Key Insights

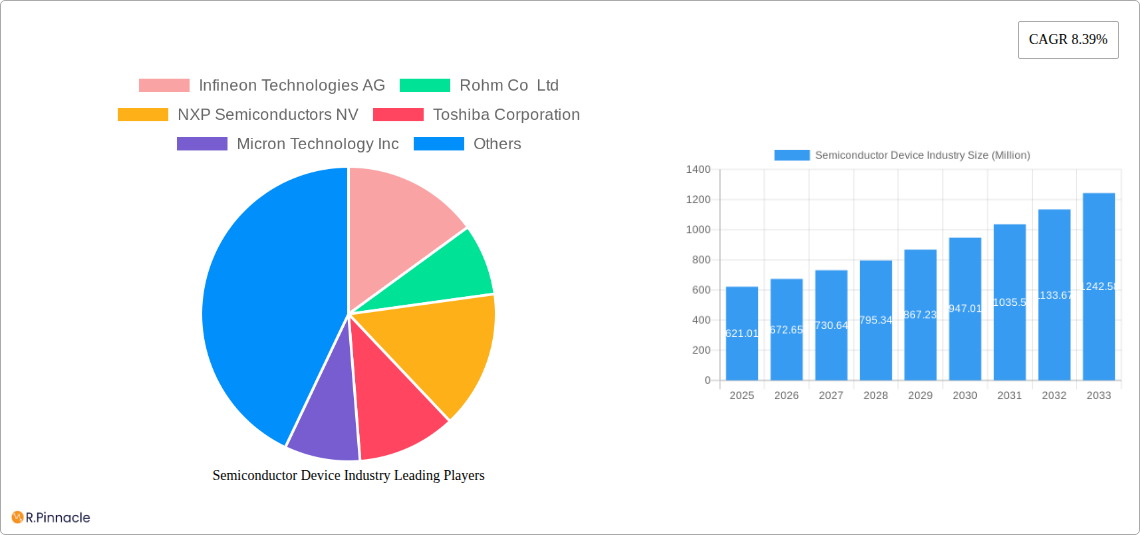

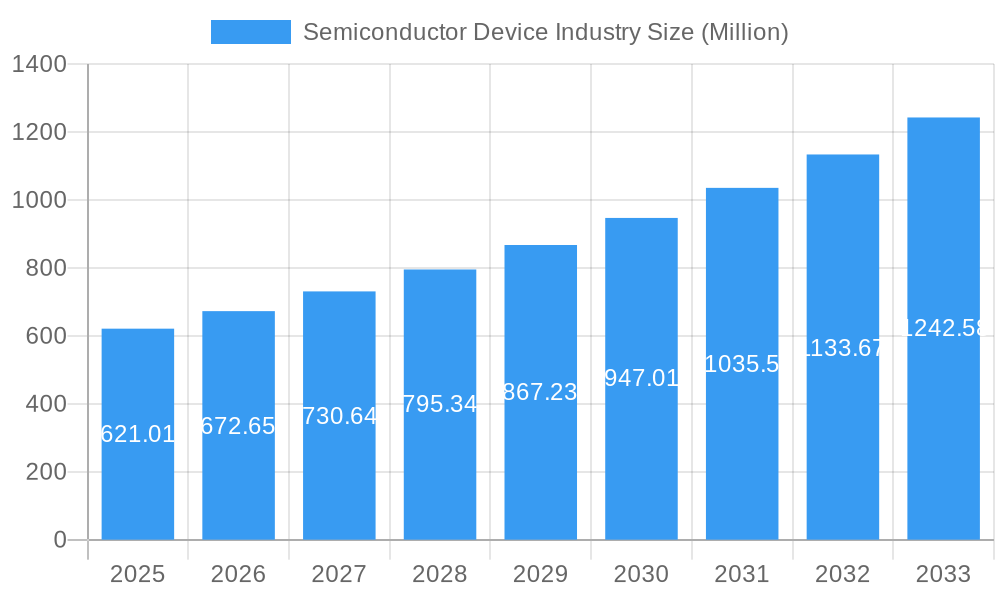

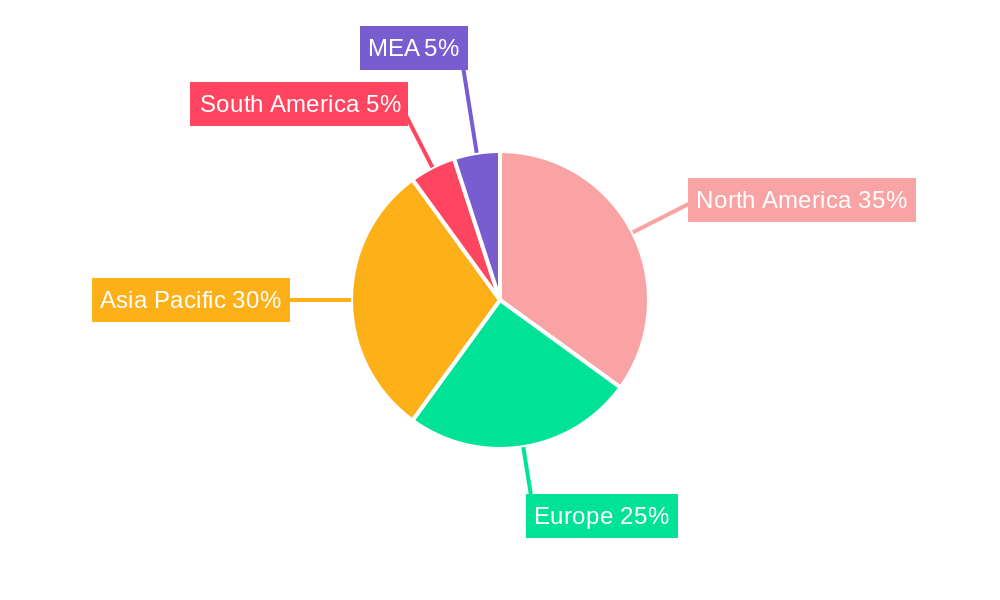

The global semiconductor device market, valued at $621.01 million in 2025, is projected to experience robust growth, driven by the increasing demand for advanced electronics across various sectors. The Compound Annual Growth Rate (CAGR) of 8.39% from 2025 to 2033 indicates a significant expansion, fueled by several key factors. The automotive industry's ongoing shift towards electric vehicles and advanced driver-assistance systems (ADAS) is a major driver, demanding sophisticated semiconductor components for power management, sensor integration, and in-vehicle computing. Furthermore, the proliferation of smart devices, the expansion of 5G and other wireless communication technologies, and the growing need for high-performance computing in data centers are all contributing to market expansion. The increasing adoption of IoT (Internet of Things) devices across diverse industries like industrial automation and consumer electronics also fuels the demand for diverse semiconductor components. Within the device type segment, integrated circuits (ICs) and microprocessors (MPUs) are projected to hold significant market share due to their crucial roles in high-performance computing and data processing. The market segmentation by end-user vertical reveals significant growth opportunities in automotive, communication, and computing sectors. Geographical analysis suggests North America and Asia Pacific will remain dominant regions, owing to established technological infrastructure and substantial manufacturing capabilities. However, emerging economies in regions like South America and MEA are expected to show considerable growth potential in the coming years.

Semiconductor Device Industry Market Size (In Million)

Competitive dynamics in the semiconductor device market are intense, with established players like Intel, Samsung, and Texas Instruments vying for market share alongside emerging companies focusing on niche technologies and specialized applications. The market is characterized by continuous innovation in materials, architectures, and manufacturing processes. Challenges such as supply chain disruptions, geopolitical uncertainties, and the need for sustainable manufacturing practices are expected to influence market growth trajectories. Nonetheless, the long-term prospects for the semiconductor device market remain positive, driven by technological advancements and increasing demand across all major application sectors. Strategic partnerships, mergers and acquisitions, and investments in research and development are likely to shape the competitive landscape further. The industry’s focus on miniaturization, power efficiency, and advanced functionalities will continue to drive innovation and market growth.

Semiconductor Device Industry Company Market Share

Semiconductor Device Industry Market Structure & Innovation Trends

This comprehensive report analyzes the semiconductor device industry, encompassing the period 2019-2033, with a focus on the year 2025. The market is characterized by a moderately concentrated structure, with key players like Intel, Samsung, and TSMC holding significant market share (xx%). However, the presence of numerous smaller, specialized companies fosters healthy competition. Innovation is driven by increasing demand for higher performance, energy efficiency, and miniaturization across various applications. Stringent regulatory frameworks, particularly regarding environmental impact and data security, influence industry practices. Product substitution is a continuous concern, with advancements in materials science and design constantly challenging established technologies. End-user demographics are shifting towards increased reliance on mobile and IoT devices, driving demand for specific semiconductor types. The historical period (2019-2024) witnessed significant M&A activity, with deal values exceeding xx Million, reflecting consolidation and strategic expansion efforts within the sector. Future M&A activity is projected at xx Million for the forecast period (2025-2033).

- Market Concentration: Moderately concentrated, with top players holding xx% market share.

- Innovation Drivers: Demand for higher performance, energy efficiency, and miniaturization.

- Regulatory Frameworks: Stringent environmental and data security regulations.

- M&A Activity (2019-2024): Deal values exceeding xx Million. Projected at xx Million (2025-2033).

Semiconductor Device Industry Market Dynamics & Trends

The global semiconductor device market exhibits robust growth, projected to achieve a CAGR of xx% during the forecast period (2025-2033). Key growth drivers include the proliferation of smart devices, the expanding automotive electronics market, and the burgeoning demand for high-performance computing in data centers and artificial intelligence. Technological disruptions, particularly the advancement of 5G and AI technologies, are reshaping the industry landscape, creating new opportunities and challenges. Consumer preferences increasingly favor energy-efficient, high-performance devices, driving demand for advanced semiconductor technologies. Competitive dynamics are intense, with companies vying for market share through innovation, strategic partnerships, and aggressive pricing strategies. Market penetration of advanced semiconductor technologies, such as GaN and SiC, is steadily increasing, driven by their superior performance characteristics.

Dominant Regions & Segments in Semiconductor Device Industry

The Asia-Pacific region currently holds the dominant position in the semiconductor device market, driven by a strong manufacturing base, supportive government policies, and a large consumer market. Within specific segments:

By End-user Vertical:

- Computing/Data Storage: This segment is experiencing significant growth due to the increasing demand for high-performance computing and data storage solutions, particularly in cloud computing and AI. Key drivers include the growth of big data analytics and the increasing adoption of cloud computing infrastructure.

- Automotive: The rapid adoption of advanced driver-assistance systems (ADAS) and electric vehicles (EVs) is fueling strong growth in this segment. Key drivers include government regulations promoting the adoption of EVs and the increasing complexity of automotive electronics.

By Device Type:

- Integrated Circuits: This segment dominates the market due to its widespread application across various electronic devices.

- Microprocessors (MPU): This segment is driven by the growing demand for high-performance computing in data centers and AI applications.

Key Drivers: Government support for technological advancement, robust infrastructure, and a highly skilled workforce.

Semiconductor Device Industry Product Innovations

Recent product innovations showcase advancements in processing power, energy efficiency, and specialized functionalities. The introduction of Intel's 14th Gen Core processors and Nvidia's GeForce RTX 40 SUPER Series GPUs exemplifies this trend, delivering significant performance improvements for both computing and gaming applications. These innovations are tailored to meet the demands of high-growth markets like AI and gaming, ensuring strong market fit and competitive advantage.

Report Scope & Segmentation Analysis

This report provides a comprehensive analysis of the semiconductor device market, segmented by end-user vertical (Automotive, Communication, Consumer, Industrial, Computing/Data Storage, Government) and device type (Discrete Semiconductors, Optoelectronics, Sensors, Integrated Circuits, Microprocessors, Microcontrollers, Digital Signal Processors). Each segment's growth projections, market size estimates, and competitive dynamics are analyzed in detail, offering a granular view of the market landscape. For instance, the automotive segment shows strong growth due to the increasing adoption of advanced driver-assistance systems (ADAS) and electric vehicles (EVs), while the Computing/Data Storage segment is driven by the growing demand for high-performance computing and data storage solutions.

Key Drivers of Semiconductor Device Industry Growth

Several factors fuel the growth of the semiconductor device industry. Technological advancements, particularly in AI, 5G, and IoT, create vast demand for advanced semiconductors. Economic expansion, particularly in emerging economies, increases consumer spending on electronics. Government incentives and policies encouraging semiconductor manufacturing and R&D also contribute significantly. For example, the US CHIPS and Science Act is designed to boost domestic semiconductor production.

Challenges in the Semiconductor Device Industry Sector

The semiconductor industry faces significant challenges, including volatile raw material pricing increasing production costs by xx%. Supply chain disruptions cause production delays and shortages, impacting revenue by xx Million annually. Geopolitical instability disrupts trade routes, leading to uncertain market conditions and increases in transportation costs. Intense competition requires continuous innovation and cost optimization to maintain profitability.

Emerging Opportunities in Semiconductor Device Industry

Emerging opportunities lie in the expanding automotive, IoT, and AI sectors. Growth in new applications like autonomous vehicles and edge computing is creating significant demand for specialized semiconductor devices. Advancements in materials science, packaging, and design are opening doors to enhanced performance and functionality. The rising demand for energy-efficient devices offers significant potential for companies focusing on low-power semiconductor technologies.

Leading Players in the Semiconductor Device Industry Market

- Infineon Technologies AG

- Rohm Co Ltd

- NXP Semiconductors NV

- Toshiba Corporation

- Micron Technology Inc

- Kyocera Corporation

- Texas Instruments Inc

- Samsung Electronics Co Ltd

- Broadcom Inc

- Wolfspeed Inc

- STMicroelectronics NV

- Qualcomm Incorporated

- Advanced Micro Devices Inc

- ON Semiconductor Corporation

- Renesas Electronics Corporation

- SK Hynix Inc

- Analog Devices Inc

- Nvidia Corporation

- Intel Corporation

- Fujitsu Semiconductor Ltd

Key Developments in Semiconductor Device Industry Industry

- January 2024: Intel launched its 14th Gen Core mobile and desktop processor families, featuring up to 24 cores and improved performance.

- January 2024: Nvidia announced the GeForce RTX 40 SUPER Series GPUs, offering enhanced performance for gaming and AI applications.

Future Outlook for Semiconductor Device Industry Market

The semiconductor device market is poised for continued strong growth, driven by technological advancements and expanding applications across various sectors. Strategic investments in R&D, expansion into new markets, and strategic partnerships will be crucial for success. The focus on energy efficiency, miniaturization, and specialized functionalities will define future market leaders. The industry's long-term prospects remain positive, with significant growth potential across diverse applications.

Semiconductor Device Industry Segmentation

-

1. Device Type

- 1.1. Discrete Semiconductors

- 1.2. Optoelectronics

- 1.3. Sensors

-

1.4. Integrated Circuits

- 1.4.1. Analog

- 1.4.2. Logic

- 1.4.3. Memory

-

1.4.4. Micro

- 1.4.4.1. Microprocessors (MPU)

- 1.4.4.2. Microcontrollers (MCU)

- 1.4.4.3. Digital Signal Processors

-

2. End-user Vertical

- 2.1. Automotive

- 2.2. Communication (Wired and Wireless)

- 2.3. Consumer

- 2.4. Industrial

- 2.5. Computing/Data Storage

- 2.6. Government (Aerospace and Defense)

Semiconductor Device Industry Segmentation By Geography

- 1. United States

- 2. Europe

- 3. Japan

- 4. China

- 5. Korea

- 6. Taiwan

- 7. Rest of the World

Semiconductor Device Industry Regional Market Share

Geographic Coverage of Semiconductor Device Industry

Semiconductor Device Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.39% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Device Type

- 5.1.1. Discrete Semiconductors

- 5.1.2. Optoelectronics

- 5.1.3. Sensors

- 5.1.4. Integrated Circuits

- 5.1.4.1. Analog

- 5.1.4.2. Logic

- 5.1.4.3. Memory

- 5.1.4.4. Micro

- 5.1.4.4.1. Microprocessors (MPU)

- 5.1.4.4.2. Microcontrollers (MCU)

- 5.1.4.4.3. Digital Signal Processors

- 5.2. Market Analysis, Insights and Forecast - by End-user Vertical

- 5.2.1. Automotive

- 5.2.2. Communication (Wired and Wireless)

- 5.2.3. Consumer

- 5.2.4. Industrial

- 5.2.5. Computing/Data Storage

- 5.2.6. Government (Aerospace and Defense)

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. United States

- 5.3.2. Europe

- 5.3.3. Japan

- 5.3.4. China

- 5.3.5. Korea

- 5.3.6. Taiwan

- 5.3.7. Rest of the World

- 5.1. Market Analysis, Insights and Forecast - by Device Type

- 6. Global Semiconductor Device Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Device Type

- 6.1.1. Discrete Semiconductors

- 6.1.2. Optoelectronics

- 6.1.3. Sensors

- 6.1.4. Integrated Circuits

- 6.1.4.1. Analog

- 6.1.4.2. Logic

- 6.1.4.3. Memory

- 6.1.4.4. Micro

- 6.1.4.4.1. Microprocessors (MPU)

- 6.1.4.4.2. Microcontrollers (MCU)

- 6.1.4.4.3. Digital Signal Processors

- 6.2. Market Analysis, Insights and Forecast - by End-user Vertical

- 6.2.1. Automotive

- 6.2.2. Communication (Wired and Wireless)

- 6.2.3. Consumer

- 6.2.4. Industrial

- 6.2.5. Computing/Data Storage

- 6.2.6. Government (Aerospace and Defense)

- 6.1. Market Analysis, Insights and Forecast - by Device Type

- 7. United States Semiconductor Device Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Device Type

- 7.1.1. Discrete Semiconductors

- 7.1.2. Optoelectronics

- 7.1.3. Sensors

- 7.1.4. Integrated Circuits

- 7.1.4.1. Analog

- 7.1.4.2. Logic

- 7.1.4.3. Memory

- 7.1.4.4. Micro

- 7.1.4.4.1. Microprocessors (MPU)

- 7.1.4.4.2. Microcontrollers (MCU)

- 7.1.4.4.3. Digital Signal Processors

- 7.2. Market Analysis, Insights and Forecast - by End-user Vertical

- 7.2.1. Automotive

- 7.2.2. Communication (Wired and Wireless)

- 7.2.3. Consumer

- 7.2.4. Industrial

- 7.2.5. Computing/Data Storage

- 7.2.6. Government (Aerospace and Defense)

- 7.1. Market Analysis, Insights and Forecast - by Device Type

- 8. Europe Semiconductor Device Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Device Type

- 8.1.1. Discrete Semiconductors

- 8.1.2. Optoelectronics

- 8.1.3. Sensors

- 8.1.4. Integrated Circuits

- 8.1.4.1. Analog

- 8.1.4.2. Logic

- 8.1.4.3. Memory

- 8.1.4.4. Micro

- 8.1.4.4.1. Microprocessors (MPU)

- 8.1.4.4.2. Microcontrollers (MCU)

- 8.1.4.4.3. Digital Signal Processors

- 8.2. Market Analysis, Insights and Forecast - by End-user Vertical

- 8.2.1. Automotive

- 8.2.2. Communication (Wired and Wireless)

- 8.2.3. Consumer

- 8.2.4. Industrial

- 8.2.5. Computing/Data Storage

- 8.2.6. Government (Aerospace and Defense)

- 8.1. Market Analysis, Insights and Forecast - by Device Type

- 9. Japan Semiconductor Device Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Device Type

- 9.1.1. Discrete Semiconductors

- 9.1.2. Optoelectronics

- 9.1.3. Sensors

- 9.1.4. Integrated Circuits

- 9.1.4.1. Analog

- 9.1.4.2. Logic

- 9.1.4.3. Memory

- 9.1.4.4. Micro

- 9.1.4.4.1. Microprocessors (MPU)

- 9.1.4.4.2. Microcontrollers (MCU)

- 9.1.4.4.3. Digital Signal Processors

- 9.2. Market Analysis, Insights and Forecast - by End-user Vertical

- 9.2.1. Automotive

- 9.2.2. Communication (Wired and Wireless)

- 9.2.3. Consumer

- 9.2.4. Industrial

- 9.2.5. Computing/Data Storage

- 9.2.6. Government (Aerospace and Defense)

- 9.1. Market Analysis, Insights and Forecast - by Device Type

- 10. China Semiconductor Device Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Device Type

- 10.1.1. Discrete Semiconductors

- 10.1.2. Optoelectronics

- 10.1.3. Sensors

- 10.1.4. Integrated Circuits

- 10.1.4.1. Analog

- 10.1.4.2. Logic

- 10.1.4.3. Memory

- 10.1.4.4. Micro

- 10.1.4.4.1. Microprocessors (MPU)

- 10.1.4.4.2. Microcontrollers (MCU)

- 10.1.4.4.3. Digital Signal Processors

- 10.2. Market Analysis, Insights and Forecast - by End-user Vertical

- 10.2.1. Automotive

- 10.2.2. Communication (Wired and Wireless)

- 10.2.3. Consumer

- 10.2.4. Industrial

- 10.2.5. Computing/Data Storage

- 10.2.6. Government (Aerospace and Defense)

- 10.1. Market Analysis, Insights and Forecast - by Device Type

- 11. Korea Semiconductor Device Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Device Type

- 11.1.1. Discrete Semiconductors

- 11.1.2. Optoelectronics

- 11.1.3. Sensors

- 11.1.4. Integrated Circuits

- 11.1.4.1. Analog

- 11.1.4.2. Logic

- 11.1.4.3. Memory

- 11.1.4.4. Micro

- 11.1.4.4.1. Microprocessors (MPU)

- 11.1.4.4.2. Microcontrollers (MCU)

- 11.1.4.4.3. Digital Signal Processors

- 11.2. Market Analysis, Insights and Forecast - by End-user Vertical

- 11.2.1. Automotive

- 11.2.2. Communication (Wired and Wireless)

- 11.2.3. Consumer

- 11.2.4. Industrial

- 11.2.5. Computing/Data Storage

- 11.2.6. Government (Aerospace and Defense)

- 11.1. Market Analysis, Insights and Forecast - by Device Type

- 12. Taiwan Semiconductor Device Industry Analysis, Insights and Forecast, 2020-2032

- 12.1. Market Analysis, Insights and Forecast - by Device Type

- 12.1.1. Discrete Semiconductors

- 12.1.2. Optoelectronics

- 12.1.3. Sensors

- 12.1.4. Integrated Circuits

- 12.1.4.1. Analog

- 12.1.4.2. Logic

- 12.1.4.3. Memory

- 12.1.4.4. Micro

- 12.1.4.4.1. Microprocessors (MPU)

- 12.1.4.4.2. Microcontrollers (MCU)

- 12.1.4.4.3. Digital Signal Processors

- 12.2. Market Analysis, Insights and Forecast - by End-user Vertical

- 12.2.1. Automotive

- 12.2.2. Communication (Wired and Wireless)

- 12.2.3. Consumer

- 12.2.4. Industrial

- 12.2.5. Computing/Data Storage

- 12.2.6. Government (Aerospace and Defense)

- 12.1. Market Analysis, Insights and Forecast - by Device Type

- 13. Rest of the World Semiconductor Device Industry Analysis, Insights and Forecast, 2020-2032

- 13.1. Market Analysis, Insights and Forecast - by Device Type

- 13.1.1. Discrete Semiconductors

- 13.1.2. Optoelectronics

- 13.1.3. Sensors

- 13.1.4. Integrated Circuits

- 13.1.4.1. Analog

- 13.1.4.2. Logic

- 13.1.4.3. Memory

- 13.1.4.4. Micro

- 13.1.4.4.1. Microprocessors (MPU)

- 13.1.4.4.2. Microcontrollers (MCU)

- 13.1.4.4.3. Digital Signal Processors

- 13.2. Market Analysis, Insights and Forecast - by End-user Vertical

- 13.2.1. Automotive

- 13.2.2. Communication (Wired and Wireless)

- 13.2.3. Consumer

- 13.2.4. Industrial

- 13.2.5. Computing/Data Storage

- 13.2.6. Government (Aerospace and Defense)

- 13.1. Market Analysis, Insights and Forecast - by Device Type

- 14. Competitive Analysis

- 14.1. Company Profiles

- 14.1.1 Infineon Technologies AG

- 14.1.1.1. Company Overview

- 14.1.1.2. Products

- 14.1.1.3. Company Financials

- 14.1.1.4. SWOT Analysis

- 14.1.2 Rohm Co Ltd

- 14.1.2.1. Company Overview

- 14.1.2.2. Products

- 14.1.2.3. Company Financials

- 14.1.2.4. SWOT Analysis

- 14.1.3 NXP Semiconductors NV

- 14.1.3.1. Company Overview

- 14.1.3.2. Products

- 14.1.3.3. Company Financials

- 14.1.3.4. SWOT Analysis

- 14.1.4 Toshiba Corporation

- 14.1.4.1. Company Overview

- 14.1.4.2. Products

- 14.1.4.3. Company Financials

- 14.1.4.4. SWOT Analysis

- 14.1.5 Micron Technology Inc

- 14.1.5.1. Company Overview

- 14.1.5.2. Products

- 14.1.5.3. Company Financials

- 14.1.5.4. SWOT Analysis

- 14.1.6 Kyocera Corporation

- 14.1.6.1. Company Overview

- 14.1.6.2. Products

- 14.1.6.3. Company Financials

- 14.1.6.4. SWOT Analysis

- 14.1.7 Texas Instruments Inc

- 14.1.7.1. Company Overview

- 14.1.7.2. Products

- 14.1.7.3. Company Financials

- 14.1.7.4. SWOT Analysis

- 14.1.8 Samsung Electronics Co Ltd

- 14.1.8.1. Company Overview

- 14.1.8.2. Products

- 14.1.8.3. Company Financials

- 14.1.8.4. SWOT Analysis

- 14.1.9 Broadcom Inc

- 14.1.9.1. Company Overview

- 14.1.9.2. Products

- 14.1.9.3. Company Financials

- 14.1.9.4. SWOT Analysis

- 14.1.10 Wolfspeed Inc

- 14.1.10.1. Company Overview

- 14.1.10.2. Products

- 14.1.10.3. Company Financials

- 14.1.10.4. SWOT Analysis

- 14.1.11 STMicroelectronics NV

- 14.1.11.1. Company Overview

- 14.1.11.2. Products

- 14.1.11.3. Company Financials

- 14.1.11.4. SWOT Analysis

- 14.1.12 Qualcomm Incorporated

- 14.1.12.1. Company Overview

- 14.1.12.2. Products

- 14.1.12.3. Company Financials

- 14.1.12.4. SWOT Analysis

- 14.1.13 Advanced Micro Devices Inc

- 14.1.13.1. Company Overview

- 14.1.13.2. Products

- 14.1.13.3. Company Financials

- 14.1.13.4. SWOT Analysis

- 14.1.14 ON Semiconductor Corporatio

- 14.1.14.1. Company Overview

- 14.1.14.2. Products

- 14.1.14.3. Company Financials

- 14.1.14.4. SWOT Analysis

- 14.1.15 Renesas Electronics Corporation

- 14.1.15.1. Company Overview

- 14.1.15.2. Products

- 14.1.15.3. Company Financials

- 14.1.15.4. SWOT Analysis

- 14.1.16 SK Hynix Inc

- 14.1.16.1. Company Overview

- 14.1.16.2. Products

- 14.1.16.3. Company Financials

- 14.1.16.4. SWOT Analysis

- 14.1.17 Analog Devices Inc

- 14.1.17.1. Company Overview

- 14.1.17.2. Products

- 14.1.17.3. Company Financials

- 14.1.17.4. SWOT Analysis

- 14.1.18 Nvidia Corporation

- 14.1.18.1. Company Overview

- 14.1.18.2. Products

- 14.1.18.3. Company Financials

- 14.1.18.4. SWOT Analysis

- 14.1.19 Intel Corporation

- 14.1.19.1. Company Overview

- 14.1.19.2. Products

- 14.1.19.3. Company Financials

- 14.1.19.4. SWOT Analysis

- 14.1.20 Fujitsu Semiconductor Ltd

- 14.1.20.1. Company Overview

- 14.1.20.2. Products

- 14.1.20.3. Company Financials

- 14.1.20.4. SWOT Analysis

- 14.1.1 Infineon Technologies AG

- 14.2. Market Entropy

- 14.2.1 Company's Key Areas Served

- 14.2.2 Recent Developments

- 14.3. Company Market Share Analysis 2025

- 14.3.1 Top 5 Companies Market Share Analysis

- 14.3.2 Top 3 Companies Market Share Analysis

- 14.4. List of Potential Customers

- 15. Research Methodology

List of Figures

- Figure 1: Global Semiconductor Device Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: United States Semiconductor Device Industry Revenue (Million), by Device Type 2025 & 2033

- Figure 3: United States Semiconductor Device Industry Revenue Share (%), by Device Type 2025 & 2033

- Figure 4: United States Semiconductor Device Industry Revenue (Million), by End-user Vertical 2025 & 2033

- Figure 5: United States Semiconductor Device Industry Revenue Share (%), by End-user Vertical 2025 & 2033

- Figure 6: United States Semiconductor Device Industry Revenue (Million), by Country 2025 & 2033

- Figure 7: United States Semiconductor Device Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe Semiconductor Device Industry Revenue (Million), by Device Type 2025 & 2033

- Figure 9: Europe Semiconductor Device Industry Revenue Share (%), by Device Type 2025 & 2033

- Figure 10: Europe Semiconductor Device Industry Revenue (Million), by End-user Vertical 2025 & 2033

- Figure 11: Europe Semiconductor Device Industry Revenue Share (%), by End-user Vertical 2025 & 2033

- Figure 12: Europe Semiconductor Device Industry Revenue (Million), by Country 2025 & 2033

- Figure 13: Europe Semiconductor Device Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Japan Semiconductor Device Industry Revenue (Million), by Device Type 2025 & 2033

- Figure 15: Japan Semiconductor Device Industry Revenue Share (%), by Device Type 2025 & 2033

- Figure 16: Japan Semiconductor Device Industry Revenue (Million), by End-user Vertical 2025 & 2033

- Figure 17: Japan Semiconductor Device Industry Revenue Share (%), by End-user Vertical 2025 & 2033

- Figure 18: Japan Semiconductor Device Industry Revenue (Million), by Country 2025 & 2033

- Figure 19: Japan Semiconductor Device Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: China Semiconductor Device Industry Revenue (Million), by Device Type 2025 & 2033

- Figure 21: China Semiconductor Device Industry Revenue Share (%), by Device Type 2025 & 2033

- Figure 22: China Semiconductor Device Industry Revenue (Million), by End-user Vertical 2025 & 2033

- Figure 23: China Semiconductor Device Industry Revenue Share (%), by End-user Vertical 2025 & 2033

- Figure 24: China Semiconductor Device Industry Revenue (Million), by Country 2025 & 2033

- Figure 25: China Semiconductor Device Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Korea Semiconductor Device Industry Revenue (Million), by Device Type 2025 & 2033

- Figure 27: Korea Semiconductor Device Industry Revenue Share (%), by Device Type 2025 & 2033

- Figure 28: Korea Semiconductor Device Industry Revenue (Million), by End-user Vertical 2025 & 2033

- Figure 29: Korea Semiconductor Device Industry Revenue Share (%), by End-user Vertical 2025 & 2033

- Figure 30: Korea Semiconductor Device Industry Revenue (Million), by Country 2025 & 2033

- Figure 31: Korea Semiconductor Device Industry Revenue Share (%), by Country 2025 & 2033

- Figure 32: Taiwan Semiconductor Device Industry Revenue (Million), by Device Type 2025 & 2033

- Figure 33: Taiwan Semiconductor Device Industry Revenue Share (%), by Device Type 2025 & 2033

- Figure 34: Taiwan Semiconductor Device Industry Revenue (Million), by End-user Vertical 2025 & 2033

- Figure 35: Taiwan Semiconductor Device Industry Revenue Share (%), by End-user Vertical 2025 & 2033

- Figure 36: Taiwan Semiconductor Device Industry Revenue (Million), by Country 2025 & 2033

- Figure 37: Taiwan Semiconductor Device Industry Revenue Share (%), by Country 2025 & 2033

- Figure 38: Rest of the World Semiconductor Device Industry Revenue (Million), by Device Type 2025 & 2033

- Figure 39: Rest of the World Semiconductor Device Industry Revenue Share (%), by Device Type 2025 & 2033

- Figure 40: Rest of the World Semiconductor Device Industry Revenue (Million), by End-user Vertical 2025 & 2033

- Figure 41: Rest of the World Semiconductor Device Industry Revenue Share (%), by End-user Vertical 2025 & 2033

- Figure 42: Rest of the World Semiconductor Device Industry Revenue (Million), by Country 2025 & 2033

- Figure 43: Rest of the World Semiconductor Device Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Semiconductor Device Industry Revenue Million Forecast, by Device Type 2020 & 2033

- Table 2: Global Semiconductor Device Industry Revenue Million Forecast, by End-user Vertical 2020 & 2033

- Table 3: Global Semiconductor Device Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Global Semiconductor Device Industry Revenue Million Forecast, by Device Type 2020 & 2033

- Table 5: Global Semiconductor Device Industry Revenue Million Forecast, by End-user Vertical 2020 & 2033

- Table 6: Global Semiconductor Device Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 7: Global Semiconductor Device Industry Revenue Million Forecast, by Device Type 2020 & 2033

- Table 8: Global Semiconductor Device Industry Revenue Million Forecast, by End-user Vertical 2020 & 2033

- Table 9: Global Semiconductor Device Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 10: Global Semiconductor Device Industry Revenue Million Forecast, by Device Type 2020 & 2033

- Table 11: Global Semiconductor Device Industry Revenue Million Forecast, by End-user Vertical 2020 & 2033

- Table 12: Global Semiconductor Device Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 13: Global Semiconductor Device Industry Revenue Million Forecast, by Device Type 2020 & 2033

- Table 14: Global Semiconductor Device Industry Revenue Million Forecast, by End-user Vertical 2020 & 2033

- Table 15: Global Semiconductor Device Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Global Semiconductor Device Industry Revenue Million Forecast, by Device Type 2020 & 2033

- Table 17: Global Semiconductor Device Industry Revenue Million Forecast, by End-user Vertical 2020 & 2033

- Table 18: Global Semiconductor Device Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 19: Global Semiconductor Device Industry Revenue Million Forecast, by Device Type 2020 & 2033

- Table 20: Global Semiconductor Device Industry Revenue Million Forecast, by End-user Vertical 2020 & 2033

- Table 21: Global Semiconductor Device Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 22: Global Semiconductor Device Industry Revenue Million Forecast, by Device Type 2020 & 2033

- Table 23: Global Semiconductor Device Industry Revenue Million Forecast, by End-user Vertical 2020 & 2033

- Table 24: Global Semiconductor Device Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Semiconductor Device Industry?

The projected CAGR is approximately 8.39%.

2. Which companies are prominent players in the Semiconductor Device Industry?

Key companies in the market include Infineon Technologies AG, Rohm Co Ltd, NXP Semiconductors NV, Toshiba Corporation, Micron Technology Inc, Kyocera Corporation, Texas Instruments Inc, Samsung Electronics Co Ltd, Broadcom Inc, Wolfspeed Inc, STMicroelectronics NV, Qualcomm Incorporated, Advanced Micro Devices Inc, ON Semiconductor Corporatio, Renesas Electronics Corporation, SK Hynix Inc, Analog Devices Inc, Nvidia Corporation, Intel Corporation, Fujitsu Semiconductor Ltd.

3. What are the main segments of the Semiconductor Device Industry?

The market segments include Device Type, End-user Vertical.

4. Can you provide details about the market size?

The market size is estimated to be USD 621.01 Million as of 2022.

5. What are some drivers contributing to market growth?

Growing Adoption of Technologies like IoT and AI; Increased Deployment of 5G and Rising Demand for 5G Smartphones.

6. What are the notable trends driving market growth?

Communication Industry to be the Largest End User.

7. Are there any restraints impacting market growth?

Limited AI Hardware Experts Coupled with Infrastructural Concerns.

8. Can you provide examples of recent developments in the market?

January 2024 - Intel introduced its latest offering, the Intel® Core 14th Gen mobile processor family. Spearheading this release is the flagship Intel® Core i9-14900HX, boasting an impressive 24 cores and promising the pinnacle of mobile experiences for enthusiasts. Additionally, Intel rolls out its full range of Intel Core 14th Gen desktop processors, available in both 65-watt and 35-watt configurations. These processors cater to a broad spectrum of devices, from mainstream desktops to all-in-one and edge devices.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Semiconductor Device Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Semiconductor Device Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Semiconductor Device Industry?

To stay informed about further developments, trends, and reports in the Semiconductor Device Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence