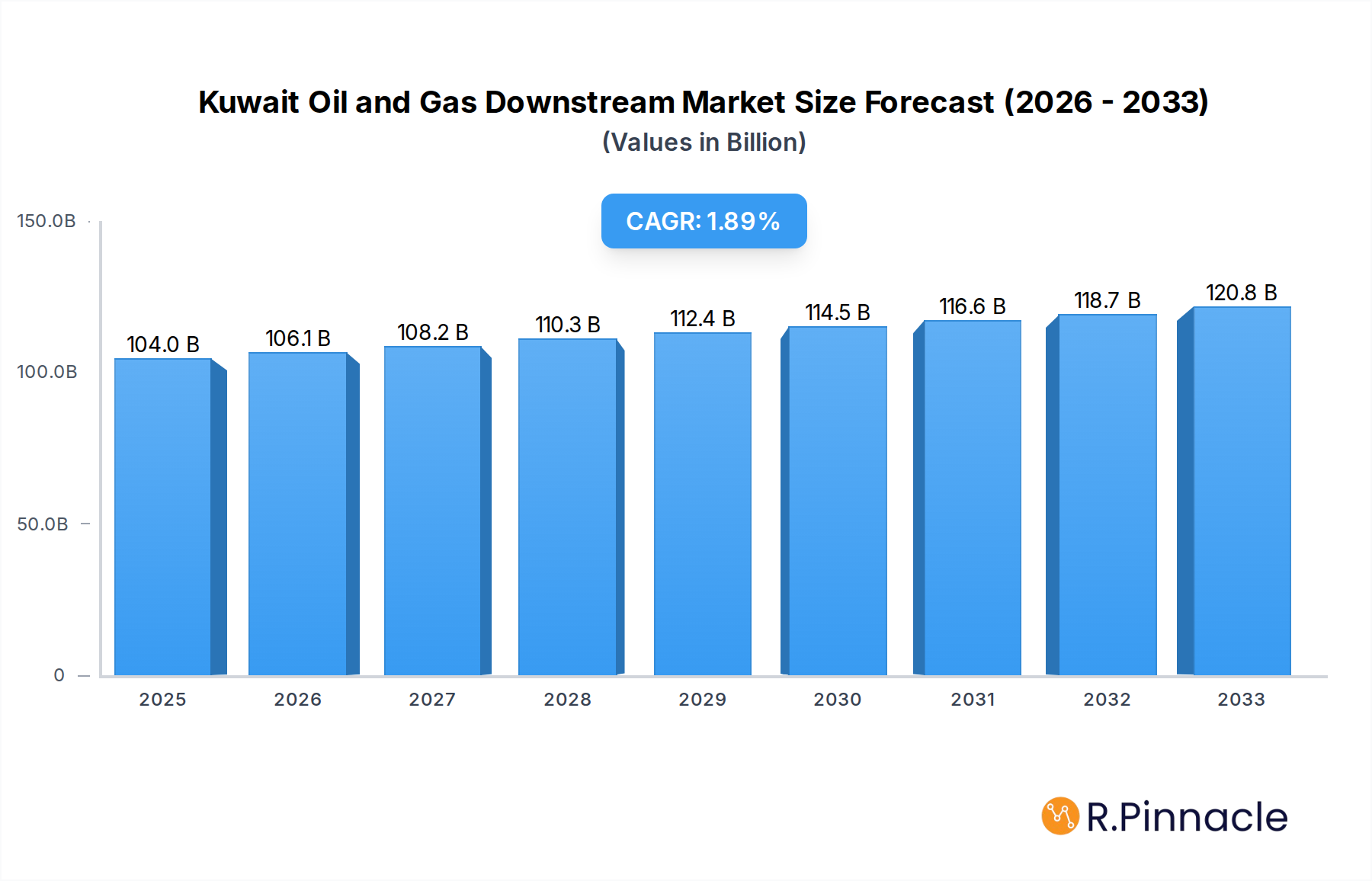

The Kuwait Oil and Gas Downstream market is poised for steady expansion, with an estimated market size of $104 billion in 2025. The sector is projected to grow at a Compound Annual Growth Rate (CAGR) of 2.1% from 2019 to 2033, indicating a sustained but moderate upward trajectory. This growth is primarily fueled by significant investments in expanding and modernizing existing refinery infrastructure and the robust development of petrochemical plants. Kuwait's strategic position and substantial hydrocarbon reserves continue to underpin the strength of its downstream sector. The focus on enhancing refining capacities and diversifying petrochemical production is a key driver, aiming to maximize the value derived from its oil and gas resources and meet growing regional and global demand for refined products and petrochemical derivatives.

Kuwait Oil and Gas Downstream Market Market Size (In Billion)

The market's forward momentum is supported by a pipeline of projects and upcoming initiatives aimed at increasing operational efficiency, incorporating advanced technologies, and expanding product portfolios. Key players such as TotalEnergies, Kuwait Oil Company, BP PLC, Petrochemical Industry Company, and Kuwait National Petroleum Company are actively involved in these developments, contributing to market dynamism. While the market benefits from strong governmental support and strategic investments, potential challenges such as fluctuating global energy prices and increasing environmental regulations could influence the pace of growth. However, the ongoing modernization of refineries and the strategic expansion of petrochemical facilities are expected to create a resilient and evolving downstream sector in Kuwait.

Kuwait Oil and Gas Downstream Market Company Market Share

This comprehensive report delves into the dynamic Kuwait Oil and Gas Downstream Market, providing an in-depth analysis of its structure, market dynamics, regional dominance, and future outlook from 2019 to 2033. With a base year of 2025 and a forecast period extending to 2033, this study is crucial for industry professionals seeking to understand the evolving landscape of Kuwait's refining and petrochemical sectors. Featuring insights into key players like Total SA, Kuwait Oil Company, BP PLC, Petrochemicals Industry Company, and Kuwait National Petroleum Company, this report offers actionable intelligence on existing infrastructure, projects in the pipeline, and upcoming projects, crucial for strategic decision-making in the Kuwait oil and gas downstream market.

Kuwait Oil and Gas Downstream Market Market Structure & Innovation Trends

The Kuwait Oil and Gas Downstream Market exhibits a moderately concentrated structure, dominated by state-owned enterprises and a few key international players. Market share is largely dictated by refining capacity and petrochemical production volume. Innovation drivers in this sector are primarily focused on enhancing operational efficiency, improving product quality to meet stringent environmental regulations, and developing higher-value petrochemical derivatives. Regulatory frameworks are robust, driven by the Ministry of Oil and other relevant government bodies, which play a significant role in shaping investment and operational guidelines. The threat of product substitutes is relatively low in the immediate term due to the essential nature of refined fuels and basic petrochemicals, though advancements in sustainable alternatives could pose a long-term challenge. End-user demographics are diverse, encompassing transportation, manufacturing, construction, and consumer goods industries. Merger and acquisition (M&A) activities have been limited, with a focus on strategic partnerships and joint ventures rather than outright acquisitions. M&A deal values are typically significant, reflecting the capital-intensive nature of downstream projects.

Kuwait Oil and Gas Downstream Market Market Dynamics & Trends

The Kuwait Oil and Gas Downstream Market is experiencing robust growth, propelled by several key factors. A primary growth driver is the government's strategic vision to diversify its economy and maximize the value derived from its vast hydrocarbon resources. Significant investments are being channeled into expanding and upgrading existing refinery infrastructure, alongside the development of new petrochemical complexes. This expansion is designed to meet both domestic demand and increasing export opportunities. Technological disruptions are playing a crucial role, with a growing emphasis on digitalization, automation, and the adoption of advanced process technologies to enhance efficiency, reduce operational costs, and minimize environmental impact. These advancements are vital for maintaining competitiveness in the global market. Consumer preferences, particularly in international markets, are shifting towards higher-quality, more specialized petrochemical products and cleaner-burning fuels, influencing production strategies. The competitive dynamics are characterized by strategic collaborations between Kuwaiti national oil companies and international energy giants, fostering knowledge transfer and technological expertise. The market penetration of specialized petrochemicals is expected to rise as new applications emerge. The projected Compound Annual Growth Rate (CAGR) for the forecast period is XX%, indicating a healthy expansion trajectory for the Kuwait oil and gas downstream market.

Dominant Regions & Segments in Kuwait Oil and Gas Downstream Market

Within Kuwait, the downstream oil and gas sector is heavily concentrated in specific industrial hubs designed to leverage proximity to production facilities and export terminals. The dominant region for both refineries and petrochemicals is the Al-Ahmadi Governorate, which hosts the majority of Kuwait's integrated refining and petrochemical complexes.

Refineries: Overview

- Existing Infrastructure: Al-Ahmadi houses some of the largest and most sophisticated refineries in the region, including the Mina Al-Ahmadi Refinery and the Shuaiba Refinery (though Shuaiba is undergoing significant modernization and potential repurposing). These facilities are crucial for processing Kuwait's crude oil into a wide range of refined products. Key drivers for their dominance include strategic coastal locations for feedstock import and product export, established logistics networks, and extensive historical investment.

- Projects in Pipeline: Significant expansion and upgrade projects are underway or planned for existing refineries. These projects aim to increase processing capacity, improve product quality to meet Euro V and VI standards, and enhance flexibility to process different crude slates. The primary goal is to maximize the production of higher-value products like naphtha, jet fuel, and diesel, while minimizing the output of lower-value fuels.

- Upcoming Projects: Future refinery developments are likely to focus on integrating further downstream processing capabilities, potentially including complex petrochemical feedstock production. These projects are influenced by long-term demand forecasts and the strategic imperative to move further up the value chain.

Petrochemicals Plants: Overview

- Existing Infrastructure: Petrochemicals Industry Company (PIC) and Kuwait National Petroleum Company (KNPC) operate world-class petrochemical facilities, often integrated with refineries in the Al-Ahmadi region. These plants produce a range of essential petrochemicals, including olefins, aromatics, and polymers, catering to both domestic and international demand. The strategic advantage here lies in the readily available and cost-competitive feedstock supplied by nearby refineries.

- Projects in Pipeline: Major projects in the petrochemical segment focus on expanding capacity for existing product lines and venturing into new, higher-margin specialty chemicals. This includes investments in new cracker units and downstream derivative plants to produce plastics, synthetic fibers, and other intermediate chemicals. The economic policies supporting industrial diversification and the government's commitment to developing a robust petrochemical industry are key drivers.

- Upcoming Projects: Future petrochemical developments will likely emphasize sustainability, with investments in circular economy initiatives and the production of bio-based or recycled petrochemicals. The proximity to major shipping routes and established export markets solidifies the dominance of this region in Kuwait's petrochemical landscape.

Kuwait Oil and Gas Downstream Market Product Innovations

Product innovations in the Kuwait Oil and Gas Downstream Market are increasingly driven by the pursuit of higher value addition and sustainability. Refineries are focusing on producing cleaner fuels and specialized feedstock for petrochemicals. Petrochemical plants are innovating in the production of advanced polymers, specialized chemicals for the automotive and construction sectors, and materials with improved performance characteristics. Competitive advantages are being sought through enhanced product purity, tailored formulations to meet specific client needs, and the development of more energy-efficient manufacturing processes. Technological trends include the adoption of digital twins for process optimization and the exploration of catalysts that enable more selective and efficient chemical reactions.

Report Scope & Segmentation Analysis

This report meticulously segments the Kuwait Oil and Gas Downstream Market across its core components: Refineries and Petrochemicals Plants.

Refineries: Overview The refinery segment encompasses the entire value chain of crude oil processing into fuels and other refined products. This includes analysis of existing infrastructure, projects in the pipeline for capacity expansion and modernization, and upcoming projects focused on technological upgrades and diversification. Growth projections for this segment are tied to global energy demand and Kuwait's strategic output targets. The market size is substantial, reflecting the capital-intensive nature of refining operations, with competitive dynamics shaped by operational efficiency and product portfolio.

Petrochemicals Plants: Overview The petrochemicals segment analyzes the production of chemical compounds derived from petroleum. Similar to refineries, this includes an assessment of existing infrastructure, projects in the pipeline for capacity growth and product diversification, and upcoming projects focused on advanced materials and specialty chemicals. Growth projections for this segment are driven by the increasing demand for polymers and intermediate chemicals in various end-use industries. The market size is significant and expected to grow as Kuwait seeks to monetize its hydrocarbon resources further. Competitive dynamics are influenced by feedstock availability, technological advancements, and global market demand for specific petrochemical derivatives.

Key Drivers of Kuwait Oil and Gas Downstream Market Growth

The growth of the Kuwait Oil and Gas Downstream Market is propelled by several interconnected drivers. Economic diversification strategies by the Kuwaiti government are a paramount influence, aiming to reduce reliance on crude oil exports by adding value domestically. Increasing global demand for refined products and petrochemicals, particularly from emerging economies, provides a strong export market. Significant government investments in infrastructure development and capacity expansion are directly fueling growth. Furthermore, the adoption of advanced technologies and digitalization is enhancing operational efficiency and competitiveness. The strategic location of Kuwait, providing access to key shipping routes, further bolsters export potential.

Challenges in the Kuwait Oil and Gas Downstream Market Sector

Despite robust growth potential, the Kuwait Oil and Gas Downstream Market faces several challenges. Regulatory hurdles and evolving environmental standards can impact project timelines and operational costs. Global price volatility for crude oil and petrochemicals poses a significant risk to profitability and investment decisions. Supply chain disruptions, as witnessed in recent global events, can affect the timely delivery of equipment and materials for new projects. Intensifying competition from other major producing nations with significant downstream capacities requires continuous innovation and cost optimization. The need for skilled human capital to operate and manage advanced facilities is another critical consideration.

Emerging Opportunities in Kuwait Oil and Gas Downstream Market

The Kuwait Oil and Gas Downstream Market is poised to capitalize on several emerging opportunities. The growing global emphasis on sustainability and the circular economy presents opportunities for developing green petrochemicals and advanced recycling technologies. Expansion into specialty chemicals and high-value derivatives offers higher profit margins and caters to niche markets. The digital transformation of the industry, including the implementation of AI and IoT, presents opportunities for enhanced efficiency, predictive maintenance, and improved safety. Furthermore, strategic partnerships and joint ventures with international companies can unlock new markets, technologies, and expertise.

Leading Players in the Kuwait Oil and Gas Downstream Market Market

- Total SA

- Kuwait Oil Company

- BP PLC

- Petrochemicals Industry Company

- Kuwait National Petroleum Company

Key Developments in Kuwait Oil and Gas Downstream Market Industry

- 2023: Kuwait National Petroleum Company (KNPC) continues aggressive expansion of its Clean Fuels Project, aiming to significantly upgrade refinery output.

- 2023: Petrochemicals Industry Company (PIC) announces plans for new polyolefins production units to meet growing regional demand.

- 2024: Kuwait Oil Company (KOC) explores advanced technologies for enhanced crude oil processing and higher downstream integration.

- 2024: International players like BP PLC and Total SA engage in discussions for potential collaborations on future downstream ventures in Kuwait.

Future Outlook for Kuwait Oil and Gas Downstream Market Market

The future outlook for the Kuwait Oil and Gas Downstream Market is highly promising, driven by continued strategic investments and a global demand for refined and petrochemical products. The market is expected to witness significant growth in capacity and a shift towards higher-value, specialized products. Key growth accelerators include the successful execution of ongoing and upcoming expansion projects, the adoption of cutting-edge digital technologies to optimize operations, and a sustained focus on sustainability initiatives. Strategic partnerships and the development of new export markets will further bolster Kuwait's position as a key player in the global downstream oil and gas arena. The market is well-positioned to benefit from the increasing demand for advanced materials and cleaner energy solutions.

Kuwait Oil and Gas Downstream Market Segmentation

-

1. Refineries

-

1.1. Overview

- 1.1.1. Existing Infrastructure

- 1.1.2. Projects in pipeline

- 1.1.3. Upcoming projects

-

1.1. Overview

-

2. Petrochemicals Plants

-

2.1. Overview

- 2.1.1. Existing Infrastructure

- 2.1.2. Projects in pipeline

- 2.1.3. Upcoming projects

-

2.1. Overview

Kuwait Oil and Gas Downstream Market Segmentation By Geography

- 1. Kuwait

Kuwait Oil and Gas Downstream Market Regional Market Share

Geographic Coverage of Kuwait Oil and Gas Downstream Market

Kuwait Oil and Gas Downstream Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 2.1% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Refineries

- 5.1.1. Overview

- 5.1.1.1. Existing Infrastructure

- 5.1.1.2. Projects in pipeline

- 5.1.1.3. Upcoming projects

- 5.1.1. Overview

- 5.2. Market Analysis, Insights and Forecast - by Petrochemicals Plants

- 5.2.1. Overview

- 5.2.1.1. Existing Infrastructure

- 5.2.1.2. Projects in pipeline

- 5.2.1.3. Upcoming projects

- 5.2.1. Overview

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Kuwait

- 5.1. Market Analysis, Insights and Forecast - by Refineries

- 6. Kuwait Oil and Gas Downstream Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Refineries

- 6.1.1. Overview

- 6.1.1.1. Existing Infrastructure

- 6.1.1.2. Projects in pipeline

- 6.1.1.3. Upcoming projects

- 6.1.1. Overview

- 6.2. Market Analysis, Insights and Forecast - by Petrochemicals Plants

- 6.2.1. Overview

- 6.2.1.1. Existing Infrastructure

- 6.2.1.2. Projects in pipeline

- 6.2.1.3. Upcoming projects

- 6.2.1. Overview

- 6.1. Market Analysis, Insights and Forecast - by Refineries

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Total SA

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Kuwait Oil Company

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 BP PLC

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Petrochemicals Industry Company

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Kuwait National Petroleum Company

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.1 Total SA

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Kuwait Oil and Gas Downstream Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Kuwait Oil and Gas Downstream Market Share (%) by Company 2025

List of Tables

- Table 1: Kuwait Oil and Gas Downstream Market Revenue billion Forecast, by Refineries 2020 & 2033

- Table 2: Kuwait Oil and Gas Downstream Market Revenue billion Forecast, by Petrochemicals Plants 2020 & 2033

- Table 3: Kuwait Oil and Gas Downstream Market Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Kuwait Oil and Gas Downstream Market Revenue billion Forecast, by Refineries 2020 & 2033

- Table 5: Kuwait Oil and Gas Downstream Market Revenue billion Forecast, by Petrochemicals Plants 2020 & 2033

- Table 6: Kuwait Oil and Gas Downstream Market Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Kuwait Oil and Gas Downstream Market?

The projected CAGR is approximately 2.1%.

2. Which companies are prominent players in the Kuwait Oil and Gas Downstream Market?

Key companies in the market include Total SA, Kuwait Oil Company, BP PLC, Petrochemicals Industry Company, Kuwait National Petroleum Company.

3. What are the main segments of the Kuwait Oil and Gas Downstream Market?

The market segments include Refineries, Petrochemicals Plants.

4. Can you provide details about the market size?

The market size is estimated to be USD 104 billion as of 2022.

5. What are some drivers contributing to market growth?

4.; Increasing investment in the downstream sector4.; Rising offshore Oil exploration activities.

6. What are the notable trends driving market growth?

Oil and Gas Refining Capacity to Witness Growth.

7. Are there any restraints impacting market growth?

4.; Rising adoption of cleaner alternatives.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Kuwait Oil and Gas Downstream Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Kuwait Oil and Gas Downstream Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Kuwait Oil and Gas Downstream Market?

To stay informed about further developments, trends, and reports in the Kuwait Oil and Gas Downstream Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence