Key Insights

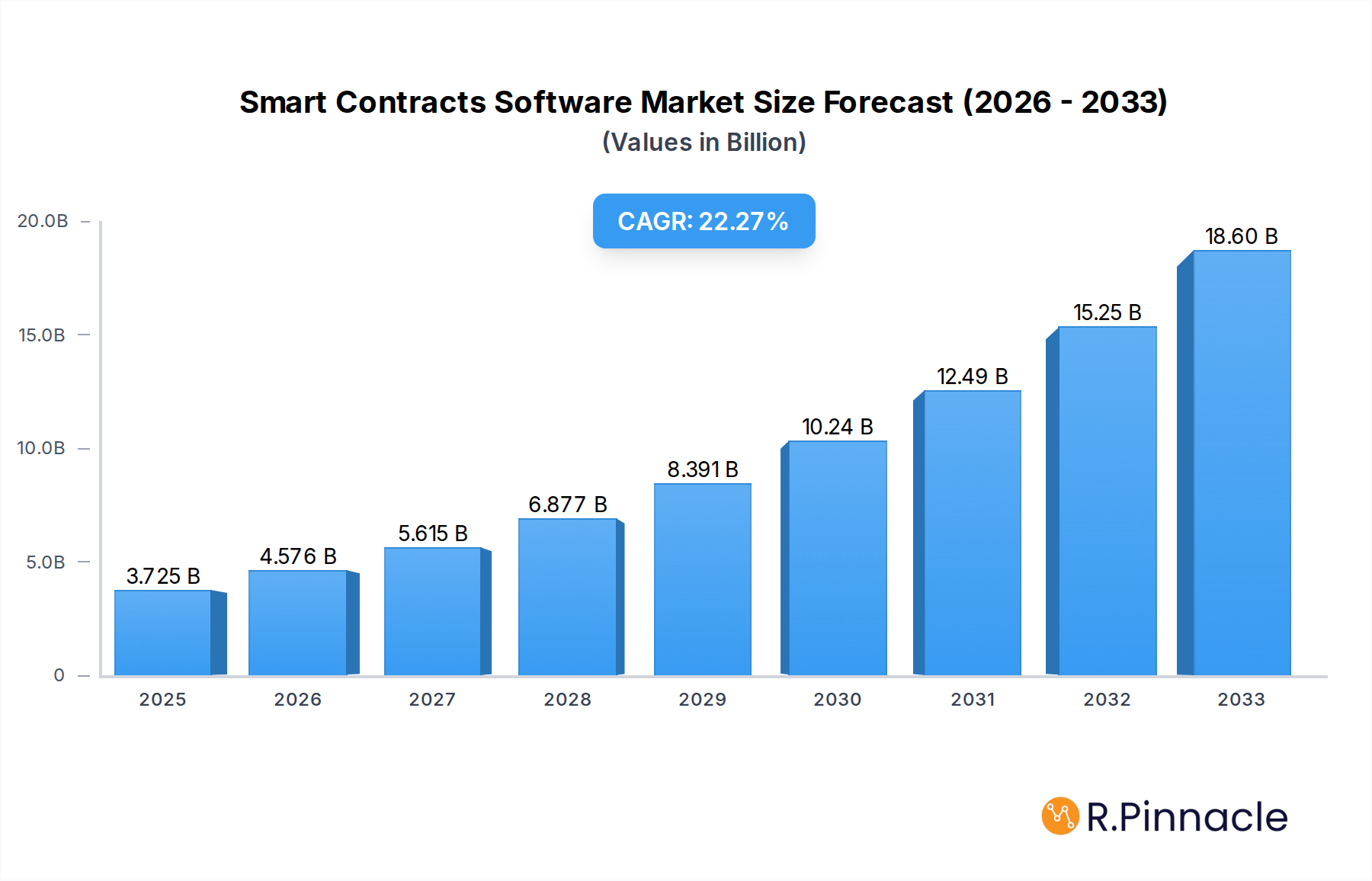

The global Smart Contracts Software market is experiencing robust expansion, projected to reach $3725 million by 2025, with an impressive Compound Annual Growth Rate (CAGR) of 24.2%. This significant growth is propelled by the increasing adoption of blockchain technology across various industries, including finance, supply chain management, and healthcare. Smart contracts, by enabling automated, secure, and transparent execution of agreements without intermediaries, are revolutionizing business processes. Key drivers include the growing demand for enhanced security in transactions, the need for operational efficiency through automation, and the inherent cost-saving potential they offer. The market is segmented by application into Large Enterprises and SMEs, with both segments demonstrating strong adoption patterns as businesses of all sizes recognize the benefits of smart contract solutions.

Smart Contracts Software Market Size (In Billion)

The market's trajectory is further bolstered by technological advancements and the continuous innovation within the blockchain space. Cloud-based solutions are witnessing rapid adoption due to their scalability, flexibility, and lower upfront costs, catering to a broader range of businesses, especially SMEs. However, on-premises solutions continue to hold relevance for organizations with stringent security and data sovereignty requirements. Emerging trends such as decentralized finance (DeFi), non-fungible tokens (NFTs), and their integration with smart contracts are opening up new avenues for market growth. While the market is characterized by significant opportunities, potential restraints include regulatory uncertainties, the complexity of implementation, and the need for skilled professionals to develop and manage smart contract applications. Leading companies like Ethereum, Corda, and Hyperledger are at the forefront of driving innovation and market penetration.

Smart Contracts Software Company Market Share

This in-depth report offers a meticulous examination of the global smart contracts software market, providing critical insights into its evolution, dynamics, and future trajectory. Designed for industry professionals, investors, and strategists, this analysis leverages high-ranking keywords to enhance visibility and deliver actionable intelligence. The study period spans from 2019 to 2033, with a base year of 2025 and a forecast period extending from 2025 to 2033.

Smart Contracts Software Market Structure & Innovation Trends

The smart contracts software market exhibits a dynamic structure characterized by a moderate level of concentration, with key players like Ethereum, Corda, and Hyperledger dominating innovation and adoption. The primary drivers of innovation stem from advancements in blockchain technology, increased demand for automated and transparent business processes, and the development of more sophisticated smart contract languages and platforms. Regulatory frameworks are evolving, with ongoing efforts to establish clear guidelines for smart contract enforceability and security, influencing market adoption across various sectors. Product substitutes, while emerging in the form of traditional automated contract solutions, often lack the inherent immutability and decentralization offered by smart contracts. End-user demographics are increasingly skewed towards large enterprises seeking to streamline complex transactions, but SMEs are also recognizing the cost-saving and efficiency benefits. Mergers and acquisitions (M&A) activity is on the rise, with deal values estimated to reach tens of millions, as established technology giants and blockchain startups consolidate their positions and expand their offerings. The market share of leading smart contract platforms is projected to see significant shifts as new technologies gain traction.

Smart Contracts Software Market Dynamics & Trends

The smart contracts software market is experiencing robust growth, driven by an insatiable appetite for enhanced efficiency, transparency, and automation across diverse industries. Technological disruptions are at the forefront, with continuous advancements in blockchain scalability, interoperability, and security fueling the development of more powerful and versatile smart contract solutions. The rising adoption of decentralized applications (dApps) and the increasing complexity of global supply chains are significant market growth drivers, compelling businesses to seek immutable and self-executing agreements. Consumer preferences are shifting towards platforms that offer user-friendly interfaces, robust security features, and cost-effectiveness, making cloud-based solutions increasingly popular. Competitive dynamics are intensifying, with a mix of established tech giants and agile blockchain startups vying for market dominance. The market penetration of smart contracts is projected to accelerate as regulatory clarity improves and the demonstrable benefits of automated agreements become more widely recognized. The compound annual growth rate (CAGR) for the smart contracts software market is anticipated to be substantial, reflecting its transformative potential.

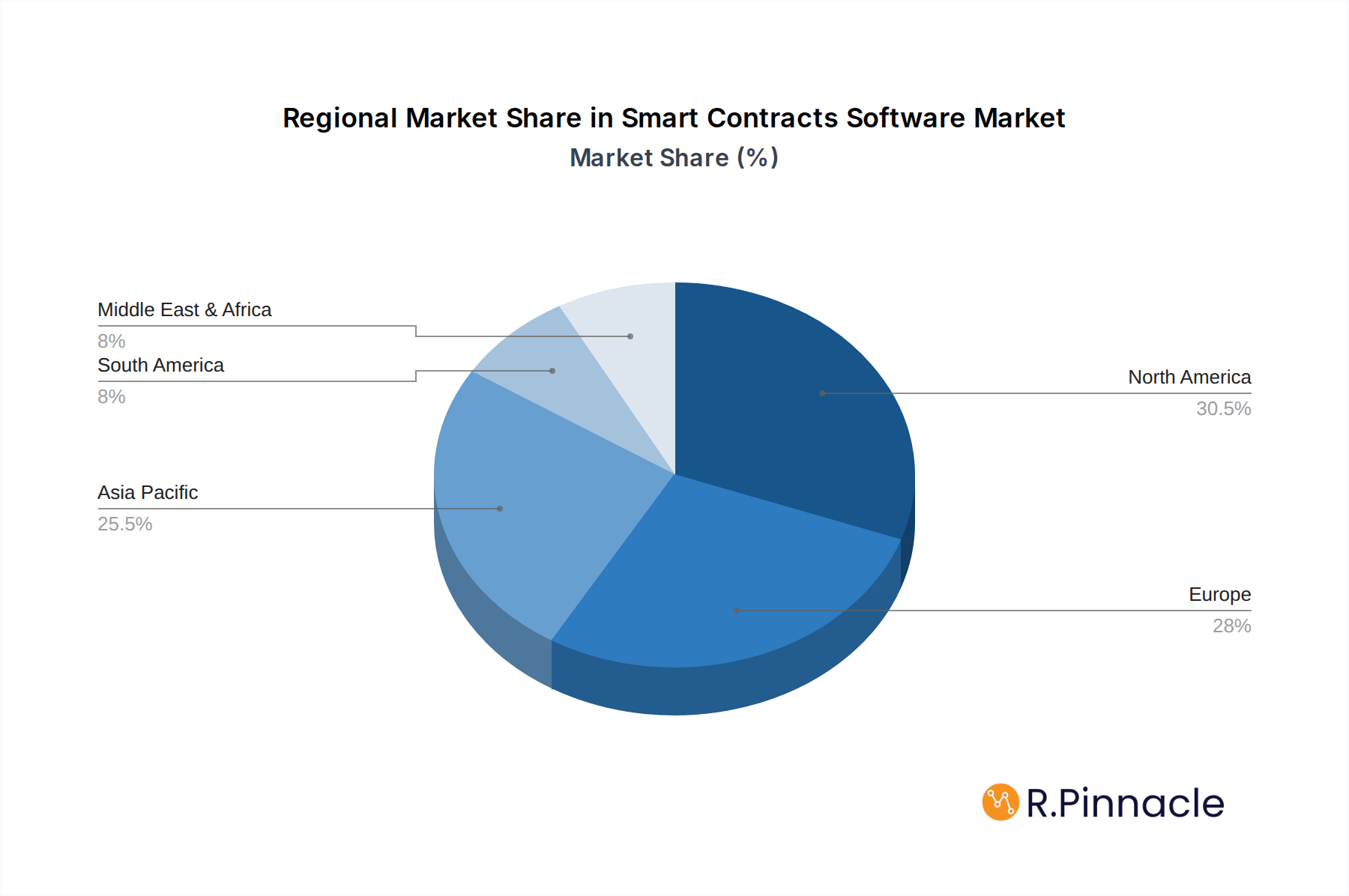

Dominant Regions & Segments in Smart Contracts Software

North America currently holds a dominant position in the smart contracts software market, driven by a strong ecosystem of technology innovation, significant venture capital investment, and the early adoption of blockchain solutions by large enterprises. The United States, in particular, spearheads this dominance due to its advanced technological infrastructure and supportive regulatory environment for emerging technologies.

Application Segment Dominance: Large Enterprises

- Key Drivers: Large enterprises are leveraging smart contracts for complex financial transactions, supply chain management, and insurance claims processing, demanding robust security, scalability, and integration capabilities. Economic policies encouraging digital transformation and the need for reduced operational costs are paramount.

- Detailed Dominance Analysis: The emphasis on automation, risk mitigation, and enhanced transparency in large-scale operations makes smart contracts software indispensable. Companies are investing heavily in custom smart contract development and integration with existing enterprise resource planning (ERP) systems. The market size for smart contracts in large enterprises is projected to reach several hundred million by 2025, with continued strong growth expected.

Type Segment Dominance: Cloud Based

- Key Drivers: The agility, scalability, and cost-effectiveness of cloud-based solutions make them highly attractive to businesses of all sizes. Reduced upfront infrastructure investment and ease of deployment are key economic policies driving adoption.

- Detailed Dominance Analysis: Cloud-based smart contracts platforms offer a flexible and accessible entry point for businesses looking to explore the benefits of smart contracts without significant IT overhead. Providers are focusing on offering Software-as-a-Service (SaaS) models that cater to diverse needs, from basic contract automation to complex decentralized finance (DeFi) applications. The market share of cloud-based solutions is expected to continue to outpace on-premises deployments due to these inherent advantages.

Smart Contracts Software Product Innovations

Recent product innovations in smart contracts software are focused on enhancing security, usability, and interoperability. Developments include advancements in formal verification techniques to minimize vulnerabilities, the creation of low-code/no-code platforms for broader accessibility, and the integration of AI for intelligent contract execution. Companies like Ethereum, Corda, and Hyperledger are continuously refining their platforms with features like improved gas efficiency, enhanced privacy controls, and cross-chain compatibility. These innovations are directly addressing market demand for more secure, efficient, and user-friendly smart contract solutions, enabling wider adoption across various industries.

Report Scope & Segmentation Analysis

This report segments the smart contracts software market by application and deployment type.

- Application: The market is analyzed across Large Enterprises and SMEs. Large enterprises represent a significant portion of the market, driven by their need for sophisticated automation and risk management solutions, with market sizes estimated in the hundreds of millions. SMEs, while currently a smaller segment, are projected for rapid growth as accessibility and cost-effectiveness increase.

- Type: Segmentation includes Cloud Based and On Premises deployment models. Cloud-based solutions are expected to dominate, with projected market sizes in the hundreds of millions, owing to their scalability and flexibility. On-premises solutions, while offering greater control, are anticipated to represent a smaller, albeit significant, market share.

Key Drivers of Smart Contracts Software Growth

Several factors are propelling the growth of the smart contracts software market. Technological advancements in blockchain, including scalability solutions and enhanced security protocols, are fundamental. Economic factors such as the increasing demand for automation and transparency in business processes, coupled with the drive for cost reduction, are significant accelerators. Furthermore, regulatory clarity and supportive government initiatives in various regions are fostering trust and encouraging wider adoption. The growing adoption of decentralized finance (DeFi) and the increasing need for efficient supply chain management are also key drivers.

Challenges in the Smart Contracts Software Sector

Despite its promising growth, the smart contracts software sector faces several challenges. Regulatory hurdles remain a significant concern, with evolving legal frameworks creating uncertainty around enforceability and liability. Security vulnerabilities in smart contract code can lead to substantial financial losses, necessitating rigorous auditing and testing. Interoperability issues between different blockchain networks also pose a barrier to widespread adoption. Furthermore, the technical complexity and the shortage of skilled developers can hinder implementation for some organizations.

Emerging Opportunities in Smart Contracts Software

The smart contracts software market is ripe with emerging opportunities. The burgeoning field of Decentralized Finance (DeFi) presents immense potential for innovative financial products and services. Supply chain digitization offers a vast market for optimizing logistics, tracking goods, and automating payments. The development of interoperable blockchain solutions will unlock new possibilities for seamless cross-chain transactions. Additionally, the increasing focus on Environmental, Social, and Governance (ESG) initiatives presents opportunities for smart contracts to ensure transparency and accountability in sustainable practices. The market is also seeing opportunities in digital identity management and tokenization of real-world assets.

Leading Players in the Smart Contracts Software Market

- Ethereum

- Corda

- Hyperledger

- Microsoft

- DigiByte Holdings

- æternity blockchain

- AlphaPoint

- AnChain.AI

- BigchainDB

- Bison Trails Co.

- BlockApps

- Block Notary

- Blockstream

- ChromaWay

- Chronicled

- CloudFabrix Software

- Credits

- Digital Asset

- IBM

- Icertis

- Kadena

- Monax

- Neo Team

- Polymath

- Riverr Pte. Ltd.

- Sanjh

- Brickblock Digital Services

- Symbiont

- BlockCAT Technologies

- OpenLaw

Key Developments in Smart Contracts Software Industry

- 2023: Significant advancements in layer-2 scaling solutions for Ethereum, aiming to improve transaction speed and reduce costs, impacting smart contract execution.

- 2023: Increased focus on interoperability protocols enabling cross-chain smart contract communication, fostering a more connected blockchain ecosystem.

- 2024: Launch of new enterprise-grade blockchain platforms and frameworks designed specifically for smart contract deployment by major tech players.

- 2024: Growing adoption of formal verification tools and security audits for smart contracts, driven by high-profile exploits.

- 2024: Expansion of smart contract applications in insurance, healthcare, and real estate sectors, demonstrating broader industry acceptance.

- 2025: Expected increase in M&A activities as larger technology companies acquire specialized blockchain and smart contract startups to bolster their offerings.

- 2025: Maturation of regulatory frameworks in key markets, providing clearer guidelines for smart contract development and deployment.

- 2026: Continued innovation in privacy-preserving smart contracts, enabling more sensitive data processing on blockchains.

- 2027: Widespread integration of AI with smart contracts for more intelligent and adaptive agreement execution.

- 2028-2033: Forecasted exponential growth in smart contract adoption across all major industries, driven by increasing efficiency, transparency, and automation benefits.

Future Outlook for Smart Contracts Software Market

The future outlook for the smart contracts software market is exceptionally bright, characterized by continuous innovation and expanding application landscapes. Growth accelerators include the increasing demand for automated business processes, the maturation of blockchain technology, and the development of user-friendly platforms. The tokenization of real-world assets, the expansion of decentralized finance, and the integration of AI with smart contracts will unlock new revenue streams and market opportunities. Strategic partnerships and continued investment in research and development will be crucial for players seeking to capitalize on the transformative potential of smart contracts, leading to significant market expansion over the forecast period.

Smart Contracts Software Segmentation

-

1. Application

- 1.1. Large Enterprises

- 1.2. SMEs

-

2. Type

- 2.1. Cloud Based

- 2.2. On Premises

Smart Contracts Software Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Smart Contracts Software Regional Market Share

Geographic Coverage of Smart Contracts Software

Smart Contracts Software REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 24.2% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Smart Contracts Software Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Large Enterprises

- 5.1.2. SMEs

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Cloud Based

- 5.2.2. On Premises

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Smart Contracts Software Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Large Enterprises

- 6.1.2. SMEs

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Cloud Based

- 6.2.2. On Premises

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Smart Contracts Software Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Large Enterprises

- 7.1.2. SMEs

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Cloud Based

- 7.2.2. On Premises

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Smart Contracts Software Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Large Enterprises

- 8.1.2. SMEs

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Cloud Based

- 8.2.2. On Premises

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Smart Contracts Software Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Large Enterprises

- 9.1.2. SMEs

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Cloud Based

- 9.2.2. On Premises

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Smart Contracts Software Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Large Enterprises

- 10.1.2. SMEs

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Cloud Based

- 10.2.2. On Premises

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Ethereum

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Corda

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Hyperledger

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Microsoft

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 DigiByte Holdings

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 æternity blockchain

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 AlphaPoint

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 AnChain.AI

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 BigchainDB

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Bison Trails Co.

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 BlockApps

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Block Notary

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Blockstream

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 ChromaWay

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Chronicled

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 CloudFabrix Software

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Credits

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 Digital Asset

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.19 IBM

- 11.2.19.1. Overview

- 11.2.19.2. Products

- 11.2.19.3. SWOT Analysis

- 11.2.19.4. Recent Developments

- 11.2.19.5. Financials (Based on Availability)

- 11.2.20 Icertis

- 11.2.20.1. Overview

- 11.2.20.2. Products

- 11.2.20.3. SWOT Analysis

- 11.2.20.4. Recent Developments

- 11.2.20.5. Financials (Based on Availability)

- 11.2.21 Kadena

- 11.2.21.1. Overview

- 11.2.21.2. Products

- 11.2.21.3. SWOT Analysis

- 11.2.21.4. Recent Developments

- 11.2.21.5. Financials (Based on Availability)

- 11.2.22 Monax

- 11.2.22.1. Overview

- 11.2.22.2. Products

- 11.2.22.3. SWOT Analysis

- 11.2.22.4. Recent Developments

- 11.2.22.5. Financials (Based on Availability)

- 11.2.23 Neo Team

- 11.2.23.1. Overview

- 11.2.23.2. Products

- 11.2.23.3. SWOT Analysis

- 11.2.23.4. Recent Developments

- 11.2.23.5. Financials (Based on Availability)

- 11.2.24 Polymath

- 11.2.24.1. Overview

- 11.2.24.2. Products

- 11.2.24.3. SWOT Analysis

- 11.2.24.4. Recent Developments

- 11.2.24.5. Financials (Based on Availability)

- 11.2.25 Riverr Pte. Ltd.

- 11.2.25.1. Overview

- 11.2.25.2. Products

- 11.2.25.3. SWOT Analysis

- 11.2.25.4. Recent Developments

- 11.2.25.5. Financials (Based on Availability)

- 11.2.26 Sanjh

- 11.2.26.1. Overview

- 11.2.26.2. Products

- 11.2.26.3. SWOT Analysis

- 11.2.26.4. Recent Developments

- 11.2.26.5. Financials (Based on Availability)

- 11.2.27 Brickblock Digital Services

- 11.2.27.1. Overview

- 11.2.27.2. Products

- 11.2.27.3. SWOT Analysis

- 11.2.27.4. Recent Developments

- 11.2.27.5. Financials (Based on Availability)

- 11.2.28 Symbiont

- 11.2.28.1. Overview

- 11.2.28.2. Products

- 11.2.28.3. SWOT Analysis

- 11.2.28.4. Recent Developments

- 11.2.28.5. Financials (Based on Availability)

- 11.2.29 BlockCAT Technologies

- 11.2.29.1. Overview

- 11.2.29.2. Products

- 11.2.29.3. SWOT Analysis

- 11.2.29.4. Recent Developments

- 11.2.29.5. Financials (Based on Availability)

- 11.2.30 OpenLaw

- 11.2.30.1. Overview

- 11.2.30.2. Products

- 11.2.30.3. SWOT Analysis

- 11.2.30.4. Recent Developments

- 11.2.30.5. Financials (Based on Availability)

- 11.2.1 Ethereum

List of Figures

- Figure 1: Global Smart Contracts Software Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Smart Contracts Software Revenue (million), by Application 2025 & 2033

- Figure 3: North America Smart Contracts Software Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Smart Contracts Software Revenue (million), by Type 2025 & 2033

- Figure 5: North America Smart Contracts Software Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Smart Contracts Software Revenue (million), by Country 2025 & 2033

- Figure 7: North America Smart Contracts Software Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Smart Contracts Software Revenue (million), by Application 2025 & 2033

- Figure 9: South America Smart Contracts Software Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Smart Contracts Software Revenue (million), by Type 2025 & 2033

- Figure 11: South America Smart Contracts Software Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Smart Contracts Software Revenue (million), by Country 2025 & 2033

- Figure 13: South America Smart Contracts Software Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Smart Contracts Software Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Smart Contracts Software Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Smart Contracts Software Revenue (million), by Type 2025 & 2033

- Figure 17: Europe Smart Contracts Software Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Smart Contracts Software Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Smart Contracts Software Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Smart Contracts Software Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Smart Contracts Software Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Smart Contracts Software Revenue (million), by Type 2025 & 2033

- Figure 23: Middle East & Africa Smart Contracts Software Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Smart Contracts Software Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Smart Contracts Software Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Smart Contracts Software Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Smart Contracts Software Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Smart Contracts Software Revenue (million), by Type 2025 & 2033

- Figure 29: Asia Pacific Smart Contracts Software Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Smart Contracts Software Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Smart Contracts Software Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Smart Contracts Software Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Smart Contracts Software Revenue million Forecast, by Type 2020 & 2033

- Table 3: Global Smart Contracts Software Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Smart Contracts Software Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Smart Contracts Software Revenue million Forecast, by Type 2020 & 2033

- Table 6: Global Smart Contracts Software Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Smart Contracts Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Smart Contracts Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Smart Contracts Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Smart Contracts Software Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Smart Contracts Software Revenue million Forecast, by Type 2020 & 2033

- Table 12: Global Smart Contracts Software Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Smart Contracts Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Smart Contracts Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Smart Contracts Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Smart Contracts Software Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Smart Contracts Software Revenue million Forecast, by Type 2020 & 2033

- Table 18: Global Smart Contracts Software Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Smart Contracts Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Smart Contracts Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Smart Contracts Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Smart Contracts Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Smart Contracts Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Smart Contracts Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Smart Contracts Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Smart Contracts Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Smart Contracts Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Smart Contracts Software Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Smart Contracts Software Revenue million Forecast, by Type 2020 & 2033

- Table 30: Global Smart Contracts Software Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Smart Contracts Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Smart Contracts Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Smart Contracts Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Smart Contracts Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Smart Contracts Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Smart Contracts Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Smart Contracts Software Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Smart Contracts Software Revenue million Forecast, by Type 2020 & 2033

- Table 39: Global Smart Contracts Software Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Smart Contracts Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Smart Contracts Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Smart Contracts Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Smart Contracts Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Smart Contracts Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Smart Contracts Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Smart Contracts Software Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Smart Contracts Software?

The projected CAGR is approximately 24.2%.

2. Which companies are prominent players in the Smart Contracts Software?

Key companies in the market include Ethereum, Corda, Hyperledger, Microsoft, DigiByte Holdings, æternity blockchain, AlphaPoint, AnChain.AI, BigchainDB, Bison Trails Co., BlockApps, Block Notary, Blockstream, ChromaWay, Chronicled, CloudFabrix Software, Credits, Digital Asset, IBM, Icertis, Kadena, Monax, Neo Team, Polymath, Riverr Pte. Ltd., Sanjh, Brickblock Digital Services, Symbiont, BlockCAT Technologies, OpenLaw.

3. What are the main segments of the Smart Contracts Software?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 3725 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Smart Contracts Software," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Smart Contracts Software report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Smart Contracts Software?

To stay informed about further developments, trends, and reports in the Smart Contracts Software, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence