Key Insights

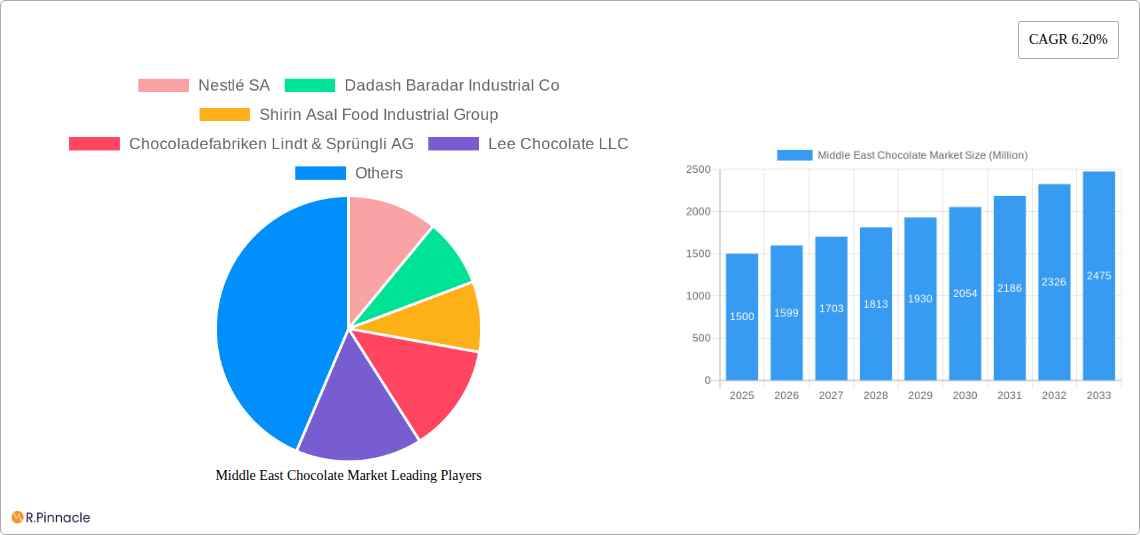

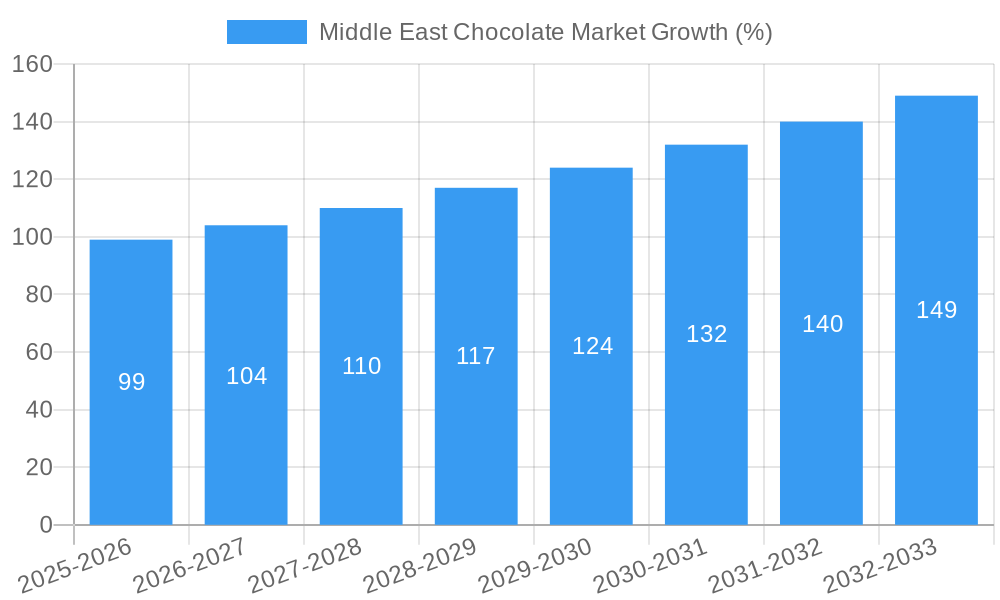

The Middle East chocolate market, valued at approximately $XX million in 2025, is projected to experience robust growth, exhibiting a Compound Annual Growth Rate (CAGR) of 6.20% from 2025 to 2033. This expansion is fueled by several key drivers. Rising disposable incomes across the region, particularly in the UAE and Saudi Arabia, are leading to increased spending on premium confectionery items, including chocolate. A burgeoning young population with a penchant for Westernized lifestyles and indulgent treats further contributes to market growth. The increasing popularity of online retail channels provides convenient access to a wider variety of chocolate products, boosting sales. Furthermore, the presence of established international players like Nestlé and Mars, alongside local brands catering to specific regional preferences, creates a dynamic and competitive landscape. However, fluctuations in commodity prices (cocoa, sugar) and potential health concerns regarding high sugar and fat content pose challenges to sustained growth. Segmentation analysis reveals strong demand for dark chocolate, reflecting a growing health-conscious segment, while supermarkets/hypermarkets remain the dominant distribution channel, although online sales are steadily increasing.

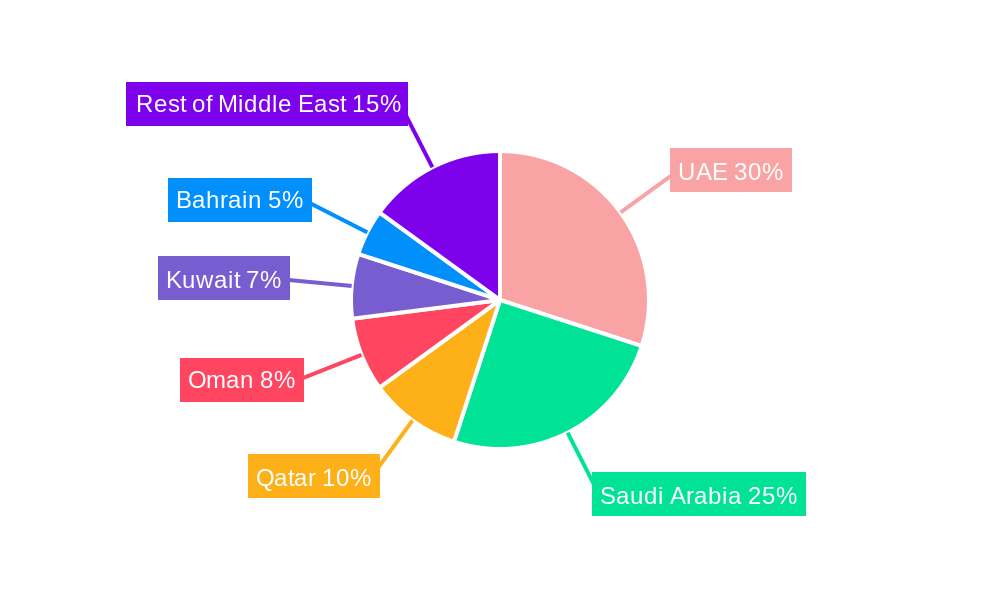

The market's segmentation highlights key opportunities. The preference for dark chocolate suggests a growing health-conscious consumer base that companies can target with innovative product offerings. While supermarkets and hypermarkets are major distribution points, there's substantial growth potential in leveraging the convenience store and online channels to reach broader consumer segments. Geographical analysis reveals significant market concentration in the UAE and Saudi Arabia due to their higher purchasing power and population density. However, other countries within the region present untapped opportunities, offering future growth potential. Strategic marketing campaigns focused on targeting specific demographics, leveraging cultural preferences, and emphasizing product quality and health benefits will be crucial for companies to succeed in this expanding market.

Middle East Chocolate Market Report: 2019-2033

This comprehensive report provides an in-depth analysis of the Middle East chocolate market, offering invaluable insights for industry professionals, investors, and stakeholders. Covering the period from 2019 to 2033, with a focus on 2025, this report examines market dynamics, leading players, and future growth opportunities across various segments and countries within the Middle East. The market is estimated to be worth xx Million in 2025 and is projected to reach xx Million by 2033.

Middle East Chocolate Market Market Structure & Innovation Trends

The Middle East chocolate market exhibits a moderately concentrated structure, with key players like Nestlé SA, Ferrero International SA, and Mars Incorporated holding significant market share. However, regional players and smaller artisanal brands also contribute significantly to the market's diversity. Innovation is driven by consumer demand for healthier options, including plant-based and reduced-sugar chocolates, as evidenced by Barry Callebaut's recent product launches. Regulatory frameworks concerning food safety and labeling influence market practices. Product substitutes include confectionery items like candies and gum, while end-user demographics encompass diverse age groups and income levels. M&A activity in the sector remains relatively moderate, with recent deals totaling an estimated xx Million in value.

- Market Concentration: Moderately concentrated, with top players holding xx% market share.

- Innovation Drivers: Healthier options (plant-based, reduced sugar), premiumization, and unique flavor profiles.

- Regulatory Framework: Focus on food safety, labeling regulations, and import/export controls.

- Product Substitutes: Candies, gums, and other confectionery items.

- End-User Demographics: Diverse age groups and income levels.

- M&A Activity: Recent deals valued at approximately xx Million.

Middle East Chocolate Market Market Dynamics & Trends

The Middle East chocolate market demonstrates robust growth, driven by rising disposable incomes, increasing urbanization, and a growing preference for premium and indulgent food products. The market's CAGR from 2019-2024 was xx%, and is projected to be xx% from 2025-2033. Technological disruptions, particularly in packaging and distribution, are influencing market efficiency and consumer experience. Consumer preferences are shifting towards healthier options, such as dark chocolate and plant-based alternatives, along with customized and personalized products. Competitive dynamics are characterized by intense competition among multinational giants and regional brands, leading to strategies focused on innovation, branding, and distribution. Market penetration remains high in major urban centers, with ongoing expansion into rural areas and less developed markets.

Dominant Regions & Segments in Middle East Chocolate Market

The United Arab Emirates (UAE) and Saudi Arabia represent the dominant markets within the Middle East chocolate sector, driven by their high population density, strong economic growth, and established retail infrastructure. The Supermarket/Hypermarket channel holds the largest market share, followed by convenience stores and online retail. Milk chocolate remains the most popular confectionery variant, followed by dark chocolate and then white chocolate.

Key Drivers in UAE & Saudi Arabia: High disposable incomes, robust tourism, and advanced retail infrastructure.

Distribution Channel Dominance: Supermarket/Hypermarket, followed by convenience stores and a rapidly growing online retail sector.

Confectionery Variant Preference: Milk chocolate holds the largest market share, followed by dark chocolate and white chocolate.

Other Countries: Significant growth potential in Oman, Qatar, Kuwait, Bahrain, and the Rest of Middle East.

Dominant Countries:

- UAE: Strong economic growth, high tourism, and sophisticated retail landscape.

- Saudi Arabia: Large population, rising disposable incomes, and government support for the food industry.

Middle East Chocolate Market Product Innovations

Recent product innovations focus on healthier options, including plant-based chocolates and those with reduced sugar content. Companies are also exploring unique flavor combinations and premium ingredients to cater to evolving consumer preferences. These innovations are aimed at attracting health-conscious consumers while maintaining the appeal of traditional chocolate products, capitalizing on emerging trends in premiumization and sustainability.

Report Scope & Segmentation Analysis

This report segments the Middle East chocolate market by country (Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, UAE, Rest of Middle East), confectionery variant (dark chocolate, milk chocolate, white chocolate), and distribution channel (convenience stores, online retail stores, supermarket/hypermarkets, others). Growth projections for each segment are provided, along with detailed analysis of market size and competitive dynamics. Each segment shows significant growth potential, driven by unique factors like economic development, consumer preferences, and retail infrastructure.

Key Drivers of Middle East Chocolate Market Growth

Several key factors drive the growth of the Middle East chocolate market, including rising disposable incomes, increased urbanization, and the growing popularity of premium and indulgent food products. The region's youthful demographics and increasing preference for Western-style snacks and treats also contribute to the market's expansion. Favorable government policies and investments in retail infrastructure further support this growth trajectory.

Challenges in the Middle East Chocolate Market Sector

Challenges include the volatile nature of commodity prices (cocoa, sugar), fluctuating exchange rates, and stringent regulations on food imports and labeling. The intense competition among international and regional players adds to the challenges faced by existing businesses. Supply chain disruptions and increased logistics costs can impact profitability.

Emerging Opportunities in Middle East Chocolate Market

Emerging opportunities include the increasing demand for healthier and ethically sourced chocolate, growth in the online retail sector, and expansion into underserved markets within the region. The potential for premiumization and the introduction of innovative flavors and product formats present substantial opportunities for players in the market.

Leading Players in the Middle East Chocolate Market Market

- Nestlé SA

- Dadash Baradar Industrial Co

- Shirin Asal Food Industrial Group

- Chocoladefabriken Lindt & Sprüngli AG

- Lee Chocolate LLC

- Berry Callebaut

- Makaw Chocolate LLC

- Ferrero International SA

- Mars Incorporated

- Yıldız Holding A

- IFFCO

- Patchi LLC

- Parand Chocolate Co

- Strauss Group Ltd

- Mondelēz International Inc

- Bostani Chocolatier Inc

- The Hershey Company

Key Developments in Middle East Chocolate Market Industry

- November 2022: Nestlé announced a SAR 7 billion investment in Saudi Arabia, including USD 99.6 million for a new manufacturing plant (opening 2025). This signifies a major commitment to the regional market and potential for increased production capacity.

- November 2022: Barry Callebaut launched its 100% plant-based chocolate NXT in Saudi Arabia, catering to the growing demand for vegan options and expanding its product portfolio.

- September 2022: Barry Callebaut launched its whole-fruit chocolate line under the Cacao Barry brand in the UAE, focusing on reduced sugar content and highlighting health-conscious consumer trends.

Future Outlook for Middle East Chocolate Market Market

The Middle East chocolate market is poised for continued growth, driven by sustained economic expansion, evolving consumer preferences, and the entry of new players. The focus on healthier options and product innovation will continue to shape market dynamics. Strategic partnerships and investments in efficient distribution channels will be crucial for success in this competitive landscape.

Middle East Chocolate Market Segmentation

-

1. Confectionery Variant

- 1.1. Dark Chocolate

- 1.2. Milk and White Chocolate

-

2. Distribution Channel

- 2.1. Convenience Store

- 2.2. Online Retail Store

- 2.3. Supermarket/Hypermarket

- 2.4. Others

Middle East Chocolate Market Segmentation By Geography

-

1. Middle East

- 1.1. Saudi Arabia

- 1.2. United Arab Emirates

- 1.3. Israel

- 1.4. Qatar

- 1.5. Kuwait

- 1.6. Oman

- 1.7. Bahrain

- 1.8. Jordan

- 1.9. Lebanon

Middle East Chocolate Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 6.20% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increasing Demand for Functional and Fortified Food; Multi-functionality and Wide Application of Riboflavin

- 3.3. Market Restrains

- 3.3.1. Low Stability of Riboflavin on Exposure to Light and Heat

- 3.4. Market Trends

- 3.4.1. OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Middle East Chocolate Market Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Confectionery Variant

- 5.1.1. Dark Chocolate

- 5.1.2. Milk and White Chocolate

- 5.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.2.1. Convenience Store

- 5.2.2. Online Retail Store

- 5.2.3. Supermarket/Hypermarket

- 5.2.4. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Middle East

- 5.1. Market Analysis, Insights and Forecast - by Confectionery Variant

- 6. United Arab Emirates Middle East Chocolate Market Analysis, Insights and Forecast, 2019-2031

- 7. Saudi Arabia Middle East Chocolate Market Analysis, Insights and Forecast, 2019-2031

- 8. Qatar Middle East Chocolate Market Analysis, Insights and Forecast, 2019-2031

- 9. Israel Middle East Chocolate Market Analysis, Insights and Forecast, 2019-2031

- 10. Egypt Middle East Chocolate Market Analysis, Insights and Forecast, 2019-2031

- 11. Oman Middle East Chocolate Market Analysis, Insights and Forecast, 2019-2031

- 12. Rest of Middle East Middle East Chocolate Market Analysis, Insights and Forecast, 2019-2031

- 13. Competitive Analysis

- 13.1. Market Share Analysis 2024

- 13.2. Company Profiles

- 13.2.1 Nestlé SA

- 13.2.1.1. Overview

- 13.2.1.2. Products

- 13.2.1.3. SWOT Analysis

- 13.2.1.4. Recent Developments

- 13.2.1.5. Financials (Based on Availability)

- 13.2.2 Dadash Baradar Industrial Co

- 13.2.2.1. Overview

- 13.2.2.2. Products

- 13.2.2.3. SWOT Analysis

- 13.2.2.4. Recent Developments

- 13.2.2.5. Financials (Based on Availability)

- 13.2.3 Shirin Asal Food Industrial Group

- 13.2.3.1. Overview

- 13.2.3.2. Products

- 13.2.3.3. SWOT Analysis

- 13.2.3.4. Recent Developments

- 13.2.3.5. Financials (Based on Availability)

- 13.2.4 Chocoladefabriken Lindt & Sprüngli AG

- 13.2.4.1. Overview

- 13.2.4.2. Products

- 13.2.4.3. SWOT Analysis

- 13.2.4.4. Recent Developments

- 13.2.4.5. Financials (Based on Availability)

- 13.2.5 Lee Chocolate LLC

- 13.2.5.1. Overview

- 13.2.5.2. Products

- 13.2.5.3. SWOT Analysis

- 13.2.5.4. Recent Developments

- 13.2.5.5. Financials (Based on Availability)

- 13.2.6 Berry Callebaut

- 13.2.6.1. Overview

- 13.2.6.2. Products

- 13.2.6.3. SWOT Analysis

- 13.2.6.4. Recent Developments

- 13.2.6.5. Financials (Based on Availability)

- 13.2.7 Makaw Chocolate LLC

- 13.2.7.1. Overview

- 13.2.7.2. Products

- 13.2.7.3. SWOT Analysis

- 13.2.7.4. Recent Developments

- 13.2.7.5. Financials (Based on Availability)

- 13.2.8 Ferrero International SA

- 13.2.8.1. Overview

- 13.2.8.2. Products

- 13.2.8.3. SWOT Analysis

- 13.2.8.4. Recent Developments

- 13.2.8.5. Financials (Based on Availability)

- 13.2.9 Mars Incorporated

- 13.2.9.1. Overview

- 13.2.9.2. Products

- 13.2.9.3. SWOT Analysis

- 13.2.9.4. Recent Developments

- 13.2.9.5. Financials (Based on Availability)

- 13.2.10 Yıldız Holding A

- 13.2.10.1. Overview

- 13.2.10.2. Products

- 13.2.10.3. SWOT Analysis

- 13.2.10.4. Recent Developments

- 13.2.10.5. Financials (Based on Availability)

- 13.2.11 IFFCO

- 13.2.11.1. Overview

- 13.2.11.2. Products

- 13.2.11.3. SWOT Analysis

- 13.2.11.4. Recent Developments

- 13.2.11.5. Financials (Based on Availability)

- 13.2.12 Patchi LLC

- 13.2.12.1. Overview

- 13.2.12.2. Products

- 13.2.12.3. SWOT Analysis

- 13.2.12.4. Recent Developments

- 13.2.12.5. Financials (Based on Availability)

- 13.2.13 Parand Chocolate Co

- 13.2.13.1. Overview

- 13.2.13.2. Products

- 13.2.13.3. SWOT Analysis

- 13.2.13.4. Recent Developments

- 13.2.13.5. Financials (Based on Availability)

- 13.2.14 Strauss Group Ltd

- 13.2.14.1. Overview

- 13.2.14.2. Products

- 13.2.14.3. SWOT Analysis

- 13.2.14.4. Recent Developments

- 13.2.14.5. Financials (Based on Availability)

- 13.2.15 Mondelēz International Inc

- 13.2.15.1. Overview

- 13.2.15.2. Products

- 13.2.15.3. SWOT Analysis

- 13.2.15.4. Recent Developments

- 13.2.15.5. Financials (Based on Availability)

- 13.2.16 Bostani Chocolatier Inc

- 13.2.16.1. Overview

- 13.2.16.2. Products

- 13.2.16.3. SWOT Analysis

- 13.2.16.4. Recent Developments

- 13.2.16.5. Financials (Based on Availability)

- 13.2.17 The Hershey Company

- 13.2.17.1. Overview

- 13.2.17.2. Products

- 13.2.17.3. SWOT Analysis

- 13.2.17.4. Recent Developments

- 13.2.17.5. Financials (Based on Availability)

- 13.2.1 Nestlé SA

List of Figures

- Figure 1: Middle East Chocolate Market Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Middle East Chocolate Market Share (%) by Company 2024

List of Tables

- Table 1: Middle East Chocolate Market Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Middle East Chocolate Market Revenue Million Forecast, by Confectionery Variant 2019 & 2032

- Table 3: Middle East Chocolate Market Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 4: Middle East Chocolate Market Revenue Million Forecast, by Region 2019 & 2032

- Table 5: Middle East Chocolate Market Revenue Million Forecast, by Country 2019 & 2032

- Table 6: United Arab Emirates Middle East Chocolate Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 7: Saudi Arabia Middle East Chocolate Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Qatar Middle East Chocolate Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Israel Middle East Chocolate Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Egypt Middle East Chocolate Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: Oman Middle East Chocolate Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: Rest of Middle East Middle East Chocolate Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: Middle East Chocolate Market Revenue Million Forecast, by Confectionery Variant 2019 & 2032

- Table 14: Middle East Chocolate Market Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 15: Middle East Chocolate Market Revenue Million Forecast, by Country 2019 & 2032

- Table 16: Saudi Arabia Middle East Chocolate Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 17: United Arab Emirates Middle East Chocolate Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 18: Israel Middle East Chocolate Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 19: Qatar Middle East Chocolate Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 20: Kuwait Middle East Chocolate Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 21: Oman Middle East Chocolate Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 22: Bahrain Middle East Chocolate Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 23: Jordan Middle East Chocolate Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 24: Lebanon Middle East Chocolate Market Revenue (Million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Middle East Chocolate Market?

The projected CAGR is approximately 6.20%.

2. Which companies are prominent players in the Middle East Chocolate Market?

Key companies in the market include Nestlé SA, Dadash Baradar Industrial Co, Shirin Asal Food Industrial Group, Chocoladefabriken Lindt & Sprüngli AG, Lee Chocolate LLC, Berry Callebaut, Makaw Chocolate LLC, Ferrero International SA, Mars Incorporated, Yıldız Holding A, IFFCO, Patchi LLC, Parand Chocolate Co, Strauss Group Ltd, Mondelēz International Inc, Bostani Chocolatier Inc, The Hershey Company.

3. What are the main segments of the Middle East Chocolate Market?

The market segments include Confectionery Variant, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Demand for Functional and Fortified Food; Multi-functionality and Wide Application of Riboflavin.

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

Low Stability of Riboflavin on Exposure to Light and Heat.

8. Can you provide examples of recent developments in the market?

November 2022: Nestlé announced plans to invest SAR 7 billion in the Kingdom of Saudi Arabia in the coming ten years in a strategic move to grow its longstanding business in the country, beginning with up to USD 99.6 million to establish a cutting-edge manufacturing plant – which is set to open in 2025.November 2022: Barry Callebaut launched 100% dairy-free and plant-based chocolate NXT in Saudi Arabia. NXT is the first-of-its-kind dairy-free, lactose-free, nut-free, allergen-free, 100% plant-based, and vegan dark and milk chocolate to respond to the growing demand for plant-based foods across the country.September 2022: Barry Callebaut launched its line of whole-fruit chocolates under the Cacao Barry brand in the United Arab Emirates. The product has less sugar than conventional dark chocolate and is made from pure cacao fruit.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Middle East Chocolate Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Middle East Chocolate Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Middle East Chocolate Market?

To stay informed about further developments, trends, and reports in the Middle East Chocolate Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence