Key Insights

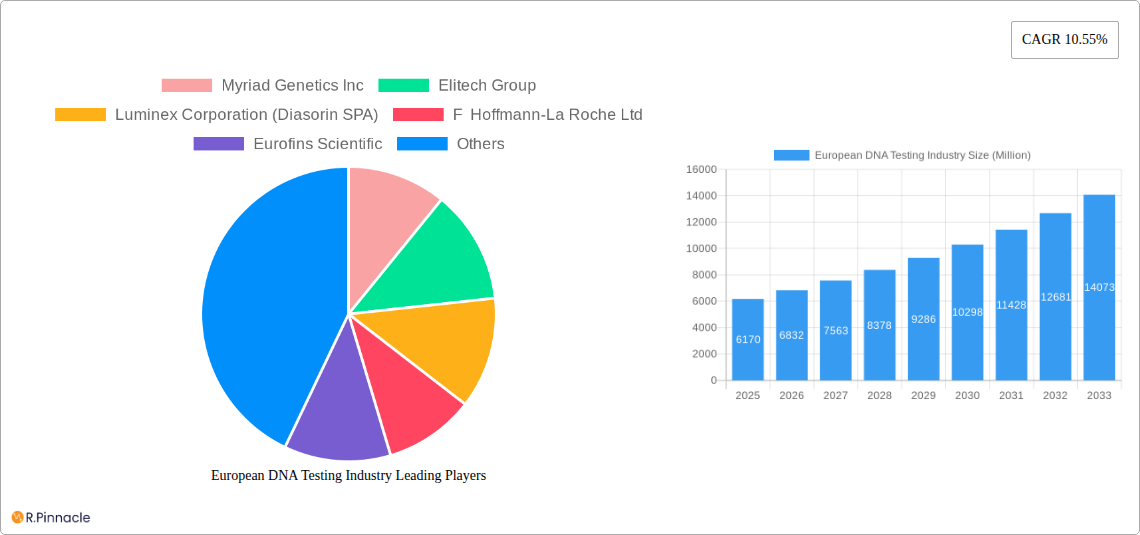

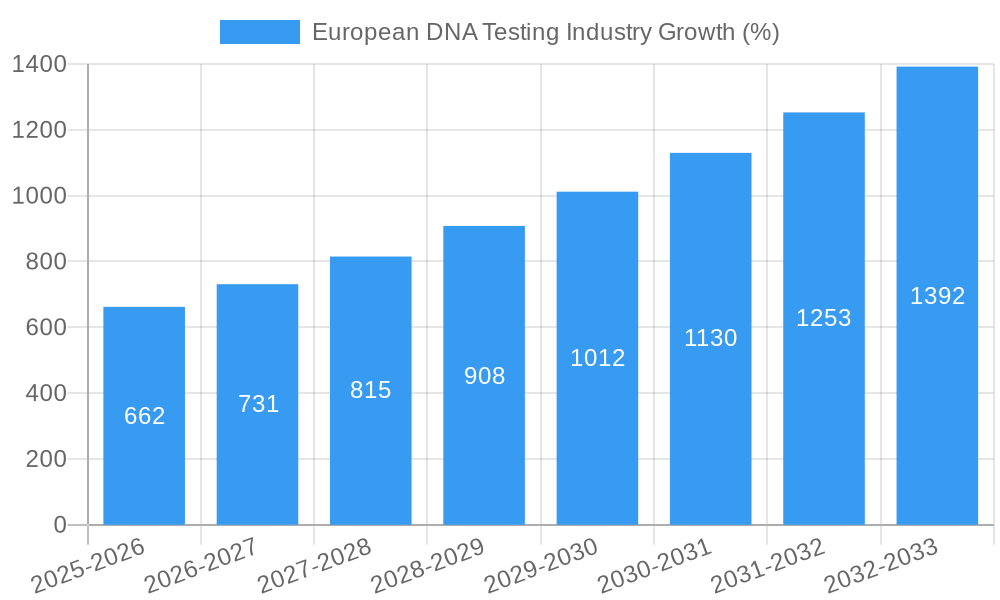

The European DNA testing market, valued at €6.17 billion in 2025, is projected to experience robust growth, exhibiting a Compound Annual Growth Rate (CAGR) of 10.55% from 2025 to 2033. This expansion is driven by several key factors. Increasing awareness of genetic predispositions to diseases like Alzheimer's, cancer, and cystic fibrosis is fueling demand for predictive and presymptomatic testing. Advancements in molecular testing technologies, offering higher accuracy and faster turnaround times, are further accelerating market growth. Government initiatives promoting early disease detection and personalized medicine are also contributing to market expansion. The segment breakdown reveals a significant portion of the market is allocated to diagnostic testing, driven by the rising prevalence of chronic diseases and the increasing adoption of DNA testing in clinical settings across major European countries like Germany, France, and the UK. Newborn screening programs, mandated in many European nations, also contribute substantially to the overall market size.

Growth is further propelled by the rising adoption of direct-to-consumer (DTC) genetic testing kits, which offer individuals insights into their ancestry, health risks, and traits. However, challenges remain. Concerns surrounding data privacy and ethical implications associated with genetic information are acting as restraints, particularly regarding the storage and use of sensitive personal data. Furthermore, the high cost of certain advanced DNA testing procedures can limit access for some segments of the population, potentially hindering overall market penetration. Despite these challenges, the market's positive trajectory is expected to continue, driven by technological innovation, increased accessibility, and a growing understanding of the benefits of DNA testing in healthcare. The strong presence of major players like Illumina, Thermo Fisher Scientific, and Roche in the European market underscores the region's significance in the global DNA testing landscape.

This comprehensive report provides a detailed analysis of the European DNA testing industry, covering market structure, dynamics, leading players, and future outlook. The study period spans from 2019 to 2033, with 2025 as the base and estimated year. The report is designed for industry professionals, investors, and anyone seeking a deep understanding of this rapidly evolving sector. The European DNA testing market is projected to reach xx Million by 2033, demonstrating significant growth potential.

European DNA Testing Industry Market Structure & Innovation Trends

This section analyzes the competitive landscape, innovation drivers, regulatory environment, and market dynamics within the European DNA testing industry. The market exhibits a moderately consolidated structure with key players such as Myriad Genetics Inc, Elitech Group, Luminex Corporation (Diasorin SPA), F Hoffmann-La Roche Ltd, Eurofins Scientific, 23andMe Inc, Abbott Laboratories, Blueprint Genetics Oy, Danaher Corporation, Qiagen, Illumina Inc, Centogene AG, and Thermo Fisher Scientific holding significant market share. However, the presence of numerous smaller players indicates a dynamic competitive environment.

Market Concentration: The market share held by the top 5 players is estimated at xx%, indicating a moderately consolidated structure. The remaining xx% is distributed across numerous smaller players, fostering competitive innovation.

Innovation Drivers:

- Advancements in Next-Generation Sequencing (NGS) technologies.

- Increased focus on personalized medicine and pharmacogenomics.

- Growing prevalence of genetic disorders and chronic diseases.

- Government initiatives promoting genetic testing and early disease detection.

Regulatory Frameworks: Stringent regulations regarding data privacy and patient consent significantly impact market growth and necessitate compliance with GDPR and other relevant directives.

Mergers & Acquisitions (M&A): The industry has witnessed several strategic M&A activities, with deal values totaling xx Million in the last five years. These activities have focused on expanding product portfolios, technological capabilities, and geographical reach. Examples include the August 2022 partnership between Myriad Genetics and Institut für Hämopathologie Hamburg and Centre Georges-Francois LeClerc.

European DNA Testing Industry Market Dynamics & Trends

The European DNA testing market is experiencing robust growth, driven by factors such as increasing awareness of genetic diseases, technological advancements, and supportive government policies. The market's Compound Annual Growth Rate (CAGR) during the historical period (2019-2024) was xx%, and is projected to be xx% during the forecast period (2025-2033). Market penetration for various testing types varies significantly, with prenatal and carrier testing showing higher penetration rates compared to others. Technological disruptions, such as the development of more affordable and accessible NGS technologies, are further accelerating market expansion. Consumer preferences are shifting towards direct-to-consumer (DTC) testing, although regulatory scrutiny in this area continues. Competitive dynamics are characterized by both intense competition among established players and the emergence of innovative startups.

Dominant Regions & Segments in European DNA Testing Industry

The European DNA testing market exhibits regional variations in growth and adoption rates. Western European countries, particularly Germany, France, and the UK, currently dominate the market due to higher healthcare expenditure, advanced healthcare infrastructure, and greater awareness of genetic testing.

Leading Regions:

- Western Europe (Germany, France, UK) – Driven by high healthcare spending, advanced infrastructure, and strong regulatory frameworks.

- Northern Europe (xx) – Experiencing steady growth due to increasing adoption of advanced technologies.

- Southern Europe (xx) – Growth is relatively slower due to various economic and infrastructural factors.

Dominant Segments:

By Type: Prenatal testing is the largest segment due to increasing demand for non-invasive prenatal screening (NIPS). Carrier testing is also experiencing significant growth driven by rising awareness of inherited genetic disorders.

By Disease: Cancer testing dominates the market due to high prevalence and improved testing technologies. Genetic testing for other diseases such as cystic fibrosis, sickle cell anemia and Huntington's Disease is also growing.

By Technology: Molecular testing, particularly PCR and NGS, is the most rapidly growing segment due to its high sensitivity, specificity, and automation capabilities.

Key Drivers:

- Government funding for research and development of new diagnostic tools.

- Strong healthcare infrastructure in leading European countries.

- Increasing awareness and understanding of genetic testing amongst healthcare professionals and the general population.

European DNA Testing Industry Product Innovations

Recent product innovations include the development of advanced NGS platforms that offer faster, cheaper, and more accurate sequencing capabilities. This leads to an expansion of applications in areas such as carrier screening, prenatal diagnostics, and pharmacogenomics. These advancements improve clinical decision-making, enabling earlier intervention and improved patient outcomes. Companies are also focusing on developing user-friendly and accessible tests to enhance market penetration and increase adoption rates.

Report Scope & Segmentation Analysis

This report segments the European DNA testing market by type (carrier, diagnostic, newborn screening, predictive/presymptomatic, prenatal, other), disease (Alzheimer’s, cancer, cystic fibrosis, sickle cell anemia, Duchenne muscular dystrophy, thalassemia, Huntington’s disease, other), and technology (cytogenetic, biochemical, molecular). Each segment is analyzed based on market size, growth rate, and competitive landscape. Market sizes are provided for each segment across the historical, base, and forecast periods, along with detailed competitive analysis highlighting major players and market shares for each segment.

Key Drivers of European DNA Testing Industry Growth

The European DNA testing industry's growth is primarily driven by several factors, including the increasing prevalence of genetic diseases, technological advancements such as NGS leading to cost reductions and improved accuracy, increasing government support for research and development, growing awareness of the benefits of personalized medicine, and supportive regulatory frameworks promoting the adoption of advanced genetic testing technologies. The rising demand for prenatal testing, particularly non-invasive methods, is also contributing significantly to market expansion.

Challenges in the European DNA Testing Industry Sector

The European DNA testing market faces challenges including high costs associated with advanced testing technologies, stringent regulatory requirements around data privacy and patient consent impacting market accessibility, ethical concerns regarding genetic information usage, and variations in healthcare reimbursement policies across different European countries. The emergence of several direct-to-consumer (DTC) genetic testing companies also creates competitive pressures.

Emerging Opportunities in European DNA Testing Industry

Emerging opportunities lie in the expansion of DTC testing (with appropriate regulatory oversight), development of new diagnostic tests for rare diseases, application of AI and machine learning for data analysis and improved diagnostics, and expansion into emerging markets within Europe. The integration of genetic testing with other diagnostic modalities holds great potential for improving healthcare outcomes.

Leading Players in the European DNA Testing Industry Market

- Myriad Genetics Inc (Myriad Genetics Inc)

- Elitech Group

- Luminex Corporation (Diasorin SPA) (Diasorin SPA)

- F Hoffmann-La Roche Ltd (F Hoffmann-La Roche Ltd)

- Eurofins Scientific (Eurofins Scientific)

- 23andMe Inc (23andMe Inc)

- Abbott Laboratories (Abbott Laboratories)

- Blueprint Genetics Oy

- Danaher Corporation (Danaher Corporation)

- Qiagen (Qiagen)

- Illumina Inc (Illumina Inc)

- Centogene AG

- Thermo Fisher Scientific (Thermo Fisher Scientific)

Key Developments in European DNA Testing Industry

- August 2022: Myriad Genetics partnered with Institut für Hämopathologie Hamburg and Centre Georges-Francois LeClerc to expand access to genetic testing in Europe, bringing MyChoice CDx Plus Testing to Germany and France.

- October 2022: NHS England launched a national genetic testing service, enabling rapid life-saving checks for children and babies, processing simple blood tests within days for over 6,000 genetic diseases.

Future Outlook for European DNA Testing Industry Market

The future of the European DNA testing industry is bright, with continued growth driven by technological advancements, increasing awareness, and supportive regulatory environments. Strategic opportunities lie in developing innovative diagnostic tools for a broader range of diseases, focusing on early detection and personalized medicine approaches. Further consolidation within the industry through M&A activity is also anticipated. The expansion of testing capabilities into previously underserved populations will drive future market growth.

European DNA Testing Industry Segmentation

-

1. Type

- 1.1. Carrier Testing

- 1.2. Diagnostic Testing

- 1.3. Newborn Screening

- 1.4. Predictive and Presymptomatic Testing

- 1.5. Prenatal Testing

- 1.6. Other Types

-

2. Disease

- 2.1. Alzheimer's Disease

- 2.2. Cancer

- 2.3. Cystic Fibrosis

- 2.4. Sickle Cell Anemia

- 2.5. Duchenne Muscular Dystrophy

- 2.6. Thalassemia

- 2.7. Huntington's Disease

- 2.8. Other Diseases

-

3. Technology

- 3.1. Cytogenetic Testing

- 3.2. Biochemical Testing

- 3.3. Molecular Testing

European DNA Testing Industry Segmentation By Geography

- 1. Germany

- 2. United Kingdom

- 3. France

- 4. Italy

- 5. Spain

- 6. Rest of Europe

European DNA Testing Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 10.55% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increasing Emphasis on Early Disease Detection and Prevention; Increasing Demand for Personalized Medicine; Increasing Application of Genetic Testing in Oncology

- 3.3. Market Restrains

- 3.3.1. High Costs of Genetic Testing; Social and Ethical Implications of Genetic Testing

- 3.4. Market Trends

- 3.4.1. The Diagnostic Testing Segment is Expected to Hold a Significant Share Over the Forecast Period

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. European DNA Testing Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Carrier Testing

- 5.1.2. Diagnostic Testing

- 5.1.3. Newborn Screening

- 5.1.4. Predictive and Presymptomatic Testing

- 5.1.5. Prenatal Testing

- 5.1.6. Other Types

- 5.2. Market Analysis, Insights and Forecast - by Disease

- 5.2.1. Alzheimer's Disease

- 5.2.2. Cancer

- 5.2.3. Cystic Fibrosis

- 5.2.4. Sickle Cell Anemia

- 5.2.5. Duchenne Muscular Dystrophy

- 5.2.6. Thalassemia

- 5.2.7. Huntington's Disease

- 5.2.8. Other Diseases

- 5.3. Market Analysis, Insights and Forecast - by Technology

- 5.3.1. Cytogenetic Testing

- 5.3.2. Biochemical Testing

- 5.3.3. Molecular Testing

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Germany

- 5.4.2. United Kingdom

- 5.4.3. France

- 5.4.4. Italy

- 5.4.5. Spain

- 5.4.6. Rest of Europe

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Germany European DNA Testing Industry Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Carrier Testing

- 6.1.2. Diagnostic Testing

- 6.1.3. Newborn Screening

- 6.1.4. Predictive and Presymptomatic Testing

- 6.1.5. Prenatal Testing

- 6.1.6. Other Types

- 6.2. Market Analysis, Insights and Forecast - by Disease

- 6.2.1. Alzheimer's Disease

- 6.2.2. Cancer

- 6.2.3. Cystic Fibrosis

- 6.2.4. Sickle Cell Anemia

- 6.2.5. Duchenne Muscular Dystrophy

- 6.2.6. Thalassemia

- 6.2.7. Huntington's Disease

- 6.2.8. Other Diseases

- 6.3. Market Analysis, Insights and Forecast - by Technology

- 6.3.1. Cytogenetic Testing

- 6.3.2. Biochemical Testing

- 6.3.3. Molecular Testing

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. United Kingdom European DNA Testing Industry Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Carrier Testing

- 7.1.2. Diagnostic Testing

- 7.1.3. Newborn Screening

- 7.1.4. Predictive and Presymptomatic Testing

- 7.1.5. Prenatal Testing

- 7.1.6. Other Types

- 7.2. Market Analysis, Insights and Forecast - by Disease

- 7.2.1. Alzheimer's Disease

- 7.2.2. Cancer

- 7.2.3. Cystic Fibrosis

- 7.2.4. Sickle Cell Anemia

- 7.2.5. Duchenne Muscular Dystrophy

- 7.2.6. Thalassemia

- 7.2.7. Huntington's Disease

- 7.2.8. Other Diseases

- 7.3. Market Analysis, Insights and Forecast - by Technology

- 7.3.1. Cytogenetic Testing

- 7.3.2. Biochemical Testing

- 7.3.3. Molecular Testing

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. France European DNA Testing Industry Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Carrier Testing

- 8.1.2. Diagnostic Testing

- 8.1.3. Newborn Screening

- 8.1.4. Predictive and Presymptomatic Testing

- 8.1.5. Prenatal Testing

- 8.1.6. Other Types

- 8.2. Market Analysis, Insights and Forecast - by Disease

- 8.2.1. Alzheimer's Disease

- 8.2.2. Cancer

- 8.2.3. Cystic Fibrosis

- 8.2.4. Sickle Cell Anemia

- 8.2.5. Duchenne Muscular Dystrophy

- 8.2.6. Thalassemia

- 8.2.7. Huntington's Disease

- 8.2.8. Other Diseases

- 8.3. Market Analysis, Insights and Forecast - by Technology

- 8.3.1. Cytogenetic Testing

- 8.3.2. Biochemical Testing

- 8.3.3. Molecular Testing

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Italy European DNA Testing Industry Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Carrier Testing

- 9.1.2. Diagnostic Testing

- 9.1.3. Newborn Screening

- 9.1.4. Predictive and Presymptomatic Testing

- 9.1.5. Prenatal Testing

- 9.1.6. Other Types

- 9.2. Market Analysis, Insights and Forecast - by Disease

- 9.2.1. Alzheimer's Disease

- 9.2.2. Cancer

- 9.2.3. Cystic Fibrosis

- 9.2.4. Sickle Cell Anemia

- 9.2.5. Duchenne Muscular Dystrophy

- 9.2.6. Thalassemia

- 9.2.7. Huntington's Disease

- 9.2.8. Other Diseases

- 9.3. Market Analysis, Insights and Forecast - by Technology

- 9.3.1. Cytogenetic Testing

- 9.3.2. Biochemical Testing

- 9.3.3. Molecular Testing

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Spain European DNA Testing Industry Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Carrier Testing

- 10.1.2. Diagnostic Testing

- 10.1.3. Newborn Screening

- 10.1.4. Predictive and Presymptomatic Testing

- 10.1.5. Prenatal Testing

- 10.1.6. Other Types

- 10.2. Market Analysis, Insights and Forecast - by Disease

- 10.2.1. Alzheimer's Disease

- 10.2.2. Cancer

- 10.2.3. Cystic Fibrosis

- 10.2.4. Sickle Cell Anemia

- 10.2.5. Duchenne Muscular Dystrophy

- 10.2.6. Thalassemia

- 10.2.7. Huntington's Disease

- 10.2.8. Other Diseases

- 10.3. Market Analysis, Insights and Forecast - by Technology

- 10.3.1. Cytogenetic Testing

- 10.3.2. Biochemical Testing

- 10.3.3. Molecular Testing

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Rest of Europe European DNA Testing Industry Analysis, Insights and Forecast, 2019-2031

- 11.1. Market Analysis, Insights and Forecast - by Type

- 11.1.1. Carrier Testing

- 11.1.2. Diagnostic Testing

- 11.1.3. Newborn Screening

- 11.1.4. Predictive and Presymptomatic Testing

- 11.1.5. Prenatal Testing

- 11.1.6. Other Types

- 11.2. Market Analysis, Insights and Forecast - by Disease

- 11.2.1. Alzheimer's Disease

- 11.2.2. Cancer

- 11.2.3. Cystic Fibrosis

- 11.2.4. Sickle Cell Anemia

- 11.2.5. Duchenne Muscular Dystrophy

- 11.2.6. Thalassemia

- 11.2.7. Huntington's Disease

- 11.2.8. Other Diseases

- 11.3. Market Analysis, Insights and Forecast - by Technology

- 11.3.1. Cytogenetic Testing

- 11.3.2. Biochemical Testing

- 11.3.3. Molecular Testing

- 11.1. Market Analysis, Insights and Forecast - by Type

- 12. Germany European DNA Testing Industry Analysis, Insights and Forecast, 2019-2031

- 13. France European DNA Testing Industry Analysis, Insights and Forecast, 2019-2031

- 14. Italy European DNA Testing Industry Analysis, Insights and Forecast, 2019-2031

- 15. United Kingdom European DNA Testing Industry Analysis, Insights and Forecast, 2019-2031

- 16. Netherlands European DNA Testing Industry Analysis, Insights and Forecast, 2019-2031

- 17. Sweden European DNA Testing Industry Analysis, Insights and Forecast, 2019-2031

- 18. Rest of Europe European DNA Testing Industry Analysis, Insights and Forecast, 2019-2031

- 19. Competitive Analysis

- 19.1. Market Share Analysis 2024

- 19.2. Company Profiles

- 19.2.1 Myriad Genetics Inc

- 19.2.1.1. Overview

- 19.2.1.2. Products

- 19.2.1.3. SWOT Analysis

- 19.2.1.4. Recent Developments

- 19.2.1.5. Financials (Based on Availability)

- 19.2.2 Elitech Group

- 19.2.2.1. Overview

- 19.2.2.2. Products

- 19.2.2.3. SWOT Analysis

- 19.2.2.4. Recent Developments

- 19.2.2.5. Financials (Based on Availability)

- 19.2.3 Luminex Corporation (Diasorin SPA)

- 19.2.3.1. Overview

- 19.2.3.2. Products

- 19.2.3.3. SWOT Analysis

- 19.2.3.4. Recent Developments

- 19.2.3.5. Financials (Based on Availability)

- 19.2.4 F Hoffmann-La Roche Ltd

- 19.2.4.1. Overview

- 19.2.4.2. Products

- 19.2.4.3. SWOT Analysis

- 19.2.4.4. Recent Developments

- 19.2.4.5. Financials (Based on Availability)

- 19.2.5 Eurofins Scientific

- 19.2.5.1. Overview

- 19.2.5.2. Products

- 19.2.5.3. SWOT Analysis

- 19.2.5.4. Recent Developments

- 19.2.5.5. Financials (Based on Availability)

- 19.2.6 F Hoffmann-La Roche Ltd*List Not Exhaustive

- 19.2.6.1. Overview

- 19.2.6.2. Products

- 19.2.6.3. SWOT Analysis

- 19.2.6.4. Recent Developments

- 19.2.6.5. Financials (Based on Availability)

- 19.2.7 23andMe Inc

- 19.2.7.1. Overview

- 19.2.7.2. Products

- 19.2.7.3. SWOT Analysis

- 19.2.7.4. Recent Developments

- 19.2.7.5. Financials (Based on Availability)

- 19.2.8 Abbott Laboratories

- 19.2.8.1. Overview

- 19.2.8.2. Products

- 19.2.8.3. SWOT Analysis

- 19.2.8.4. Recent Developments

- 19.2.8.5. Financials (Based on Availability)

- 19.2.9 Blueprint Genetics Oy

- 19.2.9.1. Overview

- 19.2.9.2. Products

- 19.2.9.3. SWOT Analysis

- 19.2.9.4. Recent Developments

- 19.2.9.5. Financials (Based on Availability)

- 19.2.10 Danaher Corporation

- 19.2.10.1. Overview

- 19.2.10.2. Products

- 19.2.10.3. SWOT Analysis

- 19.2.10.4. Recent Developments

- 19.2.10.5. Financials (Based on Availability)

- 19.2.11 Qiagen

- 19.2.11.1. Overview

- 19.2.11.2. Products

- 19.2.11.3. SWOT Analysis

- 19.2.11.4. Recent Developments

- 19.2.11.5. Financials (Based on Availability)

- 19.2.12 Illumina Inc

- 19.2.12.1. Overview

- 19.2.12.2. Products

- 19.2.12.3. SWOT Analysis

- 19.2.12.4. Recent Developments

- 19.2.12.5. Financials (Based on Availability)

- 19.2.13 Centogene AG

- 19.2.13.1. Overview

- 19.2.13.2. Products

- 19.2.13.3. SWOT Analysis

- 19.2.13.4. Recent Developments

- 19.2.13.5. Financials (Based on Availability)

- 19.2.14 Thermo Fisher Scientific

- 19.2.14.1. Overview

- 19.2.14.2. Products

- 19.2.14.3. SWOT Analysis

- 19.2.14.4. Recent Developments

- 19.2.14.5. Financials (Based on Availability)

- 19.2.1 Myriad Genetics Inc

List of Figures

- Figure 1: European DNA Testing Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: European DNA Testing Industry Share (%) by Company 2024

List of Tables

- Table 1: European DNA Testing Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: European DNA Testing Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 3: European DNA Testing Industry Revenue Million Forecast, by Disease 2019 & 2032

- Table 4: European DNA Testing Industry Revenue Million Forecast, by Technology 2019 & 2032

- Table 5: European DNA Testing Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 6: European DNA Testing Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 7: Germany European DNA Testing Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: France European DNA Testing Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Italy European DNA Testing Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: United Kingdom European DNA Testing Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: Netherlands European DNA Testing Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: Sweden European DNA Testing Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: Rest of Europe European DNA Testing Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: European DNA Testing Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 15: European DNA Testing Industry Revenue Million Forecast, by Disease 2019 & 2032

- Table 16: European DNA Testing Industry Revenue Million Forecast, by Technology 2019 & 2032

- Table 17: European DNA Testing Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 18: European DNA Testing Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 19: European DNA Testing Industry Revenue Million Forecast, by Disease 2019 & 2032

- Table 20: European DNA Testing Industry Revenue Million Forecast, by Technology 2019 & 2032

- Table 21: European DNA Testing Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 22: European DNA Testing Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 23: European DNA Testing Industry Revenue Million Forecast, by Disease 2019 & 2032

- Table 24: European DNA Testing Industry Revenue Million Forecast, by Technology 2019 & 2032

- Table 25: European DNA Testing Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 26: European DNA Testing Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 27: European DNA Testing Industry Revenue Million Forecast, by Disease 2019 & 2032

- Table 28: European DNA Testing Industry Revenue Million Forecast, by Technology 2019 & 2032

- Table 29: European DNA Testing Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 30: European DNA Testing Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 31: European DNA Testing Industry Revenue Million Forecast, by Disease 2019 & 2032

- Table 32: European DNA Testing Industry Revenue Million Forecast, by Technology 2019 & 2032

- Table 33: European DNA Testing Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 34: European DNA Testing Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 35: European DNA Testing Industry Revenue Million Forecast, by Disease 2019 & 2032

- Table 36: European DNA Testing Industry Revenue Million Forecast, by Technology 2019 & 2032

- Table 37: European DNA Testing Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the European DNA Testing Industry?

The projected CAGR is approximately 10.55%.

2. Which companies are prominent players in the European DNA Testing Industry?

Key companies in the market include Myriad Genetics Inc, Elitech Group, Luminex Corporation (Diasorin SPA), F Hoffmann-La Roche Ltd, Eurofins Scientific, F Hoffmann-La Roche Ltd*List Not Exhaustive, 23andMe Inc, Abbott Laboratories, Blueprint Genetics Oy, Danaher Corporation, Qiagen, Illumina Inc, Centogene AG, Thermo Fisher Scientific.

3. What are the main segments of the European DNA Testing Industry?

The market segments include Type, Disease, Technology.

4. Can you provide details about the market size?

The market size is estimated to be USD 6.17 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Emphasis on Early Disease Detection and Prevention; Increasing Demand for Personalized Medicine; Increasing Application of Genetic Testing in Oncology.

6. What are the notable trends driving market growth?

The Diagnostic Testing Segment is Expected to Hold a Significant Share Over the Forecast Period.

7. Are there any restraints impacting market growth?

High Costs of Genetic Testing; Social and Ethical Implications of Genetic Testing.

8. Can you provide examples of recent developments in the market?

October 2022: NHS England launched a national genetic testing service to deliver rapid life-saving checks for children and babies. As a result of the launch, patients can undergo simple blood tests. Once they are processed, the service is likely to give medical teams from across the country results within days, meaning they can kick-start lifesaving treatment plans for more than 6,000 genetic diseases.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "European DNA Testing Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the European DNA Testing Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the European DNA Testing Industry?

To stay informed about further developments, trends, and reports in the European DNA Testing Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence