Key Insights

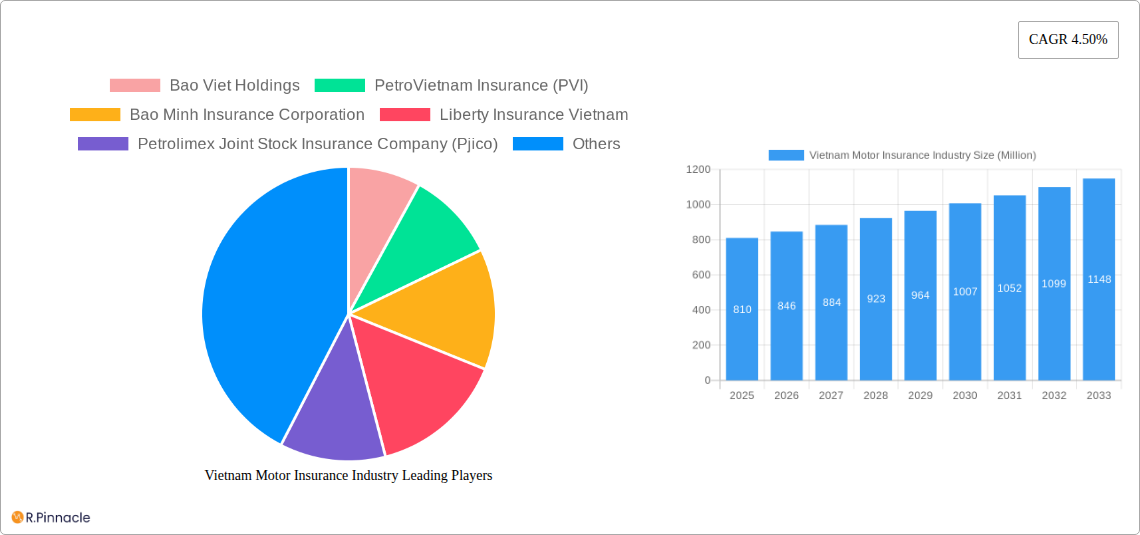

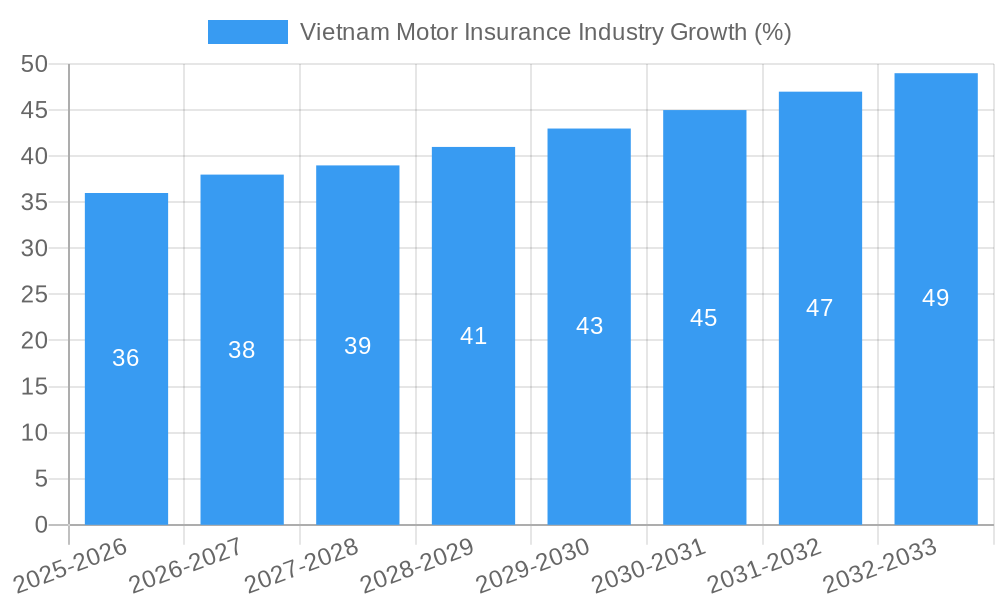

The Vietnam motor insurance market, valued at $810 million in 2025, is projected to experience robust growth, driven by a rising number of vehicles on the road, increasing awareness of insurance benefits, and government regulations promoting compulsory insurance coverage. This expansion is expected to continue at a Compound Annual Growth Rate (CAGR) of 4.5% from 2025 to 2033, reaching an estimated market size of approximately $1.2 billion by 2033. Key market drivers include rising disposable incomes leading to increased vehicle ownership, particularly motorcycles and scooters, a significant portion of the market. Government initiatives to improve road safety and stricter enforcement of insurance regulations are also contributing factors. However, challenges such as a relatively low insurance penetration rate compared to regional peers and the prevalence of uninsured drivers present opportunities for market expansion and increased competition among insurers. The competitive landscape is characterized by a mix of domestic players like Bao Viet Holdings, PetroVietnam Insurance (PVI), and Bao Minh Insurance Corporation, along with international insurers such as Liberty Insurance Vietnam and Fubon Insurance Company. These companies are actively engaging in strategies like product diversification, digitalization, and expanding distribution networks to gain market share. The market segmentation, though not explicitly provided, likely includes categories based on vehicle type (motorcycles, cars, commercial vehicles), coverage type (third-party liability, comprehensive), and customer demographics.

The forecast anticipates a steady increase in market value, driven by continued economic growth and increasing vehicle registrations. Growth may be slightly moderated by potential economic fluctuations and competition. The focus of market players will likely remain on increasing customer awareness and penetration within underserved segments. Innovative products and digital platforms will play a crucial role in attracting younger demographics and expanding the overall market reach. Further expansion is likely to be influenced by government policy regarding insurance mandates and the development of the broader financial services sector in Vietnam.

Vietnam Motor Insurance Industry Report: 2019-2033

Dive deep into the dynamic Vietnam motor insurance market with this comprehensive report, projecting a robust future. This in-depth analysis provides invaluable insights for industry professionals, investors, and strategists seeking to understand and capitalize on the growth opportunities within this rapidly evolving sector. The report covers the period 2019-2033, with a base year of 2025 and a forecast period spanning 2025-2033. Market values are expressed in Millions.

Vietnam Motor Insurance Industry Market Structure & Innovation Trends

This section analyzes the competitive landscape, innovation drivers, and regulatory environment of the Vietnam motor insurance market. We examine market concentration, identifying key players and their respective market shares. The report further explores the impact of mergers and acquisitions (M&A) activities, including deal values where available, on market structure and dynamics. Innovation drivers, such as technological advancements and evolving consumer preferences, are assessed, along with the influence of regulatory frameworks and the presence of product substitutes. End-user demographics and their influence on market segmentation are also detailed.

- Market Concentration: The market is moderately concentrated, with the top 5 players holding approximately xx% of the market share in 2025.

- Top Players (Market Share Estimates for 2025): Bao Viet Holdings (xx%), PetroVietnam Insurance (PVI) (xx%), Bao Minh Insurance Corporation (xx%), Pjico (xx%), Other (xx%).

- M&A Activity: Over the historical period (2019-2024), xx M&A deals were recorded, with a total estimated value of $xx Million. This activity is expected to continue, driven by consolidation and expansion strategies.

- Innovation Drivers: Technological advancements (telematics, AI), increasing demand for add-on services (e.g., roadside assistance), and government initiatives promoting digital insurance are driving innovation.

- Regulatory Framework: The regulatory environment is evolving to promote competition and consumer protection.

Vietnam Motor Insurance Industry Market Dynamics & Trends

This section delves into the key market dynamics driving growth and shaping the competitive landscape in the Vietnam motor insurance sector. We explore the compound annual growth rate (CAGR) and market penetration, highlighting the factors contributing to market expansion. Technological disruptions, shifting consumer preferences, and the competitive dynamics amongst key players are examined, offering a granular perspective on future market trajectories. Detailed analysis covers market size, growth projections, and critical factors influencing market performance.

- CAGR (2025-2033): xx%

- Market Penetration (2025): xx%

- Growth Drivers: Rising vehicle ownership, expanding middle class, increasing awareness of insurance benefits, and government regulations are key drivers.

- Technological Disruptions: The adoption of digital technologies (online platforms, mobile apps, telematics) is transforming the industry, enhancing customer experience and operational efficiency.

- Competitive Dynamics: Intense competition among established players and new entrants is characterized by strategic pricing, product differentiation, and expansion into new segments.

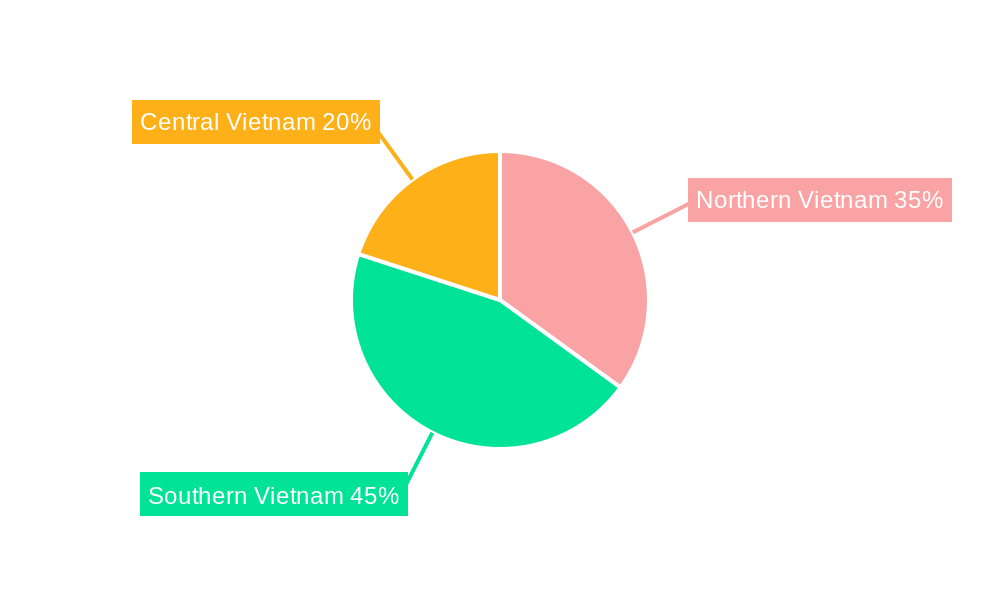

Dominant Regions & Segments in Vietnam Motor Insurance Industry

This section identifies the leading regions and segments within the Vietnamese motor insurance market. We analyze the factors contributing to their dominance, providing a detailed understanding of regional and segment-specific performance. The analysis considers both urban and rural areas, along with variations in consumer behavior and market penetration across diverse geographical regions.

- Dominant Region: Urban areas (e.g., Ho Chi Minh City, Hanoi) account for the largest market share due to higher vehicle density and greater insurance awareness.

- Key Drivers of Regional Dominance:

- Higher vehicle ownership rates

- Increased disposable income

- Better infrastructure and accessibility to insurance services

- Greater awareness of insurance benefits

- Segment Dominance: The private passenger vehicle segment holds the largest market share, followed by commercial vehicles. Motorcycle insurance is also a significant segment.

Vietnam Motor Insurance Industry Product Innovations

This section examines recent product developments, applications, and their competitive advantages. We focus on emerging technological trends and their relevance to market fit. The analysis emphasizes how product innovation is enhancing customer value propositions and driving growth within the sector.

Recent innovations include bundled insurance packages incorporating roadside assistance and telematics-based usage-based insurance (UBI) programs. These offerings are designed to improve customer experience and provide more tailored and cost-effective insurance solutions. The adoption of digital technologies, such as AI-powered claims processing, is also increasing efficiency and reducing operational costs.

Report Scope & Segmentation Analysis

This report provides a comprehensive segmentation analysis of the Vietnam motor insurance industry. It details market size, growth projections, and competitive dynamics across various segments, including geographical regions (urban/rural), vehicle type (passenger cars, commercial vehicles, motorcycles), and insurance type (third-party liability, comprehensive).

- Geographical Segmentation: The report analyzes market performance in key regions across Vietnam, highlighting regional variations in growth rates and market size.

- Vehicle Type Segmentation: Separate market analysis for passenger cars, commercial vehicles, and motorcycles, outlining specific market trends and challenges for each segment.

- Insurance Type Segmentation: Detailed analysis of the third-party liability and comprehensive insurance segments, along with comparisons of their growth trajectory and market share.

Key Drivers of Vietnam Motor Insurance Industry Growth

The growth of Vietnam's motor insurance industry is propelled by a combination of economic, technological, and regulatory factors. The rising number of vehicles, increased disposable income, and improved infrastructure play a crucial role. Government regulations promoting insurance penetration further fuel growth, along with technological advancements improving customer access and operational efficiency.

Challenges in the Vietnam Motor Insurance Industry Sector

The Vietnam motor insurance industry faces several challenges, including limited insurance penetration in certain regions, fraud, and the need to strengthen regulatory oversight. These factors hinder market growth and require effective mitigation strategies from both insurers and regulatory bodies. The lack of trust in certain areas and the underdevelopment of insurance infrastructure in certain regions present significant barriers. Competition is another major challenge impacting profitability.

Emerging Opportunities in Vietnam Motor Insurance Industry

The Vietnamese motor insurance sector presents several promising opportunities. Growing vehicle ownership, especially in rural areas, offers significant expansion potential. Leveraging technology to enhance customer experience, streamline operations, and develop innovative products (e.g., usage-based insurance) represents another substantial opportunity. The expansion of the middle class and its increasing disposable income also creates more opportunities for penetration.

Leading Players in the Vietnam Motor Insurance Industry Market

- Bao Viet Holdings

- PetroVietnam Insurance (PVI)

- Bao Minh Insurance Corporation

- Liberty Insurance Vietnam

- Petrolimex Joint Stock Insurance Company (Pjico)

- AAA Assurance Corporation

- BIDV Insurance Corporation

- Fubon Insurance Company

- Phu Hung Assurance Corporation

- Samsung Vina Insurance Company

Key Developments in Vietnam Motor Insurance Industry

- November 2023: Vietnam joined the ASEAN Compulsory Motor Insurance Scheme (ACMI), mandating third-party liability insurance for vehicles traveling within ASEAN. This development is expected to significantly increase demand for motor insurance and create new business opportunities.

- December 2023: Cathay Insurance Vietnam launched a "Dual Finance" initiative with SAWAD, offering customers financial assistance alongside mandatory insurance. The launch of a personal injury insurance scheme further expands their product offerings.

Future Outlook for Vietnam Motor Insurance Industry Market

The Vietnam motor insurance market is poised for strong growth in the coming years, driven by increasing vehicle ownership, rising disposable incomes, and ongoing economic development. The government's support for insurance penetration and technological advancements will further propel market expansion. Strategic partnerships and product innovation will be key success factors for players in this dynamic market.

Vietnam Motor Insurance Industry Segmentation

-

1. Policy Type

- 1.1. Compulsory Third-Party Liability Insurance (CTPL)

- 1.2. Comprehensive Insurance

-

2. Vehicle Type

- 2.1. Passenger Vehicles

- 2.2. Commercial Vehicles

-

3. Distribution Channel

- 3.1. Agents

- 3.2. Brokers

- 3.3. Banks

- 3.4. Online

- 3.5. Other Distribution Channels

Vietnam Motor Insurance Industry Segmentation By Geography

- 1. Vietnam

Vietnam Motor Insurance Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 4.50% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increasing Vehicle Ownership; Mandatory Motor Insurance Rules by Government

- 3.3. Market Restrains

- 3.3.1. Increasing Vehicle Ownership; Mandatory Motor Insurance Rules by Government

- 3.4. Market Trends

- 3.4.1. Surge in Vehicle Ownership Generating Major Demand in the Market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Vietnam Motor Insurance Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Policy Type

- 5.1.1. Compulsory Third-Party Liability Insurance (CTPL)

- 5.1.2. Comprehensive Insurance

- 5.2. Market Analysis, Insights and Forecast - by Vehicle Type

- 5.2.1. Passenger Vehicles

- 5.2.2. Commercial Vehicles

- 5.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.3.1. Agents

- 5.3.2. Brokers

- 5.3.3. Banks

- 5.3.4. Online

- 5.3.5. Other Distribution Channels

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Vietnam

- 5.1. Market Analysis, Insights and Forecast - by Policy Type

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2024

- 6.2. Company Profiles

- 6.2.1 Bao Viet Holdings

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 PetroVietnam Insurance (PVI)

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 Bao Minh Insurance Corporation

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Liberty Insurance Vietnam

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 Petrolimex Joint Stock Insurance Company (Pjico)

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 AAA Assurance Corporation

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 BIDV Insurance Corporation

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 Fubon Insurance Company

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 Phu Hung Assurance Corporation

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 Samsung Vina Insurance Company**List Not Exhaustive

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.1 Bao Viet Holdings

List of Figures

- Figure 1: Vietnam Motor Insurance Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Vietnam Motor Insurance Industry Share (%) by Company 2024

List of Tables

- Table 1: Vietnam Motor Insurance Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Vietnam Motor Insurance Industry Volume Billion Forecast, by Region 2019 & 2032

- Table 3: Vietnam Motor Insurance Industry Revenue Million Forecast, by Policy Type 2019 & 2032

- Table 4: Vietnam Motor Insurance Industry Volume Billion Forecast, by Policy Type 2019 & 2032

- Table 5: Vietnam Motor Insurance Industry Revenue Million Forecast, by Vehicle Type 2019 & 2032

- Table 6: Vietnam Motor Insurance Industry Volume Billion Forecast, by Vehicle Type 2019 & 2032

- Table 7: Vietnam Motor Insurance Industry Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 8: Vietnam Motor Insurance Industry Volume Billion Forecast, by Distribution Channel 2019 & 2032

- Table 9: Vietnam Motor Insurance Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 10: Vietnam Motor Insurance Industry Volume Billion Forecast, by Region 2019 & 2032

- Table 11: Vietnam Motor Insurance Industry Revenue Million Forecast, by Policy Type 2019 & 2032

- Table 12: Vietnam Motor Insurance Industry Volume Billion Forecast, by Policy Type 2019 & 2032

- Table 13: Vietnam Motor Insurance Industry Revenue Million Forecast, by Vehicle Type 2019 & 2032

- Table 14: Vietnam Motor Insurance Industry Volume Billion Forecast, by Vehicle Type 2019 & 2032

- Table 15: Vietnam Motor Insurance Industry Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 16: Vietnam Motor Insurance Industry Volume Billion Forecast, by Distribution Channel 2019 & 2032

- Table 17: Vietnam Motor Insurance Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 18: Vietnam Motor Insurance Industry Volume Billion Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Vietnam Motor Insurance Industry?

The projected CAGR is approximately 4.50%.

2. Which companies are prominent players in the Vietnam Motor Insurance Industry?

Key companies in the market include Bao Viet Holdings, PetroVietnam Insurance (PVI), Bao Minh Insurance Corporation, Liberty Insurance Vietnam, Petrolimex Joint Stock Insurance Company (Pjico), AAA Assurance Corporation, BIDV Insurance Corporation, Fubon Insurance Company, Phu Hung Assurance Corporation, Samsung Vina Insurance Company**List Not Exhaustive.

3. What are the main segments of the Vietnam Motor Insurance Industry?

The market segments include Policy Type, Vehicle Type, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 0.81 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Vehicle Ownership; Mandatory Motor Insurance Rules by Government.

6. What are the notable trends driving market growth?

Surge in Vehicle Ownership Generating Major Demand in the Market.

7. Are there any restraints impacting market growth?

Increasing Vehicle Ownership; Mandatory Motor Insurance Rules by Government.

8. Can you provide examples of recent developments in the market?

December 2023: Cathay Insurance Vietnam joined hands with SAWAD to unveil an all-inclusive "Dual Finance" initiative. This program empowers customers to seek financial assistance while securing mandatory insurance coverage seamlessly. To cater to its clientele's diverse needs, Cathay has set to roll out a personal injury insurance scheme in December, complementing its existing financial support and automobile insurance offerings.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in Billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Vietnam Motor Insurance Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Vietnam Motor Insurance Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Vietnam Motor Insurance Industry?

To stay informed about further developments, trends, and reports in the Vietnam Motor Insurance Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence