Key Insights

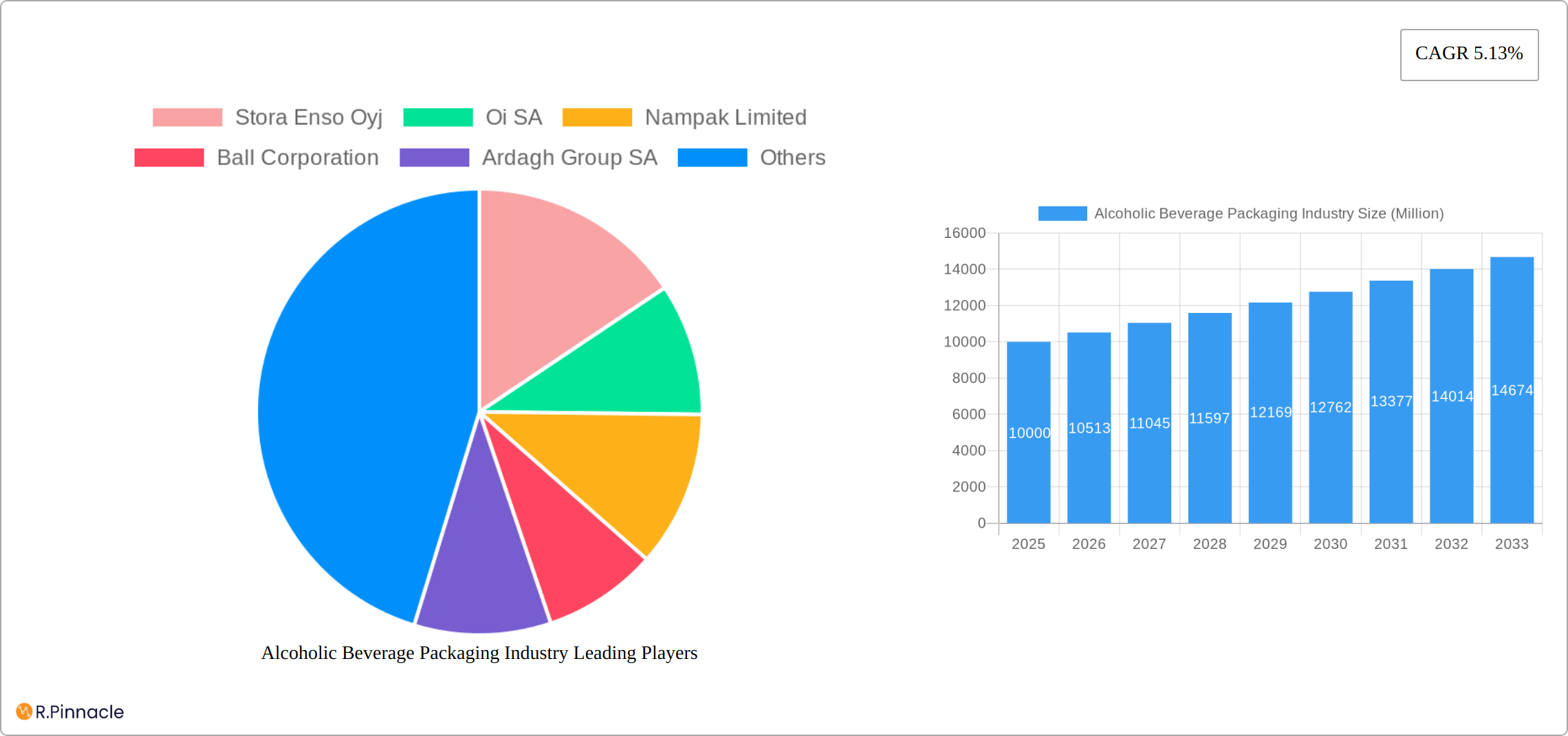

The alcoholic beverage packaging market, currently valued at approximately $XX million in 2025 (assuming a logical estimation based on the provided CAGR and market size), is projected to experience robust growth, exhibiting a Compound Annual Growth Rate (CAGR) of 5.13% from 2025 to 2033. This expansion is fueled by several key drivers. The rising demand for alcoholic beverages globally, particularly in emerging economies, is a primary factor. Furthermore, consumer preference shifts toward premiumization and innovative packaging solutions, such as lightweighting for sustainability and enhanced designs for shelf appeal, are significantly influencing market dynamics. The growing adoption of e-commerce and direct-to-consumer models also necessitates adaptable packaging formats, further stimulating market growth. However, challenges exist, including fluctuating raw material prices, stringent regulations regarding material composition and labeling, and the increasing emphasis on sustainable and eco-friendly packaging alternatives, which necessitate continuous innovation and adaptation within the industry. Segmentation reveals a diverse landscape, with glass, metal, and plastic dominating material choices, and cans and bottles remaining the most prevalent product types. Competitive rivalry is intense, with major players such as Stora Enso, Ball Corporation, Amcor, and Crown Holdings vying for market share through strategic partnerships, acquisitions, and technological advancements.

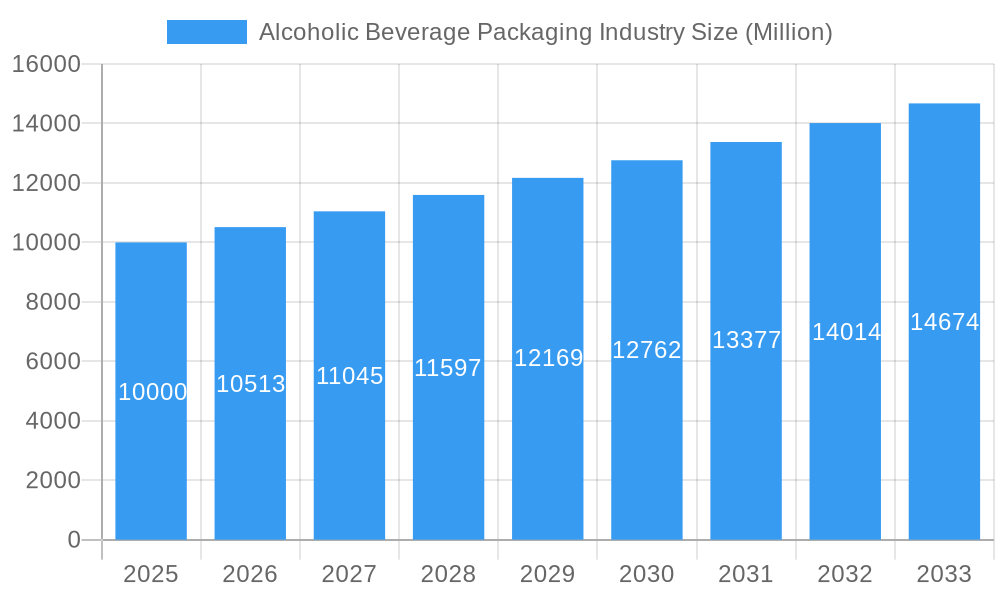

Alcoholic Beverage Packaging Industry Market Size (In Billion)

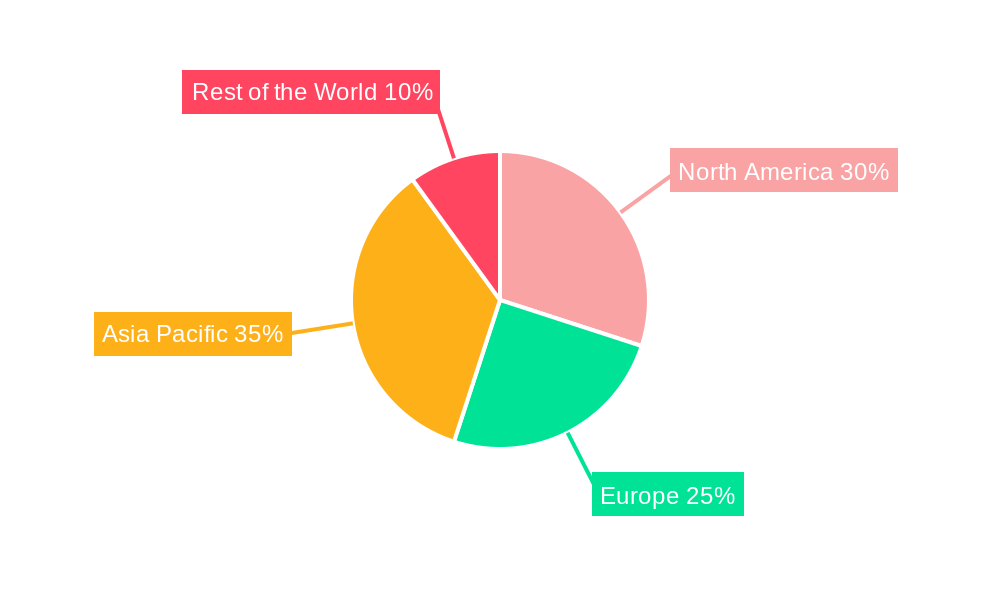

Regional analysis indicates significant variations in market maturity and growth potential. North America and Europe, while mature markets, continue to show steady growth driven by premiumization and innovation. Asia-Pacific, however, presents the most significant growth opportunities, driven by rising disposable incomes and a burgeoning middle class, leading to increased consumption of alcoholic beverages. This diverse regional landscape necessitates tailored strategies for manufacturers to successfully penetrate and capture market share effectively. The ongoing focus on sustainability, coupled with the need for cost-effective and efficient solutions, presents opportunities for manufacturers that can successfully balance these competing demands. The forecast period of 2025-2033 promises continued growth, but success will hinge on innovation, sustainability initiatives, and strategic adaptation to evolving consumer preferences and regulatory landscapes.

Alcoholic Beverage Packaging Industry Company Market Share

Alcoholic Beverage Packaging Industry Report: 2019-2033 Forecast

This comprehensive report provides a detailed analysis of the Alcoholic Beverage Packaging market, offering invaluable insights for industry professionals, investors, and strategic decision-makers. The study period covers 2019-2033, with a focus on the 2025-2033 forecast period. The report leverages extensive data analysis to provide actionable insights into market size, growth drivers, challenges, and future opportunities. The market is segmented by material (Glass, Metal, Plastic, Other Materials) and product type (Cans, Bottles, Other Products). Leading players like Stora Enso Oyj, Oi SA, Nampak Limited, Ball Corporation, and others are profiled. The report is valued at $xx Million in 2025 and is projected to reach $xx Million by 2033, exhibiting a CAGR of xx%.

Alcoholic Beverage Packaging Industry Market Structure & Innovation Trends

The Alcoholic Beverage Packaging market is moderately concentrated, with several key players holding significant market share. Stora Enso Oyj, Amcor PLC, and Ball Corporation are among the leading players, collectively commanding an estimated xx% market share in 2025. Innovation is driven by consumer demand for sustainable packaging, lightweight designs, and enhanced aesthetic appeal. Regulatory frameworks, particularly concerning recyclability and material composition, significantly influence market dynamics. The rise of craft breweries and premium spirits has fueled demand for innovative packaging solutions. Significant M&A activity has been observed, with deal values exceeding $xx Million in the past five years, mostly involving acquisitions aimed at expanding product portfolios and geographical reach.

- Market Concentration: Moderately concentrated, with top 5 players holding xx% market share (2025 estimate).

- Innovation Drivers: Sustainability, lightweighting, aesthetics, and premiumization.

- Regulatory Framework: Focus on recyclability and sustainable materials.

- M&A Activity: Significant activity with deal values exceeding $xx Million in the past five years.

Alcoholic Beverage Packaging Industry Market Dynamics & Trends

The Alcoholic Beverage Packaging market is experiencing robust growth, driven by several factors. The increasing consumption of alcoholic beverages globally, particularly in emerging markets, is a key growth driver. Technological advancements, such as the adoption of lightweighting technologies and improved printing techniques, are enhancing product appeal and reducing costs. Consumer preferences are shifting towards sustainable and eco-friendly packaging options, creating opportunities for innovative materials like recycled plastics and bio-based materials. Competitive dynamics are characterized by innovation, price competition, and strategic partnerships.

- Growth Drivers: Increasing alcoholic beverage consumption, technological advancements, and consumer preference for sustainable packaging.

- Technological Disruptions: Lightweighting, improved printing, and sustainable material adoption.

- Consumer Preferences: Growing demand for sustainable and aesthetically appealing packaging.

- Competitive Dynamics: Innovation, price competition, and strategic partnerships.

Dominant Regions & Segments in Alcoholic Beverage Packaging Industry

North America currently dominates the Alcoholic Beverage Packaging market, driven by high per capita consumption of alcoholic beverages and a robust economy. Within materials, Metal (primarily aluminum cans) holds the largest market share due to its cost-effectiveness, recyclability, and barrier properties. In product type, Cans dominate the market, reflecting the popularity of beer and ready-to-drink cocktails. Europe is another significant market, while Asia-Pacific is showing strong growth potential.

- Leading Region: North America, due to high consumption and a strong economy.

- Dominant Material: Metal (cans), driven by cost-effectiveness and recyclability.

- Dominant Product: Cans, due to the popularity of beer and ready-to-drink beverages.

- Key Drivers (North America): Strong economy, high per capita consumption, and established infrastructure.

- Key Drivers (Europe): Mature market with high consumption and stringent environmental regulations.

- Key Drivers (Asia-Pacific): Rapidly growing middle class and increasing disposable incomes.

Alcoholic Beverage Packaging Industry Product Innovations

The alcoholic beverage packaging industry is experiencing a wave of innovation driven by sustainability concerns, evolving consumer preferences, and technological advancements. A key focus is on eco-friendly materials, with a significant shift towards recycled content, bio-based polymers like PLA and PHA, and innovative lightweighting techniques to minimize environmental impact. This includes exploring alternatives to traditional glass and plastic, such as paper-based solutions and innovative closures designed for recyclability and reduced material usage. Beyond material choices, functional improvements are enhancing product protection through improved barrier properties, tamper evidence, and oxygen scavenging technologies. The consumer experience is also being elevated with designs focused on aesthetics, convenience (e.g., resealable closures), and brand storytelling. The integration of smart packaging technologies, such as RFID tags and NFC chips, is gaining momentum, offering enhanced traceability, brand engagement opportunities (through augmented reality experiences, for example), and combating counterfeiting.

Report Scope & Segmentation Analysis

This report segments the Alcoholic Beverage Packaging market by material (Glass, Metal, Plastic, Other Materials) and product type (Cans, Bottles, Other Products). Each segment is analyzed based on market size, growth projections, and competitive dynamics. The Metal segment is expected to experience strong growth due to its recyclability and cost-effectiveness. The Cans segment will continue to dominate, driven by the high demand for beer and ready-to-drink beverages. Growth projections for each segment are provided for the forecast period (2025-2033).

Key Drivers of Alcoholic Beverage Packaging Industry Growth

The key drivers of market growth include the increasing global consumption of alcoholic beverages, particularly in emerging markets. Technological advancements such as lightweighting and improved printing techniques enhance product aesthetics and reduce costs. Consumer preference for sustainable and eco-friendly packaging is a major factor, as are evolving regulatory frameworks promoting sustainability.

Challenges in the Alcoholic Beverage Packaging Industry Sector

Despite the innovative strides, the alcoholic beverage packaging industry faces considerable challenges. Fluctuations in raw material prices, particularly for aluminum, glass, and paperboard, create significant cost volatility. Stringent environmental regulations, including extended producer responsibility (EPR) schemes and bans on certain materials, necessitate continuous adaptation and investment in sustainable solutions. Intensifying competition requires companies to constantly innovate and differentiate themselves in terms of both cost-effectiveness and sustainability credentials. Supply chain disruptions, exacerbated by geopolitical instability and unforeseen events, pose a significant risk to production and timely delivery. Balancing consumer demand for sustainable packaging with the need for cost-effective solutions remains a critical challenge, requiring careful consideration of the entire lifecycle of packaging materials.

Emerging Opportunities in Alcoholic Beverage Packaging Industry

The growing consumer awareness of environmental issues presents significant opportunities for innovative and sustainable packaging solutions. Lightweighting technologies are gaining traction, enabling reduced transportation costs and carbon emissions. The development and adoption of bio-based and compostable materials offer a pathway towards a circular economy. Emerging markets in Asia, Africa, and Latin America present considerable growth potential, particularly for packaging solutions adapted to local conditions and preferences. The integration of smart packaging technologies opens doors to personalized consumer experiences, enhanced brand loyalty, and improved supply chain traceability and management. Furthermore, there's a growing opportunity for companies that can provide end-to-end sustainable packaging solutions, including design, production, and recycling programs.

Leading Players in the Alcoholic Beverage Packaging Industry Market

Key Developments in Alcoholic Beverage Packaging Industry

- January 2023: Amcor PLC launched a new range of sustainable packaging solutions for alcoholic beverages, emphasizing recycled content and reduced carbon footprint.

- March 2022: Ball Corporation announced a significant investment in a new aluminum can manufacturing facility, highlighting the continued demand for aluminum cans in the beverage industry.

- June 2021: Stora Enso Oyj partnered with a leading brewery to develop innovative paper-based packaging, showcasing the growing interest in sustainable alternatives to traditional materials.

- (Further details to be added based on specific developments)

Future Outlook for Alcoholic Beverage Packaging Industry Market

The Alcoholic Beverage Packaging market is poised for continued growth, driven by favorable macroeconomic factors, rising consumer demand, and ongoing innovation in sustainable materials and packaging technologies. Strategic partnerships, investment in new technologies, and expansion into emerging markets will be key to success in the coming years. The focus on sustainability and consumer preference for eco-friendly packaging will remain a significant driver of growth.

Alcoholic Beverage Packaging Industry Segmentation

-

1. Material

- 1.1. Glass

- 1.2. Metal

- 1.3. Plastic

- 1.4. Other Materials

-

2. Product

- 2.1. Cans

- 2.2. Bottles

- 2.3. Other Products

Alcoholic Beverage Packaging Industry Segmentation By Geography

-

1. North America

- 1.1. Unites States

- 1.2. Canada

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Rest of Asia Pacific

-

4. Rest of the World

- 4.1. Latin America

- 4.2. Middle East

Alcoholic Beverage Packaging Industry Regional Market Share

Geographic Coverage of Alcoholic Beverage Packaging Industry

Alcoholic Beverage Packaging Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.8% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. ; Increasing Consumption of Alcoholic Beverages; Increased Focus on Recycling; Rising Demand for Long Shelf Life of the Product

- 3.3. Market Restrains

- 3.3.1. ; Implementation of Stringent Regulations on Packaging Materials

- 3.4. Market Trends

- 3.4.1. Glass Packaging Segment to Account for a Crucial Share

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Alcoholic Beverage Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Material

- 5.1.1. Glass

- 5.1.2. Metal

- 5.1.3. Plastic

- 5.1.4. Other Materials

- 5.2. Market Analysis, Insights and Forecast - by Product

- 5.2.1. Cans

- 5.2.2. Bottles

- 5.2.3. Other Products

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Rest of the World

- 5.1. Market Analysis, Insights and Forecast - by Material

- 6. North America Alcoholic Beverage Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Material

- 6.1.1. Glass

- 6.1.2. Metal

- 6.1.3. Plastic

- 6.1.4. Other Materials

- 6.2. Market Analysis, Insights and Forecast - by Product

- 6.2.1. Cans

- 6.2.2. Bottles

- 6.2.3. Other Products

- 6.1. Market Analysis, Insights and Forecast - by Material

- 7. Europe Alcoholic Beverage Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Material

- 7.1.1. Glass

- 7.1.2. Metal

- 7.1.3. Plastic

- 7.1.4. Other Materials

- 7.2. Market Analysis, Insights and Forecast - by Product

- 7.2.1. Cans

- 7.2.2. Bottles

- 7.2.3. Other Products

- 7.1. Market Analysis, Insights and Forecast - by Material

- 8. Asia Pacific Alcoholic Beverage Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Material

- 8.1.1. Glass

- 8.1.2. Metal

- 8.1.3. Plastic

- 8.1.4. Other Materials

- 8.2. Market Analysis, Insights and Forecast - by Product

- 8.2.1. Cans

- 8.2.2. Bottles

- 8.2.3. Other Products

- 8.1. Market Analysis, Insights and Forecast - by Material

- 9. Rest of the World Alcoholic Beverage Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Material

- 9.1.1. Glass

- 9.1.2. Metal

- 9.1.3. Plastic

- 9.1.4. Other Materials

- 9.2. Market Analysis, Insights and Forecast - by Product

- 9.2.1. Cans

- 9.2.2. Bottles

- 9.2.3. Other Products

- 9.1. Market Analysis, Insights and Forecast - by Material

- 10. Competitive Analysis

- 10.1. Global Market Share Analysis 2025

- 10.2. Company Profiles

- 10.2.1 Stora Enso Oyj

- 10.2.1.1. Overview

- 10.2.1.2. Products

- 10.2.1.3. SWOT Analysis

- 10.2.1.4. Recent Developments

- 10.2.1.5. Financials (Based on Availability)

- 10.2.2 Oi SA

- 10.2.2.1. Overview

- 10.2.2.2. Products

- 10.2.2.3. SWOT Analysis

- 10.2.2.4. Recent Developments

- 10.2.2.5. Financials (Based on Availability)

- 10.2.3 Nampak Limited

- 10.2.3.1. Overview

- 10.2.3.2. Products

- 10.2.3.3. SWOT Analysis

- 10.2.3.4. Recent Developments

- 10.2.3.5. Financials (Based on Availability)

- 10.2.4 Ball Corporation

- 10.2.4.1. Overview

- 10.2.4.2. Products

- 10.2.4.3. SWOT Analysis

- 10.2.4.4. Recent Developments

- 10.2.4.5. Financials (Based on Availability)

- 10.2.5 Ardagh Group SA

- 10.2.5.1. Overview

- 10.2.5.2. Products

- 10.2.5.3. SWOT Analysis

- 10.2.5.4. Recent Developments

- 10.2.5.5. Financials (Based on Availability)

- 10.2.6 Krones AG

- 10.2.6.1. Overview

- 10.2.6.2. Products

- 10.2.6.3. SWOT Analysis

- 10.2.6.4. Recent Developments

- 10.2.6.5. Financials (Based on Availability)

- 10.2.7 Crown Holdings Inc

- 10.2.7.1. Overview

- 10.2.7.2. Products

- 10.2.7.3. SWOT Analysis

- 10.2.7.4. Recent Developments

- 10.2.7.5. Financials (Based on Availability)

- 10.2.8 Amcor PLC

- 10.2.8.1. Overview

- 10.2.8.2. Products

- 10.2.8.3. SWOT Analysis

- 10.2.8.4. Recent Developments

- 10.2.8.5. Financials (Based on Availability)

- 10.2.9 Mondi PLC

- 10.2.9.1. Overview

- 10.2.9.2. Products

- 10.2.9.3. SWOT Analysis

- 10.2.9.4. Recent Developments

- 10.2.9.5. Financials (Based on Availability)

- 10.2.10 Gerresheimer AG*List Not Exhaustive

- 10.2.10.1. Overview

- 10.2.10.2. Products

- 10.2.10.3. SWOT Analysis

- 10.2.10.4. Recent Developments

- 10.2.10.5. Financials (Based on Availability)

- 10.2.11 Berry Global Inc

- 10.2.11.1. Overview

- 10.2.11.2. Products

- 10.2.11.3. SWOT Analysis

- 10.2.11.4. Recent Developments

- 10.2.11.5. Financials (Based on Availability)

- 10.2.12 Sidel SA

- 10.2.12.1. Overview

- 10.2.12.2. Products

- 10.2.12.3. SWOT Analysis

- 10.2.12.4. Recent Developments

- 10.2.12.5. Financials (Based on Availability)

- 10.2.1 Stora Enso Oyj

List of Figures

- Figure 1: Global Alcoholic Beverage Packaging Industry Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Alcoholic Beverage Packaging Industry Revenue (undefined), by Material 2025 & 2033

- Figure 3: North America Alcoholic Beverage Packaging Industry Revenue Share (%), by Material 2025 & 2033

- Figure 4: North America Alcoholic Beverage Packaging Industry Revenue (undefined), by Product 2025 & 2033

- Figure 5: North America Alcoholic Beverage Packaging Industry Revenue Share (%), by Product 2025 & 2033

- Figure 6: North America Alcoholic Beverage Packaging Industry Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Alcoholic Beverage Packaging Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe Alcoholic Beverage Packaging Industry Revenue (undefined), by Material 2025 & 2033

- Figure 9: Europe Alcoholic Beverage Packaging Industry Revenue Share (%), by Material 2025 & 2033

- Figure 10: Europe Alcoholic Beverage Packaging Industry Revenue (undefined), by Product 2025 & 2033

- Figure 11: Europe Alcoholic Beverage Packaging Industry Revenue Share (%), by Product 2025 & 2033

- Figure 12: Europe Alcoholic Beverage Packaging Industry Revenue (undefined), by Country 2025 & 2033

- Figure 13: Europe Alcoholic Beverage Packaging Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Pacific Alcoholic Beverage Packaging Industry Revenue (undefined), by Material 2025 & 2033

- Figure 15: Asia Pacific Alcoholic Beverage Packaging Industry Revenue Share (%), by Material 2025 & 2033

- Figure 16: Asia Pacific Alcoholic Beverage Packaging Industry Revenue (undefined), by Product 2025 & 2033

- Figure 17: Asia Pacific Alcoholic Beverage Packaging Industry Revenue Share (%), by Product 2025 & 2033

- Figure 18: Asia Pacific Alcoholic Beverage Packaging Industry Revenue (undefined), by Country 2025 & 2033

- Figure 19: Asia Pacific Alcoholic Beverage Packaging Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Rest of the World Alcoholic Beverage Packaging Industry Revenue (undefined), by Material 2025 & 2033

- Figure 21: Rest of the World Alcoholic Beverage Packaging Industry Revenue Share (%), by Material 2025 & 2033

- Figure 22: Rest of the World Alcoholic Beverage Packaging Industry Revenue (undefined), by Product 2025 & 2033

- Figure 23: Rest of the World Alcoholic Beverage Packaging Industry Revenue Share (%), by Product 2025 & 2033

- Figure 24: Rest of the World Alcoholic Beverage Packaging Industry Revenue (undefined), by Country 2025 & 2033

- Figure 25: Rest of the World Alcoholic Beverage Packaging Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Alcoholic Beverage Packaging Industry Revenue undefined Forecast, by Material 2020 & 2033

- Table 2: Global Alcoholic Beverage Packaging Industry Revenue undefined Forecast, by Product 2020 & 2033

- Table 3: Global Alcoholic Beverage Packaging Industry Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Alcoholic Beverage Packaging Industry Revenue undefined Forecast, by Material 2020 & 2033

- Table 5: Global Alcoholic Beverage Packaging Industry Revenue undefined Forecast, by Product 2020 & 2033

- Table 6: Global Alcoholic Beverage Packaging Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: Unites States Alcoholic Beverage Packaging Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Alcoholic Beverage Packaging Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Global Alcoholic Beverage Packaging Industry Revenue undefined Forecast, by Material 2020 & 2033

- Table 10: Global Alcoholic Beverage Packaging Industry Revenue undefined Forecast, by Product 2020 & 2033

- Table 11: Global Alcoholic Beverage Packaging Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 12: Germany Alcoholic Beverage Packaging Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 13: United Kingdom Alcoholic Beverage Packaging Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: France Alcoholic Beverage Packaging Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of Europe Alcoholic Beverage Packaging Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Alcoholic Beverage Packaging Industry Revenue undefined Forecast, by Material 2020 & 2033

- Table 17: Global Alcoholic Beverage Packaging Industry Revenue undefined Forecast, by Product 2020 & 2033

- Table 18: Global Alcoholic Beverage Packaging Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: China Alcoholic Beverage Packaging Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Japan Alcoholic Beverage Packaging Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: India Alcoholic Beverage Packaging Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Rest of Asia Pacific Alcoholic Beverage Packaging Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Global Alcoholic Beverage Packaging Industry Revenue undefined Forecast, by Material 2020 & 2033

- Table 24: Global Alcoholic Beverage Packaging Industry Revenue undefined Forecast, by Product 2020 & 2033

- Table 25: Global Alcoholic Beverage Packaging Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 26: Latin America Alcoholic Beverage Packaging Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Middle East Alcoholic Beverage Packaging Industry Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Alcoholic Beverage Packaging Industry?

The projected CAGR is approximately 5.8%.

2. Which companies are prominent players in the Alcoholic Beverage Packaging Industry?

Key companies in the market include Stora Enso Oyj, Oi SA, Nampak Limited, Ball Corporation, Ardagh Group SA, Krones AG, Crown Holdings Inc, Amcor PLC, Mondi PLC, Gerresheimer AG*List Not Exhaustive, Berry Global Inc, Sidel SA.

3. What are the main segments of the Alcoholic Beverage Packaging Industry?

The market segments include Material, Product.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

; Increasing Consumption of Alcoholic Beverages; Increased Focus on Recycling; Rising Demand for Long Shelf Life of the Product.

6. What are the notable trends driving market growth?

Glass Packaging Segment to Account for a Crucial Share.

7. Are there any restraints impacting market growth?

; Implementation of Stringent Regulations on Packaging Materials.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Alcoholic Beverage Packaging Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Alcoholic Beverage Packaging Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Alcoholic Beverage Packaging Industry?

To stay informed about further developments, trends, and reports in the Alcoholic Beverage Packaging Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence