Key Insights

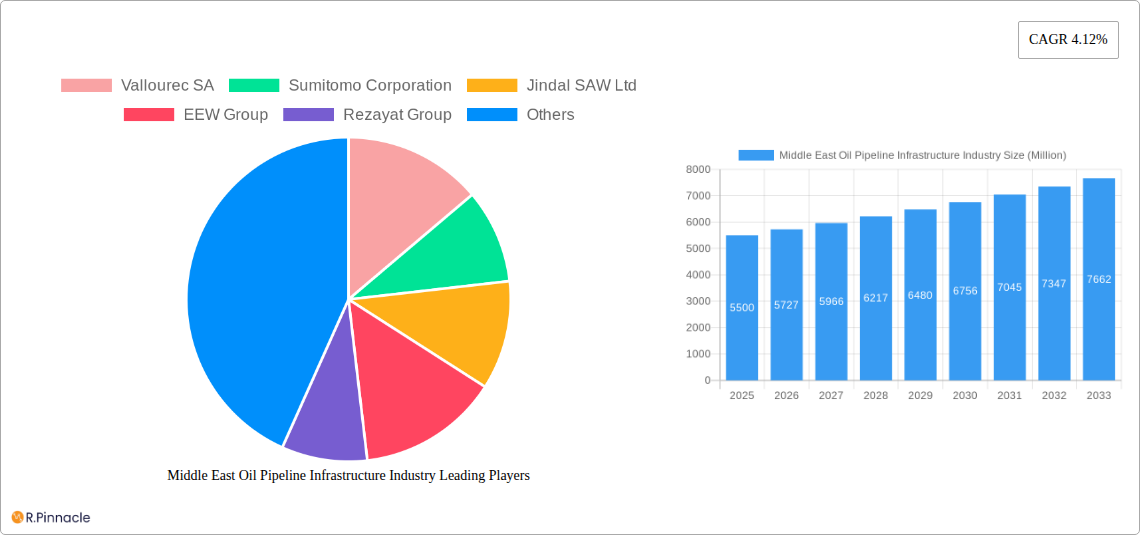

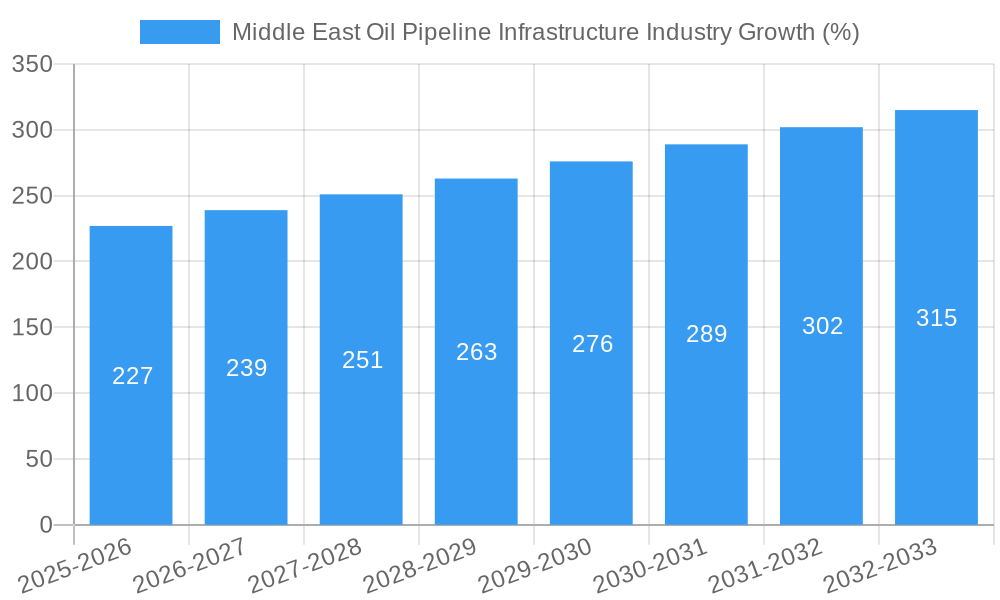

The Middle East Oil Pipeline Infrastructure market, valued at $5.5 billion in 2025, is projected to experience robust growth, driven by increasing oil production and the region's strategic importance in global energy supply. A Compound Annual Growth Rate (CAGR) of 4.12% from 2025 to 2033 indicates a significant expansion of the market, reaching an estimated value of approximately $8.0 billion by 2033. This growth is fueled by several key factors. Firstly, ongoing investments in oil and gas exploration and production within the region necessitate substantial upgrades and expansions to existing pipeline networks to accommodate increased throughput. Secondly, the ongoing geopolitical landscape underscores the need for secure and reliable pipeline infrastructure, driving investment in advanced technologies like smart pipelines and enhanced security measures. Finally, the rising demand for crude oil globally, coupled with the Middle East's role as a major producer, creates a sustained need for robust and efficient pipeline systems. The market is segmented by pipe type, primarily into seamless and welded pipes, with seamless pipes holding a larger market share due to their superior pressure resistance and durability. Major players, including Vallourec SA, Sumitomo Corporation, Jindal SAW Ltd, EEW Group, Rezayat Group, Arabian Pipes Company, and ArcelorMittal SA, are actively engaged in expanding their capacities and developing innovative solutions to cater to this growing demand.

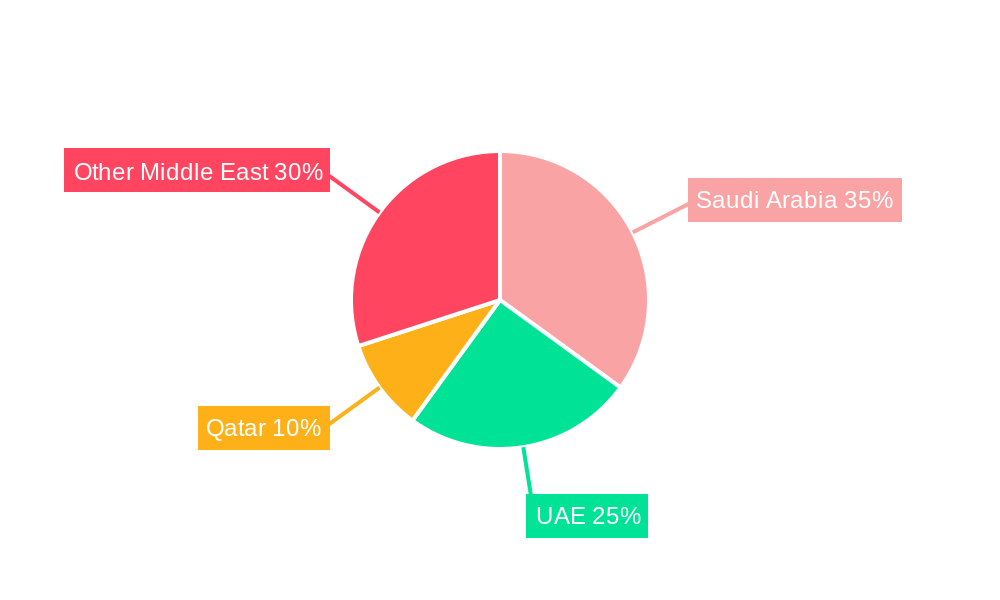

The regional breakdown shows significant contributions from countries like Saudi Arabia, the UAE, and Qatar, reflecting their substantial oil reserves and production capabilities. However, other Middle Eastern nations are also witnessing growth in their pipeline infrastructure due to increasing domestic consumption and regional energy trade. While challenges such as fluctuating oil prices and geopolitical uncertainties exist, the long-term outlook for the Middle East Oil Pipeline Infrastructure market remains positive, driven by consistent investment in energy infrastructure and sustained global demand for oil. This growth will likely see a continued focus on pipeline maintenance, modernization, and capacity expansion to improve efficiency, reliability, and safety within the sector. Technological advancements, including the adoption of digitalization and automation, will also play a crucial role in shaping the market's trajectory.

Middle East Oil Pipeline Infrastructure Industry Report: 2019-2033

This comprehensive report provides an in-depth analysis of the Middle East Oil Pipeline Infrastructure Industry, offering crucial insights for industry professionals, investors, and strategic planners. Covering the period 2019-2033, with a base year of 2025 and a forecast period of 2025-2033, this report meticulously examines market dynamics, technological advancements, and key players shaping the future of this vital sector. The report utilizes data from the historical period (2019-2024) to project future trends, providing a robust and reliable forecast for the coming decade.

Middle East Oil Pipeline Infrastructure Industry Market Structure & Innovation Trends

This section analyzes the competitive landscape of the Middle East oil pipeline infrastructure market, examining market concentration, innovation drivers, regulatory frameworks, and key market activities. The market exhibits a moderately concentrated structure, with a few dominant players commanding significant market share. Estimates indicate that the top five players hold approximately xx% of the overall market share in 2025.

Market Concentration & Key Players:

- High market concentration with a few major players.

- Significant presence of international and regional companies.

- Ongoing consolidation through mergers and acquisitions (M&A).

Innovation Drivers & Regulatory Frameworks:

- Growing demand for efficient and reliable pipeline systems.

- Stringent environmental regulations driving the adoption of advanced technologies.

- Technological advancements in materials science and pipeline construction techniques.

- Government initiatives promoting infrastructure development and energy security.

M&A Activities: The past five years have witnessed significant M&A activity, with deal values exceeding USD xx Million. These activities demonstrate the industry’s consolidation trend and the strategic pursuit of growth and market expansion by major players. Further analysis suggests a continued trend of M&A deals in the forecast period.

Middle East Oil Pipeline Infrastructure Industry Market Dynamics & Trends

The Middle East oil pipeline infrastructure market is experiencing robust growth driven by several factors. The region’s significant oil and gas reserves, coupled with increasing energy demand both domestically and internationally, are primary catalysts for expansion. Technological advancements, such as the adoption of smart pipelines and improved materials, are further enhancing efficiency and reducing operational costs. The market is projected to witness a Compound Annual Growth Rate (CAGR) of xx% during the forecast period (2025-2033), with market penetration expected to reach xx% by 2033. Competitive dynamics are characterized by both intense rivalry among established players and the emergence of new entrants. Consumer preferences are shifting towards sustainable and environmentally friendly solutions, influencing the adoption of advanced technologies and operational practices.

Dominant Regions & Segments in Middle East Oil Pipeline Infrastructure Industry

The Middle East region, encompassing countries like Saudi Arabia, the UAE, and Iraq, dominates the oil pipeline infrastructure market. This dominance is attributed to the region's vast hydrocarbon reserves and strategic geographical location.

Key Drivers of Regional Dominance:

- Vast Oil and Gas Reserves: The Middle East holds a substantial share of the world's proven oil and gas reserves.

- Strategic Geographic Location: The region serves as a crucial transit point for global energy trade.

- Government Support: Significant investments in infrastructure development by regional governments.

- Robust Economic Growth: The expanding economies of the Middle East fuel energy demand.

Segment Analysis: Both seamless and welded pipes are significant segments, with seamless pipes holding a slightly larger market share in 2025 at approximately xx%. The choice between seamless and welded pipes depends on factors like pressure, diameter, and application. Welded pipes are expected to experience faster growth in the coming years due to their cost-effectiveness and suitability for certain applications.

Middle East Oil Pipeline Infrastructure Industry Product Innovations

Recent innovations in the industry focus on enhancing pipeline efficiency, safety, and sustainability. Advanced materials, such as high-strength steel and composite pipes, are being employed to improve durability and reduce maintenance costs. Smart pipeline technologies, incorporating sensors and data analytics, are optimizing operational efficiency and reducing environmental impact. These innovations enhance safety protocols and aid in proactive maintenance, minimizing downtime and ensuring consistent operations.

Report Scope & Segmentation Analysis

This report provides a comprehensive segmentation analysis of the Middle East oil pipeline infrastructure market based on pipe type:

Seamless Pipes: This segment represents a significant portion of the market, driven by its superior strength and reliability in high-pressure applications. The seamless pipes segment is projected to grow at a CAGR of xx% during the forecast period, reaching a market size of USD xx Million by 2033.

Welded Pipes: This segment offers cost-effective solutions for various applications. Driven by technological advancements in welding techniques and material quality, the welded pipes segment is anticipated to grow at a CAGR of xx% during the forecast period, reaching a market size of USD xx Million by 2033. Competitive dynamics are characterized by both price competition and differentiation based on technological advancements and specialized applications.

Key Drivers of Middle East Oil Pipeline Infrastructure Industry Growth

Several factors contribute to the growth of the Middle East oil pipeline infrastructure industry. The region's vast oil and gas reserves, coupled with increasing global energy demand, create a strong foundation for market expansion. Government initiatives promoting infrastructure development and energy security play a significant role in driving investment and growth. Furthermore, technological advancements in pipeline construction, materials, and monitoring systems contribute to increased efficiency, safety, and reliability.

Challenges in the Middle East Oil Pipeline Infrastructure Industry Sector

The industry faces various challenges, including geopolitical instability which can disrupt operations and investment. Supply chain complexities and price volatility in raw materials pose significant risks to project costs and timelines. Stringent environmental regulations require compliance with evolving standards, potentially impacting project feasibility and cost.

Emerging Opportunities in Middle East Oil Pipeline Infrastructure Industry

The industry is witnessing several emerging opportunities. The growing adoption of smart pipeline technologies and the expansion of renewable energy infrastructure offer significant potential for growth. The development of new pipeline projects to support increasing energy demand and the optimization of existing infrastructure through advanced analytics present lucrative opportunities for industry players.

Leading Players in the Middle East Oil Pipeline Infrastructure Industry Market

- Vallourec SA

- Sumitomo Corporation

- Jindal SAW Ltd

- EEW Group

- Rezayat Group

- Arabian Pipes Company

- ArcelorMittal SA

- *List Not Exhaustive

Key Developments in Middle East Oil Pipeline Infrastructure Industry Industry

August 2022: Kazakhstan's redirection of crude oil through Azerbaijan's pipeline signifies a shift in geopolitical dynamics and creates new opportunities for pipeline infrastructure development in the region. This development could lead to increased demand for pipeline capacity and associated services.

March 2023: The USD 13.58 Million EPC contract awarded to Gas Arabian Services Company highlights the ongoing investment in gas pipeline infrastructure in the Middle East. This signifies a growing focus on gas pipeline development, impacting the overall market demand for pipeline materials and services.

Future Outlook for Middle East Oil Pipeline Infrastructure Industry Market

The future of the Middle East oil pipeline infrastructure market appears promising, driven by sustained energy demand, government initiatives, and technological advancements. Strategic investments in pipeline infrastructure, the integration of renewable energy sources, and the adoption of advanced technologies will continue to shape the industry's growth trajectory. The market’s potential for expansion lies in both optimizing existing infrastructure and developing new pipelines to accommodate the region's growing energy needs and facilitate international trade.

Middle East Oil Pipeline Infrastructure Industry Segmentation

-

1. Type

- 1.1. Seamless

- 1.2. Welded

-

2. Geography

- 2.1. United Arab Emirates

- 2.2. Saudi Arabia

- 2.3. Rest of Middle East

Middle East Oil Pipeline Infrastructure Industry Segmentation By Geography

- 1. United Arab Emirates

- 2. Saudi Arabia

- 3. Rest of Middle East

Middle East Oil Pipeline Infrastructure Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 4.12% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. 4.; Proven Shale Gas Reserves 4.; Technological Advancement in Horizontal Drilling and Hydraulic Fracturing

- 3.3. Market Restrains

- 3.3.1. 4.; High Exploration Cost

- 3.4. Market Trends

- 3.4.1. Seamless Type Segment to Witness a Significant Growth

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Middle East Oil Pipeline Infrastructure Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Seamless

- 5.1.2. Welded

- 5.2. Market Analysis, Insights and Forecast - by Geography

- 5.2.1. United Arab Emirates

- 5.2.2. Saudi Arabia

- 5.2.3. Rest of Middle East

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. United Arab Emirates

- 5.3.2. Saudi Arabia

- 5.3.3. Rest of Middle East

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. United Arab Emirates Middle East Oil Pipeline Infrastructure Industry Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Seamless

- 6.1.2. Welded

- 6.2. Market Analysis, Insights and Forecast - by Geography

- 6.2.1. United Arab Emirates

- 6.2.2. Saudi Arabia

- 6.2.3. Rest of Middle East

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Saudi Arabia Middle East Oil Pipeline Infrastructure Industry Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Seamless

- 7.1.2. Welded

- 7.2. Market Analysis, Insights and Forecast - by Geography

- 7.2.1. United Arab Emirates

- 7.2.2. Saudi Arabia

- 7.2.3. Rest of Middle East

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Rest of Middle East Middle East Oil Pipeline Infrastructure Industry Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Seamless

- 8.1.2. Welded

- 8.2. Market Analysis, Insights and Forecast - by Geography

- 8.2.1. United Arab Emirates

- 8.2.2. Saudi Arabia

- 8.2.3. Rest of Middle East

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. United Arab Emirates Middle East Oil Pipeline Infrastructure Industry Analysis, Insights and Forecast, 2019-2031

- 10. Saudi Arabia Middle East Oil Pipeline Infrastructure Industry Analysis, Insights and Forecast, 2019-2031

- 11. Qatar Middle East Oil Pipeline Infrastructure Industry Analysis, Insights and Forecast, 2019-2031

- 12. Israel Middle East Oil Pipeline Infrastructure Industry Analysis, Insights and Forecast, 2019-2031

- 13. Egypt Middle East Oil Pipeline Infrastructure Industry Analysis, Insights and Forecast, 2019-2031

- 14. Oman Middle East Oil Pipeline Infrastructure Industry Analysis, Insights and Forecast, 2019-2031

- 15. Rest of Middle East Middle East Oil Pipeline Infrastructure Industry Analysis, Insights and Forecast, 2019-2031

- 16. Competitive Analysis

- 16.1. Market Share Analysis 2024

- 16.2. Company Profiles

- 16.2.1 Vallourec SA

- 16.2.1.1. Overview

- 16.2.1.2. Products

- 16.2.1.3. SWOT Analysis

- 16.2.1.4. Recent Developments

- 16.2.1.5. Financials (Based on Availability)

- 16.2.2 Sumitomo Corporation

- 16.2.2.1. Overview

- 16.2.2.2. Products

- 16.2.2.3. SWOT Analysis

- 16.2.2.4. Recent Developments

- 16.2.2.5. Financials (Based on Availability)

- 16.2.3 Jindal SAW Ltd

- 16.2.3.1. Overview

- 16.2.3.2. Products

- 16.2.3.3. SWOT Analysis

- 16.2.3.4. Recent Developments

- 16.2.3.5. Financials (Based on Availability)

- 16.2.4 EEW Group

- 16.2.4.1. Overview

- 16.2.4.2. Products

- 16.2.4.3. SWOT Analysis

- 16.2.4.4. Recent Developments

- 16.2.4.5. Financials (Based on Availability)

- 16.2.5 Rezayat Group

- 16.2.5.1. Overview

- 16.2.5.2. Products

- 16.2.5.3. SWOT Analysis

- 16.2.5.4. Recent Developments

- 16.2.5.5. Financials (Based on Availability)

- 16.2.6 Arabian Pipes Company

- 16.2.6.1. Overview

- 16.2.6.2. Products

- 16.2.6.3. SWOT Analysis

- 16.2.6.4. Recent Developments

- 16.2.6.5. Financials (Based on Availability)

- 16.2.7 ArcelorMittal SA*List Not Exhaustive

- 16.2.7.1. Overview

- 16.2.7.2. Products

- 16.2.7.3. SWOT Analysis

- 16.2.7.4. Recent Developments

- 16.2.7.5. Financials (Based on Availability)

- 16.2.1 Vallourec SA

List of Figures

- Figure 1: Middle East Oil Pipeline Infrastructure Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Middle East Oil Pipeline Infrastructure Industry Share (%) by Company 2024

List of Tables

- Table 1: Middle East Oil Pipeline Infrastructure Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Middle East Oil Pipeline Infrastructure Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 3: Middle East Oil Pipeline Infrastructure Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 4: Middle East Oil Pipeline Infrastructure Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 5: Middle East Oil Pipeline Infrastructure Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 6: United Arab Emirates Middle East Oil Pipeline Infrastructure Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 7: Saudi Arabia Middle East Oil Pipeline Infrastructure Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Qatar Middle East Oil Pipeline Infrastructure Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Israel Middle East Oil Pipeline Infrastructure Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Egypt Middle East Oil Pipeline Infrastructure Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: Oman Middle East Oil Pipeline Infrastructure Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: Rest of Middle East Middle East Oil Pipeline Infrastructure Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: Middle East Oil Pipeline Infrastructure Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 14: Middle East Oil Pipeline Infrastructure Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 15: Middle East Oil Pipeline Infrastructure Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 16: Middle East Oil Pipeline Infrastructure Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 17: Middle East Oil Pipeline Infrastructure Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 18: Middle East Oil Pipeline Infrastructure Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 19: Middle East Oil Pipeline Infrastructure Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 20: Middle East Oil Pipeline Infrastructure Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 21: Middle East Oil Pipeline Infrastructure Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Middle East Oil Pipeline Infrastructure Industry?

The projected CAGR is approximately 4.12%.

2. Which companies are prominent players in the Middle East Oil Pipeline Infrastructure Industry?

Key companies in the market include Vallourec SA, Sumitomo Corporation, Jindal SAW Ltd, EEW Group, Rezayat Group, Arabian Pipes Company, ArcelorMittal SA*List Not Exhaustive.

3. What are the main segments of the Middle East Oil Pipeline Infrastructure Industry?

The market segments include Type, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 5.50 Million as of 2022.

5. What are some drivers contributing to market growth?

4.; Proven Shale Gas Reserves 4.; Technological Advancement in Horizontal Drilling and Hydraulic Fracturing.

6. What are the notable trends driving market growth?

Seamless Type Segment to Witness a Significant Growth.

7. Are there any restraints impacting market growth?

4.; High Exploration Cost.

8. Can you provide examples of recent developments in the market?

August 2022: Kazakhstan is expected to sell its crude oil through Azerbaijan's main oil pipeline, as the country seeks alternatives to a route threatened by Russia. Another 3.5 million metric tons of Kazakh crude per year could begin flowing through another Azeri pipeline to Georgia's Black Sea port of Supsa in 2023.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Middle East Oil Pipeline Infrastructure Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Middle East Oil Pipeline Infrastructure Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Middle East Oil Pipeline Infrastructure Industry?

To stay informed about further developments, trends, and reports in the Middle East Oil Pipeline Infrastructure Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence