Key Insights

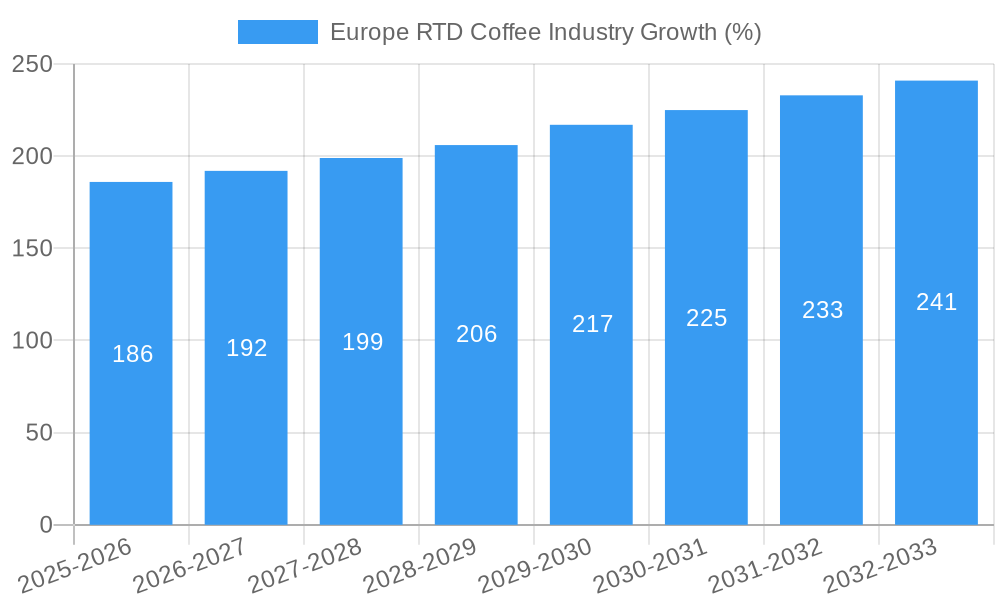

The European Ready-to-Drink (RTD) coffee market is experiencing robust growth, driven by evolving consumer preferences towards convenience and premium coffee experiences. The market, valued at approximately €X billion in 2025 (assuming a reasonable market size based on global RTD coffee market data and European consumption patterns), is projected to expand at a Compound Annual Growth Rate (CAGR) of 3.72% from 2025 to 2033. This growth is fueled by several key factors. The increasing popularity of cold brew and iced coffee variations caters to health-conscious consumers seeking refreshing alternatives to hot coffee. Furthermore, the expanding availability of RTD coffee through diverse distribution channels, including off-trade (supermarkets, convenience stores) and on-trade (cafes, restaurants), enhances accessibility and broadens the market reach. Premiumization, with brands offering high-quality coffee beans and innovative flavors, contributes to higher average selling prices and overall market value. Aseptic packaging, alongside glass bottles and PET bottles, dominates packaging types, reflecting both preservation needs and consumer appeal. Major players like Nestle, PepsiCo, and Coca-Cola, alongside specialized coffee companies like Lavazza and Illycaffè, are actively competing through product innovation and strategic partnerships. Germany, France, the UK, and Italy represent significant market segments within Europe, reflecting established coffee cultures and consumer spending power.

However, market growth is not without challenges. Price sensitivity among consumers, particularly in budget-conscious segments, can constrain market expansion. Competition from established beverage categories and emerging alternative beverages necessitates ongoing innovation and brand differentiation to sustain market share. Fluctuations in raw material costs, particularly coffee bean prices, may impact profitability and necessitate strategic pricing adjustments. Furthermore, environmental concerns surrounding packaging waste are prompting the industry to adopt sustainable practices and explore eco-friendly alternatives, influencing packaging choices and consumer perceptions. Despite these restraints, the long-term outlook for the European RTD coffee market remains positive, driven by the aforementioned growth drivers and the continuous adaptation to evolving consumer demands. The market's segmentation across various packaging types, distribution channels, and coffee types provides opportunities for targeted marketing strategies and niche product development.

Europe RTD Coffee Industry Report: 2019-2033

This comprehensive report provides a detailed analysis of the Europe Ready-to-Drink (RTD) coffee industry, offering invaluable insights for industry professionals, investors, and strategic planners. Covering the period 2019-2033, with a focus on 2025, this report meticulously examines market dynamics, competitive landscapes, and future growth prospects. The report leverages extensive data analysis and expert insights to deliver actionable intelligence for informed decision-making.

Europe RTD Coffee Industry Market Structure & Innovation Trends

This section analyzes the competitive landscape of the European RTD coffee market, examining market concentration, key innovation drivers, regulatory influences, and significant mergers and acquisitions (M&A) activities. The study period covers 2019-2024, with a forecast extending to 2033.

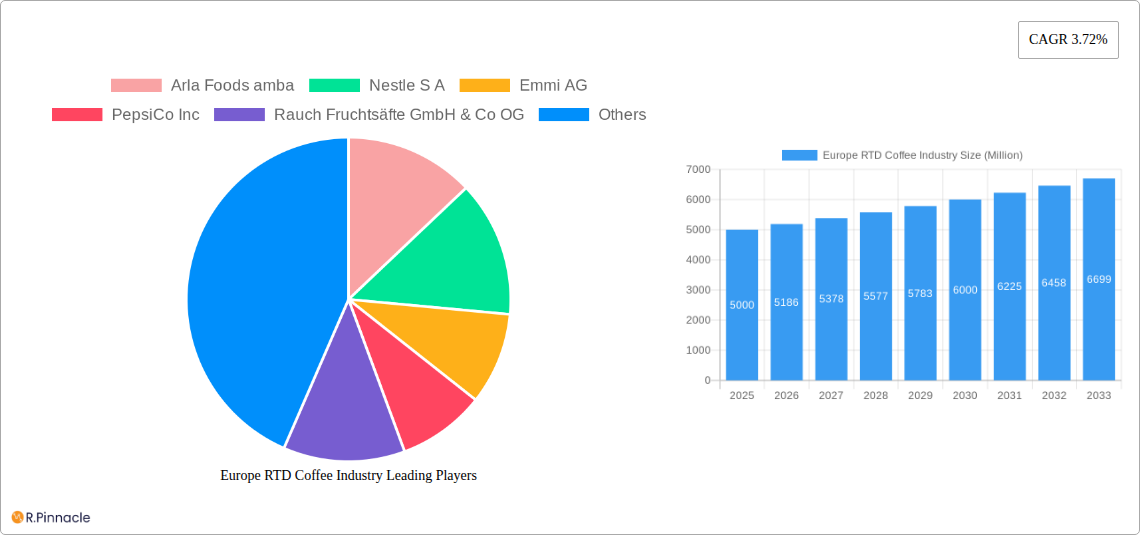

Market Concentration: The European RTD coffee market exhibits a moderately concentrated structure, with key players holding significant market share. Nestlé S.A. and PepsiCo Inc. are anticipated to hold approximately xx% and xx% of the market share, respectively, in 2025. Smaller players such as Rauch Fruchtsäfte and illycaffè S p A focus on niche segments, driving innovation and competition.

Innovation Drivers: Consumer demand for premiumization, convenience, and healthier options is driving innovation. The rise of cold brew coffee and plant-based alternatives fuels product diversification. Sustainability initiatives, including eco-friendly packaging, are gaining traction.

Regulatory Framework: EU regulations regarding food safety, labeling, and marketing significantly influence the industry. Changes in sugar taxes and health claims regulations necessitate ongoing adaptation by companies.

Product Substitutes: Other beverages like bottled tea, fruit juices, and energy drinks pose competitive threats, particularly within the convenience and on-the-go segments.

End-User Demographics: The primary consumer base comprises young adults and professionals seeking convenient and refreshing options. Growing health consciousness drives demand for low-sugar and functional beverages.

M&A Activities: The industry has witnessed notable M&A activity. For instance, Britvic PLC’s USD 300 Million acquisition of Jimmy's in July 2023 signifies the strategic importance of expanding the RTD coffee portfolio. Further M&A activity is anticipated, driving consolidation and market share shifts. Total M&A deal value for the period 2019-2024 is estimated at €xx Billion.

Europe RTD Coffee Industry Market Dynamics & Trends

This section delves into the key factors shaping the market's trajectory, including growth drivers, technological advancements, consumer preferences, and competitive dynamics. The analysis incorporates historical data (2019-2024) and projections for the forecast period (2025-2033).

The European RTD coffee market is experiencing robust growth, driven by the increasing popularity of convenient and refreshing coffee options. The market's compound annual growth rate (CAGR) is projected at xx% during the forecast period (2025-2033). This growth is primarily fueled by changing consumer lifestyles, with a rising preference for on-the-go consumption and the increasing demand for premium and specialized coffee products. Technological advancements in packaging and production processes are further enhancing efficiency and product quality. However, competitive intensity and price pressures from private label brands pose challenges to market expansion. Market penetration of RTD coffee is expected to reach xx% by 2033.

Dominant Regions & Segments in Europe RTD Coffee Industry

This section identifies the leading regions, countries, and product segments within the European RTD coffee market. The analysis considers key factors influencing market dominance, including economic conditions, consumer preferences, and distribution channels.

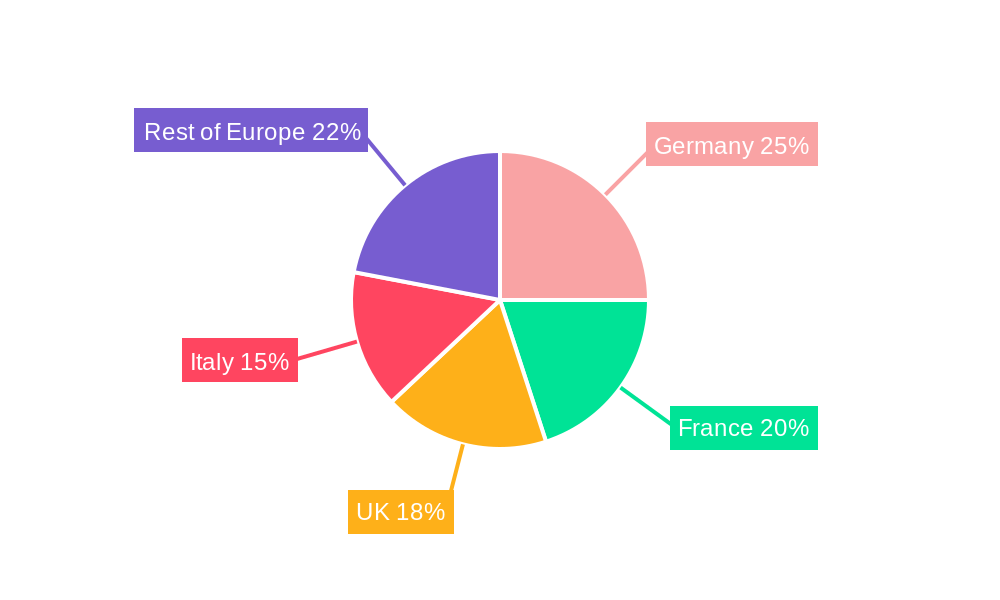

Leading Region: Western Europe, particularly Germany, UK and France, dominate the market due to high coffee consumption, strong distribution networks, and established consumer preferences for convenience beverages.

Leading Country: Germany exhibits the highest market share due to its large population and high per capita coffee consumption. Strong consumer preference for premium RTD coffee products, coupled with extensive distribution channels and a developed retail landscape, further contributes to the German market's prominence.

Dominant Segments:

- Packaging Type: PET Bottles hold a significant share, benefiting from their affordability and lightweight nature, suitable for on-the-go consumption.

- Distribution Channel: Off-trade channels (supermarkets, convenience stores) account for the largest market share, emphasizing the importance of retail distribution for product reach.

- Soft Drink Type: Iced coffee currently holds the largest segment of the RTD coffee market and shows the most robust growth, reflecting consumers' increasing demand for refreshing cold coffee options.

Key Drivers:

- Strong disposable incomes and a young, urban population in major markets.

- Well-developed retail infrastructure and efficient supply chains across Western Europe.

- Favorable government policies that promote the growth of the food and beverage industry.

Europe RTD Coffee Industry Product Innovations

Recent innovations focus on premiumization, health and wellness, and sustainability. Cold brew coffee continues to gain popularity, offering a smoother, less acidic taste profile. Plant-based milk alternatives, such as oat and almond milk, are increasingly incorporated to cater to a growing vegan consumer base. Companies are also prioritizing sustainable packaging options, such as recyclable and compostable materials. The integration of functional ingredients and convenient packaging formats further enhances product appeal and market fit.

Report Scope & Segmentation Analysis

This report segments the European RTD coffee market based on packaging type (aseptic packages, glass bottles, metal cans, PET bottles), distribution channel (off-trade, on-trade), and soft drink type (cold brew coffee, iced coffee, other RTD coffee). Each segment's market size, growth projections, and competitive landscape are analyzed individually. The market is expected to reach €xx Billion by 2033, with PET bottles maintaining a dominant share in packaging. The off-trade channel is projected to experience greater growth due to widespread retail accessibility. The iced coffee segment is expected to witness a surge in demand, driven by changing consumer preferences.

Key Drivers of Europe RTD Coffee Industry Growth

The growth of the European RTD coffee market is propelled by several key factors. Rising disposable incomes and changing lifestyles are driving demand for convenient and premium coffee options. The increasing popularity of cold brew coffee and plant-based alternatives further fuels market expansion. Technological advancements in packaging and production, facilitating efficient and sustainable practices, contribute to industry growth. Government regulations supporting the food and beverage sector provide favorable market conditions.

Challenges in the Europe RTD Coffee Industry Sector

The European RTD coffee market faces several challenges. Intense competition from established players and emerging brands creates price pressures and necessitates continuous innovation. Fluctuations in raw material costs (coffee beans, milk, sugar) impact profitability. Stringent regulatory requirements concerning food safety, labeling, and sustainability necessitate compliance, adding operational costs. Supply chain disruptions can affect production and distribution, creating uncertainty in market stability.

Emerging Opportunities in Europe RTD Coffee Industry

Emerging opportunities abound in the European RTD coffee market. The growing demand for premium and specialty coffee provides scope for introducing new product offerings, such as unique flavor profiles and functional beverages. Expansion into emerging markets with significant growth potential presents significant business prospects. The adoption of sustainable packaging solutions and the use of innovative production technologies enhance brand image and improve operational efficiency. The exploration of functional ingredients to create health-conscious products positions the RTD coffee market for sustainable future growth.

Leading Players in the Europe RTD Coffee Industry Market

- Arla Foods amba

- Nestlé S.A. [Nestlé]

- Emmi AG [Emmi]

- PepsiCo Inc. [PepsiCo]

- Rauch Fruchtsäfte GmbH & Co OG

- Crediton Dairy Ltd

- Luigi Lavazza S.p.A. [Lavazza]

- The Coca-Cola Company [Coca-Cola]

- Britvic PLC [Britvic]

- illycaffè S.p.A. [illycaffè]

- Sodiaal Union

- The Fayrefield Group Limited

Key Developments in Europe RTD Coffee Industry

July 2023: Britvic expands its portfolio with the acquisition of Jimmy's, the UK's fastest-growing RTD iced coffee brand, for USD 300 million, significantly boosting its market presence.

January 2023: Columbus Café & Co. and Sodiaal Cooperative partner to launch a range of iced lattes, expanding the product offerings in the market and capitalizing on the growing demand for convenient and premium coffee options.

August 2022: Sodiaal Union and Columbus Café & Co. collaborate to develop a range of innovative RTD coffee beverages (cappuccino, latte, chocolate, and Speculoos-flavored latte), increasing product diversity and attracting a broader consumer base.

Future Outlook for Europe RTD Coffee Industry Market

The future outlook for the European RTD coffee market remains highly positive. Continued growth is anticipated, driven by consistent demand for convenient, premium, and innovative coffee products. Further expansion into new markets and product categories is expected. Sustainability initiatives and the introduction of functional ingredients will shape the market's evolution. Strategic partnerships and M&A activity will continue to drive market consolidation and innovation. The market is poised for significant expansion, presenting substantial opportunities for existing and new entrants.

Europe RTD Coffee Industry Segmentation

-

1. Soft Drink Type

- 1.1. Cold Brew Coffee

- 1.2. Iced coffee

- 1.3. Other RTD Coffee

-

2. Packaging Type

- 2.1. Aseptic packages

- 2.2. Glass Bottles

- 2.3. Metal Can

- 2.4. PET Bottles

-

3. Distribution Channel

-

3.1. Off-trade

- 3.1.1. Convenience Stores

- 3.1.2. Online Retail

- 3.1.3. Specialty Stores

- 3.1.4. Supermarket/Hypermarket

- 3.1.5. Others

- 3.2. On-trade

-

3.1. Off-trade

Europe RTD Coffee Industry Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Netherlands

- 1.7. Belgium

- 1.8. Sweden

- 1.9. Norway

- 1.10. Poland

- 1.11. Denmark

Europe RTD Coffee Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 3.72% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Rising Consumer Awareness about Health and Fitness; Increasing the Use of Casein and Caseinate in Food and Beverage Industry

- 3.3. Market Restrains

- 3.3.1. High Competition From Alternative Protein Sources

- 3.4. Market Trends

- 3.4.1. OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Europe RTD Coffee Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Soft Drink Type

- 5.1.1. Cold Brew Coffee

- 5.1.2. Iced coffee

- 5.1.3. Other RTD Coffee

- 5.2. Market Analysis, Insights and Forecast - by Packaging Type

- 5.2.1. Aseptic packages

- 5.2.2. Glass Bottles

- 5.2.3. Metal Can

- 5.2.4. PET Bottles

- 5.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.3.1. Off-trade

- 5.3.1.1. Convenience Stores

- 5.3.1.2. Online Retail

- 5.3.1.3. Specialty Stores

- 5.3.1.4. Supermarket/Hypermarket

- 5.3.1.5. Others

- 5.3.2. On-trade

- 5.3.1. Off-trade

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by Soft Drink Type

- 6. Germany Europe RTD Coffee Industry Analysis, Insights and Forecast, 2019-2031

- 7. France Europe RTD Coffee Industry Analysis, Insights and Forecast, 2019-2031

- 8. Italy Europe RTD Coffee Industry Analysis, Insights and Forecast, 2019-2031

- 9. United Kingdom Europe RTD Coffee Industry Analysis, Insights and Forecast, 2019-2031

- 10. Netherlands Europe RTD Coffee Industry Analysis, Insights and Forecast, 2019-2031

- 11. Sweden Europe RTD Coffee Industry Analysis, Insights and Forecast, 2019-2031

- 12. Rest of Europe Europe RTD Coffee Industry Analysis, Insights and Forecast, 2019-2031

- 13. Competitive Analysis

- 13.1. Market Share Analysis 2024

- 13.2. Company Profiles

- 13.2.1 Arla Foods amba

- 13.2.1.1. Overview

- 13.2.1.2. Products

- 13.2.1.3. SWOT Analysis

- 13.2.1.4. Recent Developments

- 13.2.1.5. Financials (Based on Availability)

- 13.2.2 Nestle S A

- 13.2.2.1. Overview

- 13.2.2.2. Products

- 13.2.2.3. SWOT Analysis

- 13.2.2.4. Recent Developments

- 13.2.2.5. Financials (Based on Availability)

- 13.2.3 Emmi AG

- 13.2.3.1. Overview

- 13.2.3.2. Products

- 13.2.3.3. SWOT Analysis

- 13.2.3.4. Recent Developments

- 13.2.3.5. Financials (Based on Availability)

- 13.2.4 PepsiCo Inc

- 13.2.4.1. Overview

- 13.2.4.2. Products

- 13.2.4.3. SWOT Analysis

- 13.2.4.4. Recent Developments

- 13.2.4.5. Financials (Based on Availability)

- 13.2.5 Rauch Fruchtsäfte GmbH & Co OG

- 13.2.5.1. Overview

- 13.2.5.2. Products

- 13.2.5.3. SWOT Analysis

- 13.2.5.4. Recent Developments

- 13.2.5.5. Financials (Based on Availability)

- 13.2.6 Crediton Dairy Ltd

- 13.2.6.1. Overview

- 13.2.6.2. Products

- 13.2.6.3. SWOT Analysis

- 13.2.6.4. Recent Developments

- 13.2.6.5. Financials (Based on Availability)

- 13.2.7 Luigi Lavazza S p A

- 13.2.7.1. Overview

- 13.2.7.2. Products

- 13.2.7.3. SWOT Analysis

- 13.2.7.4. Recent Developments

- 13.2.7.5. Financials (Based on Availability)

- 13.2.8 The Coca-Cola Company

- 13.2.8.1. Overview

- 13.2.8.2. Products

- 13.2.8.3. SWOT Analysis

- 13.2.8.4. Recent Developments

- 13.2.8.5. Financials (Based on Availability)

- 13.2.9 Britvic PLC

- 13.2.9.1. Overview

- 13.2.9.2. Products

- 13.2.9.3. SWOT Analysis

- 13.2.9.4. Recent Developments

- 13.2.9.5. Financials (Based on Availability)

- 13.2.10 illycaffè S p A

- 13.2.10.1. Overview

- 13.2.10.2. Products

- 13.2.10.3. SWOT Analysis

- 13.2.10.4. Recent Developments

- 13.2.10.5. Financials (Based on Availability)

- 13.2.11 Sodiaal Union

- 13.2.11.1. Overview

- 13.2.11.2. Products

- 13.2.11.3. SWOT Analysis

- 13.2.11.4. Recent Developments

- 13.2.11.5. Financials (Based on Availability)

- 13.2.12 The Fayrefield Group Limite

- 13.2.12.1. Overview

- 13.2.12.2. Products

- 13.2.12.3. SWOT Analysis

- 13.2.12.4. Recent Developments

- 13.2.12.5. Financials (Based on Availability)

- 13.2.1 Arla Foods amba

List of Figures

- Figure 1: Europe RTD Coffee Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Europe RTD Coffee Industry Share (%) by Company 2024

List of Tables

- Table 1: Europe RTD Coffee Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Europe RTD Coffee Industry Revenue Million Forecast, by Soft Drink Type 2019 & 2032

- Table 3: Europe RTD Coffee Industry Revenue Million Forecast, by Packaging Type 2019 & 2032

- Table 4: Europe RTD Coffee Industry Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 5: Europe RTD Coffee Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 6: Europe RTD Coffee Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 7: Germany Europe RTD Coffee Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: France Europe RTD Coffee Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Italy Europe RTD Coffee Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: United Kingdom Europe RTD Coffee Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: Netherlands Europe RTD Coffee Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: Sweden Europe RTD Coffee Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: Rest of Europe Europe RTD Coffee Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: Europe RTD Coffee Industry Revenue Million Forecast, by Soft Drink Type 2019 & 2032

- Table 15: Europe RTD Coffee Industry Revenue Million Forecast, by Packaging Type 2019 & 2032

- Table 16: Europe RTD Coffee Industry Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 17: Europe RTD Coffee Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 18: United Kingdom Europe RTD Coffee Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 19: Germany Europe RTD Coffee Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 20: France Europe RTD Coffee Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 21: Italy Europe RTD Coffee Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 22: Spain Europe RTD Coffee Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 23: Netherlands Europe RTD Coffee Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 24: Belgium Europe RTD Coffee Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 25: Sweden Europe RTD Coffee Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 26: Norway Europe RTD Coffee Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 27: Poland Europe RTD Coffee Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 28: Denmark Europe RTD Coffee Industry Revenue (Million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe RTD Coffee Industry?

The projected CAGR is approximately 3.72%.

2. Which companies are prominent players in the Europe RTD Coffee Industry?

Key companies in the market include Arla Foods amba, Nestle S A, Emmi AG, PepsiCo Inc, Rauch Fruchtsäfte GmbH & Co OG, Crediton Dairy Ltd, Luigi Lavazza S p A, The Coca-Cola Company, Britvic PLC, illycaffè S p A, Sodiaal Union, The Fayrefield Group Limite.

3. What are the main segments of the Europe RTD Coffee Industry?

The market segments include Soft Drink Type, Packaging Type, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Rising Consumer Awareness about Health and Fitness; Increasing the Use of Casein and Caseinate in Food and Beverage Industry.

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

High Competition From Alternative Protein Sources.

8. Can you provide examples of recent developments in the market?

July 2023: Britvic expands its portfolio with the addition of the UK’s fastest growing ‘ready to drink’ iced coffee brand Jimmy's with a deal of USD 300 million.January 2023: Columbus Café & Co. and Sodiaal Cooperative signed a partnership to launch a range of iced lattes made up of 4 gourmet recipes in a resealable 25 cl brick, easy to taste and transport with its resealable bio-based plastic cap. The drinks will be sold in supermarkets, as well as in bakeries, Relay stores, or on the highways.August 2022: Sodiaal Union's Candia marketing & innovation teams, together with Columbus Café & Co., the French coffee shop network, developed a range of innovative RTD coffee beverages (cappuccino, latte, chocolate, and It offers latte, the signature of the chain, flavored with Speculoos)

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe RTD Coffee Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe RTD Coffee Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe RTD Coffee Industry?

To stay informed about further developments, trends, and reports in the Europe RTD Coffee Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence