Key Insights

The North American data center server market is experiencing robust growth, projected to reach a significant size by 2033. Driven by the increasing adoption of cloud computing, big data analytics, and artificial intelligence (AI), the demand for high-performance servers is surging. The IT & Telecommunication sector remains the dominant end-user, fueled by the expansion of 5G networks and the need for advanced data processing capabilities. However, growth is also being seen in other sectors like BFSI and government, driven by digital transformation initiatives and the need for enhanced security and data management solutions. The diverse form factors available – blade, rack, and tower servers – cater to varying needs and deployment scenarios, with rack servers maintaining a significant market share due to their scalability and cost-effectiveness. While the market shows strong potential, factors such as supply chain disruptions and increasing energy costs pose challenges to sustained growth. However, innovative solutions like energy-efficient server designs and advancements in cooling technologies are expected to mitigate these constraints.

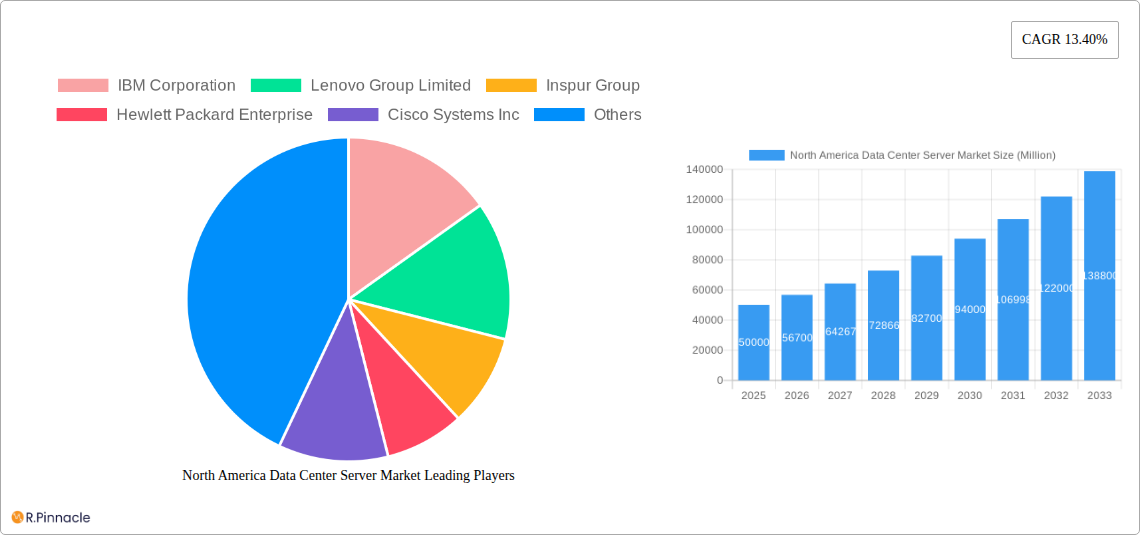

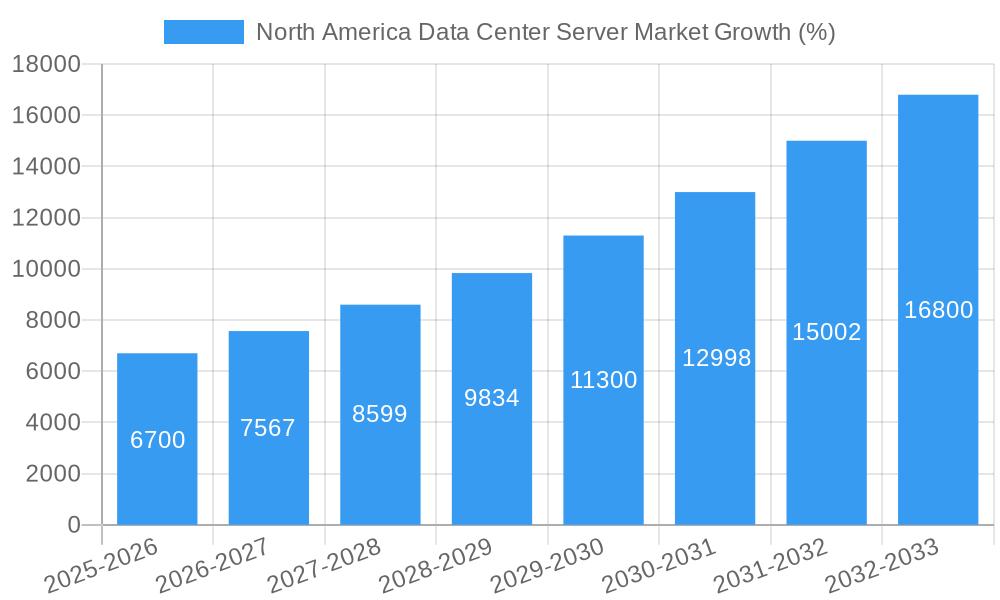

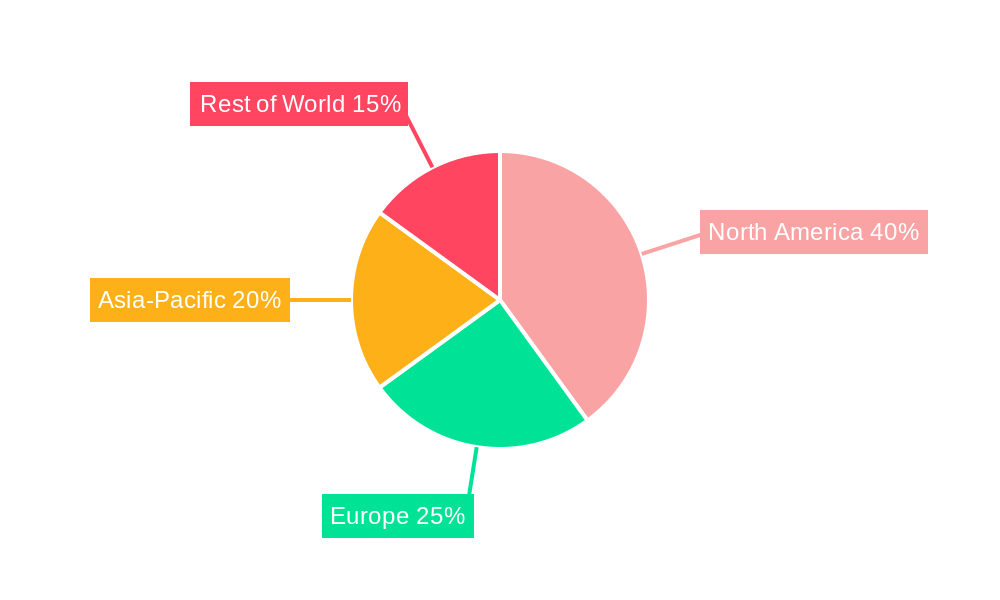

The forecast period (2025-2033) anticipates a continuation of the strong growth trajectory, with a Compound Annual Growth Rate (CAGR) of 13.40% expected. This growth will be further fueled by the increasing adoption of edge computing, which necessitates a decentralized server infrastructure. Competition is intense, with established players like IBM, Lenovo, Hewlett Packard Enterprise, and Dell alongside emerging players vying for market share. The market’s evolution is likely to see increased emphasis on sustainable practices, as organizations prioritize environmentally friendly data center operations. The North American market is expected to maintain a substantial global market share due to its strong technological infrastructure and high concentration of data centers. Specific regional dynamics within North America will vary, with the United States likely to hold the largest share, followed by Canada and Mexico.

North America Data Center Server Market Report: 2019-2033

This comprehensive report provides an in-depth analysis of the North America data center server market, offering actionable insights for industry professionals. The study period spans 2019-2033, with 2025 serving as the base and estimated year. The report covers market size, segmentation, growth drivers, challenges, opportunities, and key players, utilizing a combination of historical data (2019-2024) and forecast projections (2025-2033). Expected market value is projected at xx Million by 2033.

North America Data Center Server Market Structure & Innovation Trends

This section analyzes the competitive landscape, innovation drivers, and regulatory factors shaping the North America data center server market. The market is characterized by a moderately concentrated structure, with key players holding significant market share. The top 10 players—IBM Corporation, Lenovo Group Limited, Inspur Group, Hewlett Packard Enterprise, Cisco Systems Inc, Super Micro Computer Inc, Fujitsu Limited, Quanta Computer Inc, Dell Inc, and Kingston Technology Company Inc—collectively account for an estimated xx% of the market.

- Market Concentration: High concentration among leading vendors, leading to competitive pricing strategies and product differentiation.

- Innovation Drivers: Demand for high-performance computing, increasing adoption of cloud computing and AI, and the need for energy-efficient solutions. Recent advancements in processor technology (e.g., Intel Sapphire Rapids) are key drivers.

- Regulatory Framework: Compliance requirements (data privacy, security) influence server design and deployment.

- Product Substitutes: Virtualization and cloud-based solutions pose some competition, but the demand for on-premises servers remains robust.

- End-User Demographics: The IT & Telecommunication sector is a significant end-user segment, followed by BFSI, Government, and Media & Entertainment.

- M&A Activities: Consolidation in the market through mergers and acquisitions (M&A) is expected to continue, with deal values projected at xx Million annually in the forecast period.

North America Data Center Server Market Dynamics & Trends

The North America data center server market is experiencing significant growth, driven by several key factors. The market exhibited a CAGR of xx% during the historical period (2019-2024) and is projected to maintain a healthy growth trajectory with a CAGR of xx% during the forecast period (2025-2033). This growth is primarily fueled by the increasing adoption of cloud computing, the rise of big data analytics, and the growing demand for high-performance computing. Technological advancements, such as the introduction of more energy-efficient servers and the development of new server architectures to support AI workloads are also crucial catalysts. Furthermore, consumer preference for faster processing speeds, improved data security, and greater energy efficiency in data centers is driving demand. Competitive dynamics are intense, with major vendors continuously striving to improve their offerings through innovations and strategic partnerships. Market penetration of blade servers is expected to increase due to their space-saving design and high density, while the rack server segment will maintain its dominant position.

Dominant Regions & Segments in North America Data Center Server Market

The report identifies key regions and segments within the North America data center server market that are experiencing the strongest growth.

Dominant Region: The United States is expected to continue its dominance in the market throughout the forecast period, driven by strong technological advancements and high adoption of cloud services. Canada and Mexico are also key markets showing steady growth.

Dominant Form Factors: The rack server segment currently holds the largest market share, driven by its versatility and scalability, followed by blade servers, favored for their space efficiency. The tower server segment has lower market share but maintains steady demand, particularly in small and medium-sized businesses.

Dominant End-Users: The IT & Telecommunication sector remains the dominant end-user, primarily due to its significant investments in infrastructure and cloud computing. The BFSI sector is also a significant contributor, followed by the Government and Media & Entertainment sectors. Growth within these sectors is directly linked to their respective digital transformation initiatives and technological advancements within the data center infrastructure. Key drivers include increasing data volume, need for improved security, stringent compliance requirements and need to support growing remote workforces.

North America Data Center Server Market Product Innovations

Recent product innovations underscore the market's dynamic nature. Dell's launch of generative AI solutions exemplifies the shift towards high-performance computing for AI applications. Cisco's energy-efficient UCS X servers address growing concerns about sustainability in data centers. Lenovo's introduction of new servers with Intel's Sapphire Rapids processors demonstrates the continuous advancement in processor technology and its impact on server performance and efficiency. These advancements highlight the continuous push towards faster processing, increased energy efficiency, and enhanced security. The market is experiencing a considerable demand for GPU accelerator servers due to the intensive computational demands of generative AI workflows.

Report Scope & Segmentation Analysis

This report segments the North America data center server market based on form factor (blade, rack, tower) and end-user (IT & Telecommunication, BFSI, Government, Media & Entertainment, Other). Each segment's growth projections, market sizes, and competitive dynamics are analyzed separately. The report projects significant growth in the blade server segment due to increasing demand for high density and space-saving solutions. The rack server segment is expected to dominate due to its versatility and adaptability, while the tower server segment will see moderate growth in niche markets. For end-users, the IT & Telecommunication sector is projected to have the highest growth rate due to increasing adoption of cloud services and expansion of 5G networks. The BFSI, Government, and Media & Entertainment segments will experience steady growth, driven by their need for enhanced security, data analytics, and sophisticated data management capabilities.

Key Drivers of North America Data Center Server Market Growth

Several factors propel the market's growth. Firstly, the escalating demand for cloud computing, big data analytics, and AI necessitates advanced server technologies with high processing power and storage capabilities. Secondly, the growing adoption of digital technologies across various sectors creates a surge in demand for data center infrastructure upgrades. Finally, advancements in semiconductor technology continuously improve server performance, energy efficiency, and overall cost-effectiveness.

Challenges in the North America Data Center Server Market Sector

Challenges include supply chain disruptions impacting component availability and increasing production costs. Competition among major vendors leads to price pressure, reducing profit margins. Furthermore, stringent regulatory requirements related to data privacy and security add to the complexity and cost of server deployments.

Emerging Opportunities in North America Data Center Server Market

The market presents significant opportunities in emerging technologies like edge computing and AI. The growing adoption of 5G networks opens new avenues for deploying high-performance servers at the network edge. Furthermore, the demand for energy-efficient servers presents an opportunity for innovation and market leadership.

Leading Players in the North America Data Center Server Market Market

- IBM Corporation

- Lenovo Group Limited

- Inspur Group

- Hewlett Packard Enterprise

- Cisco Systems Inc

- Super Micro Computer Inc

- Fujitsu Limited

- Quanta Computer Inc

- Dell Inc

- Kingston Technology Company Inc

Key Developments in North America Data Center Server Market Industry

- July 2023: Dell Inc. launched generative AI solutions, boosting demand for GPU accelerator servers.

- May 2023: Cisco Systems Inc. introduced energy-efficient UCS X servers, significantly reducing data center energy consumption.

- September 2022: Lenovo Group Ltd. launched new servers incorporating Intel's Sapphire Rapids processors, signaling advancements in processing power.

Future Outlook for North America Data Center Server Market Market

The North America data center server market is poised for continued growth, driven by ongoing technological advancements, increasing adoption of cloud and AI technologies, and the growing demand for energy-efficient solutions. Strategic partnerships, product innovation, and expansion into emerging markets will be crucial for maintaining a competitive edge. The market is projected to achieve significant growth in the coming years, presenting attractive opportunities for both established players and new entrants.

North America Data Center Server Market Segmentation

-

1. Form Factor

- 1.1. Blade Server

- 1.2. Rack Server

- 1.3. Tower Server

-

2. End-User

- 2.1. IT & Telecommunication

- 2.2. BFSI

- 2.3. Government

- 2.4. Media & Entertainment

- 2.5. Other End-User

-

3. Geography

- 3.1. United States

- 3.2. Canada

- 3.3. Mexico

- 3.4. Rest of North America

North America Data Center Server Market Segmentation By Geography

- 1. United States

- 2. Canada

- 3. Mexico

- 4. Rest of North America

North America Data Center Server Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 13.40% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increasing Adoption of Cloud and IoT Services; Large-scale commercialization of 5G networks

- 3.3. Market Restrains

- 3.3.1. Rising CapEx for data center construction

- 3.4. Market Trends

- 3.4.1. IT & Telecommunication Segment Holds The Major Share.

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. North America Data Center Server Market Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Form Factor

- 5.1.1. Blade Server

- 5.1.2. Rack Server

- 5.1.3. Tower Server

- 5.2. Market Analysis, Insights and Forecast - by End-User

- 5.2.1. IT & Telecommunication

- 5.2.2. BFSI

- 5.2.3. Government

- 5.2.4. Media & Entertainment

- 5.2.5. Other End-User

- 5.3. Market Analysis, Insights and Forecast - by Geography

- 5.3.1. United States

- 5.3.2. Canada

- 5.3.3. Mexico

- 5.3.4. Rest of North America

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. United States

- 5.4.2. Canada

- 5.4.3. Mexico

- 5.4.4. Rest of North America

- 5.1. Market Analysis, Insights and Forecast - by Form Factor

- 6. United States North America Data Center Server Market Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Form Factor

- 6.1.1. Blade Server

- 6.1.2. Rack Server

- 6.1.3. Tower Server

- 6.2. Market Analysis, Insights and Forecast - by End-User

- 6.2.1. IT & Telecommunication

- 6.2.2. BFSI

- 6.2.3. Government

- 6.2.4. Media & Entertainment

- 6.2.5. Other End-User

- 6.3. Market Analysis, Insights and Forecast - by Geography

- 6.3.1. United States

- 6.3.2. Canada

- 6.3.3. Mexico

- 6.3.4. Rest of North America

- 6.1. Market Analysis, Insights and Forecast - by Form Factor

- 7. Canada North America Data Center Server Market Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Form Factor

- 7.1.1. Blade Server

- 7.1.2. Rack Server

- 7.1.3. Tower Server

- 7.2. Market Analysis, Insights and Forecast - by End-User

- 7.2.1. IT & Telecommunication

- 7.2.2. BFSI

- 7.2.3. Government

- 7.2.4. Media & Entertainment

- 7.2.5. Other End-User

- 7.3. Market Analysis, Insights and Forecast - by Geography

- 7.3.1. United States

- 7.3.2. Canada

- 7.3.3. Mexico

- 7.3.4. Rest of North America

- 7.1. Market Analysis, Insights and Forecast - by Form Factor

- 8. Mexico North America Data Center Server Market Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Form Factor

- 8.1.1. Blade Server

- 8.1.2. Rack Server

- 8.1.3. Tower Server

- 8.2. Market Analysis, Insights and Forecast - by End-User

- 8.2.1. IT & Telecommunication

- 8.2.2. BFSI

- 8.2.3. Government

- 8.2.4. Media & Entertainment

- 8.2.5. Other End-User

- 8.3. Market Analysis, Insights and Forecast - by Geography

- 8.3.1. United States

- 8.3.2. Canada

- 8.3.3. Mexico

- 8.3.4. Rest of North America

- 8.1. Market Analysis, Insights and Forecast - by Form Factor

- 9. Rest of North America North America Data Center Server Market Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Form Factor

- 9.1.1. Blade Server

- 9.1.2. Rack Server

- 9.1.3. Tower Server

- 9.2. Market Analysis, Insights and Forecast - by End-User

- 9.2.1. IT & Telecommunication

- 9.2.2. BFSI

- 9.2.3. Government

- 9.2.4. Media & Entertainment

- 9.2.5. Other End-User

- 9.3. Market Analysis, Insights and Forecast - by Geography

- 9.3.1. United States

- 9.3.2. Canada

- 9.3.3. Mexico

- 9.3.4. Rest of North America

- 9.1. Market Analysis, Insights and Forecast - by Form Factor

- 10. United States North America Data Center Server Market Analysis, Insights and Forecast, 2019-2031

- 11. Canada North America Data Center Server Market Analysis, Insights and Forecast, 2019-2031

- 12. Mexico North America Data Center Server Market Analysis, Insights and Forecast, 2019-2031

- 13. Rest of North America North America Data Center Server Market Analysis, Insights and Forecast, 2019-2031

- 14. Competitive Analysis

- 14.1. Market Share Analysis 2024

- 14.2. Company Profiles

- 14.2.1 IBM Corporation

- 14.2.1.1. Overview

- 14.2.1.2. Products

- 14.2.1.3. SWOT Analysis

- 14.2.1.4. Recent Developments

- 14.2.1.5. Financials (Based on Availability)

- 14.2.2 Lenovo Group Limited

- 14.2.2.1. Overview

- 14.2.2.2. Products

- 14.2.2.3. SWOT Analysis

- 14.2.2.4. Recent Developments

- 14.2.2.5. Financials (Based on Availability)

- 14.2.3 Inspur Group

- 14.2.3.1. Overview

- 14.2.3.2. Products

- 14.2.3.3. SWOT Analysis

- 14.2.3.4. Recent Developments

- 14.2.3.5. Financials (Based on Availability)

- 14.2.4 Hewlett Packard Enterprise

- 14.2.4.1. Overview

- 14.2.4.2. Products

- 14.2.4.3. SWOT Analysis

- 14.2.4.4. Recent Developments

- 14.2.4.5. Financials (Based on Availability)

- 14.2.5 Cisco Systems Inc

- 14.2.5.1. Overview

- 14.2.5.2. Products

- 14.2.5.3. SWOT Analysis

- 14.2.5.4. Recent Developments

- 14.2.5.5. Financials (Based on Availability)

- 14.2.6 Super Micro Computer Inc

- 14.2.6.1. Overview

- 14.2.6.2. Products

- 14.2.6.3. SWOT Analysis

- 14.2.6.4. Recent Developments

- 14.2.6.5. Financials (Based on Availability)

- 14.2.7 Fujitsu Limited

- 14.2.7.1. Overview

- 14.2.7.2. Products

- 14.2.7.3. SWOT Analysis

- 14.2.7.4. Recent Developments

- 14.2.7.5. Financials (Based on Availability)

- 14.2.8 Quanta Computer Inc

- 14.2.8.1. Overview

- 14.2.8.2. Products

- 14.2.8.3. SWOT Analysis

- 14.2.8.4. Recent Developments

- 14.2.8.5. Financials (Based on Availability)

- 14.2.9 Dell Inc

- 14.2.9.1. Overview

- 14.2.9.2. Products

- 14.2.9.3. SWOT Analysis

- 14.2.9.4. Recent Developments

- 14.2.9.5. Financials (Based on Availability)

- 14.2.10 Kingston Technology Company Inc

- 14.2.10.1. Overview

- 14.2.10.2. Products

- 14.2.10.3. SWOT Analysis

- 14.2.10.4. Recent Developments

- 14.2.10.5. Financials (Based on Availability)

- 14.2.1 IBM Corporation

List of Figures

- Figure 1: North America Data Center Server Market Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: North America Data Center Server Market Share (%) by Company 2024

List of Tables

- Table 1: North America Data Center Server Market Revenue Million Forecast, by Region 2019 & 2032

- Table 2: North America Data Center Server Market Revenue Million Forecast, by Form Factor 2019 & 2032

- Table 3: North America Data Center Server Market Revenue Million Forecast, by End-User 2019 & 2032

- Table 4: North America Data Center Server Market Revenue Million Forecast, by Geography 2019 & 2032

- Table 5: North America Data Center Server Market Revenue Million Forecast, by Region 2019 & 2032

- Table 6: North America Data Center Server Market Revenue Million Forecast, by Country 2019 & 2032

- Table 7: United States North America Data Center Server Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Canada North America Data Center Server Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Mexico North America Data Center Server Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Rest of North America North America Data Center Server Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: North America Data Center Server Market Revenue Million Forecast, by Form Factor 2019 & 2032

- Table 12: North America Data Center Server Market Revenue Million Forecast, by End-User 2019 & 2032

- Table 13: North America Data Center Server Market Revenue Million Forecast, by Geography 2019 & 2032

- Table 14: North America Data Center Server Market Revenue Million Forecast, by Country 2019 & 2032

- Table 15: North America Data Center Server Market Revenue Million Forecast, by Form Factor 2019 & 2032

- Table 16: North America Data Center Server Market Revenue Million Forecast, by End-User 2019 & 2032

- Table 17: North America Data Center Server Market Revenue Million Forecast, by Geography 2019 & 2032

- Table 18: North America Data Center Server Market Revenue Million Forecast, by Country 2019 & 2032

- Table 19: North America Data Center Server Market Revenue Million Forecast, by Form Factor 2019 & 2032

- Table 20: North America Data Center Server Market Revenue Million Forecast, by End-User 2019 & 2032

- Table 21: North America Data Center Server Market Revenue Million Forecast, by Geography 2019 & 2032

- Table 22: North America Data Center Server Market Revenue Million Forecast, by Country 2019 & 2032

- Table 23: North America Data Center Server Market Revenue Million Forecast, by Form Factor 2019 & 2032

- Table 24: North America Data Center Server Market Revenue Million Forecast, by End-User 2019 & 2032

- Table 25: North America Data Center Server Market Revenue Million Forecast, by Geography 2019 & 2032

- Table 26: North America Data Center Server Market Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Data Center Server Market?

The projected CAGR is approximately 13.40%.

2. Which companies are prominent players in the North America Data Center Server Market?

Key companies in the market include IBM Corporation, Lenovo Group Limited, Inspur Group, Hewlett Packard Enterprise, Cisco Systems Inc, Super Micro Computer Inc, Fujitsu Limited, Quanta Computer Inc , Dell Inc, Kingston Technology Company Inc.

3. What are the main segments of the North America Data Center Server Market?

The market segments include Form Factor, End-User, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Adoption of Cloud and IoT Services; Large-scale commercialization of 5G networks.

6. What are the notable trends driving market growth?

IT & Telecommunication Segment Holds The Major Share..

7. Are there any restraints impacting market growth?

Rising CapEx for data center construction.

8. Can you provide examples of recent developments in the market?

July 2023: Dell Inc. launched generative artificial intelligence solutions that offer a modular, full-stack architecture for enterprises seeking a secure, high-performance, proven architecture for deploying large language models (LLM). A paradigm shift in IT planning has taken place due to the rapid demand for GenAI at work, which will continue to ripple through the industry. Thus, there has been a strong demand for graphics processing unit (GPU) accelerator servers that are driving the computational intensive training and inferencing of GenAI workflows.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Data Center Server Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Data Center Server Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Data Center Server Market?

To stay informed about further developments, trends, and reports in the North America Data Center Server Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence