Key Insights

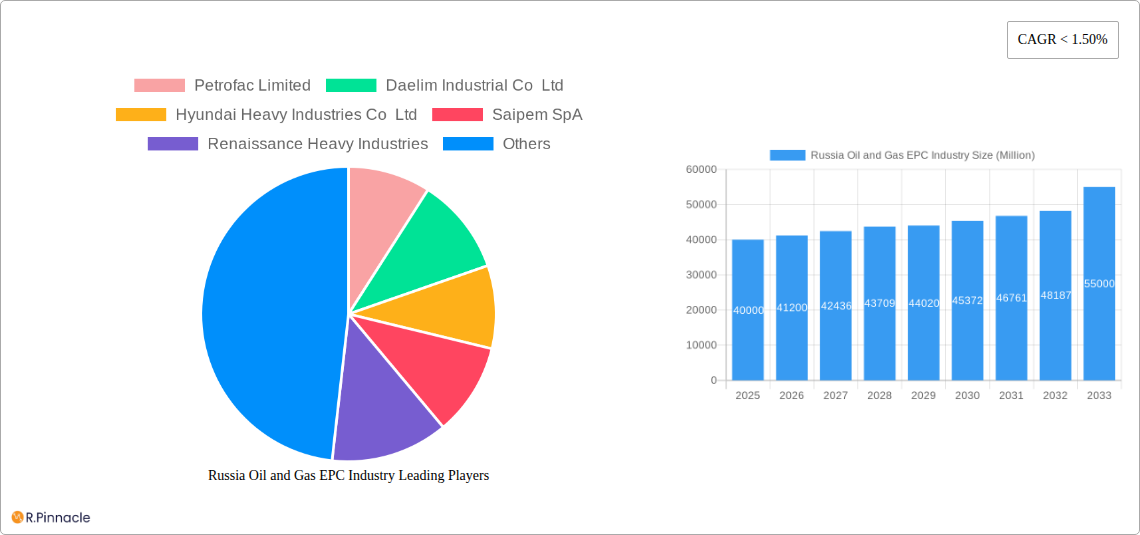

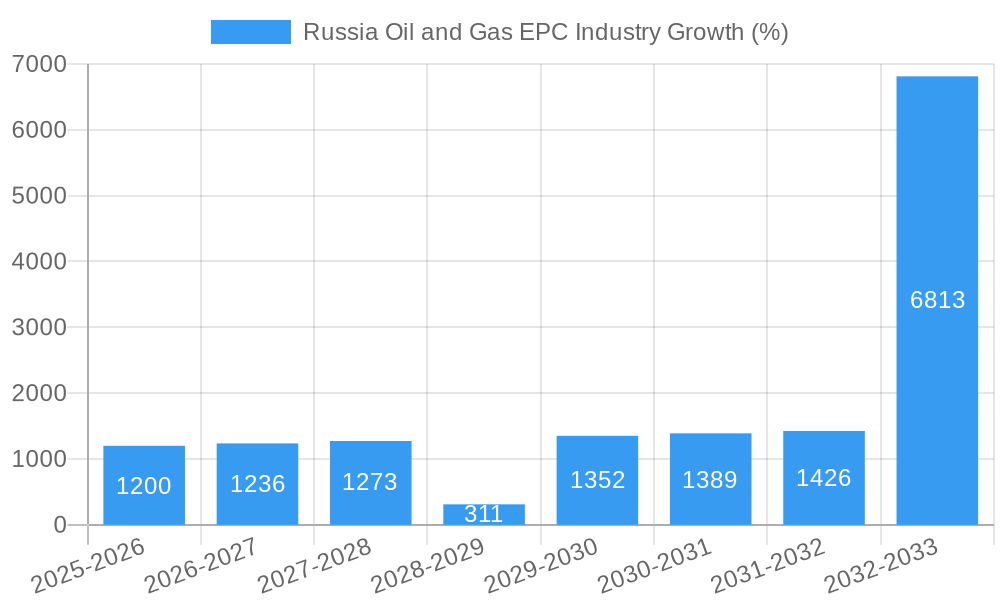

The Russia Oil and Gas EPC (Engineering, Procurement, and Construction) industry, while facing significant geopolitical challenges, presents a complex and evolving market landscape. The period from 2019-2024 witnessed fluctuating growth, largely influenced by global oil prices, sanctions, and domestic policy shifts. While precise figures for market size are unavailable publicly, a reasonable estimate, considering similar global EPC markets and Russia's historical production, suggests a market size of approximately $40 billion USD in 2025. This estimate accounts for decreased activity due to sanctions, but also recognizes ongoing domestic investment in energy infrastructure modernization and potential new projects. The forecast period (2025-2033) is expected to see a moderate Compound Annual Growth Rate (CAGR). Assuming a conservative CAGR of 3%, the market could reach approximately $55 billion USD by 2033. This growth will likely be driven by domestic demand for infrastructure upgrades, though potential sanctions and geopolitical instability remain significant headwinds. Opportunities exist for companies focusing on sustainable energy solutions and those leveraging digital technologies to improve efficiency.

The industry's future hinges on several critical factors. The success of diversification efforts by Russia into new energy sources, the effectiveness of sanctions, and the fluctuating global demand for oil and gas will significantly influence the market's trajectory. The availability of skilled labor and technological advancements also play a considerable role. Despite the uncertainties, the inherent need for energy infrastructure maintenance and potential new projects offers a degree of resilience. Strategic partnerships and a focus on innovation are crucial for players seeking to navigate this complex environment and capitalize on available opportunities within the Russian oil and gas EPC sector.

This comprehensive report provides an in-depth analysis of the Russia Oil & Gas EPC industry, offering valuable insights for industry professionals, investors, and strategic decision-makers. Covering the period from 2019 to 2033, with a focus on 2025, this report unveils market dynamics, key players, and future growth opportunities. Our analysis incorporates data on market size, CAGR, market share, and M&A activities, providing a clear picture of the current landscape and future trajectory of this crucial sector.

Russia Oil and Gas EPC Industry Market Structure & Innovation Trends

The Russian Oil & Gas EPC market exhibits a moderately concentrated structure, with a few major international and domestic players holding significant market share. The market share of the top 5 players is estimated at xx% in 2025, with Petrofac Limited, Saipem SpA, and TechnipFMC PLC amongst the leading global players. Innovation is driven by the need for enhanced efficiency, reduced environmental impact, and the development of new technologies for challenging environments. Regulatory frameworks, while evolving, continue to shape the industry's development, impacting project approvals and investment decisions. Product substitutes, such as renewable energy sources, pose a long-term challenge, although their current market penetration in the oil and gas sector remains limited. End-user demographics are largely defined by state-owned and private oil and gas companies, with large-scale projects dominating the market. M&A activity has been relatively moderate in recent years, with deal values totaling approximately USD xx billion between 2019 and 2024.

- Market Concentration: Top 5 players hold xx% market share (2025 estimate).

- Innovation Drivers: Efficiency gains, environmental concerns, and technological advancements in harsh environments.

- Regulatory Framework: Evolving regulations influence project approvals and investments.

- M&A Activity: Total deal value of approximately USD xx billion (2019-2024).

Russia Oil and Gas EPC Industry Market Dynamics & Trends

The Russian Oil & Gas EPC market is projected to experience a CAGR of xx% during the forecast period (2025-2033). Key growth drivers include increasing domestic oil and gas production, government initiatives supporting infrastructure development, and the ongoing need for modernization of existing facilities. Technological disruptions, such as the adoption of digitalization and automation, are significantly impacting efficiency and project timelines. Consumer preferences are shifting towards environmentally friendly solutions, pushing the industry to adopt more sustainable practices. Competitive dynamics are influenced by global players seeking to expand their presence in the Russian market and the increasing participation of domestic EPC contractors. Market penetration of advanced technologies is steadily growing, with an estimated xx% adoption rate in 2025.

Dominant Regions & Segments in Russia Oil and Gas EPC Industry

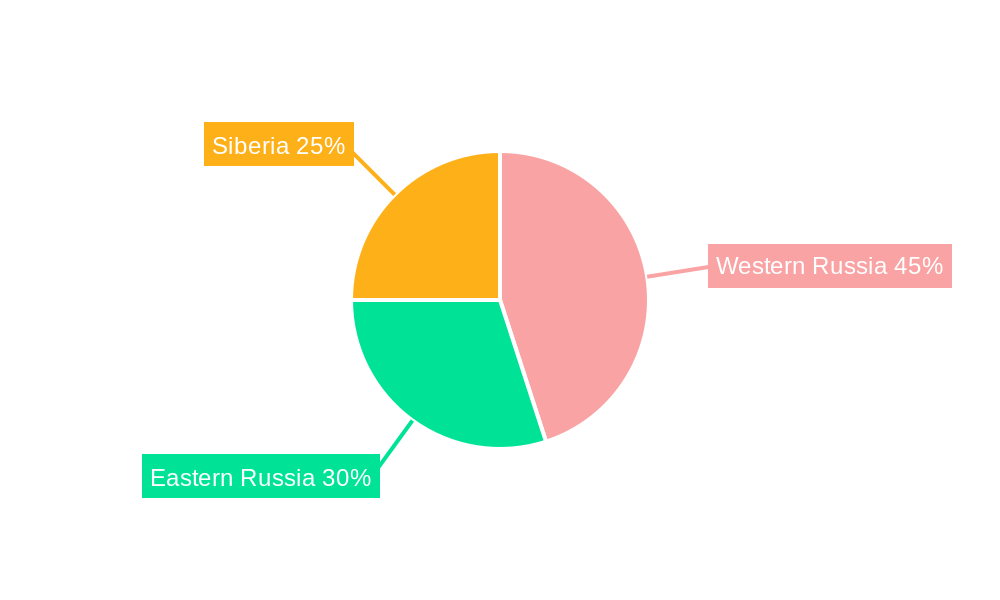

While the entire Russian Federation is significant, specific regions are crucial for oil and gas production and refining activities. Western Siberia, Eastern Siberia, and the Volga region, for example, are vital areas for upstream operations. The downstream sector, focused on refining and petrochemicals, is concentrated near major population centers and ports. The upstream sector, representing approximately xx% of the market in 2025, is dominated by large-scale projects like those in West Siberia. The midstream sector displays comparatively slower growth compared to upstream and downstream.

- Key Drivers: Government policies, investment in infrastructure, and geographical location of resources.

- Upstream Dominance: Driven by large-scale oil and gas field development projects.

- Downstream Focus: Concentrated around major refining hubs and consumer markets.

Russia Oil and Gas EPC Industry Product Innovations

Recent innovations focus on modularization, prefabrication, and the integration of digital technologies to enhance project efficiency and safety. Advanced materials and construction techniques are being employed to withstand challenging environmental conditions. The emphasis is on reducing project timelines and overall costs, while also minimizing environmental impact. These innovations are improving the market fit of EPC services by enhancing speed, efficiency, and sustainability.

Report Scope & Segmentation Analysis

This report segments the Russian Oil & Gas EPC market by sector (Upstream, Midstream, Downstream), application (Oil & gas production, Oil & gas transportation, Oil & gas refining), and geography (Russia, with a focus on key regions, and comparison to the Middle East and Asia-Pacific). Each segment's growth projections, market size, and competitive dynamics are analyzed in detail. The Upstream sector is expected to grow at a faster pace than Midstream and Downstream by xx% CAGR from 2025-2033. The Russian market dominates the geographic segmentation, accounting for xx% in 2025.

Key Drivers of Russia Oil and Gas EPC Industry Growth

Several factors drive the growth of the Russian Oil & Gas EPC industry. Increased domestic oil and gas production targets set by the government fuel demand for EPC services. Significant investments in infrastructure projects, including pipelines and refineries, further stimulate growth. Technological advancements leading to improved efficiency and reduced environmental impact are also key factors. Finally, favorable government policies and incentives aimed at attracting foreign investment play a crucial role.

Challenges in the Russia Oil and Gas EPC Industry Sector

The industry faces challenges such as geopolitical instability impacting investment decisions. Sanctions and export restrictions can disrupt supply chains and project execution. The increasing emphasis on environmental regulations necessitates higher capital expenditure for cleaner technologies and can lead to increased project costs. Furthermore, intense competition from both domestic and international players adds pressure on profit margins. These factors collectively create a complex operating environment.

Emerging Opportunities in Russia Oil and Gas EPC Industry

Opportunities exist in the development of Arctic oil and gas reserves, requiring specialized EPC expertise. The adoption of digital technologies and automation offers scope for efficiency improvements and cost reductions. Furthermore, the growing focus on carbon capture, utilization, and storage (CCUS) presents significant potential for new projects and technological advancements. Government initiatives to promote domestic manufacturing and technology development offer further opportunities for local EPC contractors.

Leading Players in the Russia Oil and Gas EPC Industry Market

- Petrofac Limited

- Daelim Industrial Co Ltd

- Hyundai Heavy Industries Co Ltd

- Saipem SpA

- Renaissance Heavy Industries

- McDermott International Inc

- VELESSTROY

- Assystem SA

- Linde plc

- TechnipFMC PLC

Key Developments in Russia Oil and Gas EPC Industry Industry

- January 2022: DL E&C signed a USD 1.33 billion contract for the Russian Baltic Complex Project, including the construction of a large polymer plant. This signifies significant investment in petrochemical infrastructure.

- January 2022: Maire Tecnimont S.p.A. secured a USD 1.24 billion EPC contract with Rosneft for the VGO Hydrocracking Complex at Ryazan Refining Company, boosting the refining sector.

Future Outlook for Russia Oil and Gas EPC Industry Market

The Russian Oil & Gas EPC market is poised for continued growth, driven by long-term domestic energy demand and ongoing investments in infrastructure development. Technological advancements, particularly in digitalization and sustainability, will shape the industry's future. Strategic partnerships and collaborations will be crucial for navigating challenges and capitalizing on emerging opportunities within this dynamic sector. The market’s growth trajectory will significantly rely on the evolution of geopolitical factors and the government's continued support for the oil and gas industry.

Russia Oil and Gas EPC Industry Segmentation

-

1. Sector

- 1.1. Upstream

- 1.2. Midstream

- 1.3. Downstream

Russia Oil and Gas EPC Industry Segmentation By Geography

- 1. Russia

Russia Oil and Gas EPC Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of < 1.50% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1 4.; Increasing Demand for Crude Oil and Natural Gas4.; Growing Emphasis on Safe

- 3.2.2 Economic

- 3.2.3 and Reliable Connectivity for Oil and Gas Exploration

- 3.3. Market Restrains

- 3.3.1 4.; Technical Challenges Like Construction

- 3.3.2 Deep-Water Challenges

- 3.3.3 and High Construction Costs

- 3.4. Market Trends

- 3.4.1. Midstream Segment to Dominate the Market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Russia Oil and Gas EPC Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Sector

- 5.1.1. Upstream

- 5.1.2. Midstream

- 5.1.3. Downstream

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. Russia

- 5.1. Market Analysis, Insights and Forecast - by Sector

- 6. Western Russia Russia Oil and Gas EPC Industry Analysis, Insights and Forecast, 2019-2031

- 7. Eastern Russia Russia Oil and Gas EPC Industry Analysis, Insights and Forecast, 2019-2031

- 8. Southern Russia Russia Oil and Gas EPC Industry Analysis, Insights and Forecast, 2019-2031

- 9. Northern Russia Russia Oil and Gas EPC Industry Analysis, Insights and Forecast, 2019-2031

- 10. Competitive Analysis

- 10.1. Market Share Analysis 2024

- 10.2. Company Profiles

- 10.2.1 Petrofac Limited

- 10.2.1.1. Overview

- 10.2.1.2. Products

- 10.2.1.3. SWOT Analysis

- 10.2.1.4. Recent Developments

- 10.2.1.5. Financials (Based on Availability)

- 10.2.2 Daelim Industrial Co Ltd

- 10.2.2.1. Overview

- 10.2.2.2. Products

- 10.2.2.3. SWOT Analysis

- 10.2.2.4. Recent Developments

- 10.2.2.5. Financials (Based on Availability)

- 10.2.3 Hyundai Heavy Industries Co Ltd

- 10.2.3.1. Overview

- 10.2.3.2. Products

- 10.2.3.3. SWOT Analysis

- 10.2.3.4. Recent Developments

- 10.2.3.5. Financials (Based on Availability)

- 10.2.4 Saipem SpA

- 10.2.4.1. Overview

- 10.2.4.2. Products

- 10.2.4.3. SWOT Analysis

- 10.2.4.4. Recent Developments

- 10.2.4.5. Financials (Based on Availability)

- 10.2.5 Renaissance Heavy Industries

- 10.2.5.1. Overview

- 10.2.5.2. Products

- 10.2.5.3. SWOT Analysis

- 10.2.5.4. Recent Developments

- 10.2.5.5. Financials (Based on Availability)

- 10.2.6 McDermott International Inc

- 10.2.6.1. Overview

- 10.2.6.2. Products

- 10.2.6.3. SWOT Analysis

- 10.2.6.4. Recent Developments

- 10.2.6.5. Financials (Based on Availability)

- 10.2.7 VELESSTROY

- 10.2.7.1. Overview

- 10.2.7.2. Products

- 10.2.7.3. SWOT Analysis

- 10.2.7.4. Recent Developments

- 10.2.7.5. Financials (Based on Availability)

- 10.2.8 Assystem SA

- 10.2.8.1. Overview

- 10.2.8.2. Products

- 10.2.8.3. SWOT Analysis

- 10.2.8.4. Recent Developments

- 10.2.8.5. Financials (Based on Availability)

- 10.2.9 Linde plc

- 10.2.9.1. Overview

- 10.2.9.2. Products

- 10.2.9.3. SWOT Analysis

- 10.2.9.4. Recent Developments

- 10.2.9.5. Financials (Based on Availability)

- 10.2.10 TechnipFMC PLC

- 10.2.10.1. Overview

- 10.2.10.2. Products

- 10.2.10.3. SWOT Analysis

- 10.2.10.4. Recent Developments

- 10.2.10.5. Financials (Based on Availability)

- 10.2.1 Petrofac Limited

List of Figures

- Figure 1: Russia Oil and Gas EPC Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Russia Oil and Gas EPC Industry Share (%) by Company 2024

List of Tables

- Table 1: Russia Oil and Gas EPC Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Russia Oil and Gas EPC Industry Revenue Million Forecast, by Sector 2019 & 2032

- Table 3: Russia Oil and Gas EPC Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 4: Russia Oil and Gas EPC Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 5: Western Russia Russia Oil and Gas EPC Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 6: Eastern Russia Russia Oil and Gas EPC Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 7: Southern Russia Russia Oil and Gas EPC Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Northern Russia Russia Oil and Gas EPC Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Russia Oil and Gas EPC Industry Revenue Million Forecast, by Sector 2019 & 2032

- Table 10: Russia Oil and Gas EPC Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Russia Oil and Gas EPC Industry?

The projected CAGR is approximately < 1.50%.

2. Which companies are prominent players in the Russia Oil and Gas EPC Industry?

Key companies in the market include Petrofac Limited, Daelim Industrial Co Ltd, Hyundai Heavy Industries Co Ltd, Saipem SpA, Renaissance Heavy Industries, McDermott International Inc, VELESSTROY, Assystem SA, Linde plc, TechnipFMC PLC.

3. What are the main segments of the Russia Oil and Gas EPC Industry?

The market segments include Sector.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

4.; Increasing Demand for Crude Oil and Natural Gas4.; Growing Emphasis on Safe. Economic. and Reliable Connectivity for Oil and Gas Exploration.

6. What are the notable trends driving market growth?

Midstream Segment to Dominate the Market.

7. Are there any restraints impacting market growth?

4.; Technical Challenges Like Construction. Deep-Water Challenges. and High Construction Costs.

8. Can you provide examples of recent developments in the market?

January 2022: an agreement was signed by DL E&C to participate in the Russian Baltic Complex Project. The contract is worth USD 1.33 billion, and DL E&C will be responsible for the project's design and procurement of all equipment. Among the objectives of the project is to construct the largest polymer plant in the world on a single-line basis in Ust-Luga, 110 kilometers southwest of St. Petersburg. Upon completion, the plant will be able to produce 3 million tons of polyethylene, 120,000 tons of butane, and 50,000 tons of hexane each year.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Russia Oil and Gas EPC Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Russia Oil and Gas EPC Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Russia Oil and Gas EPC Industry?

To stay informed about further developments, trends, and reports in the Russia Oil and Gas EPC Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence