Key Insights

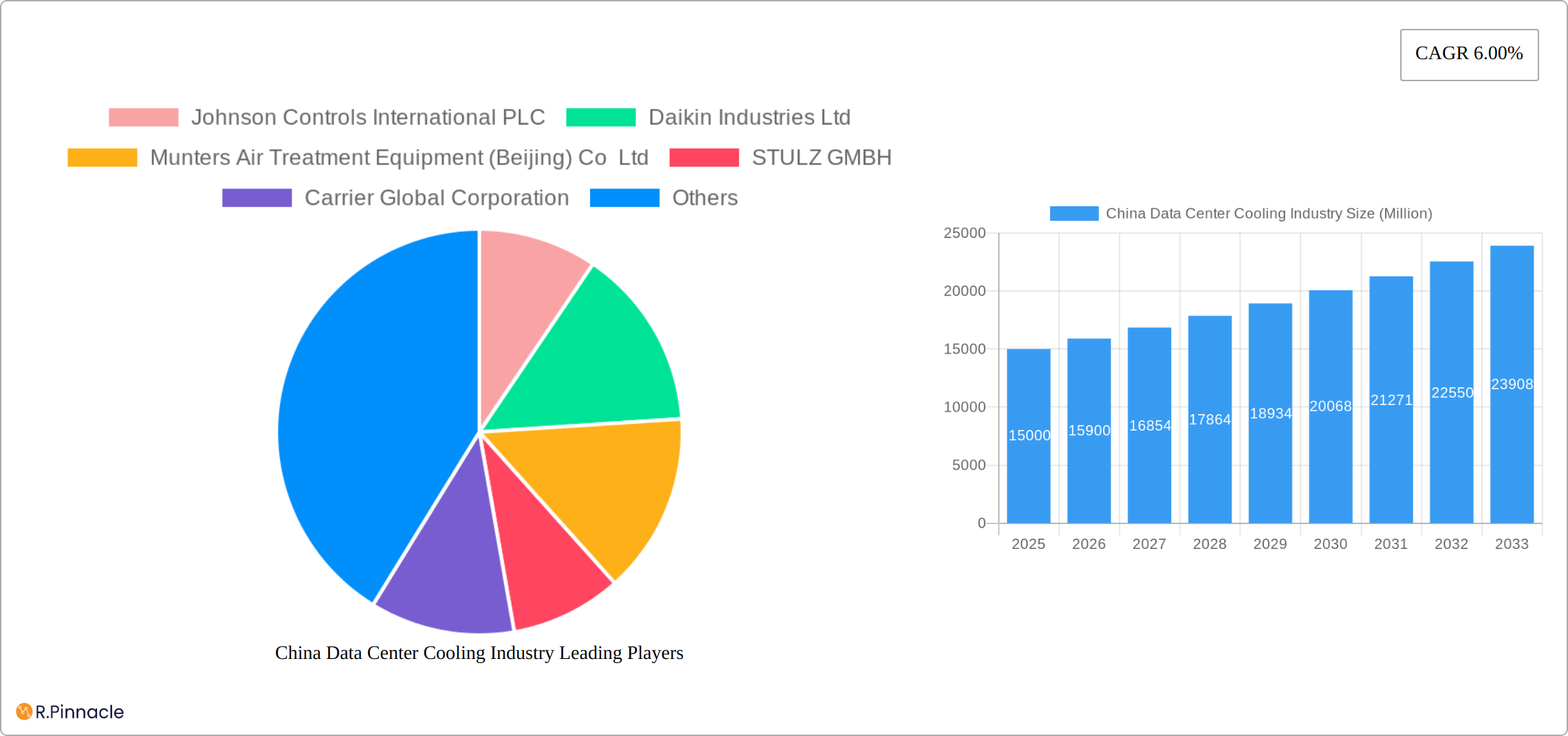

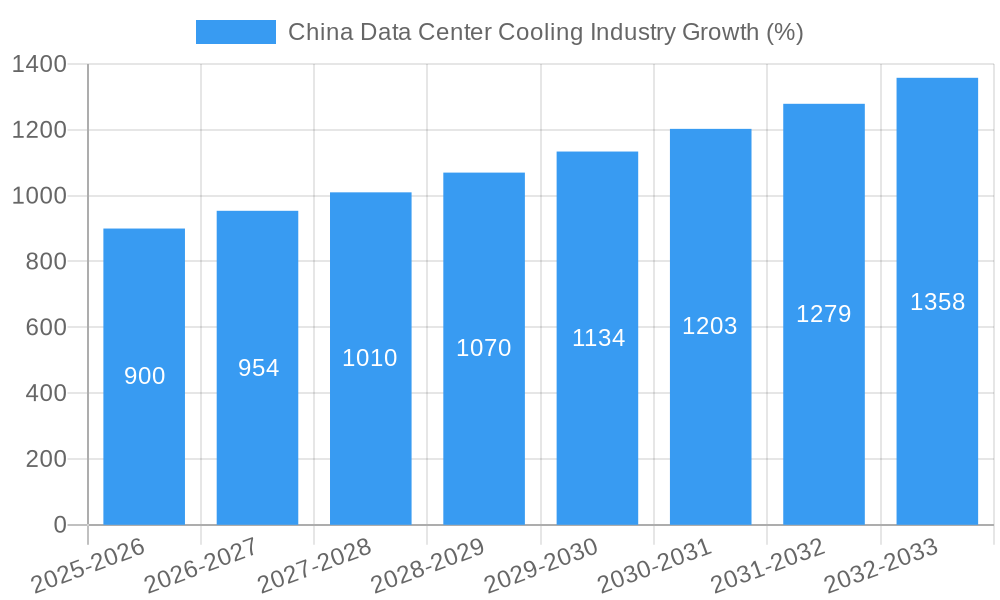

The China data center cooling market is experiencing robust growth, driven by the rapid expansion of the country's digital infrastructure and increasing demand for high-performance computing. With a Compound Annual Growth Rate (CAGR) of 6.00% from 2019-2033, the market is projected to reach a substantial size. This growth is fueled by several key factors. The burgeoning IT and telecommunication sector, along with the expanding financial services (BFSI) and government sectors, are major consumers of data center cooling solutions. Furthermore, the rise of cloud computing, big data analytics, and artificial intelligence (AI) applications necessitate advanced cooling technologies to manage the escalating heat generated by increasingly powerful servers. The adoption of energy-efficient cooling solutions, such as liquid-based cooling and evaporative cooling, is gaining momentum due to increasing environmental concerns and rising energy costs. However, the market faces challenges such as high initial investment costs for advanced cooling systems and the need for skilled workforce to install and maintain them. Competitive dynamics among leading players like Johnson Controls, Daikin, and STULZ are intensifying, leading to innovation in cooling technology and pricing strategies. The market segmentation reveals a preference for air-based cooling, likely due to its lower initial cost compared to other technologies. However, the increasing adoption of liquid cooling and evaporative cooling is anticipated to reshape this segment in the coming years.

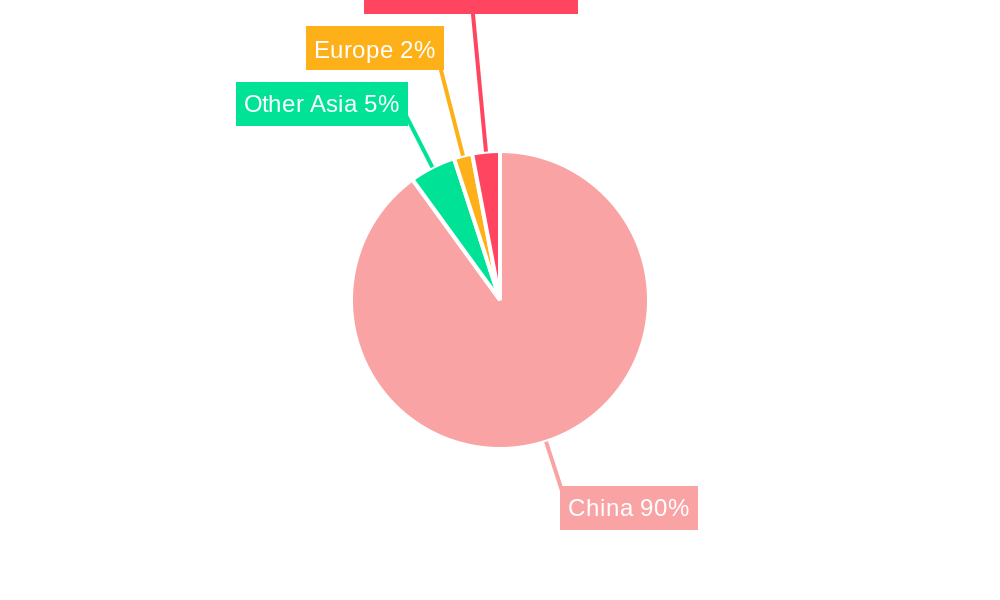

The China data center cooling market is geographically concentrated, with significant activity in major technology hubs. Given the substantial investments in data center infrastructure in these regions, the market is expected to maintain a strong growth trajectory throughout the forecast period (2025-2033). The competition among established players and emerging local companies will continue to shape the market landscape. Future growth will depend on the successful implementation of national digitalization strategies, the continued expansion of cloud computing services, and the development of more sustainable and efficient cooling technologies. Despite the challenges, the long-term outlook for the China data center cooling market remains positive, driven by the unstoppable growth of data and the need for reliable, efficient, and cost-effective cooling solutions. Considering the 2019-2024 historical period and the provided CAGR, a reasonable estimate for the 2025 market size could be in the range of $X Billion (assuming a logical extrapolation based on the provided CAGR).

China Data Center Cooling Industry Market Report: 2019-2033

This comprehensive report provides a detailed analysis of the China data center cooling industry, offering invaluable insights for industry professionals, investors, and strategic planners. The report covers the period from 2019 to 2033, with a focus on market size, segmentation, key players, technological advancements, and future growth prospects. The market is projected to reach xx Million by 2033.

China Data Center Cooling Industry Market Structure & Innovation Trends

This section analyzes the competitive landscape, innovation drivers, and regulatory influences shaping the China data center cooling market. The market is characterized by a mix of global and domestic players, with varying degrees of market concentration. Key players include Johnson Controls International PLC, Daikin Industries Ltd, Munters Air Treatment Equipment (Beijing) Co Ltd, STULZ GMBH, Carrier Global Corporation, Trane Inc, Condair Group, Vertiv Co, Schneider Electric SE, Chat Union Climaveneta, RITTAL Electro-Mechanical Technology Co Ltd, Gree Electric Appliances Inc of Zhuhai, and Mitsubishi Heavy Industries Ltd. However, this list is not exhaustive.

Market Concentration: The market exhibits moderate concentration, with the top 5 players holding an estimated xx% market share in 2025. This is expected to remain relatively stable throughout the forecast period.

Innovation Drivers: Stringent energy efficiency regulations, the increasing adoption of high-performance computing, and the growing demand for sustainable data center solutions are driving innovation in cooling technologies. Significant investments in R&D are observed across the industry.

Regulatory Frameworks: Government policies promoting energy efficiency and environmental sustainability are playing a crucial role in shaping the market. These policies are expected to influence the adoption of energy-efficient cooling technologies.

Product Substitutes: While traditional air-based cooling remains dominant, liquid-based and evaporative cooling systems are gaining traction due to their higher efficiency.

End-User Demographics: The IT & Telecommunication sector is the largest end-user segment, followed by BFSI, Government, and Media & Entertainment. The growth of these sectors directly fuels the demand for data center cooling solutions.

M&A Activities: The industry has witnessed a moderate level of M&A activity in recent years, with deal values totaling approximately xx Million during the historical period. Consolidation is expected to continue, driven by the need for increased scale and technological capabilities.

China Data Center Cooling Industry Market Dynamics & Trends

The China data center cooling market is experiencing robust growth, driven by several factors. The CAGR for the forecast period (2025-2033) is projected at xx%. Market penetration of advanced cooling technologies, such as liquid cooling, is steadily increasing.

Market Growth Drivers: The rapid expansion of the IT and telecommunications sector, the increasing adoption of cloud computing and big data analytics, and the growing demand for reliable and efficient data centers are primary drivers of market growth. Government initiatives promoting digital infrastructure development are also contributing significantly.

Technological Disruptions: Advancements in cooling technologies, including waterless cooling solutions (like Vertiv's X-Cooling), direct liquid cooling, and AI-powered optimization systems, are disrupting the traditional cooling landscape.

Consumer Preferences: End-users are increasingly prioritizing energy efficiency, sustainability, and reduced operational costs. This is driving the demand for innovative and eco-friendly cooling solutions.

Competitive Dynamics: The market is characterized by intense competition, with established players and emerging companies vying for market share through product innovation, strategic partnerships, and mergers and acquisitions.

Dominant Regions & Segments in China Data Center Cooling Industry

Leading Region: The eastern coastal regions of China, including Beijing, Shanghai, and Guangdong, dominate the data center cooling market due to the concentration of IT infrastructure, businesses, and data centers.

Dominant Segments:

Cooling Technology: Air-based cooling currently holds the largest market share, but liquid-based cooling is experiencing the fastest growth rate due to its higher efficiency in high-density data centers.

End-User: The IT & Telecommunication sector is the largest end-user segment, driven by the rapid expansion of cloud computing and digital services.

Key Drivers (Bullet Points):

- Robust economic growth: Driving increased investment in IT infrastructure.

- Government support: Through policies promoting digitalization and technological advancement.

- Expanding data center infrastructure: Fueled by the growth of e-commerce, cloud computing, and big data.

China Data Center Cooling Industry Product Innovations

Recent product innovations focus on improving energy efficiency, reducing water consumption, and enhancing cooling capacity. The introduction of waterless cooling technology like X-Cooling represents a significant breakthrough. Liquid cooling solutions, particularly direct-to-chip approaches, are gaining popularity due to their ability to handle high-density computing environments. These innovations are enhancing the overall performance and sustainability of data centers across various segments.

Report Scope & Segmentation Analysis

This report segments the China data center cooling market by cooling technology (air-based, liquid-based, evaporative) and end-user (IT & Telecommunication, BFSI, Government, Media & Entertainment, Other). Each segment's market size, growth projections, and competitive dynamics are analyzed. The market is anticipated to expand significantly driven by technological advancements and supportive government initiatives.

Cooling Technology Segmentation: Each technology segment demonstrates unique growth trajectories, with liquid-based cooling predicted for accelerated growth due to its efficiency advantages.

End-User Segmentation: The IT & Telecommunication segment will remain the largest contributor to overall revenue growth, while other sectors will contribute comparatively less.

Key Drivers of China Data Center Cooling Industry Growth

The China data center cooling industry's growth is driven by:

- Rapid growth of data centers: Fueled by increasing digitalization and cloud computing adoption.

- Government initiatives: Promoting digital infrastructure development and energy efficiency.

- Technological advancements: In cooling technologies, leading to higher efficiency and reduced operating costs.

Challenges in the China Data Center Cooling Industry Sector

Challenges include:

- High upfront costs: Associated with implementing advanced cooling solutions.

- Energy consumption: Concerns remain about the environmental impact of data centers.

- Supply chain disruptions: Causing delays and impacting the availability of components.

Emerging Opportunities in China Data Center Cooling Industry

Opportunities exist in:

- Waterless cooling technologies: Offering improved sustainability and efficiency.

- AI-powered cooling management systems: Optimizing energy consumption and reducing operational costs.

- Expansion into smaller cities: Bringing cooling solutions to data centers beyond major urban areas.

Leading Players in the China Data Center Cooling Industry Market

- Johnson Controls International PLC

- Daikin Industries Ltd

- Munters Air Treatment Equipment (Beijing) Co Ltd

- STULZ GMBH

- Carrier Global Corporation

- Trane Inc

- Condair Group

- Vertiv Co

- Schneider Electric SE

- Chat Union Climaveneta

- RITTAL Electro-Mechanical Technology Co Ltd

- Gree Electric Appliances Inc of Zhuhai

- Mitsubishi Heavy Industries Ltd

Key Developments in China Data Center Cooling Industry Industry

- July 2022: Chindata Group and Vertiv unveiled X-Cooling, a waterless cooling technology.

- February 2022: Gigabyte launched high-performance servers with CoolIT's direct liquid cooling system.

Future Outlook for China Data Center Cooling Industry Market

The China data center cooling market is poised for continued robust growth, driven by technological advancements, increasing data center deployments, and supportive government policies. The focus on energy efficiency and sustainability will further shape the market's trajectory, creating significant opportunities for innovative companies offering advanced cooling solutions.

China Data Center Cooling Industry Segmentation

-

1. Cooling Technology

-

1.1. Air-based Cooling

- 1.1.1. Chiller and Economizer

- 1.1.2. CRAH

- 1.1.3. Cooling

- 1.1.4. Other Air-based Cooling Technologies

-

1.2. Liquid-based Cooling

- 1.2.1. Immersion Cooling

- 1.2.2. Direct-to-chip Cooling

- 1.2.3. Rear-door Heat Exchanger

-

1.1. Air-based Cooling

-

2. Type

- 2.1. Hyperscaler (Owned and Leased)

- 2.2. Enterprise (On-premise)

- 2.3. Colocation

-

3. End-user Industry

- 3.1. IT and Telecom

- 3.2. Retail and Consumer Goods

- 3.3. Healthcare

- 3.4. Media and Entertainment

- 3.5. Federal and Institutional agencies

- 3.6. Other End-user Industries

China Data Center Cooling Industry Segmentation By Geography

- 1. China

China Data Center Cooling Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 6.00% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Development of IT Infrastructure in the Region; Emergence of Green Data Centers

- 3.3. Market Restrains

- 3.3.1 Costs

- 3.3.2 Adaptability Requirements

- 3.3.3 and Power Outages

- 3.4. Market Trends

- 3.4.1. Liquid-based cooling is the fastest growing segment

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. China Data Center Cooling Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Cooling Technology

- 5.1.1. Air-based Cooling

- 5.1.1.1. Chiller and Economizer

- 5.1.1.2. CRAH

- 5.1.1.3. Cooling

- 5.1.1.4. Other Air-based Cooling Technologies

- 5.1.2. Liquid-based Cooling

- 5.1.2.1. Immersion Cooling

- 5.1.2.2. Direct-to-chip Cooling

- 5.1.2.3. Rear-door Heat Exchanger

- 5.1.1. Air-based Cooling

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Hyperscaler (Owned and Leased)

- 5.2.2. Enterprise (On-premise)

- 5.2.3. Colocation

- 5.3. Market Analysis, Insights and Forecast - by End-user Industry

- 5.3.1. IT and Telecom

- 5.3.2. Retail and Consumer Goods

- 5.3.3. Healthcare

- 5.3.4. Media and Entertainment

- 5.3.5. Federal and Institutional agencies

- 5.3.6. Other End-user Industries

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. China

- 5.1. Market Analysis, Insights and Forecast - by Cooling Technology

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2024

- 6.2. Company Profiles

- 6.2.1 Johnson Controls International PLC

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 Daikin Industries Ltd

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 Munters Air Treatment Equipment (Beijing) Co Ltd

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 STULZ GMBH

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 Carrier Global Corporation

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 Trane Inc

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 Condair Group

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 Vertiv Co

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 Schneider Electric SE

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 Chat Union Climaveneta *List Not Exhaustive

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.11 RITTAL Electro-Mechanical Technology Co Ltd (RITTAL GMBH & CO KG)

- 6.2.11.1. Overview

- 6.2.11.2. Products

- 6.2.11.3. SWOT Analysis

- 6.2.11.4. Recent Developments

- 6.2.11.5. Financials (Based on Availability)

- 6.2.12 Gree Electric Appliances Inc of Zhuhai

- 6.2.12.1. Overview

- 6.2.12.2. Products

- 6.2.12.3. SWOT Analysis

- 6.2.12.4. Recent Developments

- 6.2.12.5. Financials (Based on Availability)

- 6.2.13 Mitsubishi Heavy Industries Ltd

- 6.2.13.1. Overview

- 6.2.13.2. Products

- 6.2.13.3. SWOT Analysis

- 6.2.13.4. Recent Developments

- 6.2.13.5. Financials (Based on Availability)

- 6.2.1 Johnson Controls International PLC

List of Figures

- Figure 1: China Data Center Cooling Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: China Data Center Cooling Industry Share (%) by Company 2024

List of Tables

- Table 1: China Data Center Cooling Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: China Data Center Cooling Industry Revenue Million Forecast, by Cooling Technology 2019 & 2032

- Table 3: China Data Center Cooling Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 4: China Data Center Cooling Industry Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 5: China Data Center Cooling Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 6: China Data Center Cooling Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 7: China Data Center Cooling Industry Revenue Million Forecast, by Cooling Technology 2019 & 2032

- Table 8: China Data Center Cooling Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 9: China Data Center Cooling Industry Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 10: China Data Center Cooling Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the China Data Center Cooling Industry?

The projected CAGR is approximately 6.00%.

2. Which companies are prominent players in the China Data Center Cooling Industry?

Key companies in the market include Johnson Controls International PLC, Daikin Industries Ltd, Munters Air Treatment Equipment (Beijing) Co Ltd, STULZ GMBH, Carrier Global Corporation, Trane Inc, Condair Group, Vertiv Co, Schneider Electric SE, Chat Union Climaveneta *List Not Exhaustive, RITTAL Electro-Mechanical Technology Co Ltd (RITTAL GMBH & CO KG), Gree Electric Appliances Inc of Zhuhai, Mitsubishi Heavy Industries Ltd.

3. What are the main segments of the China Data Center Cooling Industry?

The market segments include Cooling Technology, Type, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Development of IT Infrastructure in the Region; Emergence of Green Data Centers.

6. What are the notable trends driving market growth?

Liquid-based cooling is the fastest growing segment.

7. Are there any restraints impacting market growth?

Costs. Adaptability Requirements. and Power Outages.

8. Can you provide examples of recent developments in the market?

July 2022: During the 2022 China Computing Conference, Chindata Group, in collaboration with their technology research partner Vertiv Technology, unveiled groundbreaking waterless cooling technology known as X-Cooling. This innovation enables data centers to achieve an unprecedented level of efficiency with WUE Zero Cooling, setting a new industry standard. By embracing X-Cooling, data centers can significantly contribute to sustainability efforts, inspiring further advancements in the development of highly efficient data centers.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "China Data Center Cooling Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the China Data Center Cooling Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the China Data Center Cooling Industry?

To stay informed about further developments, trends, and reports in the China Data Center Cooling Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence