Key Insights

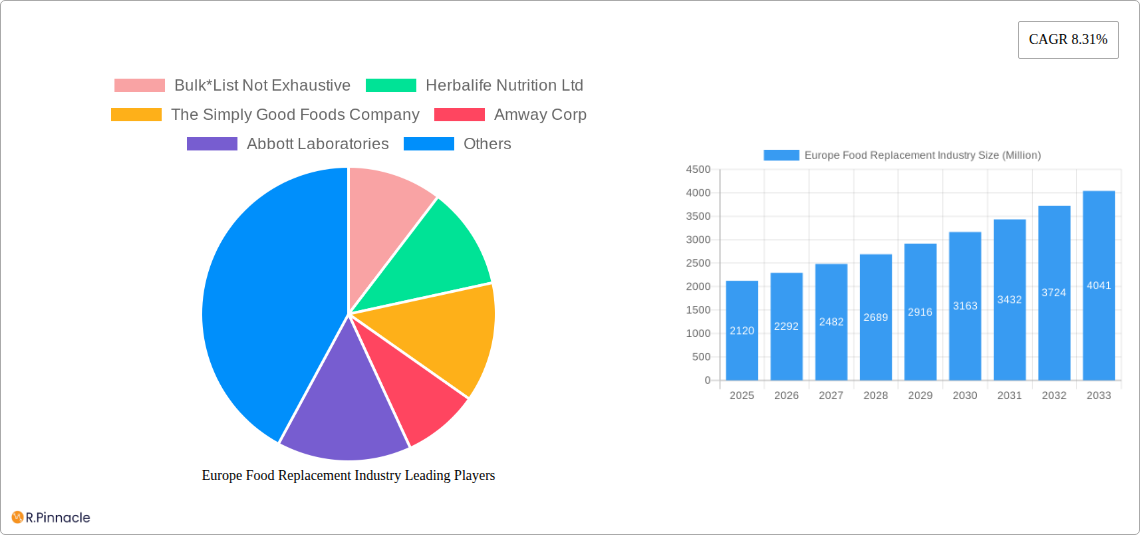

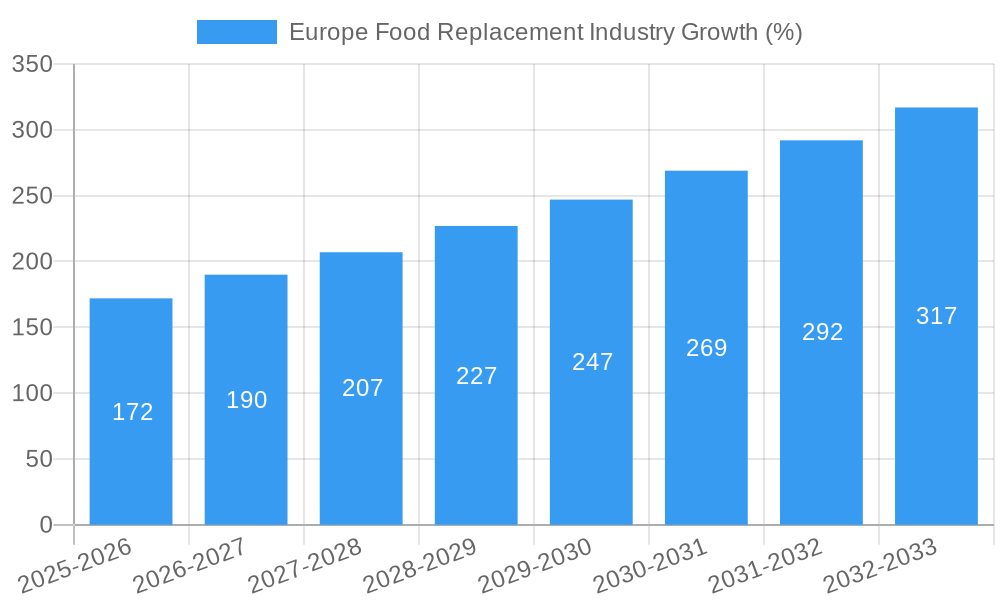

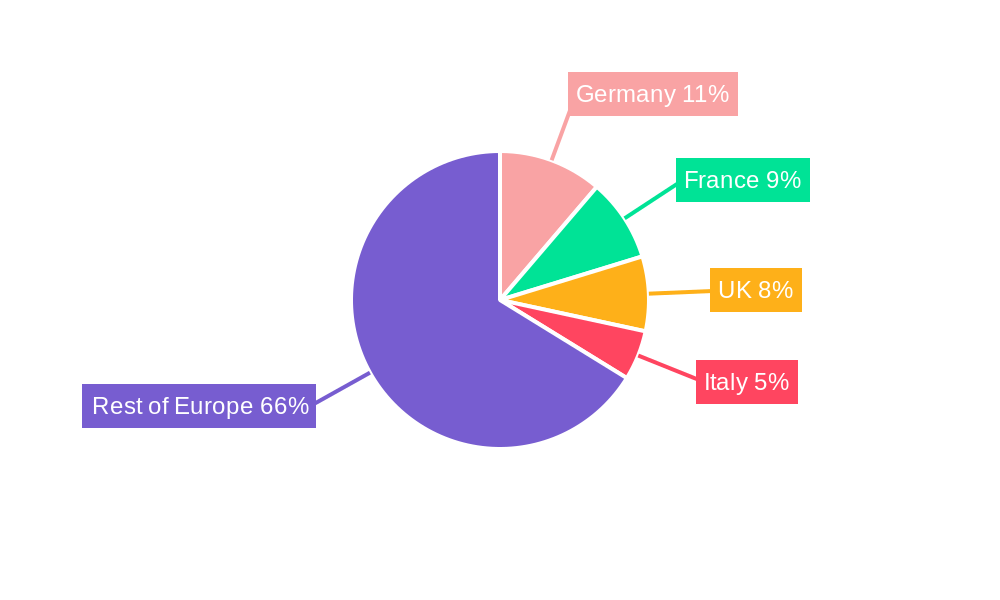

The European food replacement market, valued at €2.12 billion in 2025, is projected to experience robust growth, exhibiting a Compound Annual Growth Rate (CAGR) of 8.31% from 2025 to 2033. This expansion is fueled by several key drivers. The rising prevalence of obesity and related health issues across Europe is prompting increased consumer interest in healthier alternatives to traditional meals. Simultaneously, the growing awareness of the benefits of convenient and nutritious meal options is driving demand, particularly among busy professionals and health-conscious individuals. Furthermore, the increasing adoption of plant-based diets and the growing popularity of personalized nutrition plans are contributing to market growth. Key product segments include ready-to-drink products, nutritional bars, and powdered supplements, with ready-to-drink products holding a significant market share due to their convenience. Distribution channels are diversifying, encompassing supermarkets/hypermarkets, online retail stores, and specialty stores, reflecting evolving consumer preferences and shopping habits. Major players like Herbalife Nutrition, Simply Good Foods, and Nestlé are strategically investing in product innovation and expansion to capture a larger market share. The competitive landscape is dynamic, with both established players and emerging brands vying for consumer attention. Germany, France, and the UK are currently the leading markets within Europe, but other countries are exhibiting increasing growth potential.

The market's growth trajectory is, however, subject to certain restraints. Fluctuations in raw material prices and the potential for regulatory changes related to food labeling and supplement regulations could impact market expansion. Furthermore, consumer perceptions of the long-term health effects of food replacement products and the prevalence of misinformation need to be carefully addressed by industry stakeholders to ensure sustained market growth. To mitigate these challenges, companies are increasingly focusing on transparency in ingredient sourcing, promoting evidence-based health benefits, and actively engaging with consumers to build trust and loyalty. The long-term outlook for the European food replacement market remains positive, driven by ongoing health consciousness and the continued innovation within the industry.

Europe Food Replacement Industry Report: 2019-2033

This comprehensive report provides an in-depth analysis of the Europe food replacement industry, covering market dynamics, key players, and future growth prospects from 2019 to 2033. The study period is 2019-2033, with 2025 as the base and estimated year. The forecast period is 2025-2033, and the historical period is 2019-2024. This report is invaluable for industry professionals, investors, and anyone seeking to understand this rapidly evolving market.

Europe Food Replacement Industry Market Structure & Innovation Trends

The Europe food replacement market exhibits a moderately concentrated structure, with several multinational corporations holding significant market share. Key players like Nestlé S.A., Herbalife Nutrition Ltd., and Glanbia PLC, along with emerging brands like Abnormal and Huel Inc., contribute to a dynamic competitive landscape. Market share data for 2024 indicates Nestlé S.A. holds approximately xx% market share, followed by Herbalife Nutrition Ltd. at xx%, and Glanbia PLC at xx%. The remaining market share is distributed among numerous smaller players.

Innovation is driven by several factors:

- Health and Wellness Trends: Growing consumer awareness of health and nutrition fuels demand for convenient, nutritious meal replacements.

- Technological Advancements: Innovations in food technology, including personalized nutrition and improved taste and texture, enhance product appeal.

- Regulatory Changes: Evolving food safety regulations and labeling requirements influence product formulation and marketing strategies.

- Product Substitutes: Competition from traditional food products and other healthy eating options creates pressure for innovation and differentiation.

- End-User Demographics: The target audience is expanding beyond athletes and weight-conscious individuals, encompassing busy professionals and older adults seeking convenient and nutritious meals.

- M&A Activities: Consolidation in the industry, reflected in recent M&A deals valued at approximately EUR xx Million (cumulative value from 2019-2024), shapes market structure and competitive dynamics.

Europe Food Replacement Industry Market Dynamics & Trends

The Europe food replacement market is experiencing robust growth, driven by several key factors. The market's Compound Annual Growth Rate (CAGR) from 2019 to 2024 was approximately xx%, and projections for 2025-2033 indicate a CAGR of xx%. Market penetration is currently at xx% of the target consumer base and is expected to increase to xx% by 2033.

- Growth Drivers: The rising prevalence of busy lifestyles, increased health consciousness, and growing demand for convenient and nutritious food options are key growth drivers. The shift towards online retail also contributes significantly.

- Technological Disruptions: The adoption of personalized nutrition, advanced food technologies (e.g., 3D food printing), and innovative packaging solutions is reshaping the market.

- Consumer Preferences: Consumers increasingly prioritize natural ingredients, sustainable sourcing, and functional benefits in their meal replacements. This has led to a surge in demand for plant-based and organic options.

- Competitive Dynamics: Intense competition among established players and new entrants fuels product innovation, price adjustments, and strategic partnerships.

Dominant Regions & Segments in Europe Food Replacement Industry

The United Kingdom and Germany are currently the leading markets in Europe, driven by high consumer demand, strong retail infrastructure, and established health and wellness culture. France and Italy are also significant markets, showing potential for future growth.

Leading Segments:

- Product Type: Powdered supplements currently hold the largest market share, followed by ready-to-drink products. Nutritional bars represent a smaller but rapidly growing segment.

- Distribution Channel: Online retail stores are experiencing significant growth, driven by convenience and widespread accessibility. Supermarkets/hypermarkets remain a dominant channel, however.

Key Drivers of Regional Dominance:

- UK: Strong consumer awareness of health and wellness, robust e-commerce infrastructure, and a high density of health-conscious consumers.

- Germany: Significant market size, well-established retail networks, and a focus on functional food products.

- France & Italy: Growing consumer interest in healthy and convenient food options, though the market penetration is relatively lower compared to the UK and Germany.

Europe Food Replacement Industry Product Innovations

Recent innovations focus on enhancing taste, texture, and nutritional profiles of meal replacements. Companies are increasingly incorporating natural and organic ingredients, personalized formulations, and functional benefits (e.g., added probiotics or prebiotics) to cater to specific dietary needs and preferences. This reflects a broader trend toward creating more appealing and effective products that align with evolving consumer demands.

Report Scope & Segmentation Analysis

This report provides a detailed segmentation analysis of the Europe food replacement industry based on product type (ready-to-drink products, nutritional bars, powdered supplements, other product types) and distribution channel (supermarkets/hypermarkets, online retail stores, convenience stores, specialty stores, other distribution channels). Each segment’s growth projections, market sizes, and competitive dynamics are thoroughly examined.

Key Drivers of Europe Food Replacement Industry Growth

Several factors drive the growth of the Europe food replacement industry, including rising health consciousness, busy lifestyles, increasing demand for convenience, and growing technological advancements in personalized nutrition. Favorable government regulations promoting healthy eating habits also contribute to growth. The increasing availability of plant-based and organic options fuels growth further.

Challenges in the Europe Food Replacement Industry Sector

The industry faces challenges including intense competition, stringent regulations, and concerns about the long-term health impacts of relying heavily on meal replacements. Supply chain disruptions and fluctuating raw material prices add to the operational complexities.

Emerging Opportunities in Europe Food Replacement Industry

Emerging opportunities exist in personalized nutrition, innovative product formats (e.g., functional snacks), expansion into new markets (e.g., Eastern Europe), and the development of sustainable and ethically sourced products. Meeting growing consumer demand for tailored and plant-based alternatives presents significant growth potential.

Leading Players in the Europe Food Replacement Industry Market

- Bulk*List Not Exhaustive

- Herbalife Nutrition Ltd

- The Simply Good Foods Company

- Amway Corp

- Abbott Laboratories

- Glanbia PLC

- Abnormal

- Peeroton GmbH

- THG PLC (MyProtein)

- Huel Inc

- USN- Ultimate Sports Nutrition

- Nestlé S A

Key Developments in Europe Food Replacement Industry

- July 2021: Myprotein launched its BeNu meal replacement brand, offering plant-based and non-plant-based options, boosting competition in the ready-to-drink segment.

- February 2021: Abnormal invested EUR 1 Million in a personalized meal replacement service, highlighting the growing trend towards customized nutrition solutions.

- February 2021: Bulk launched its first meal replacement shakes, increasing product variety within the powdered supplement segment.

Future Outlook for Europe Food Replacement Industry Market

The Europe food replacement market is poised for continued growth, driven by evolving consumer preferences and technological advancements. Strategic partnerships, product diversification, and expansion into new markets will be crucial for sustained success. The focus on personalized nutrition, plant-based options, and sustainable practices will shape the industry's future.

Europe Food Replacement Industry Segmentation

-

1. Product Type

- 1.1. Ready-to-Drink Products

- 1.2. Nutritional Bars

- 1.3. Powdered Supplements

- 1.4. Other Product Types

-

2. Distribution Channel

- 2.1. Supermarkets/Hypermarkets

- 2.2. Online Retail Stores

- 2.3. Convenience Stores

- 2.4. Specialty Stores

- 2.5. Other Distribution Channel

Europe Food Replacement Industry Segmentation By Geography

- 1. Spain

- 2. United Kingdom

- 3. Germany

- 4. France

- 5. Italy

- 6. Russia

- 7. Rest of Europe

Europe Food Replacement Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 8.31% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increasing Focus on Maintaining Health and Well-Being; Launching Supplements For Specific Purposes and Targeted Population

- 3.3. Market Restrains

- 3.3.1. Supplement Consumption and Their Side-effects; Inclination Towards Substitute Products

- 3.4. Market Trends

- 3.4.1. Consumers Managing Special Diets Strive on Meal Replacements

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Europe Food Replacement Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. Ready-to-Drink Products

- 5.1.2. Nutritional Bars

- 5.1.3. Powdered Supplements

- 5.1.4. Other Product Types

- 5.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.2.1. Supermarkets/Hypermarkets

- 5.2.2. Online Retail Stores

- 5.2.3. Convenience Stores

- 5.2.4. Specialty Stores

- 5.2.5. Other Distribution Channel

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Spain

- 5.3.2. United Kingdom

- 5.3.3. Germany

- 5.3.4. France

- 5.3.5. Italy

- 5.3.6. Russia

- 5.3.7. Rest of Europe

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. Spain Europe Food Replacement Industry Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 6.1.1. Ready-to-Drink Products

- 6.1.2. Nutritional Bars

- 6.1.3. Powdered Supplements

- 6.1.4. Other Product Types

- 6.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.2.1. Supermarkets/Hypermarkets

- 6.2.2. Online Retail Stores

- 6.2.3. Convenience Stores

- 6.2.4. Specialty Stores

- 6.2.5. Other Distribution Channel

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 7. United Kingdom Europe Food Replacement Industry Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 7.1.1. Ready-to-Drink Products

- 7.1.2. Nutritional Bars

- 7.1.3. Powdered Supplements

- 7.1.4. Other Product Types

- 7.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 7.2.1. Supermarkets/Hypermarkets

- 7.2.2. Online Retail Stores

- 7.2.3. Convenience Stores

- 7.2.4. Specialty Stores

- 7.2.5. Other Distribution Channel

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 8. Germany Europe Food Replacement Industry Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 8.1.1. Ready-to-Drink Products

- 8.1.2. Nutritional Bars

- 8.1.3. Powdered Supplements

- 8.1.4. Other Product Types

- 8.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 8.2.1. Supermarkets/Hypermarkets

- 8.2.2. Online Retail Stores

- 8.2.3. Convenience Stores

- 8.2.4. Specialty Stores

- 8.2.5. Other Distribution Channel

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 9. France Europe Food Replacement Industry Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 9.1.1. Ready-to-Drink Products

- 9.1.2. Nutritional Bars

- 9.1.3. Powdered Supplements

- 9.1.4. Other Product Types

- 9.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 9.2.1. Supermarkets/Hypermarkets

- 9.2.2. Online Retail Stores

- 9.2.3. Convenience Stores

- 9.2.4. Specialty Stores

- 9.2.5. Other Distribution Channel

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 10. Italy Europe Food Replacement Industry Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 10.1.1. Ready-to-Drink Products

- 10.1.2. Nutritional Bars

- 10.1.3. Powdered Supplements

- 10.1.4. Other Product Types

- 10.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 10.2.1. Supermarkets/Hypermarkets

- 10.2.2. Online Retail Stores

- 10.2.3. Convenience Stores

- 10.2.4. Specialty Stores

- 10.2.5. Other Distribution Channel

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 11. Russia Europe Food Replacement Industry Analysis, Insights and Forecast, 2019-2031

- 11.1. Market Analysis, Insights and Forecast - by Product Type

- 11.1.1. Ready-to-Drink Products

- 11.1.2. Nutritional Bars

- 11.1.3. Powdered Supplements

- 11.1.4. Other Product Types

- 11.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 11.2.1. Supermarkets/Hypermarkets

- 11.2.2. Online Retail Stores

- 11.2.3. Convenience Stores

- 11.2.4. Specialty Stores

- 11.2.5. Other Distribution Channel

- 11.1. Market Analysis, Insights and Forecast - by Product Type

- 12. Rest of Europe Europe Food Replacement Industry Analysis, Insights and Forecast, 2019-2031

- 12.1. Market Analysis, Insights and Forecast - by Product Type

- 12.1.1. Ready-to-Drink Products

- 12.1.2. Nutritional Bars

- 12.1.3. Powdered Supplements

- 12.1.4. Other Product Types

- 12.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 12.2.1. Supermarkets/Hypermarkets

- 12.2.2. Online Retail Stores

- 12.2.3. Convenience Stores

- 12.2.4. Specialty Stores

- 12.2.5. Other Distribution Channel

- 12.1. Market Analysis, Insights and Forecast - by Product Type

- 13. Germany Europe Food Replacement Industry Analysis, Insights and Forecast, 2019-2031

- 14. France Europe Food Replacement Industry Analysis, Insights and Forecast, 2019-2031

- 15. Italy Europe Food Replacement Industry Analysis, Insights and Forecast, 2019-2031

- 16. United Kingdom Europe Food Replacement Industry Analysis, Insights and Forecast, 2019-2031

- 17. Netherlands Europe Food Replacement Industry Analysis, Insights and Forecast, 2019-2031

- 18. Sweden Europe Food Replacement Industry Analysis, Insights and Forecast, 2019-2031

- 19. Rest of Europe Europe Food Replacement Industry Analysis, Insights and Forecast, 2019-2031

- 20. Competitive Analysis

- 20.1. Market Share Analysis 2024

- 20.2. Company Profiles

- 20.2.1 Bulk*List Not Exhaustive

- 20.2.1.1. Overview

- 20.2.1.2. Products

- 20.2.1.3. SWOT Analysis

- 20.2.1.4. Recent Developments

- 20.2.1.5. Financials (Based on Availability)

- 20.2.2 Herbalife Nutrition Ltd

- 20.2.2.1. Overview

- 20.2.2.2. Products

- 20.2.2.3. SWOT Analysis

- 20.2.2.4. Recent Developments

- 20.2.2.5. Financials (Based on Availability)

- 20.2.3 The Simply Good Foods Company

- 20.2.3.1. Overview

- 20.2.3.2. Products

- 20.2.3.3. SWOT Analysis

- 20.2.3.4. Recent Developments

- 20.2.3.5. Financials (Based on Availability)

- 20.2.4 Amway Corp

- 20.2.4.1. Overview

- 20.2.4.2. Products

- 20.2.4.3. SWOT Analysis

- 20.2.4.4. Recent Developments

- 20.2.4.5. Financials (Based on Availability)

- 20.2.5 Abbott Laboratories

- 20.2.5.1. Overview

- 20.2.5.2. Products

- 20.2.5.3. SWOT Analysis

- 20.2.5.4. Recent Developments

- 20.2.5.5. Financials (Based on Availability)

- 20.2.6 Glanbia PLC

- 20.2.6.1. Overview

- 20.2.6.2. Products

- 20.2.6.3. SWOT Analysis

- 20.2.6.4. Recent Developments

- 20.2.6.5. Financials (Based on Availability)

- 20.2.7 Abnormal

- 20.2.7.1. Overview

- 20.2.7.2. Products

- 20.2.7.3. SWOT Analysis

- 20.2.7.4. Recent Developments

- 20.2.7.5. Financials (Based on Availability)

- 20.2.8 Peeroton GmbH

- 20.2.8.1. Overview

- 20.2.8.2. Products

- 20.2.8.3. SWOT Analysis

- 20.2.8.4. Recent Developments

- 20.2.8.5. Financials (Based on Availability)

- 20.2.9 THG PLC (MyProtein)

- 20.2.9.1. Overview

- 20.2.9.2. Products

- 20.2.9.3. SWOT Analysis

- 20.2.9.4. Recent Developments

- 20.2.9.5. Financials (Based on Availability)

- 20.2.10 Huel Inc

- 20.2.10.1. Overview

- 20.2.10.2. Products

- 20.2.10.3. SWOT Analysis

- 20.2.10.4. Recent Developments

- 20.2.10.5. Financials (Based on Availability)

- 20.2.11 USN- Ultimate Sports Nutrition

- 20.2.11.1. Overview

- 20.2.11.2. Products

- 20.2.11.3. SWOT Analysis

- 20.2.11.4. Recent Developments

- 20.2.11.5. Financials (Based on Availability)

- 20.2.12 Nestlé S A

- 20.2.12.1. Overview

- 20.2.12.2. Products

- 20.2.12.3. SWOT Analysis

- 20.2.12.4. Recent Developments

- 20.2.12.5. Financials (Based on Availability)

- 20.2.1 Bulk*List Not Exhaustive

List of Figures

- Figure 1: Europe Food Replacement Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Europe Food Replacement Industry Share (%) by Company 2024

List of Tables

- Table 1: Europe Food Replacement Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Europe Food Replacement Industry Revenue Million Forecast, by Product Type 2019 & 2032

- Table 3: Europe Food Replacement Industry Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 4: Europe Food Replacement Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 5: Europe Food Replacement Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 6: Germany Europe Food Replacement Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 7: France Europe Food Replacement Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Italy Europe Food Replacement Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: United Kingdom Europe Food Replacement Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Netherlands Europe Food Replacement Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: Sweden Europe Food Replacement Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: Rest of Europe Europe Food Replacement Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: Europe Food Replacement Industry Revenue Million Forecast, by Product Type 2019 & 2032

- Table 14: Europe Food Replacement Industry Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 15: Europe Food Replacement Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 16: Europe Food Replacement Industry Revenue Million Forecast, by Product Type 2019 & 2032

- Table 17: Europe Food Replacement Industry Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 18: Europe Food Replacement Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 19: Europe Food Replacement Industry Revenue Million Forecast, by Product Type 2019 & 2032

- Table 20: Europe Food Replacement Industry Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 21: Europe Food Replacement Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 22: Europe Food Replacement Industry Revenue Million Forecast, by Product Type 2019 & 2032

- Table 23: Europe Food Replacement Industry Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 24: Europe Food Replacement Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 25: Europe Food Replacement Industry Revenue Million Forecast, by Product Type 2019 & 2032

- Table 26: Europe Food Replacement Industry Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 27: Europe Food Replacement Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 28: Europe Food Replacement Industry Revenue Million Forecast, by Product Type 2019 & 2032

- Table 29: Europe Food Replacement Industry Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 30: Europe Food Replacement Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 31: Europe Food Replacement Industry Revenue Million Forecast, by Product Type 2019 & 2032

- Table 32: Europe Food Replacement Industry Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 33: Europe Food Replacement Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Food Replacement Industry?

The projected CAGR is approximately 8.31%.

2. Which companies are prominent players in the Europe Food Replacement Industry?

Key companies in the market include Bulk*List Not Exhaustive, Herbalife Nutrition Ltd, The Simply Good Foods Company, Amway Corp, Abbott Laboratories, Glanbia PLC, Abnormal, Peeroton GmbH, THG PLC (MyProtein), Huel Inc, USN- Ultimate Sports Nutrition, Nestlé S A.

3. What are the main segments of the Europe Food Replacement Industry?

The market segments include Product Type, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 2.12 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Focus on Maintaining Health and Well-Being; Launching Supplements For Specific Purposes and Targeted Population.

6. What are the notable trends driving market growth?

Consumers Managing Special Diets Strive on Meal Replacements.

7. Are there any restraints impacting market growth?

Supplement Consumption and Their Side-effects; Inclination Towards Substitute Products.

8. Can you provide examples of recent developments in the market?

Jul 2021: Myprotein intended to strengthen its presence in the market with the launch of its meal replacement brand, BeNu. Myprotein's BeNu launched two meal replacement products called "Complete Balanced Nutrition," which differ in their primary ingredients, as one is entirely plant-based and vegan-friendly. BeNu was advertised as having a balance of protein, carbs, fiber, omega-3 and omega-6 fats, as well as all 27 of the essential vitamins and minerals.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Food Replacement Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Food Replacement Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Food Replacement Industry?

To stay informed about further developments, trends, and reports in the Europe Food Replacement Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence