Key Insights

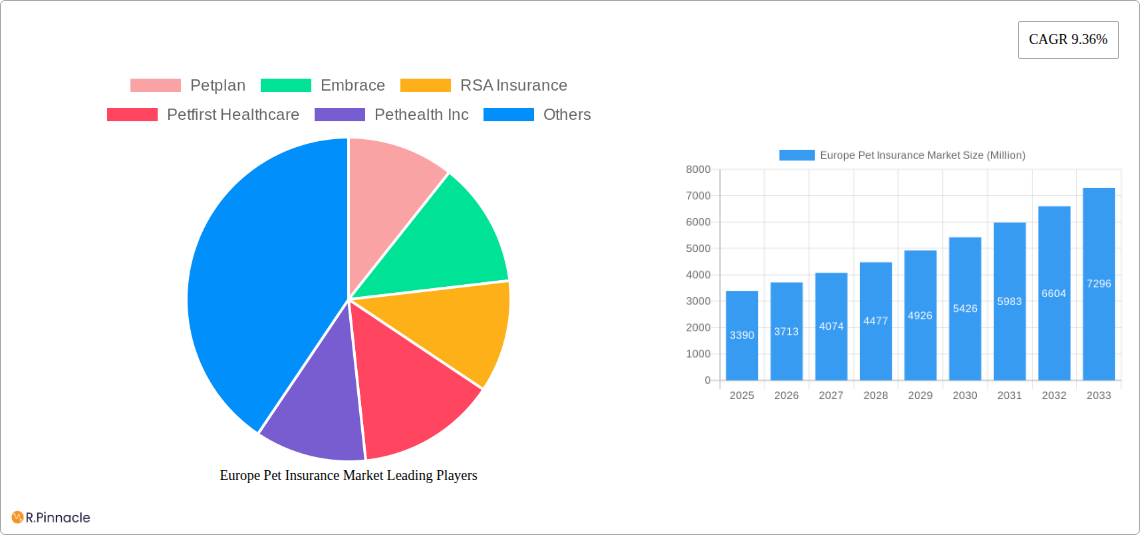

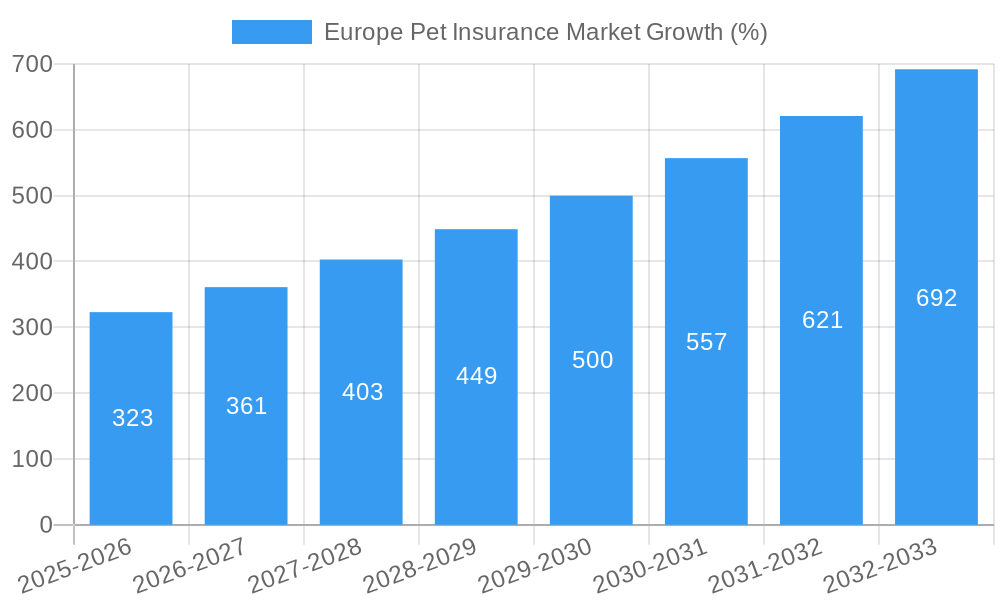

The European pet insurance market, valued at €3.39 billion in 2025, is experiencing robust growth, projected to expand at a compound annual growth rate (CAGR) of 9.36% from 2025 to 2033. This surge is driven by several key factors. Increasing pet ownership across Europe, coupled with rising pet humanization trends, is leading to greater awareness and adoption of pet insurance. Owners are increasingly willing to invest in their pets' healthcare, viewing insurance as a crucial financial safeguard against unexpected veterinary bills. Furthermore, innovative product offerings from insurers, including comprehensive coverage options and flexible payment plans, are contributing to market expansion. The rising prevalence of chronic diseases in pets also fuels demand for insurance, as these conditions often necessitate expensive and ongoing treatment. While regulatory changes and economic fluctuations could pose potential restraints, the overall market outlook remains positive, driven by the strong underlying trends.

The market is segmented by pet type (dogs, cats, others), insurance type (accident-only, comprehensive), and distribution channel (direct, brokers). Key players such as Petplan, Embrace, RSA Insurance, Petfirst Healthcare, Pethealth Inc, Protectapet, AGILA, Petsecure, Hartville Group, and NSM Insurance Group are competing through product differentiation, strategic partnerships, and technological advancements. Geographic variations in pet ownership rates and insurance penetration levels contribute to regional market differences within Europe. The forecast period (2025-2033) suggests continued expansion, driven by increased awareness, improving insurance offerings, and a growing commitment to pet wellbeing across the continent. Further market penetration, particularly in less saturated regions, is expected to contribute significantly to future growth.

Europe Pet Insurance Market Report: 2019-2033

This comprehensive report provides an in-depth analysis of the Europe Pet Insurance Market, offering invaluable insights for industry professionals, investors, and strategic decision-makers. Covering the period from 2019 to 2033, with a focus on 2025, this report unveils the market's structure, dynamics, and future trajectory. The report leverages extensive data analysis and expert insights to deliver actionable intelligence, helping you navigate the complexities of this rapidly evolving market. The market size is projected to reach xx Million by 2033.

Europe Pet Insurance Market Structure & Innovation Trends

This section analyzes the competitive landscape of the European pet insurance market, examining market concentration, innovation drivers, regulatory frameworks, and M&A activities. Key players such as Petplan, Embrace, RSA Insurance, Petfirst Healthcare, Pethealth Inc, Protectapet, AGILA, Petsecure, Hartville Group, and NSM Insurance Group (list not exhaustive) contribute to a dynamic market.

Market Concentration: The market exhibits a moderately concentrated structure, with a few major players holding significant market share. The exact market share distribution requires further in-depth analysis. However, the presence of several smaller, regional players adds complexity.

Innovation Drivers: Technological advancements (telematics, AI-driven risk assessment), increasing pet ownership, and rising pet healthcare costs are key drivers of innovation.

Regulatory Frameworks: Varying regulatory landscapes across European nations influence product offerings and pricing strategies. Further research is needed to analyze the specific regulations across the different countries.

Product Substitutes: Limited direct substitutes exist; however, alternative financial planning for pet healthcare expenses could be considered indirect substitutes.

End-User Demographics: The market is primarily driven by the increasing number of pet owners, particularly in higher-income demographics with a greater willingness to invest in pet insurance.

M&A Activities: Recent acquisitions, like Trupanion's acquisition of PetExpert (November 2022), illustrate the consolidation trend within the market and the estimated values are xx Million. Further analysis is needed to assess overall M&A activity and their respective values.

Europe Pet Insurance Market Dynamics & Trends

This section delves into the market's growth drivers, technological disruptions, consumer preferences, and competitive dynamics. The compound annual growth rate (CAGR) during the forecast period (2025-2033) is estimated to be xx%. Market penetration, particularly in certain regions, remains below xx%, presenting substantial growth potential.

The European pet insurance market is experiencing rapid growth, driven by several key factors: rising pet ownership rates, increasing pet healthcare costs, the growing human-animal bond, and increased awareness of pet insurance benefits. Technological advancements, such as telemedicine and AI-powered risk assessment, are transforming the industry and improving efficiency. Consumer preferences are shifting towards comprehensive coverage and personalized plans, demanding innovative products from insurance providers. The market is characterized by intense competition, with companies continuously striving to differentiate their offerings.

Dominant Regions & Segments in Europe Pet Insurance Market

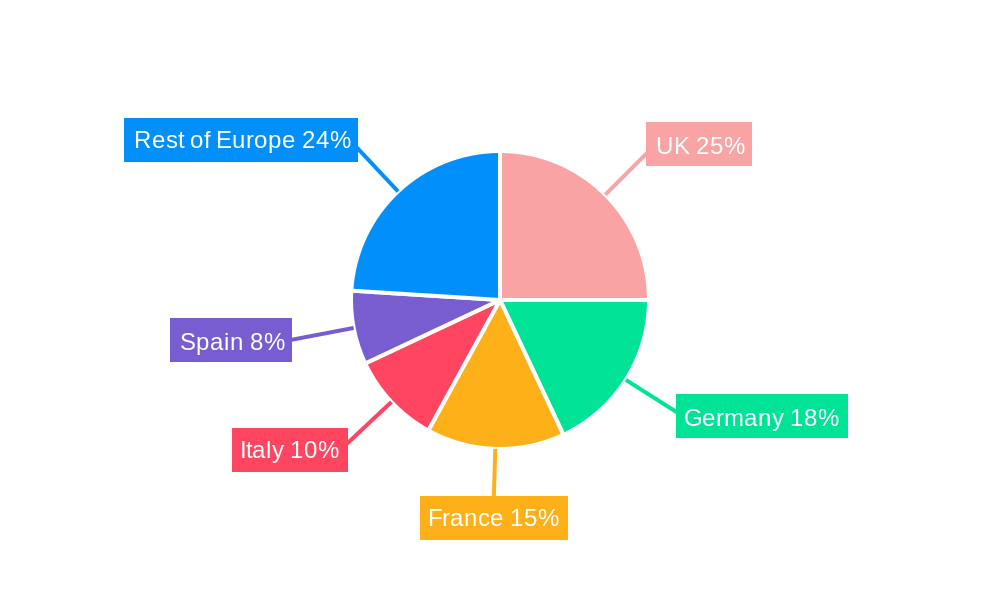

This section identifies the leading regions and segments within the European pet insurance market. The United Kingdom currently holds the largest market share due to factors like high pet ownership, robust pet healthcare infrastructure, and established insurance market. Other countries in Western Europe also display significant growth potential.

- Key Drivers for UK Dominance:

- High pet ownership rates.

- Well-developed veterinary infrastructure.

- Strong consumer awareness of pet insurance.

- Established insurance market with advanced regulatory frameworks.

Germany and France also represent significant markets, although varying pet ownership rates and cultural differences may influence market penetration and growth trajectory. Further analysis will uncover specific regional dominance based on various factors including the economic policies and insurance penetration across different countries.

Europe Pet Insurance Market Product Innovations

The pet insurance market is witnessing significant product innovation, with companies developing increasingly comprehensive plans, such as those including wellness packages and emergency coverage. Technology plays a key role, with digital platforms and mobile apps improving accessibility and customer engagement. The integration of telemedicine options also streamlines claim processes. This trend directly enhances customer satisfaction and increases the competitive advantages of the insurers.

Report Scope & Segmentation Analysis

This report segments the Europe Pet Insurance Market by various factors to deliver a granular understanding of the market dynamics:

By Animal Type: Dogs, Cats, Others (Birds, Reptiles, etc.) Each segment displays unique growth trajectories based on factors such as population, healthcare costs, and consumer behavior. Market sizes for each segment are estimated to be xx Million respectively.

By Coverage Type: Accident-only, Accident & Illness, Wellness. Market dynamics vary across these categories, driven by customer preferences and pricing structures. Each segment is further segmented by different criteria and analyzed.

By Distribution Channel: Online, Offline. The preference for distribution channels differs across customer demographics. Detailed analysis of each segment is included in this report.

Key Drivers of Europe Pet Insurance Market Growth

Several factors are driving the growth of the European pet insurance market. Rising pet ownership, particularly in urban areas and among younger demographics, fuels demand for pet insurance. The increasing cost of veterinary care pushes pet owners to seek financial protection for their beloved companions. Growing awareness of pet insurance benefits, combined with effective marketing strategies by insurance providers, also contribute to market expansion.

Challenges in the Europe Pet Insurance Market Sector

Despite the growth, the sector faces challenges including high claim costs, particularly for older or high-risk pets. Varying regulatory frameworks across European countries pose operational complexities. Maintaining competitive pricing against established players is a continuous challenge. Fraudulent claims also represent a significant problem. Furthermore, increasing competition will require continuous innovation and the establishment of competitive strategies.

Emerging Opportunities in Europe Pet Insurance Market

The market presents several emerging opportunities. Expansion into underserved regions, like Eastern Europe, offers significant potential. Product innovation, particularly in the area of preventative healthcare and wellness plans, will be crucial to cater to evolving consumer preferences. Leveraging technologies such as AI and telemedicine is a key opportunity to streamline operations and optimize customer engagement.

Leading Players in the Europe Pet Insurance Market Market

- Petplan

- Embrace

- RSA Insurance

- Petfirst Healthcare

- Pethealth Inc

- Protectapet

- AGILA

- Petsecure

- Hartville Group

- NSM Insurance Group (List Not Exhaustive)

Key Developments in Europe Pet Insurance Market Industry

- February 2023: Agria Petinsure launches in the Irish market, aiming to increase pet insurance penetration (currently 10-15% for dogs, 5% for cats).

- November 2022: Trupanion acquires Royal Blue s.r.o., parent company of PetExpert, marking its second European acquisition.

Future Outlook for Europe Pet Insurance Market Market

The Europe Pet Insurance Market is poised for continued growth, driven by increasing pet ownership and rising veterinary costs. Innovation in product offerings and leveraging technological advancements are key to capitalizing on future opportunities. The market will likely witness further consolidation through mergers and acquisitions as companies strive to enhance their market share and achieve economies of scale. Expanding into new markets in Eastern Europe and developing tailored insurance plans that cater to specific pet breeds and healthcare needs will become pivotal for future success.

Europe Pet Insurance Market Segmentation

-

1. Insurance Type

- 1.1. Accident & Illness

- 1.2. Accident Only

-

2. Policy Type

- 2.1. Lifetime Coverage

- 2.2. Non-Lifetime Coverage

-

3. Animal Type

- 3.1. Dogs

- 3.2. Cats

- 3.3. Other Animal Types

-

4. Provider

- 4.1. Public

- 4.2. Private

-

5. Distribution Channel

- 5.1. Insurance Agency

- 5.2. Bancassurance

- 5.3. Brokers

- 5.4. Direct Sales

Europe Pet Insurance Market Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Netherlands

- 1.7. Belgium

- 1.8. Sweden

- 1.9. Norway

- 1.10. Poland

- 1.11. Denmark

Europe Pet Insurance Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 9.36% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 3.4.1. Increasing trend of Dog Insurance Premiums in Europe

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Europe Pet Insurance Market Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Insurance Type

- 5.1.1. Accident & Illness

- 5.1.2. Accident Only

- 5.2. Market Analysis, Insights and Forecast - by Policy Type

- 5.2.1. Lifetime Coverage

- 5.2.2. Non-Lifetime Coverage

- 5.3. Market Analysis, Insights and Forecast - by Animal Type

- 5.3.1. Dogs

- 5.3.2. Cats

- 5.3.3. Other Animal Types

- 5.4. Market Analysis, Insights and Forecast - by Provider

- 5.4.1. Public

- 5.4.2. Private

- 5.5. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.5.1. Insurance Agency

- 5.5.2. Bancassurance

- 5.5.3. Brokers

- 5.5.4. Direct Sales

- 5.6. Market Analysis, Insights and Forecast - by Region

- 5.6.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by Insurance Type

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2024

- 6.2. Company Profiles

- 6.2.1 Petplan

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 Embrace

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 RSA Insurance

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Petfirst Healthcare

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 Pethealth Inc

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 Protectapet

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 AGILA

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 Petsecure

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 Hartville Group

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 NSM Insurance Group**List Not Exhaustive

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.1 Petplan

List of Figures

- Figure 1: Europe Pet Insurance Market Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Europe Pet Insurance Market Share (%) by Company 2024

List of Tables

- Table 1: Europe Pet Insurance Market Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Europe Pet Insurance Market Volume Billion Forecast, by Region 2019 & 2032

- Table 3: Europe Pet Insurance Market Revenue Million Forecast, by Insurance Type 2019 & 2032

- Table 4: Europe Pet Insurance Market Volume Billion Forecast, by Insurance Type 2019 & 2032

- Table 5: Europe Pet Insurance Market Revenue Million Forecast, by Policy Type 2019 & 2032

- Table 6: Europe Pet Insurance Market Volume Billion Forecast, by Policy Type 2019 & 2032

- Table 7: Europe Pet Insurance Market Revenue Million Forecast, by Animal Type 2019 & 2032

- Table 8: Europe Pet Insurance Market Volume Billion Forecast, by Animal Type 2019 & 2032

- Table 9: Europe Pet Insurance Market Revenue Million Forecast, by Provider 2019 & 2032

- Table 10: Europe Pet Insurance Market Volume Billion Forecast, by Provider 2019 & 2032

- Table 11: Europe Pet Insurance Market Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 12: Europe Pet Insurance Market Volume Billion Forecast, by Distribution Channel 2019 & 2032

- Table 13: Europe Pet Insurance Market Revenue Million Forecast, by Region 2019 & 2032

- Table 14: Europe Pet Insurance Market Volume Billion Forecast, by Region 2019 & 2032

- Table 15: Europe Pet Insurance Market Revenue Million Forecast, by Insurance Type 2019 & 2032

- Table 16: Europe Pet Insurance Market Volume Billion Forecast, by Insurance Type 2019 & 2032

- Table 17: Europe Pet Insurance Market Revenue Million Forecast, by Policy Type 2019 & 2032

- Table 18: Europe Pet Insurance Market Volume Billion Forecast, by Policy Type 2019 & 2032

- Table 19: Europe Pet Insurance Market Revenue Million Forecast, by Animal Type 2019 & 2032

- Table 20: Europe Pet Insurance Market Volume Billion Forecast, by Animal Type 2019 & 2032

- Table 21: Europe Pet Insurance Market Revenue Million Forecast, by Provider 2019 & 2032

- Table 22: Europe Pet Insurance Market Volume Billion Forecast, by Provider 2019 & 2032

- Table 23: Europe Pet Insurance Market Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 24: Europe Pet Insurance Market Volume Billion Forecast, by Distribution Channel 2019 & 2032

- Table 25: Europe Pet Insurance Market Revenue Million Forecast, by Country 2019 & 2032

- Table 26: Europe Pet Insurance Market Volume Billion Forecast, by Country 2019 & 2032

- Table 27: United Kingdom Europe Pet Insurance Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 28: United Kingdom Europe Pet Insurance Market Volume (Billion) Forecast, by Application 2019 & 2032

- Table 29: Germany Europe Pet Insurance Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 30: Germany Europe Pet Insurance Market Volume (Billion) Forecast, by Application 2019 & 2032

- Table 31: France Europe Pet Insurance Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 32: France Europe Pet Insurance Market Volume (Billion) Forecast, by Application 2019 & 2032

- Table 33: Italy Europe Pet Insurance Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 34: Italy Europe Pet Insurance Market Volume (Billion) Forecast, by Application 2019 & 2032

- Table 35: Spain Europe Pet Insurance Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 36: Spain Europe Pet Insurance Market Volume (Billion) Forecast, by Application 2019 & 2032

- Table 37: Netherlands Europe Pet Insurance Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 38: Netherlands Europe Pet Insurance Market Volume (Billion) Forecast, by Application 2019 & 2032

- Table 39: Belgium Europe Pet Insurance Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 40: Belgium Europe Pet Insurance Market Volume (Billion) Forecast, by Application 2019 & 2032

- Table 41: Sweden Europe Pet Insurance Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 42: Sweden Europe Pet Insurance Market Volume (Billion) Forecast, by Application 2019 & 2032

- Table 43: Norway Europe Pet Insurance Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 44: Norway Europe Pet Insurance Market Volume (Billion) Forecast, by Application 2019 & 2032

- Table 45: Poland Europe Pet Insurance Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 46: Poland Europe Pet Insurance Market Volume (Billion) Forecast, by Application 2019 & 2032

- Table 47: Denmark Europe Pet Insurance Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 48: Denmark Europe Pet Insurance Market Volume (Billion) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Pet Insurance Market?

The projected CAGR is approximately 9.36%.

2. Which companies are prominent players in the Europe Pet Insurance Market?

Key companies in the market include Petplan, Embrace, RSA Insurance, Petfirst Healthcare, Pethealth Inc, Protectapet, AGILA, Petsecure, Hartville Group, NSM Insurance Group**List Not Exhaustive.

3. What are the main segments of the Europe Pet Insurance Market?

The market segments include Insurance Type, Policy Type, Animal Type, Provider, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 3.39 Million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

Increasing trend of Dog Insurance Premiums in Europe.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

February 2023: The new brand Agria Petinsure, formerly Petinsure, is entering the Irish market with a clear mission. Currently, the insurance rate for dogs in the Irish market is approximately 10%-15%, while the rate for cats is approximately 5%. It is estimated that 90% of dogs and 50% of cats in Sweden have pet insurance. Agria Petinsure believes that the same safety should be available for all Irish pets, and pet owners should enjoy peace of mind if their pet needs medical treatment.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in Billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Pet Insurance Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Pet Insurance Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Pet Insurance Market?

To stay informed about further developments, trends, and reports in the Europe Pet Insurance Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence