Key Insights

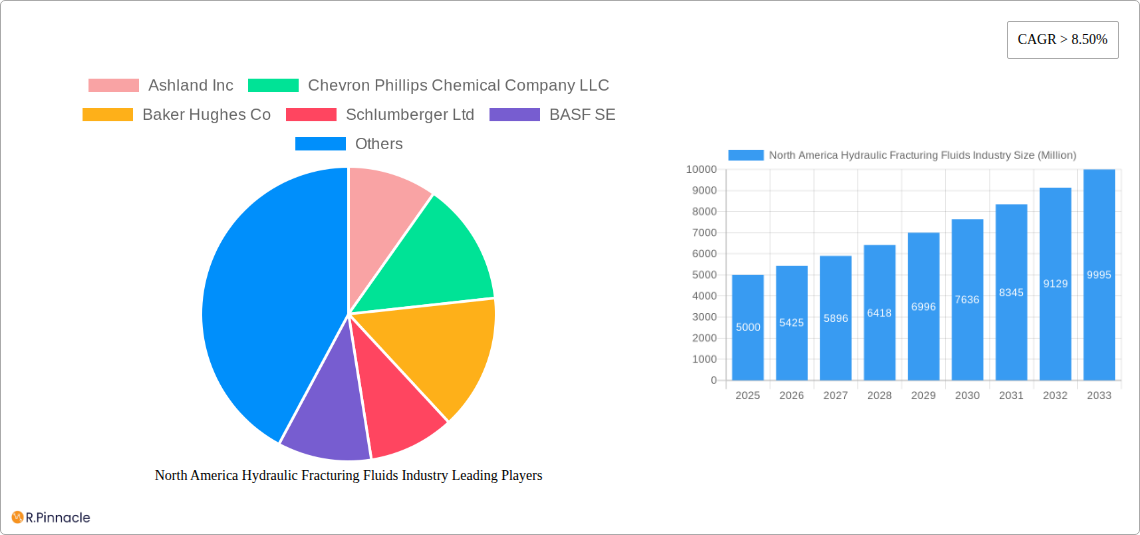

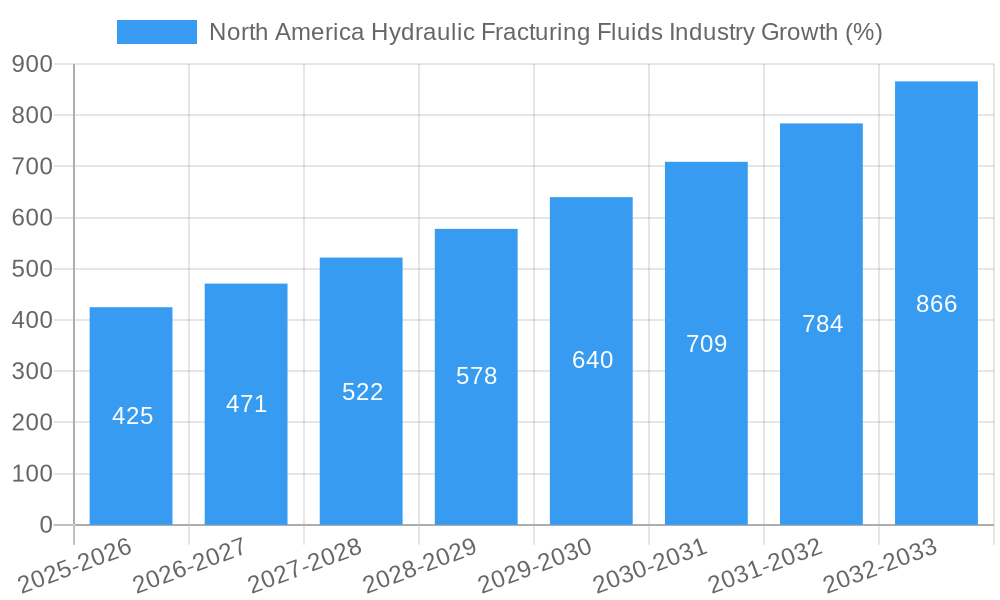

The North American hydraulic fracturing fluids market is experiencing robust growth, driven by the increasing demand for shale gas and oil extraction. With a Compound Annual Growth Rate (CAGR) exceeding 8.5% from 2019 to 2024, and a projected continuation of this trend through 2033, this sector presents significant opportunities for investors and industry players. The market size in 2025 is estimated to be in the billions (precise figure unavailable from provided data, but readily estimable through public market research reports and expert analysis of related industry data.). Horizontal well types currently dominate the market, reflecting the efficiency gains in shale gas and oil production. Slick water-based fluids remain the most widely used fluid type due to their cost-effectiveness and environmental considerations, although the demand for other base fluids is steadily increasing due to evolving technological advancements and varied geological formations. Key players such as Ashland Inc., Chevron Phillips Chemical Company LLC, and Baker Hughes Co. are actively involved in innovation and expansion to capitalize on this market's potential. Growth is further fueled by technological advancements aimed at enhancing extraction efficiency and minimizing environmental impact.

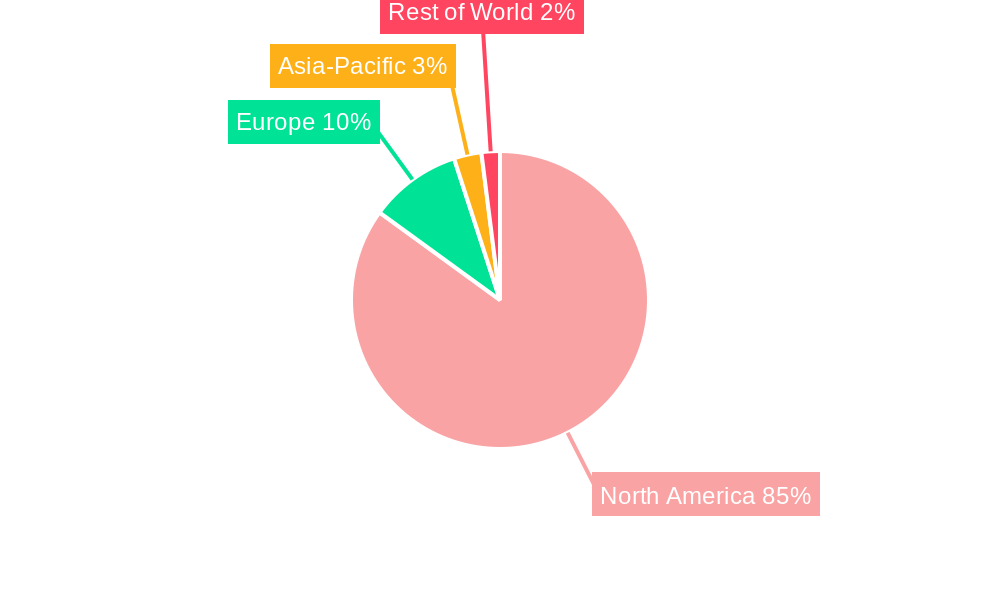

Despite the positive outlook, the market faces certain restraints. These include fluctuating oil and gas prices, stringent environmental regulations aimed at reducing the impact of hydraulic fracturing on water resources and ecosystems, and concerns about the potential for induced seismicity. However, continuous technological advancements focusing on eco-friendly solutions and improved operational safety are expected to mitigate these challenges. The regional focus remains heavily concentrated in the United States, with Canada and Mexico representing smaller, albeit growing, segments. The consistent demand for energy and the ongoing exploration of shale reserves will likely continue to underpin the expansive growth trajectory of this market in the coming years. The North American market's dominance is expected to persist, fueled by robust shale gas and oil reserves and a supportive regulatory environment (relative to other regions).

North America Hydraulic Fracturing Fluids Industry: 2019-2033 Market Report

This comprehensive report provides an in-depth analysis of the North America hydraulic fracturing fluids industry, covering the period from 2019 to 2033. It offers actionable insights for industry professionals, investors, and stakeholders seeking to understand the market's dynamics, growth drivers, and future potential. The report leverages extensive data analysis to provide a clear picture of the current landscape and forecast future trends. The total market size in 2025 is estimated at $XX Million, with a projected Compound Annual Growth Rate (CAGR) of XX% during the forecast period (2025-2033).

North America Hydraulic Fracturing Fluids Industry Market Structure & Innovation Trends

This section analyzes the competitive landscape, innovation drivers, and regulatory influences shaping the North American hydraulic fracturing fluids market. The market exhibits moderate concentration, with key players such as Ashland Inc, Chevron Phillips Chemical Company LLC, Baker Hughes Co, Schlumberger Ltd, BASF SE, DuPont de Nemours Inc, Halliburton Company, Akzonobel NV, Clariant International Ltd, and Calfrac Well Services Ltd holding significant market share. However, the list is not exhaustive, and smaller, specialized companies also contribute. Market share data for 2024 reveals that the top five players account for approximately XX% of the total market.

M&A activity has been moderate in recent years, with deal values totaling approximately $XX Million in 2024. Innovation is driven by the need for environmentally friendly fluids, improved efficiency, and reduced wellbore damage. Regulatory frameworks, particularly concerning environmental protection and waste disposal, significantly influence the industry. The market also faces pressure from substitute technologies such as alternative completion methods. End-user demographics are primarily focused on oil and gas exploration and production companies in key regions of North America.

North America Hydraulic Fracturing Fluids Industry Market Dynamics & Trends

The North American hydraulic fracturing fluids market is experiencing dynamic growth fueled by several key factors. The increasing demand for shale gas and tight oil, driven by energy security concerns and price fluctuations, is a major driver. Technological advancements in fracturing techniques and fluid formulations are enhancing efficiency and reducing costs. Furthermore, the ongoing exploration and development of unconventional resources in regions like the Permian Basin and Bakken Shale continue to bolster demand.

However, the market also faces challenges. Fluctuations in oil and gas prices can significantly impact investment decisions and demand. Environmental concerns and stricter regulations around water usage and waste disposal pose significant operational and financial constraints. Competition among established players and the emergence of new entrants are also influencing market dynamics. The market penetration of slickwater-based fluids remains dominant, exceeding XX% in 2024.

Dominant Regions & Segments in North America Hydraulic Fracturing Fluids Industry

The Permian Basin in the United States and the Montney formation in Canada are currently the dominant regions for hydraulic fracturing fluid consumption, driven by significant unconventional resource development activities.

- Key Drivers for the Permian Basin: Abundant shale resources, existing infrastructure, supportive government policies, and substantial investments.

- Key Drivers for the Montney Formation: Significant natural gas reserves, growing pipeline capacity, and favorable regulatory environments.

Within the segment breakdown:

- Well Type: Horizontal wells constitute the largest segment, accounting for approximately XX% of total consumption in 2024, due to their higher productivity compared to vertical wells.

- Fluid Type: Slickwater-based fluids are the dominant fluid type, reflecting cost-effectiveness and technological maturity. However, the demand for environmentally friendly fluids like foam-based and other base fluids is steadily growing.

North America Hydraulic Fracturing Fluids Industry Product Innovations

Recent innovations focus on developing environmentally friendly and cost-effective fluids. This includes the development of bio-based additives, improved rheology modifiers, and enhanced proppant suspensions. These advancements aim to minimize environmental impact while improving fracture propagation and proppant placement efficiency. The focus on enhanced performance and reduced environmental footprint is shaping the competitive landscape and creating opportunities for specialized providers.

Report Scope & Segmentation Analysis

This report segments the North American hydraulic fracturing fluids market based on well type (horizontal and vertical) and fluid type (slickwater-based fluid, foam-based fluid, gelled oil-based fluid, and other base fluids). Each segment is analyzed based on historical data (2019-2024), current estimates (2025), and future projections (2025-2033). The report provides detailed analysis of market size, growth rate, and competitive dynamics for each segment. For example, the slickwater-based fluid segment is expected to maintain its dominance, with a projected CAGR of XX% during the forecast period, while the demand for other base fluids is expected to grow at a faster pace due to increasing environmental regulations and technological advancements.

Key Drivers of North America Hydraulic Fracturing Fluids Industry Growth

Several factors are driving the growth of the North American hydraulic fracturing fluids market:

- Increased demand for shale gas and tight oil: Driven by energy security concerns and fluctuating oil prices.

- Technological advancements: Leading to increased efficiency and reduced costs in hydraulic fracturing operations.

- Government support and incentives: Including tax breaks and streamlined permitting processes in some regions.

Challenges in the North America Hydraulic Fracturing Fluids Industry Sector

The industry faces challenges including:

- Environmental regulations: Stricter rules on water usage and waste disposal increasing operational costs.

- Fluctuations in oil and gas prices: Affecting investment decisions and demand.

- Supply chain disruptions: Impacting the availability and cost of raw materials.

Emerging Opportunities in North America Hydraulic Fracturing Fluids Industry

Emerging opportunities include:

- Development of environmentally friendly fluids: Meeting growing regulatory requirements and consumer preferences.

- Expansion into new geographical areas: Exploring unconventional resources in less-developed regions.

- Technological advancements: Improving efficiency and reducing costs through innovations like automated systems and data analytics.

Leading Players in the North America Hydraulic Fracturing Fluids Industry Market

- Ashland Inc

- Chevron Phillips Chemical Company LLC

- Baker Hughes Co

- Schlumberger Ltd

- BASF SE

- DuPont de Nemours Inc

- Halliburton Company

- Akzonobel NV

- Clariant International Ltd

- Calfrac Well Services Ltd

Key Developments in North America Hydraulic Fracturing Fluids Industry Industry

- 2024 Q4: Ashland Inc. launched a new line of environmentally friendly fracturing fluids.

- 2023 Q3: Baker Hughes Co. and Schlumberger Ltd. announced a joint venture to develop advanced fracturing technologies.

- 2022 Q2: New environmental regulations were implemented in several US states, impacting fluid formulation requirements. (Further specific developments would be detailed in the full report.)

Future Outlook for North America Hydraulic Fracturing Fluids Industry Market

The North American hydraulic fracturing fluids market is poised for continued growth, driven by increasing energy demand, technological advancements, and exploration of new unconventional resources. Strategic opportunities exist for companies focused on developing sustainable and efficient fluid technologies, leveraging data analytics for optimized operations, and expanding into emerging markets. The focus on reducing environmental impact and enhancing operational efficiency will be key to success in the coming years.

North America Hydraulic Fracturing Fluids Industry Segmentation

-

1. Well Type

- 1.1. Horizontal

- 1.2. Vertical

-

2. Fluid Type

- 2.1. Slick Water-based Fluid

- 2.2. Foam-based Fluid

- 2.3. Gelled Oil-based Fluid

- 2.4. Other Base Fluids

-

3. Geography

- 3.1. United States

- 3.2. Canada

- 3.3. Rest of North America

North America Hydraulic Fracturing Fluids Industry Segmentation By Geography

- 1. United States

- 2. Canada

- 3. Rest of North America

North America Hydraulic Fracturing Fluids Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of > 8.50% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. 4.; Presence of Strict Government Regulations to Control Air Pollution

- 3.3. Market Restrains

- 3.3.1. 4.; Increasing Adoption of Renewable Energy

- 3.4. Market Trends

- 3.4.1. Horizontal Wells to Dominate the Market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. North America Hydraulic Fracturing Fluids Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Well Type

- 5.1.1. Horizontal

- 5.1.2. Vertical

- 5.2. Market Analysis, Insights and Forecast - by Fluid Type

- 5.2.1. Slick Water-based Fluid

- 5.2.2. Foam-based Fluid

- 5.2.3. Gelled Oil-based Fluid

- 5.2.4. Other Base Fluids

- 5.3. Market Analysis, Insights and Forecast - by Geography

- 5.3.1. United States

- 5.3.2. Canada

- 5.3.3. Rest of North America

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. United States

- 5.4.2. Canada

- 5.4.3. Rest of North America

- 5.1. Market Analysis, Insights and Forecast - by Well Type

- 6. United States North America Hydraulic Fracturing Fluids Industry Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Well Type

- 6.1.1. Horizontal

- 6.1.2. Vertical

- 6.2. Market Analysis, Insights and Forecast - by Fluid Type

- 6.2.1. Slick Water-based Fluid

- 6.2.2. Foam-based Fluid

- 6.2.3. Gelled Oil-based Fluid

- 6.2.4. Other Base Fluids

- 6.3. Market Analysis, Insights and Forecast - by Geography

- 6.3.1. United States

- 6.3.2. Canada

- 6.3.3. Rest of North America

- 6.1. Market Analysis, Insights and Forecast - by Well Type

- 7. Canada North America Hydraulic Fracturing Fluids Industry Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Well Type

- 7.1.1. Horizontal

- 7.1.2. Vertical

- 7.2. Market Analysis, Insights and Forecast - by Fluid Type

- 7.2.1. Slick Water-based Fluid

- 7.2.2. Foam-based Fluid

- 7.2.3. Gelled Oil-based Fluid

- 7.2.4. Other Base Fluids

- 7.3. Market Analysis, Insights and Forecast - by Geography

- 7.3.1. United States

- 7.3.2. Canada

- 7.3.3. Rest of North America

- 7.1. Market Analysis, Insights and Forecast - by Well Type

- 8. Rest of North America North America Hydraulic Fracturing Fluids Industry Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Well Type

- 8.1.1. Horizontal

- 8.1.2. Vertical

- 8.2. Market Analysis, Insights and Forecast - by Fluid Type

- 8.2.1. Slick Water-based Fluid

- 8.2.2. Foam-based Fluid

- 8.2.3. Gelled Oil-based Fluid

- 8.2.4. Other Base Fluids

- 8.3. Market Analysis, Insights and Forecast - by Geography

- 8.3.1. United States

- 8.3.2. Canada

- 8.3.3. Rest of North America

- 8.1. Market Analysis, Insights and Forecast - by Well Type

- 9. United States North America Hydraulic Fracturing Fluids Industry Analysis, Insights and Forecast, 2019-2031

- 10. Canada North America Hydraulic Fracturing Fluids Industry Analysis, Insights and Forecast, 2019-2031

- 11. Mexico North America Hydraulic Fracturing Fluids Industry Analysis, Insights and Forecast, 2019-2031

- 12. Rest of North America North America Hydraulic Fracturing Fluids Industry Analysis, Insights and Forecast, 2019-2031

- 13. Competitive Analysis

- 13.1. Market Share Analysis 2024

- 13.2. Company Profiles

- 13.2.1 Ashland Inc

- 13.2.1.1. Overview

- 13.2.1.2. Products

- 13.2.1.3. SWOT Analysis

- 13.2.1.4. Recent Developments

- 13.2.1.5. Financials (Based on Availability)

- 13.2.2 Chevron Phillips Chemical Company LLC

- 13.2.2.1. Overview

- 13.2.2.2. Products

- 13.2.2.3. SWOT Analysis

- 13.2.2.4. Recent Developments

- 13.2.2.5. Financials (Based on Availability)

- 13.2.3 Baker Hughes Co

- 13.2.3.1. Overview

- 13.2.3.2. Products

- 13.2.3.3. SWOT Analysis

- 13.2.3.4. Recent Developments

- 13.2.3.5. Financials (Based on Availability)

- 13.2.4 Schlumberger Ltd

- 13.2.4.1. Overview

- 13.2.4.2. Products

- 13.2.4.3. SWOT Analysis

- 13.2.4.4. Recent Developments

- 13.2.4.5. Financials (Based on Availability)

- 13.2.5 BASF SE

- 13.2.5.1. Overview

- 13.2.5.2. Products

- 13.2.5.3. SWOT Analysis

- 13.2.5.4. Recent Developments

- 13.2.5.5. Financials (Based on Availability)

- 13.2.6 DuPont de Nemours Inc *List Not Exhaustive

- 13.2.6.1. Overview

- 13.2.6.2. Products

- 13.2.6.3. SWOT Analysis

- 13.2.6.4. Recent Developments

- 13.2.6.5. Financials (Based on Availability)

- 13.2.7 Halliburton Company

- 13.2.7.1. Overview

- 13.2.7.2. Products

- 13.2.7.3. SWOT Analysis

- 13.2.7.4. Recent Developments

- 13.2.7.5. Financials (Based on Availability)

- 13.2.8 Akzonobel NV

- 13.2.8.1. Overview

- 13.2.8.2. Products

- 13.2.8.3. SWOT Analysis

- 13.2.8.4. Recent Developments

- 13.2.8.5. Financials (Based on Availability)

- 13.2.9 Clariant International Ltd

- 13.2.9.1. Overview

- 13.2.9.2. Products

- 13.2.9.3. SWOT Analysis

- 13.2.9.4. Recent Developments

- 13.2.9.5. Financials (Based on Availability)

- 13.2.10 Calfrac Well Services Ltd

- 13.2.10.1. Overview

- 13.2.10.2. Products

- 13.2.10.3. SWOT Analysis

- 13.2.10.4. Recent Developments

- 13.2.10.5. Financials (Based on Availability)

- 13.2.1 Ashland Inc

List of Figures

- Figure 1: North America Hydraulic Fracturing Fluids Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: North America Hydraulic Fracturing Fluids Industry Share (%) by Company 2024

List of Tables

- Table 1: North America Hydraulic Fracturing Fluids Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: North America Hydraulic Fracturing Fluids Industry Revenue Million Forecast, by Well Type 2019 & 2032

- Table 3: North America Hydraulic Fracturing Fluids Industry Revenue Million Forecast, by Fluid Type 2019 & 2032

- Table 4: North America Hydraulic Fracturing Fluids Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 5: North America Hydraulic Fracturing Fluids Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 6: North America Hydraulic Fracturing Fluids Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 7: United States North America Hydraulic Fracturing Fluids Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Canada North America Hydraulic Fracturing Fluids Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Mexico North America Hydraulic Fracturing Fluids Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Rest of North America North America Hydraulic Fracturing Fluids Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: North America Hydraulic Fracturing Fluids Industry Revenue Million Forecast, by Well Type 2019 & 2032

- Table 12: North America Hydraulic Fracturing Fluids Industry Revenue Million Forecast, by Fluid Type 2019 & 2032

- Table 13: North America Hydraulic Fracturing Fluids Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 14: North America Hydraulic Fracturing Fluids Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 15: North America Hydraulic Fracturing Fluids Industry Revenue Million Forecast, by Well Type 2019 & 2032

- Table 16: North America Hydraulic Fracturing Fluids Industry Revenue Million Forecast, by Fluid Type 2019 & 2032

- Table 17: North America Hydraulic Fracturing Fluids Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 18: North America Hydraulic Fracturing Fluids Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 19: North America Hydraulic Fracturing Fluids Industry Revenue Million Forecast, by Well Type 2019 & 2032

- Table 20: North America Hydraulic Fracturing Fluids Industry Revenue Million Forecast, by Fluid Type 2019 & 2032

- Table 21: North America Hydraulic Fracturing Fluids Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 22: North America Hydraulic Fracturing Fluids Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Hydraulic Fracturing Fluids Industry?

The projected CAGR is approximately > 8.50%.

2. Which companies are prominent players in the North America Hydraulic Fracturing Fluids Industry?

Key companies in the market include Ashland Inc, Chevron Phillips Chemical Company LLC, Baker Hughes Co, Schlumberger Ltd, BASF SE, DuPont de Nemours Inc *List Not Exhaustive, Halliburton Company, Akzonobel NV, Clariant International Ltd, Calfrac Well Services Ltd.

3. What are the main segments of the North America Hydraulic Fracturing Fluids Industry?

The market segments include Well Type, Fluid Type, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

4.; Presence of Strict Government Regulations to Control Air Pollution.

6. What are the notable trends driving market growth?

Horizontal Wells to Dominate the Market.

7. Are there any restraints impacting market growth?

4.; Increasing Adoption of Renewable Energy.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Hydraulic Fracturing Fluids Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Hydraulic Fracturing Fluids Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Hydraulic Fracturing Fluids Industry?

To stay informed about further developments, trends, and reports in the North America Hydraulic Fracturing Fluids Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence