Key Insights

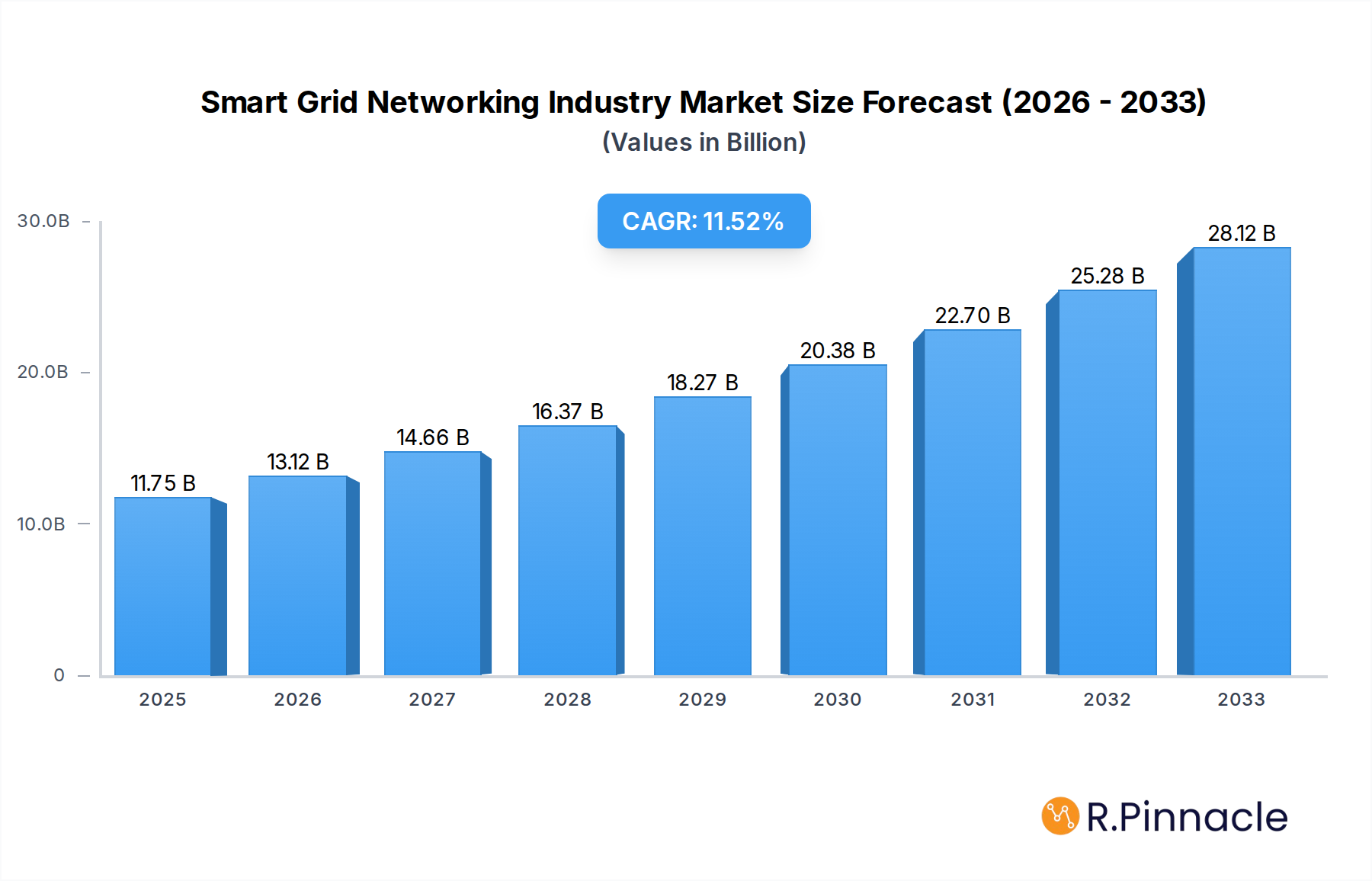

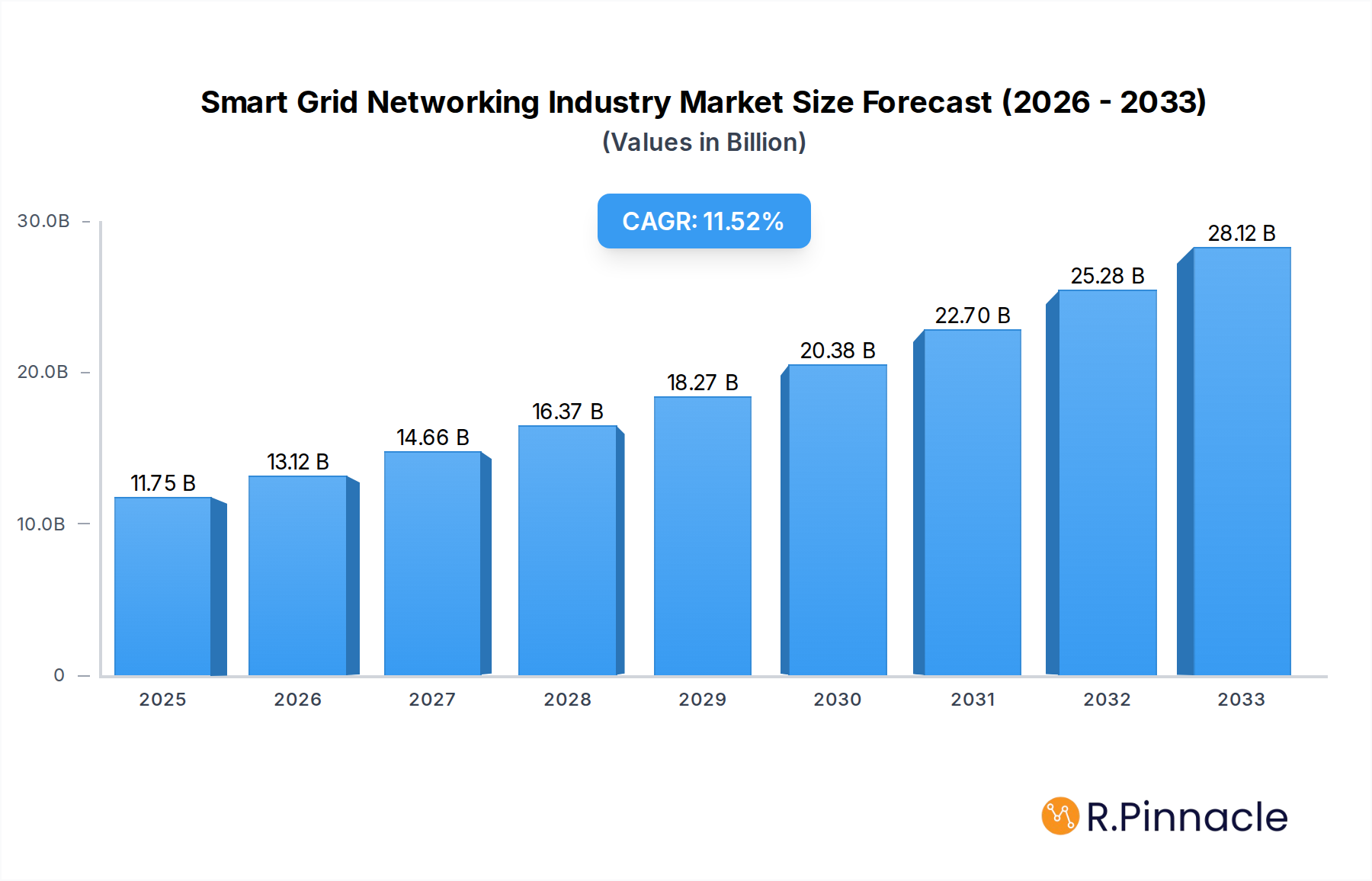

The Smart Grid Networking industry is poised for robust expansion, projected to reach an estimated market size of $11.75 billion in 2025. This impressive growth is underpinned by a compelling compound annual growth rate (CAGR) of 11.73% anticipated over the forecast period of 2025-2033. This upward trajectory is primarily driven by the escalating need for enhanced grid efficiency, improved reliability, and the seamless integration of renewable energy sources. The growing adoption of smart technologies within the energy sector, coupled with supportive government initiatives and increasing investments in grid modernization, are key catalysts for this expansion. Furthermore, the demand for sophisticated solutions in areas like Demand Response and Advanced Metering Infrastructure (AMI) is significantly contributing to the market's dynamism. The evolving energy landscape, characterized by decentralized generation and the imperative for a more resilient and responsive power infrastructure, presents a fertile ground for the proliferation of smart grid networking solutions.

Smart Grid Networking Industry Market Size (In Billion)

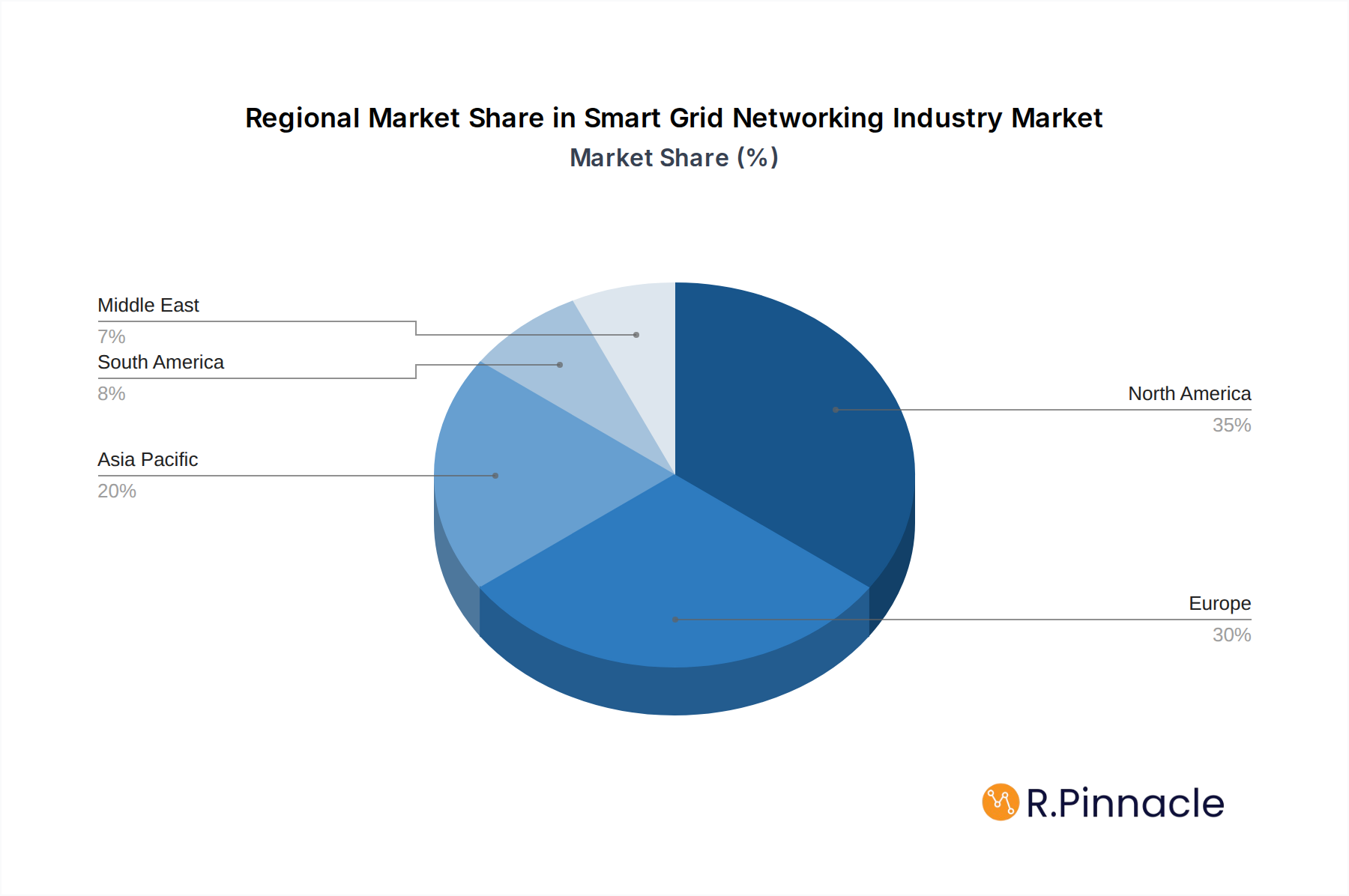

The market's segmentation reveals a strong focus on Technology Application Areas such as Transmission, Demand Response, and Advanced Metering Infrastructure (AMI), indicating areas of concentrated innovation and adoption. Key industry players like Itron Inc., ABB Ltd., Siemens AG, and Cisco Systems Inc. are at the forefront, driving technological advancements and expanding their market presence. Geographically, North America and Europe are expected to lead in market share, owing to established smart grid initiatives and substantial investments. However, the Asia Pacific region is anticipated to exhibit the fastest growth, fueled by rapid urbanization, increasing energy demand, and a growing emphasis on smart city development. While the market benefits from strong drivers, potential restraints such as high initial investment costs and cybersecurity concerns need to be strategically addressed by stakeholders to ensure sustained and widespread adoption of smart grid networking technologies.

Smart Grid Networking Industry Company Market Share

This in-depth report offers a definitive analysis of the global Smart Grid Networking industry, providing critical insights for stakeholders seeking to understand market dynamics, technological advancements, and future growth trajectories. Covering the historical period from 2019 to 2024, the base year of 2025, and a robust forecast period extending to 2033, this report delivers actionable intelligence on market size, segmentation, competitive landscapes, and emerging opportunities. We leverage high-ranking keywords to ensure maximum search visibility for industry professionals and decision-makers.

Smart Grid Networking Industry Market Structure & Innovation Trends

The Smart Grid Networking industry is characterized by a moderately concentrated market structure, with key players continuously driving innovation to meet evolving energy demands. Major companies like Itron Inc., ABB Ltd., Hitachi Ltd., Cisco Systems Inc., Siemens AG, Schneider Electric SE, Eaton Corporation PLC, General Electric Company, Honeywell International Inc, and Osaki Electric Co Ltd. hold significant market share. Innovation is primarily driven by the increasing need for grid modernization, renewable energy integration, and enhanced grid resilience. Regulatory frameworks play a crucial role in shaping market adoption, with government initiatives promoting smart grid deployment worldwide. While direct product substitutes are limited, the emergence of decentralized energy solutions presents a competitive dynamic. End-user demographics are shifting towards utilities and grid operators prioritizing efficiency, reliability, and sustainability. Mergers and acquisitions (M&A) are prevalent, with significant deal values indicating consolidation and strategic expansion. For instance, the acquisition of DC Systems BV by Schneider Electric in January 2021 underscores the industry's drive for technological integration and market consolidation.

Smart Grid Networking Industry Market Dynamics & Trends

The Smart Grid Networking industry is poised for substantial growth, propelled by a confluence of compelling market drivers and transformative technological disruptions. The escalating global demand for reliable and sustainable energy, coupled with the imperative to reduce carbon emissions, serves as a primary growth catalyst. Utilities worldwide are investing billions in modernizing their aging infrastructure to enhance grid efficiency, improve outage management, and integrate a growing volume of intermittent renewable energy sources like solar and wind power. This modernization necessitates advanced networking solutions capable of handling bidirectional power flow, real-time data transmission, and sophisticated control mechanisms.

Technological advancements are fundamentally reshaping the industry. The proliferation of the Internet of Things (IoT) has enabled the deployment of intelligent sensors and devices across the grid, facilitating unprecedented levels of data collection and analysis. Artificial intelligence (AI) and machine learning (ML) are increasingly being employed for predictive maintenance, load forecasting, and optimized energy distribution, leading to billions in operational cost savings. Cybersecurity remains a paramount concern, driving significant investment in secure networking solutions to protect critical energy infrastructure from cyber threats.

Consumer preferences are also influencing market dynamics. End-users, both residential and commercial, are demanding greater control over their energy consumption, driving the adoption of smart metering and demand response programs. This shift empowers consumers to participate actively in grid management, leading to more efficient energy utilization and reduced peak demand. The increasing prevalence of electric vehicles (EVs) presents another significant trend, creating new challenges and opportunities for grid operators to manage charging loads and integrate EV charging infrastructure seamlessly into the smart grid.

Competitive dynamics within the industry are intense, with established players continually innovating and new entrants emerging with specialized solutions. Companies are investing heavily in research and development to offer end-to-end smart grid solutions, encompassing hardware, software, and services. Strategic partnerships and acquisitions are common, aimed at expanding market reach, acquiring new technologies, and strengthening competitive positioning. The market penetration of smart grid technologies is steadily increasing, with billions projected in investments across various regions. The compound annual growth rate (CAGR) for the smart grid networking market is estimated to be robust, reflecting the sustained demand for modern, resilient, and efficient energy infrastructures.

Dominant Regions & Segments in Smart Grid Networking Industry

North America, particularly the United States, currently stands as the dominant region in the Smart Grid Networking industry. This leadership is underpinned by a combination of aggressive government initiatives, significant investments in grid modernization, and a strong regulatory push for energy efficiency and renewable energy integration. The region's advanced technological infrastructure and the presence of major utility companies with substantial budgets for smart grid deployment further solidify its leading position.

Within the Technology Application Area, Advanced Metering Infrastructure (AMI) is emerging as a key segment driving dominance. The widespread deployment of smart meters across residential, commercial, and industrial sectors is crucial for enabling bidirectional communication, real-time data exchange, and remote meter reading. This segment is fueled by the need for enhanced billing accuracy, improved outage detection, and the provision of detailed energy consumption data to consumers. The financial investment in AMI deployment alone amounts to billions annually, reflecting its strategic importance.

Key Drivers for Dominance:

- Economic Policies & Infrastructure: Government incentives, such as tax credits and grants for grid modernization projects, play a pivotal role. The existing robust telecommunications and IT infrastructure in North America provides a solid foundation for smart grid deployment.

- Regulatory Frameworks: Forward-thinking regulations mandating smart meter adoption and encouraging demand response programs create a conducive environment for market growth. Utility commissions actively support investments that promise improved grid reliability and efficiency.

- Technological Adoption: A high rate of adoption for advanced technologies, including IoT, AI, and cloud computing, allows for seamless integration of smart grid solutions. The presence of leading technology providers headquartered in the region also fosters innovation.

While AMI leads, the Transmission segment is also experiencing significant growth. The integration of renewable energy sources, often located in remote areas, necessitates advanced grid management and control systems to ensure stability and efficient power flow. Billions are being invested in upgrading transmission infrastructure to handle the complexities of a decentralized energy landscape.

The Demand Response segment is gaining traction as utilities seek to manage peak loads and reduce the need for expensive peaker plants. Consumer engagement through smart devices and incentives for load shifting is becoming increasingly important, representing a growing market segment.

The Other Technology Application Areas encompass a range of emerging solutions, including grid automation, substation modernization, and cybersecurity for critical infrastructure, all contributing billions to the overall market expansion.

Smart Grid Networking Industry Product Innovations

Product innovations in the Smart Grid Networking industry are focused on enhancing grid intelligence, reliability, and efficiency. Leading companies are developing advanced communication protocols, robust sensor technologies, and intelligent software platforms that enable real-time monitoring and control of the power grid. Innovations in areas like distributed ledger technology (DLT) for secure energy trading and AI-powered analytics for predictive maintenance are gaining traction. These advancements provide utilities with greater visibility into grid operations, improve fault detection, and facilitate the seamless integration of renewable energy sources, offering significant competitive advantages and contributing to billions in operational improvements.

Report Scope & Segmentation Analysis

This report meticulously analyzes the Smart Grid Networking industry across key segments.

Transmission: This segment focuses on the networking technologies and solutions vital for the reliable and efficient transfer of electricity across long distances. It includes solutions for grid monitoring, control, and protection, crucial for integrating diverse energy sources and ensuring grid stability. Growth projections indicate substantial market expansion driven by the need for grid resilience.

Demand Response: This segment encompasses technologies and strategies that enable utilities to manage electricity demand by incentivizing consumers to reduce their consumption during peak hours. This includes smart home devices, communication platforms, and control systems that facilitate participation in demand response programs, with projected growth fueled by energy cost optimization.

Advanced Metering Infrastructure (AMI): This segment covers smart meters, communication networks, and data management systems that provide detailed, real-time energy consumption data. AMI enables bidirectional communication between utilities and consumers, facilitating smart billing, outage detection, and energy management. This segment is experiencing robust growth due to its foundational role in smart grid development.

Other Technology Application Areas: This broad category includes innovations in areas such as grid automation, substation modernization, cybersecurity for energy infrastructure, and microgrid networking. These solutions address specific challenges and opportunities within the broader smart grid ecosystem, contributing to billions in market value and diverse growth trajectories.

Key Drivers of Smart Grid Networking Industry Growth

The Smart Grid Networking industry is experiencing robust growth driven by several critical factors. The escalating demand for reliable and sustainable energy sources is a primary catalyst, pushing utilities to modernize their infrastructure. Government initiatives and regulatory mandates worldwide are accelerating the adoption of smart grid technologies to enhance energy efficiency, reduce carbon emissions, and improve grid resilience. Technological advancements, particularly in IoT, AI, and advanced communication networks, are enabling more intelligent and responsive grid operations, creating billions in new market opportunities. Furthermore, the increasing integration of renewable energy sources like solar and wind power necessitates sophisticated networking solutions for grid stability and load balancing. The growing consumer demand for greater control over energy consumption and participation in demand response programs also fuels market expansion.

Challenges in the Smart Grid Networking Industry Sector

Despite its promising growth, the Smart Grid Networking industry faces several significant challenges. High upfront investment costs associated with deploying advanced networking infrastructure and smart grid technologies can be a barrier for some utilities, requiring billions in capital expenditure. Cybersecurity threats pose a substantial risk, demanding robust security protocols and continuous vigilance to protect critical energy infrastructure from sophisticated attacks. Regulatory hurdles and the complexity of interoperability standards across different vendors and regions can slow down widespread adoption. Supply chain disruptions, particularly for specialized components, can impact project timelines and costs. Finally, public perception and the need for consumer education regarding the benefits and security of smart grid technologies remain crucial for widespread acceptance and successful implementation, impacting billions in potential revenue.

Emerging Opportunities in Smart Grid Networking Industry

The Smart Grid Networking industry is ripe with emerging opportunities. The rapid growth of electric vehicle (EV) adoption presents a significant opportunity for grid operators to develop smart charging infrastructure and manage charging loads efficiently, representing billions in future market potential. The increasing adoption of distributed energy resources (DERs) and microgrids creates demand for advanced networking solutions that can manage decentralized energy generation and consumption. The development of blockchain technology for secure energy trading and peer-to-peer energy markets offers a disruptive opportunity. Furthermore, the growing focus on grid modernization in developing economies presents a vast untapped market for smart grid solutions, with billions in investment projected. Enhanced data analytics capabilities, leveraging AI and machine learning, are opening up new avenues for predictive maintenance, demand forecasting, and grid optimization services.

Leading Players in the Smart Grid Networking Industry Market

- Itron Inc.

- ABB Ltd.

- Hitachi Ltd.

- Cisco Systems Inc.

- Siemens AG

- Schneider Electric SE

- Eaton Corporation PLC

- General Electric Company

- Honeywell International Inc

- Osaki Electric Co Ltd.

Key Developments in Smart Grid Networking Industry Industry

- January 2021: Schneider Electric acquired DC Systems BV, a major supplier of smart systems. This acquisition has helped Schneider Electric advance innovations in the electrical distribution and smart grid sectors.

- September 2020: Siemens Energy launched its new Unified Power Flow Controller (UPFC) PLUS and expanded the options for grid stabilization. The UPFC PLUS helps system operators stabilize the grid by dynamically controlling the load flow in alternating-current grids.

Future Outlook for Smart Grid Networking Industry Market

The future outlook for the Smart Grid Networking industry is exceptionally strong, driven by the indispensable need for modernized, resilient, and sustainable energy systems. Billions in continued investment are anticipated as utilities worldwide accelerate their digital transformation initiatives. Key growth accelerators include the pervasive integration of renewable energy, the proliferation of electric vehicles, and the increasing demand for grid flexibility and demand-side management. Strategic opportunities lie in developing solutions that enhance grid cybersecurity, enable peer-to-peer energy trading, and facilitate the widespread adoption of microgrids. The market is poised for significant expansion, offering substantial potential for innovation and profitability as smart grids become the backbone of future energy infrastructure.

Smart Grid Networking Industry Segmentation

-

1. Technology Application Area

- 1.1. Transmission

- 1.2. Demand Response

- 1.3. Advanced Metering Infrastructure (AMI)

- 1.4. Other Technology Application Areas

Smart Grid Networking Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia Pacific

- 4. South America

- 5. Middle East

Smart Grid Networking Industry Regional Market Share

Geographic Coverage of Smart Grid Networking Industry

Smart Grid Networking Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 10% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Technology Application Area

- 5.1.1. Transmission

- 5.1.2. Demand Response

- 5.1.3. Advanced Metering Infrastructure (AMI)

- 5.1.4. Other Technology Application Areas

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. North America

- 5.2.2. Europe

- 5.2.3. Asia Pacific

- 5.2.4. South America

- 5.2.5. Middle East

- 5.1. Market Analysis, Insights and Forecast - by Technology Application Area

- 6. Global Smart Grid Networking Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Technology Application Area

- 6.1.1. Transmission

- 6.1.2. Demand Response

- 6.1.3. Advanced Metering Infrastructure (AMI)

- 6.1.4. Other Technology Application Areas

- 6.1. Market Analysis, Insights and Forecast - by Technology Application Area

- 7. North America Smart Grid Networking Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Technology Application Area

- 7.1.1. Transmission

- 7.1.2. Demand Response

- 7.1.3. Advanced Metering Infrastructure (AMI)

- 7.1.4. Other Technology Application Areas

- 7.1. Market Analysis, Insights and Forecast - by Technology Application Area

- 8. Europe Smart Grid Networking Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Technology Application Area

- 8.1.1. Transmission

- 8.1.2. Demand Response

- 8.1.3. Advanced Metering Infrastructure (AMI)

- 8.1.4. Other Technology Application Areas

- 8.1. Market Analysis, Insights and Forecast - by Technology Application Area

- 9. Asia Pacific Smart Grid Networking Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Technology Application Area

- 9.1.1. Transmission

- 9.1.2. Demand Response

- 9.1.3. Advanced Metering Infrastructure (AMI)

- 9.1.4. Other Technology Application Areas

- 9.1. Market Analysis, Insights and Forecast - by Technology Application Area

- 10. South America Smart Grid Networking Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Technology Application Area

- 10.1.1. Transmission

- 10.1.2. Demand Response

- 10.1.3. Advanced Metering Infrastructure (AMI)

- 10.1.4. Other Technology Application Areas

- 10.1. Market Analysis, Insights and Forecast - by Technology Application Area

- 11. Middle East Smart Grid Networking Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Technology Application Area

- 11.1.1. Transmission

- 11.1.2. Demand Response

- 11.1.3. Advanced Metering Infrastructure (AMI)

- 11.1.4. Other Technology Application Areas

- 11.1. Market Analysis, Insights and Forecast - by Technology Application Area

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Itron Inc

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 ABB Ltd

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Hitachi Ltd

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Cisco Systems Inc

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Siemens AG

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Schneider Electric SE

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Eaton Corporation PLC

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 General Electric Company

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Honeywell International Inc *List Not Exhaustive

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Osaki Electric Co Ltd

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Itron Inc

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Smart Grid Networking Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Smart Grid Networking Industry Revenue (billion), by Technology Application Area 2025 & 2033

- Figure 3: North America Smart Grid Networking Industry Revenue Share (%), by Technology Application Area 2025 & 2033

- Figure 4: North America Smart Grid Networking Industry Revenue (billion), by Country 2025 & 2033

- Figure 5: North America Smart Grid Networking Industry Revenue Share (%), by Country 2025 & 2033

- Figure 6: Europe Smart Grid Networking Industry Revenue (billion), by Technology Application Area 2025 & 2033

- Figure 7: Europe Smart Grid Networking Industry Revenue Share (%), by Technology Application Area 2025 & 2033

- Figure 8: Europe Smart Grid Networking Industry Revenue (billion), by Country 2025 & 2033

- Figure 9: Europe Smart Grid Networking Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Asia Pacific Smart Grid Networking Industry Revenue (billion), by Technology Application Area 2025 & 2033

- Figure 11: Asia Pacific Smart Grid Networking Industry Revenue Share (%), by Technology Application Area 2025 & 2033

- Figure 12: Asia Pacific Smart Grid Networking Industry Revenue (billion), by Country 2025 & 2033

- Figure 13: Asia Pacific Smart Grid Networking Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: South America Smart Grid Networking Industry Revenue (billion), by Technology Application Area 2025 & 2033

- Figure 15: South America Smart Grid Networking Industry Revenue Share (%), by Technology Application Area 2025 & 2033

- Figure 16: South America Smart Grid Networking Industry Revenue (billion), by Country 2025 & 2033

- Figure 17: South America Smart Grid Networking Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Middle East Smart Grid Networking Industry Revenue (billion), by Technology Application Area 2025 & 2033

- Figure 19: Middle East Smart Grid Networking Industry Revenue Share (%), by Technology Application Area 2025 & 2033

- Figure 20: Middle East Smart Grid Networking Industry Revenue (billion), by Country 2025 & 2033

- Figure 21: Middle East Smart Grid Networking Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Smart Grid Networking Industry Revenue billion Forecast, by Technology Application Area 2020 & 2033

- Table 2: Global Smart Grid Networking Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 3: Global Smart Grid Networking Industry Revenue billion Forecast, by Technology Application Area 2020 & 2033

- Table 4: Global Smart Grid Networking Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 5: Global Smart Grid Networking Industry Revenue billion Forecast, by Technology Application Area 2020 & 2033

- Table 6: Global Smart Grid Networking Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: Global Smart Grid Networking Industry Revenue billion Forecast, by Technology Application Area 2020 & 2033

- Table 8: Global Smart Grid Networking Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 9: Global Smart Grid Networking Industry Revenue billion Forecast, by Technology Application Area 2020 & 2033

- Table 10: Global Smart Grid Networking Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 11: Global Smart Grid Networking Industry Revenue billion Forecast, by Technology Application Area 2020 & 2033

- Table 12: Global Smart Grid Networking Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Smart Grid Networking Industry?

The projected CAGR is approximately 10%.

2. Which companies are prominent players in the Smart Grid Networking Industry?

Key companies in the market include Itron Inc, ABB Ltd, Hitachi Ltd, Cisco Systems Inc, Siemens AG, Schneider Electric SE, Eaton Corporation PLC, General Electric Company, Honeywell International Inc *List Not Exhaustive, Osaki Electric Co Ltd.

3. What are the main segments of the Smart Grid Networking Industry?

The market segments include Technology Application Area.

4. Can you provide details about the market size?

The market size is estimated to be USD 16.47 billion as of 2022.

5. What are some drivers contributing to market growth?

4.; Growing Power Demand from the Commercial and Industrial Sectors.

6. What are the notable trends driving market growth?

Advanced Metering Infrastructure (AMI) to Witness Significant Growth.

7. Are there any restraints impacting market growth?

4.; Stringent Environmental and Safety Regulations.

8. Can you provide examples of recent developments in the market?

In January 2021, Schneider Electric acquired DC Systems BV, a major supplier of smart systems. This acquisition has helped Schneider Electric advance innovations in the electrical distribution and smart grid sectors.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Smart Grid Networking Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Smart Grid Networking Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Smart Grid Networking Industry?

To stay informed about further developments, trends, and reports in the Smart Grid Networking Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence