Key Insights

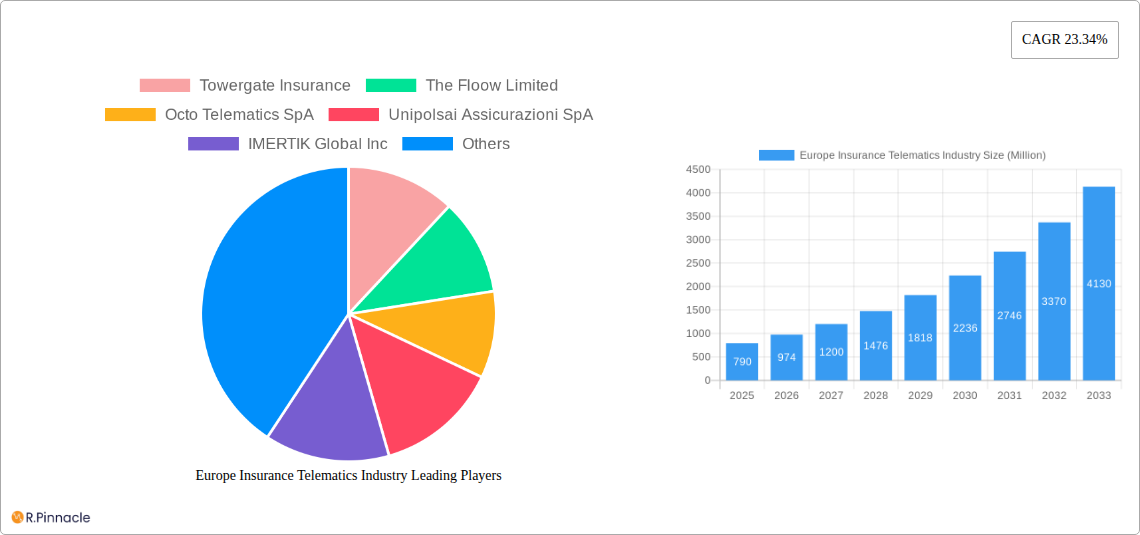

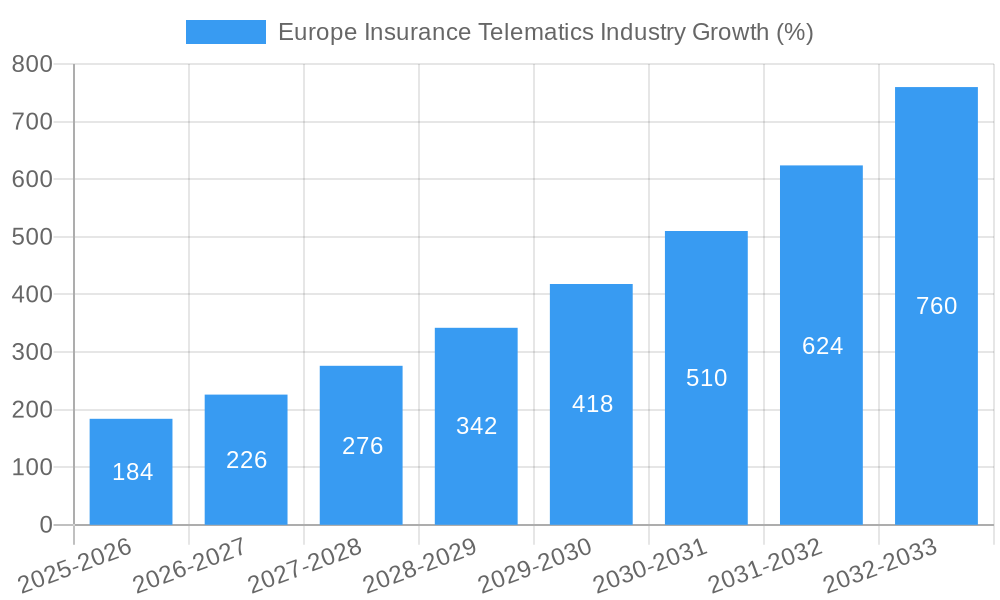

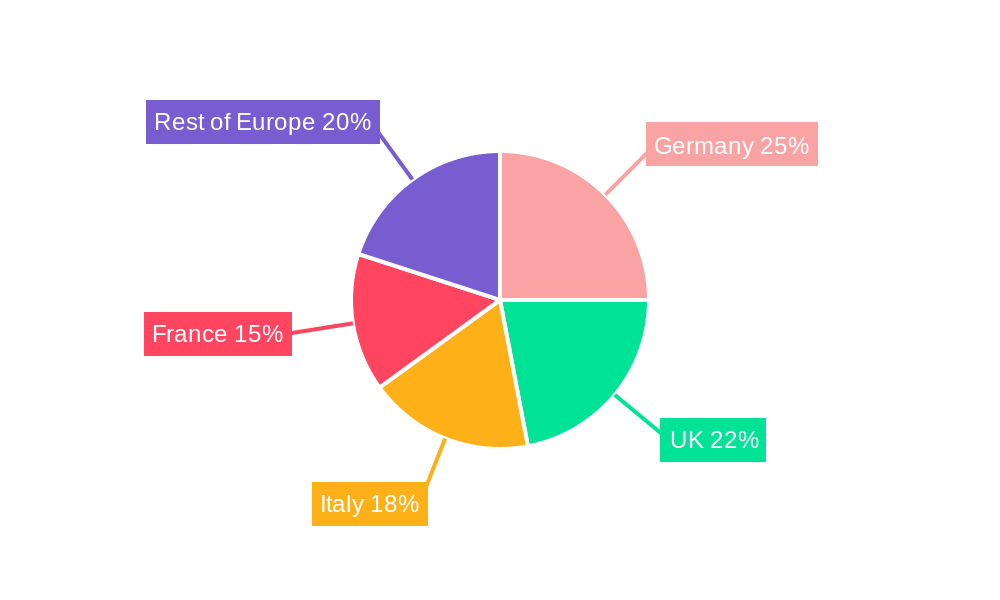

The European insurance telematics market is experiencing robust growth, projected to reach a substantial size driven by increasing adoption of connected car technologies and the demand for usage-based insurance (UBI) products. The market's Compound Annual Growth Rate (CAGR) of 23.34% from 2019 to 2024 indicates a significant upward trajectory, and this momentum is expected to continue through 2033. Key drivers include the rising prevalence of smartphones, the increasing affordability of telematics devices, and a growing awareness among consumers of the potential cost savings associated with UBI. Furthermore, stricter regulations aimed at improving road safety and reducing insurance fraud are also bolstering market expansion. The market is segmented by type (Pay-As-You-Drive, Pay-How-You-Drive, Manage-How-You-Drive) and geography, with Germany, the United Kingdom, and Italy representing significant market segments within Europe. Competition is fierce, with established insurance providers like AXA and UnipolSai alongside specialized telematics companies like Octo Telematics and The Floow vying for market share. The market's success hinges on technological advancements, data security concerns, and the continued development of innovative insurance products that leverage telematics data to offer personalized pricing and risk management.

The Pay-As-You-Drive segment currently holds the largest market share due to its simplicity and appeal to cost-conscious consumers. However, the Pay-How-You-Drive and Manage-How-You-Drive segments are witnessing rapid growth as insurers develop more sophisticated pricing models that consider a wider range of driving behaviors. This reflects a shift towards more holistic risk assessment, moving beyond simply mileage-based pricing. The ongoing integration of advanced driver-assistance systems (ADAS) and the potential for predictive analytics based on telematics data will further fuel innovation and market expansion. The Rest of Europe segment shows considerable potential for future growth as UBI adoption increases in less developed telematics markets. The continued focus on data privacy and security, alongside collaborations between insurers and technology providers, will be crucial for sustaining the market's growth trajectory.

Europe Insurance Telematics Industry: A Comprehensive Market Report (2019-2033)

This comprehensive report provides an in-depth analysis of the Europe Insurance Telematics Industry, offering invaluable insights for industry professionals, investors, and strategic decision-makers. Covering the period from 2019 to 2033, with a base year of 2025 and a forecast period of 2025-2033, this report meticulously examines market dynamics, competitive landscapes, and future growth potential. The total market size in 2025 is estimated at €XX Billion.

Study Period: 2019-2033 Base Year: 2025 Estimated Year: 2025 Forecast Period: 2025-2033 Historical Period: 2019-2024

Europe Insurance Telematics Industry Market Structure & Innovation Trends

This section analyzes the market concentration, innovation drivers, regulatory frameworks, product substitutes, end-user demographics, and M&A activities within the European insurance telematics sector. The market exhibits a moderately concentrated structure, with key players holding significant market share. However, the presence of numerous smaller, specialized firms fosters innovation and competition.

- Market Concentration: The top 5 players account for approximately xx% of the market share in 2025.

- Innovation Drivers: Advancements in IoT, AI, and big data analytics are driving the development of sophisticated telematics solutions. Government regulations promoting road safety and insurance efficiency further propel innovation.

- Regulatory Frameworks: GDPR and other data privacy regulations significantly influence the market, shaping data collection and usage practices. Differing regulations across European countries create complexities for market players.

- Product Substitutes: Traditional insurance models without telematics represent the primary substitute, although their competitiveness is diminishing due to telematics' cost-effectiveness and risk mitigation capabilities.

- End-User Demographics: The market primarily targets younger, tech-savvy drivers and fleet operators seeking cost savings and improved risk management. However, adoption is gradually expanding to other demographics.

- M&A Activities: The sector has witnessed significant M&A activity in recent years, with deal values exceeding €XX Billion between 2019 and 2024. These mergers and acquisitions aim to consolidate market share and enhance technological capabilities. For example, the acquisition of [Company A] by [Company B] in [Year] resulted in a combined market share of xx%.

Europe Insurance Telematics Industry Market Dynamics & Trends

This section delves into the key market drivers, technological disruptions, evolving consumer preferences, and competitive dynamics shaping the European insurance telematics landscape. The market is characterized by robust growth, driven by a combination of factors.

The market is expected to exhibit a Compound Annual Growth Rate (CAGR) of xx% during the forecast period (2025-2033), driven by increasing adoption of pay-as-you-drive (PAYD) and pay-how-you-drive (PAYHD) insurance models, coupled with advancements in data analytics and IoT technologies. Market penetration is expected to reach xx% by 2033, indicating significant growth potential. Consumer preference for personalized and data-driven insurance solutions is a key driver. Increased competition among telematics providers is leading to innovative product offerings and competitive pricing. Technological advancements, particularly in AI-powered risk assessment and predictive modeling, are continuously transforming the industry.

Dominant Regions & Segments in Europe Insurance Telematics Industry

This section identifies the leading regions and segments within the European insurance telematics market.

By Country: The United Kingdom currently holds the largest market share, driven by high insurance penetration and a proactive regulatory environment. Germany and Italy follow closely, with significant growth potential in the rest of Europe. Key drivers include:

- United Kingdom: Strong consumer adoption of telematics-based insurance, well-developed infrastructure, and supportive government policies.

- Germany: Growing awareness of the benefits of telematics, coupled with increasing investments in technological infrastructure.

- Italy: High adoption rates in specific regions, fueled by insurance companies actively promoting telematics-based products.

- Rest of Europe: Market growth is expected to accelerate in this segment as awareness and adoption increases.

By Type: Pay-As-You-Drive (PAYD) holds the largest market share currently due to its cost-effectiveness and appeal to budget-conscious drivers. Pay-How-You-Drive (PAYHD) and Manage-How-You-Drive (MHYD) are experiencing increasing adoption as consumers appreciate the nuanced risk assessment capabilities.

Europe Insurance Telematics Industry Product Innovations

The European insurance telematics market is characterized by continuous product innovation. New offerings leverage advancements in AI, machine learning, and IoT to provide more personalized, accurate, and cost-effective insurance solutions. Products are increasingly incorporating features such as driver behavior scoring, accident detection and notification, and remote vehicle diagnostics. These innovations are enhancing risk management capabilities for insurers, while simultaneously offering consumers greater control and cost savings.

Report Scope & Segmentation Analysis

This report provides a detailed segmentation of the European insurance telematics market across various parameters.

By Type: The report analyzes the Pay-As-You-Drive (PAYD), Pay-How-You-Drive (PAYHD), and Manage-How-You-Drive (MHYD) segments, including their market size, growth projections, and competitive dynamics.

By Country: The report provides in-depth analysis for Italy, the United Kingdom, Germany, and the Rest of Europe, outlining growth trajectories and regional specificities. Each segment's competitive landscape and growth drivers are discussed.

Key Drivers of Europe Insurance Telematics Industry Growth

Several factors are fueling the growth of the European insurance telematics industry. Technological advancements, such as the proliferation of connected cars and the development of sophisticated data analytics capabilities, are key drivers. Favorable regulatory environments in several European countries are encouraging wider adoption of telematics-based insurance products. Additionally, the increasing consumer demand for personalized and cost-effective insurance solutions is contributing to market expansion.

Challenges in the Europe Insurance Telematics Industry Sector

Despite significant growth potential, the European insurance telematics industry faces certain challenges. Data privacy concerns and stringent regulations related to data collection and usage are key obstacles. The high initial investment costs associated with deploying telematics solutions can pose a barrier to entry for smaller companies. Furthermore, fierce competition among established players and new entrants requires constant innovation and adaptation. Cybersecurity threats also represent a significant challenge.

Emerging Opportunities in Europe Insurance Telematics Industry

The European insurance telematics industry presents several emerging opportunities. The expansion of 5G networks is expected to enhance data transmission capabilities, facilitating the development of more advanced telematics solutions. The growing adoption of connected car technologies creates new possibilities for integrating telematics data with other vehicle systems. Furthermore, the increasing demand for personalized and usage-based insurance products offers significant opportunities for growth.

Leading Players in the Europe Insurance Telematics Industry Market

- Towergate Insurance

- The Floow Limited

- Octo Telematics SpA

- Unipolsai Assicurazioni SpA

- IMERTIK Global Inc

- AXA S A

- Drive Quant

- Viasat Group

- LexisNexis Risk Solutions

- Vodafone Automotive SpA

- List Not Exhaustive

Key Developments in Europe Insurance Telematics Industry Industry

- February 2023: OCTO Telematics partners with Ford Motor Company to expand its data streaming partnership into Europe, solidifying its position in fleet telematics and smart mobility solutions. This partnership significantly enhances OCTO's market reach and data capabilities.

Future Outlook for Europe Insurance Telematics Industry Market

The future outlook for the European insurance telematics market remains positive. Continued technological advancements, increasing consumer adoption, and supportive regulatory environments are expected to drive sustained market growth. Strategic partnerships and mergers and acquisitions will likely continue to shape the competitive landscape. The market is poised for significant expansion, driven by innovation and the growing demand for personalized, data-driven insurance solutions.

Europe Insurance Telematics Industry Segmentation

-

1. Type

- 1.1. Pay-As-You-Drive

- 1.2. Pay-How-You-Drive

- 1.3. Manage-How-You-Drive

-

2. BY COUNTRY

- 2.1. Italy

- 2.2. United Kingdom

- 2.3. Germany

- 2.4. Rest of the Europe

Europe Insurance Telematics Industry Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Netherlands

- 1.7. Belgium

- 1.8. Sweden

- 1.9. Norway

- 1.10. Poland

- 1.11. Denmark

Europe Insurance Telematics Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 23.34% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increasing Adoption of Usage-based Insurance by Insurance Companies

- 3.3. Market Restrains

- 3.3.1. Shortage of Skilled Workforce and Low Capital Investment

- 3.4. Market Trends

- 3.4.1. Adoption of Usage-based Insurance by Insurance Companies will Drive The Market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Europe Insurance Telematics Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Pay-As-You-Drive

- 5.1.2. Pay-How-You-Drive

- 5.1.3. Manage-How-You-Drive

- 5.2. Market Analysis, Insights and Forecast - by BY COUNTRY

- 5.2.1. Italy

- 5.2.2. United Kingdom

- 5.2.3. Germany

- 5.2.4. Rest of the Europe

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Germany Europe Insurance Telematics Industry Analysis, Insights and Forecast, 2019-2031

- 7. France Europe Insurance Telematics Industry Analysis, Insights and Forecast, 2019-2031

- 8. Italy Europe Insurance Telematics Industry Analysis, Insights and Forecast, 2019-2031

- 9. United Kingdom Europe Insurance Telematics Industry Analysis, Insights and Forecast, 2019-2031

- 10. Netherlands Europe Insurance Telematics Industry Analysis, Insights and Forecast, 2019-2031

- 11. Sweden Europe Insurance Telematics Industry Analysis, Insights and Forecast, 2019-2031

- 12. Rest of Europe Europe Insurance Telematics Industry Analysis, Insights and Forecast, 2019-2031

- 13. Competitive Analysis

- 13.1. Market Share Analysis 2024

- 13.2. Company Profiles

- 13.2.1 Towergate Insurance

- 13.2.1.1. Overview

- 13.2.1.2. Products

- 13.2.1.3. SWOT Analysis

- 13.2.1.4. Recent Developments

- 13.2.1.5. Financials (Based on Availability)

- 13.2.2 The Floow Limited

- 13.2.2.1. Overview

- 13.2.2.2. Products

- 13.2.2.3. SWOT Analysis

- 13.2.2.4. Recent Developments

- 13.2.2.5. Financials (Based on Availability)

- 13.2.3 Octo Telematics SpA

- 13.2.3.1. Overview

- 13.2.3.2. Products

- 13.2.3.3. SWOT Analysis

- 13.2.3.4. Recent Developments

- 13.2.3.5. Financials (Based on Availability)

- 13.2.4 Unipolsai Assicurazioni SpA

- 13.2.4.1. Overview

- 13.2.4.2. Products

- 13.2.4.3. SWOT Analysis

- 13.2.4.4. Recent Developments

- 13.2.4.5. Financials (Based on Availability)

- 13.2.5 IMERTIK Global Inc

- 13.2.5.1. Overview

- 13.2.5.2. Products

- 13.2.5.3. SWOT Analysis

- 13.2.5.4. Recent Developments

- 13.2.5.5. Financials (Based on Availability)

- 13.2.6 *List Not Exhaustive*List Not Exhaustive

- 13.2.6.1. Overview

- 13.2.6.2. Products

- 13.2.6.3. SWOT Analysis

- 13.2.6.4. Recent Developments

- 13.2.6.5. Financials (Based on Availability)

- 13.2.7 AXA S A

- 13.2.7.1. Overview

- 13.2.7.2. Products

- 13.2.7.3. SWOT Analysis

- 13.2.7.4. Recent Developments

- 13.2.7.5. Financials (Based on Availability)

- 13.2.8 Drive Quant

- 13.2.8.1. Overview

- 13.2.8.2. Products

- 13.2.8.3. SWOT Analysis

- 13.2.8.4. Recent Developments

- 13.2.8.5. Financials (Based on Availability)

- 13.2.9 Viasat Group

- 13.2.9.1. Overview

- 13.2.9.2. Products

- 13.2.9.3. SWOT Analysis

- 13.2.9.4. Recent Developments

- 13.2.9.5. Financials (Based on Availability)

- 13.2.10 LexisNexis Risks Solutions

- 13.2.10.1. Overview

- 13.2.10.2. Products

- 13.2.10.3. SWOT Analysis

- 13.2.10.4. Recent Developments

- 13.2.10.5. Financials (Based on Availability)

- 13.2.11 Vodafone Automotive SpA

- 13.2.11.1. Overview

- 13.2.11.2. Products

- 13.2.11.3. SWOT Analysis

- 13.2.11.4. Recent Developments

- 13.2.11.5. Financials (Based on Availability)

- 13.2.1 Towergate Insurance

List of Figures

- Figure 1: Europe Insurance Telematics Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Europe Insurance Telematics Industry Share (%) by Company 2024

List of Tables

- Table 1: Europe Insurance Telematics Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Europe Insurance Telematics Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 3: Europe Insurance Telematics Industry Revenue Million Forecast, by BY COUNTRY 2019 & 2032

- Table 4: Europe Insurance Telematics Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 5: Europe Insurance Telematics Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 6: Germany Europe Insurance Telematics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 7: France Europe Insurance Telematics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Italy Europe Insurance Telematics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: United Kingdom Europe Insurance Telematics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Netherlands Europe Insurance Telematics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: Sweden Europe Insurance Telematics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: Rest of Europe Europe Insurance Telematics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: Europe Insurance Telematics Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 14: Europe Insurance Telematics Industry Revenue Million Forecast, by BY COUNTRY 2019 & 2032

- Table 15: Europe Insurance Telematics Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 16: United Kingdom Europe Insurance Telematics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 17: Germany Europe Insurance Telematics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 18: France Europe Insurance Telematics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 19: Italy Europe Insurance Telematics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 20: Spain Europe Insurance Telematics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 21: Netherlands Europe Insurance Telematics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 22: Belgium Europe Insurance Telematics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 23: Sweden Europe Insurance Telematics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 24: Norway Europe Insurance Telematics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 25: Poland Europe Insurance Telematics Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 26: Denmark Europe Insurance Telematics Industry Revenue (Million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Insurance Telematics Industry?

The projected CAGR is approximately 23.34%.

2. Which companies are prominent players in the Europe Insurance Telematics Industry?

Key companies in the market include Towergate Insurance, The Floow Limited, Octo Telematics SpA, Unipolsai Assicurazioni SpA, IMERTIK Global Inc, *List Not Exhaustive*List Not Exhaustive, AXA S A, Drive Quant, Viasat Group, LexisNexis Risks Solutions, Vodafone Automotive SpA.

3. What are the main segments of the Europe Insurance Telematics Industry?

The market segments include Type, BY COUNTRY.

4. Can you provide details about the market size?

The market size is estimated to be USD 0.79 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Adoption of Usage-based Insurance by Insurance Companies.

6. What are the notable trends driving market growth?

Adoption of Usage-based Insurance by Insurance Companies will Drive The Market.

7. Are there any restraints impacting market growth?

Shortage of Skilled Workforce and Low Capital Investment.

8. Can you provide examples of recent developments in the market?

February 2023 -OCTO Telematics, a provider of telematics and data analytics for the insurance sector, has partnered with Ford Motor Company to extend its data streaming partnership into Europe. The company has positioned itself as one of the leading companies offering Fleet Telematics and Smart Mobility solutions. The company is on a mission to leverage its advanced analytics and set of IoT Big Data to generate actionable analytics, giving life to a new era of Smart Telematics.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Insurance Telematics Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Insurance Telematics Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Insurance Telematics Industry?

To stay informed about further developments, trends, and reports in the Europe Insurance Telematics Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence