Key Insights

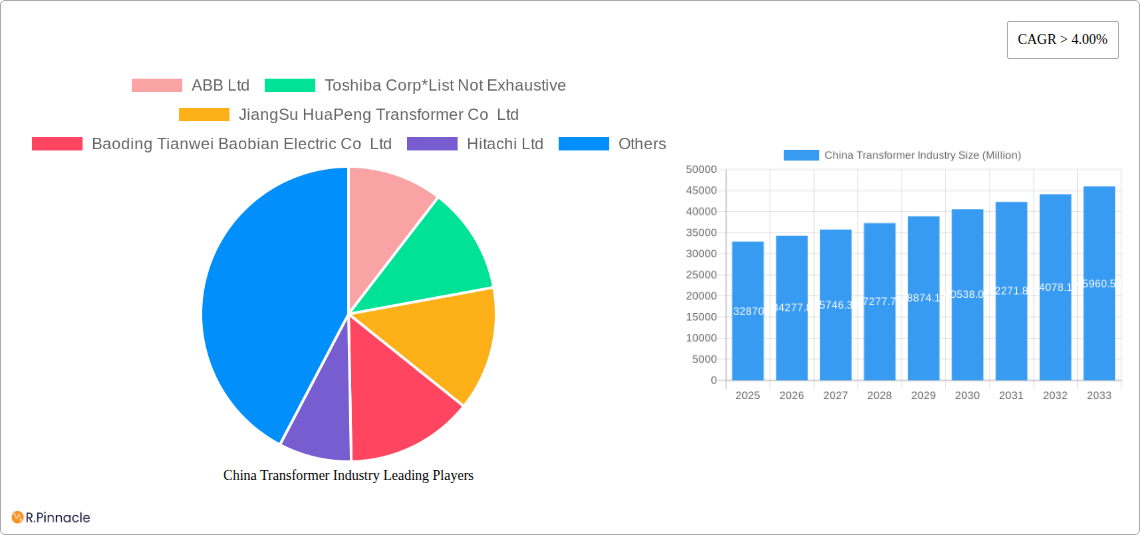

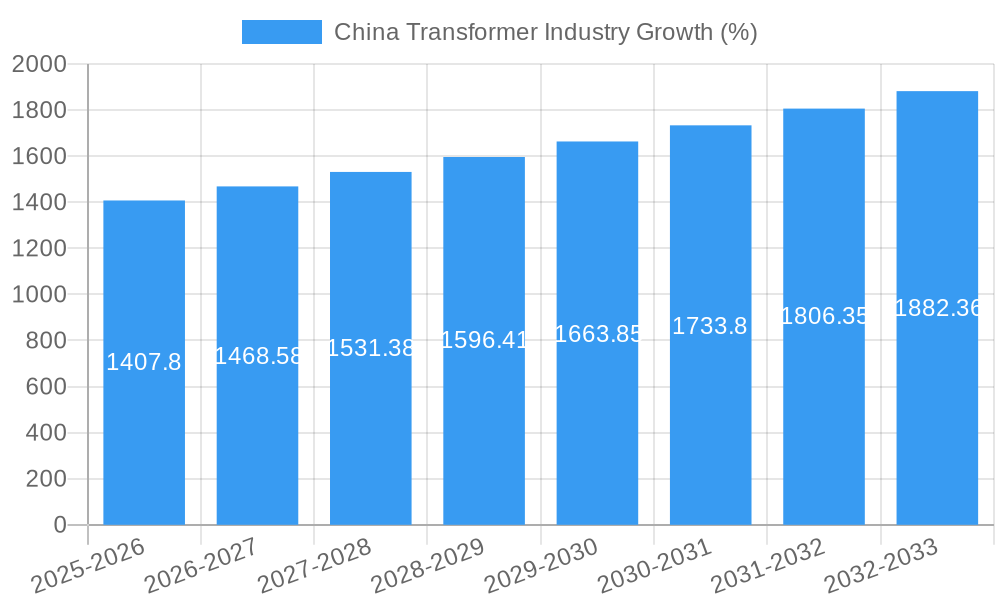

The China transformer industry, valued at $32.87 billion in 2025, is poised for robust growth, exhibiting a Compound Annual Growth Rate (CAGR) exceeding 4.00% from 2025 to 2033. This expansion is fueled by several key drivers. The ongoing modernization of China's power grid infrastructure, including significant investments in renewable energy sources like solar and wind power, necessitates a substantial increase in transformer capacity. Furthermore, rapid urbanization and industrialization continue to boost electricity demand, creating a strong need for efficient and reliable power transformers and distribution transformers across various sectors. Growing adoption of smart grids and the increasing integration of advanced technologies within the energy sector further contribute to the market's positive trajectory. Market segmentation reveals significant demand across power ratings (small, medium, and large), cooling types (air-cooled and oil-cooled), and transformer types (power and distribution transformers). While challenges such as raw material price fluctuations and stringent environmental regulations exist, the overall market outlook remains optimistic due to government support for renewable energy integration and consistent infrastructural development.

The competitive landscape is characterized by a mix of established global players like ABB Ltd, Toshiba Corp, Hitachi Ltd, Siemens AG, and Schneider Electric SE, alongside prominent domestic manufacturers such as Jiangsu HuaPeng Transformer Co Ltd and Baoding Tianwei Baobian Electric Co Ltd. These companies are strategically focusing on technological advancements, enhancing production efficiency, and expanding their distribution networks to cater to the growing demand. The dominance of China in the global transformer manufacturing sector is expected to continue, benefiting from its substantial manufacturing capabilities and cost-effectiveness. However, increased competition, particularly from other Asian economies, necessitates a focus on innovation and differentiation for market leadership. The forecast period (2025-2033) is projected to witness further market consolidation and technological advancements, leading to a more sophisticated and efficient transformer industry in China.

China Transformer Industry Report: 2019-2033

This comprehensive report provides an in-depth analysis of the China transformer industry, offering invaluable insights for industry professionals, investors, and strategic decision-makers. Covering the period 2019-2033, with a focus on 2025, this report leverages rigorous data analysis to forecast market trends and identify lucrative opportunities. The report includes detailed segmentation by power rating, cooling type, and transformer type, examining key players, market dynamics, and future growth prospects.

China Transformer Industry Market Structure & Innovation Trends

The China transformer industry exhibits a moderately concentrated market structure, with several major domestic and international players holding significant market share. ABB Ltd, Toshiba Corp, Jiangsu HuaPeng Transformer Co Ltd, Baoding Tianwei Baobian Electric Co Ltd, Hitachi Ltd, Mitsubishi Electric Corporation, Siemens AG, Schneider Electric SE, General Electric Company, and Panasonic Corporation are among the key players. However, the presence of numerous smaller, regional players contributes to a dynamic competitive landscape. Market share data for 2024 indicates that the top 5 players control approximately xx% of the market, with the remaining share distributed among smaller companies.

Innovation within the industry is driven by government initiatives promoting renewable energy integration and smart grid technologies. Stringent environmental regulations, coupled with increasing demand for energy efficiency, are pushing companies to develop advanced cooling technologies and environmentally friendly materials. Regulatory frameworks, including those related to safety standards and energy efficiency, significantly shape the industry's growth trajectory. The prevalence of M&A activity, with a total deal value exceeding $xx Million in the past five years, reflects consolidation efforts and attempts to gain market share. Product substitutes, such as solid-state transformers, are emerging but haven't significantly impacted the market share of traditional transformers yet. The end-user demographics are diverse, encompassing power generation, transmission, and distribution companies, as well as industrial and commercial consumers.

China Transformer Industry Market Dynamics & Trends

The China transformer industry is experiencing robust growth, driven by large-scale infrastructure projects, rapid urbanization, and increasing electricity demand across various sectors. The market's compound annual growth rate (CAGR) during the historical period (2019-2024) was approximately xx%, and is projected to be xx% during the forecast period (2025-2033). This growth is fueled by government investments in renewable energy sources like solar and wind power, requiring substantial transformer infrastructure upgrades. Technological disruptions are evident in the adoption of digital technologies like smart sensors and advanced control systems, which are enhancing operational efficiency and reliability. Consumer preferences are shifting towards energy-efficient transformers with longer lifespans and reduced maintenance needs. The competitive dynamics are marked by intense competition among both domestic and international players, leading to price pressures and innovation efforts. Market penetration of advanced transformer technologies is gradually increasing, with xx% of new installations utilizing digital features in 2024.

Dominant Regions & Segments in China Transformer Industry

The eastern coastal regions of China, particularly provinces like Guangdong, Jiangsu, and Zhejiang, dominate the transformer market due to high electricity demand and advanced infrastructure development. This dominance is driven by factors such as high population density, robust industrial activity, and supportive government policies.

- Key Drivers for Eastern Coastal Regions:

- Extensive power grid infrastructure development.

- Concentration of manufacturing and industrial activities.

- High electricity consumption rates in urban centers.

- Government initiatives to promote renewable energy integration.

Analyzing segments:

- Power Rating: The large transformer segment holds the largest market share, driven by the needs of large-scale power transmission projects.

- Cooling Type: Oil-cooled transformers dominate the market due to their higher capacity and efficiency in large power applications.

- Transformer Type: Power transformers represent a larger market share compared to distribution transformers due to their role in large-scale power transmission.

The detailed dominance analysis reveals that the large power transformer segment, particularly oil-cooled types, within the eastern coastal region holds the most significant market share.

China Transformer Industry Product Innovations

Recent innovations include the development of high-efficiency transformers with advanced cooling systems, the integration of smart sensors and digital control systems for improved grid management, and the emergence of environmentally friendly materials to reduce the industry's carbon footprint. These innovations improve operational efficiency, reliability, and reduce environmental impact, strengthening their market fit. The integration of digital technologies enhances grid stability and enables predictive maintenance, further bolstering their competitive advantages.

Report Scope & Segmentation Analysis

This report segments the China transformer market based on power rating (small, medium, large), cooling type (air-cooled, oil-cooled), and transformer type (power transformer, distribution transformer). Each segment's growth projections, market sizes for 2025 (in Million USD), and competitive dynamics are analyzed in detail. The large power transformer segment demonstrates the highest growth potential, while oil-cooled transformers are projected to maintain their market dominance due to their superior performance.

Key Drivers of China Transformer Industry Growth

Several factors drive the growth of the China transformer industry. Firstly, substantial government investments in infrastructure projects, including expansion of power grids and renewable energy integration, fuels significant demand. Secondly, the rapid urbanization and industrialization drive increased electricity consumption, creating a need for more robust power transmission and distribution infrastructure. Thirdly, the ongoing adoption of smart grid technologies creates demand for more sophisticated and technologically advanced transformers.

Challenges in the China Transformer Industry Sector

The industry faces several challenges. Stringent environmental regulations require the adoption of environmentally friendly materials and technologies, increasing production costs. Fluctuations in raw material prices and global supply chain disruptions impact production efficiency and profitability. Intense competition, both domestically and internationally, puts downward pressure on prices and margins. The estimated impact of these challenges is a reduction in projected growth by approximately xx% in the next 5 years.

Emerging Opportunities in China Transformer Industry

Emerging opportunities lie in the increasing adoption of renewable energy sources, necessitating efficient energy transmission and distribution solutions. The integration of smart grid technologies opens new avenues for advanced transformer applications. Furthermore, the growth of electric vehicles and data centers creates additional demand for high-capacity and efficient transformers.

Leading Players in the China Transformer Industry Market

- ABB Ltd

- Toshiba Corp

- Jiangsu HuaPeng Transformer Co Ltd

- Baoding Tianwei Baobian Electric Co Ltd

- Hitachi Ltd

- Mitsubishi Electric Corporation

- Siemens AG

- Schneider Electric SE

- General Electric Company

- Panasonic Corporation

Key Developments in China Transformer Industry

November 2022: Successful installation of the first domestically built converter transformer with on-load tap changers in a major west-to-east power transmission project in Guangdong Province. This marked a significant technological advancement in high-end electric equipment manufacturing capabilities within China.

March 2022: The State Grid Corporation of China (SGCC) ordered two 110 kilovolts, 63 megavolt ampere EconiQ™ power transformers from Hitachi Energy for a sustainable substation project in Jiangsu Province, showcasing the increasing adoption of eco-friendly technologies.

Future Outlook for China Transformer Industry Market

The China transformer industry is poised for continued growth, fueled by ongoing infrastructure development, increasing electricity demand, and the expanding adoption of renewable energy sources. Strategic opportunities exist for companies that can leverage technological innovation, enhance efficiency, and adapt to evolving regulatory frameworks. The market's robust growth trajectory is expected to continue, with significant potential for further expansion in the coming years.

China Transformer Industry Segmentation

-

1. Power Rating

- 1.1. Small

- 1.2. Large

- 1.3. Medium

-

2. Cooling Type

- 2.1. Air-Cooled

- 2.2. Oil-Cooled

-

3. Transformer Type

- 3.1. Power Transformer

- 3.2. Distribution Transformer

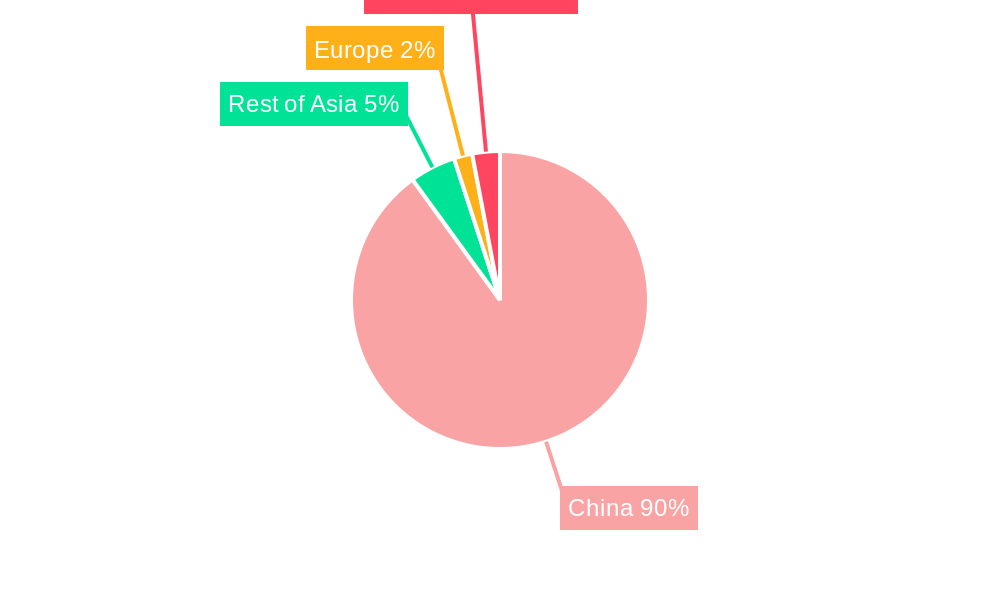

China Transformer Industry Segmentation By Geography

- 1. China

China Transformer Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of > 4.00% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. 4.; Increasing Natural Gas Demand4.; Rising Pipeline Network and Associated Infrastructure Development

- 3.3. Market Restrains

- 3.3.1. 4.; Rising Shift toward Renewable Energy

- 3.4. Market Trends

- 3.4.1. Distribution Transformer Expected to Dominate the Market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. China Transformer Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Power Rating

- 5.1.1. Small

- 5.1.2. Large

- 5.1.3. Medium

- 5.2. Market Analysis, Insights and Forecast - by Cooling Type

- 5.2.1. Air-Cooled

- 5.2.2. Oil-Cooled

- 5.3. Market Analysis, Insights and Forecast - by Transformer Type

- 5.3.1. Power Transformer

- 5.3.2. Distribution Transformer

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. China

- 5.1. Market Analysis, Insights and Forecast - by Power Rating

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2024

- 6.2. Company Profiles

- 6.2.1 ABB Ltd

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 Toshiba Corp*List Not Exhaustive

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 JiangSu HuaPeng Transformer Co Ltd

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Baoding Tianwei Baobian Electric Co Ltd

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 Hitachi Ltd

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 Mitsubishi Electric Corporation

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 Siemens AG

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 Schneider Electric SE

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 General Electric Company

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 Panasonic Corporation

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.1 ABB Ltd

List of Figures

- Figure 1: China Transformer Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: China Transformer Industry Share (%) by Company 2024

List of Tables

- Table 1: China Transformer Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: China Transformer Industry Revenue Million Forecast, by Power Rating 2019 & 2032

- Table 3: China Transformer Industry Revenue Million Forecast, by Cooling Type 2019 & 2032

- Table 4: China Transformer Industry Revenue Million Forecast, by Transformer Type 2019 & 2032

- Table 5: China Transformer Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 6: China Transformer Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 7: China Transformer Industry Revenue Million Forecast, by Power Rating 2019 & 2032

- Table 8: China Transformer Industry Revenue Million Forecast, by Cooling Type 2019 & 2032

- Table 9: China Transformer Industry Revenue Million Forecast, by Transformer Type 2019 & 2032

- Table 10: China Transformer Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the China Transformer Industry?

The projected CAGR is approximately > 4.00%.

2. Which companies are prominent players in the China Transformer Industry?

Key companies in the market include ABB Ltd, Toshiba Corp*List Not Exhaustive, JiangSu HuaPeng Transformer Co Ltd, Baoding Tianwei Baobian Electric Co Ltd, Hitachi Ltd, Mitsubishi Electric Corporation, Siemens AG, Schneider Electric SE, General Electric Company, Panasonic Corporation.

3. What are the main segments of the China Transformer Industry?

The market segments include Power Rating, Cooling Type, Transformer Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 32.87 Million as of 2022.

5. What are some drivers contributing to market growth?

4.; Increasing Natural Gas Demand4.; Rising Pipeline Network and Associated Infrastructure Development.

6. What are the notable trends driving market growth?

Distribution Transformer Expected to Dominate the Market.

7. Are there any restraints impacting market growth?

4.; Rising Shift toward Renewable Energy.

8. Can you provide examples of recent developments in the market?

November 2022: An major west-to-east power transmission project in Guangdong Province, South China, successfully installed the first convertor transformer using on-load tap changers built in China. This signifies that China has successfully overcome the limitations imposed by this key technology in high-end electric equipment.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "China Transformer Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the China Transformer Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the China Transformer Industry?

To stay informed about further developments, trends, and reports in the China Transformer Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence