Key Insights

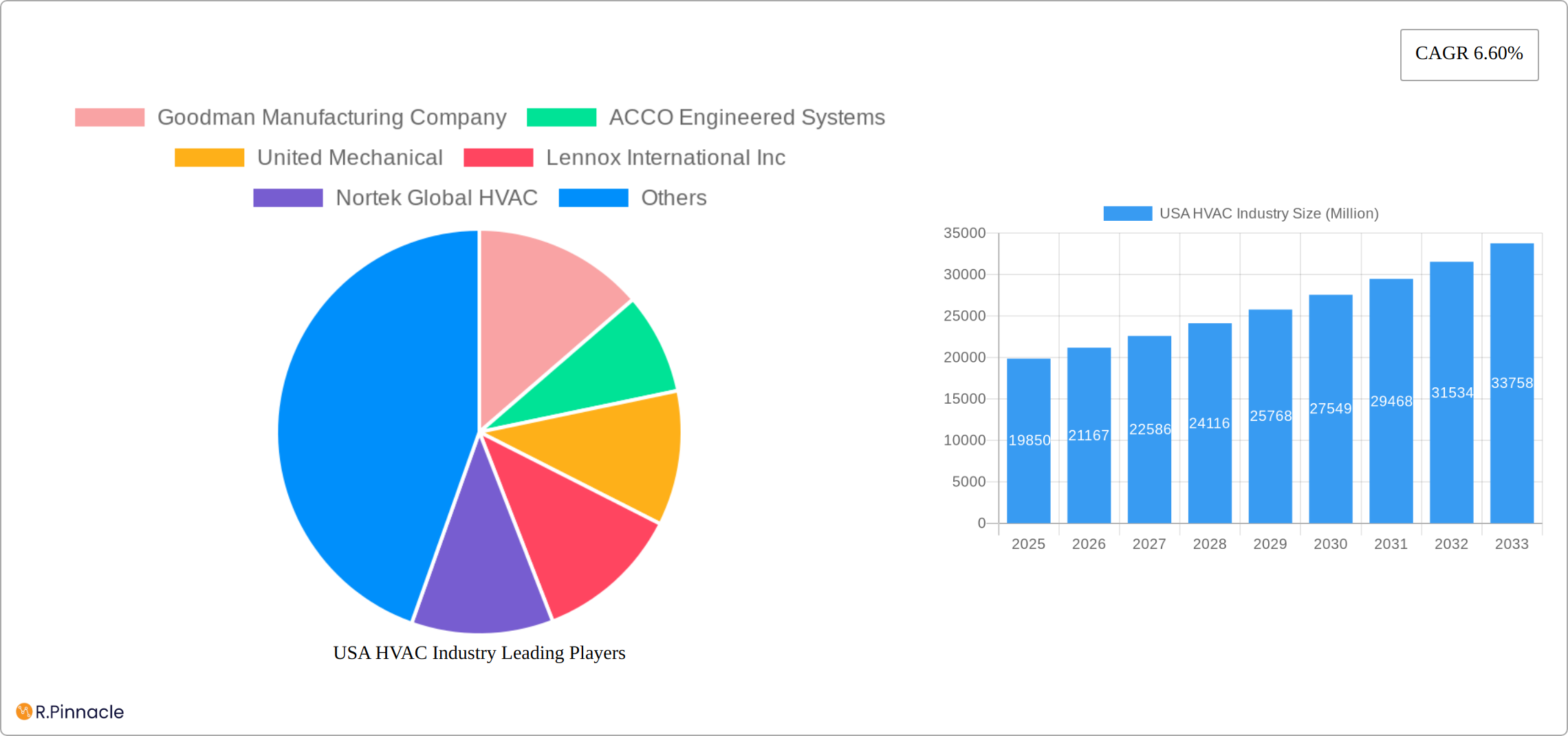

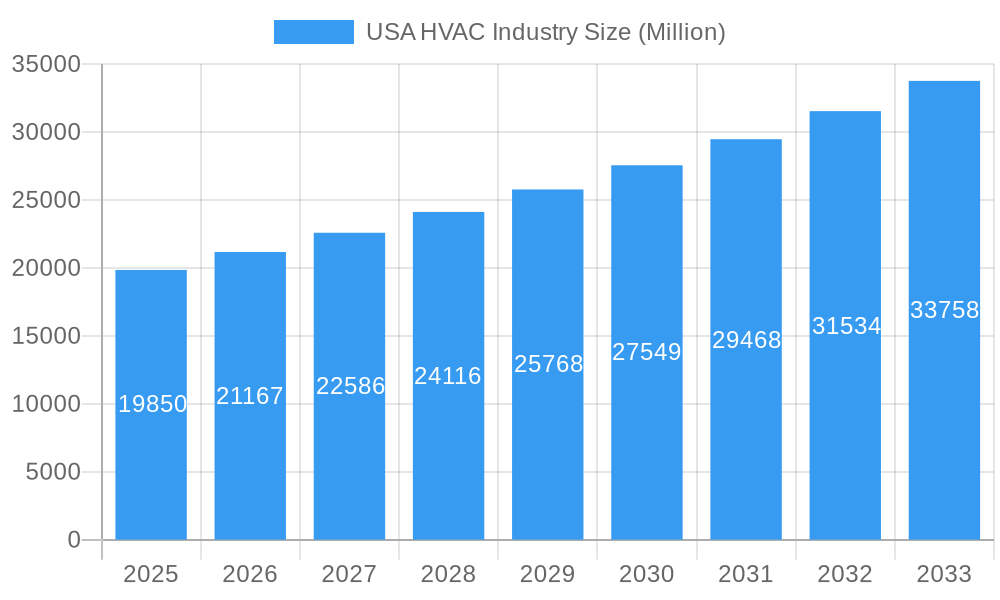

The US HVAC market, valued at $19.85 billion in 2025, is projected to experience robust growth, driven by factors such as increasing urbanization, rising disposable incomes leading to higher spending on home improvements, and stringent government regulations promoting energy efficiency. The strong emphasis on sustainability and reducing carbon emissions is further fueling demand for energy-efficient HVAC systems, particularly in the commercial and industrial sectors. Technological advancements, such as smart thermostats and improved refrigerants, are enhancing system performance and user experience, contributing to market expansion. The market is segmented by end-user (residential, industrial, and commercial) and type (new installations and retrofits), with the residential segment currently dominating due to a large housing stock and consistent demand for replacements and upgrades. Growth in the commercial and industrial segments is anticipated to be faster, driven by expansion of businesses and stricter environmental regulations in these sectors. Retrofits are expected to present significant growth opportunities, particularly as older, inefficient systems are replaced with more sustainable options.

USA HVAC Industry Market Size (In Billion)

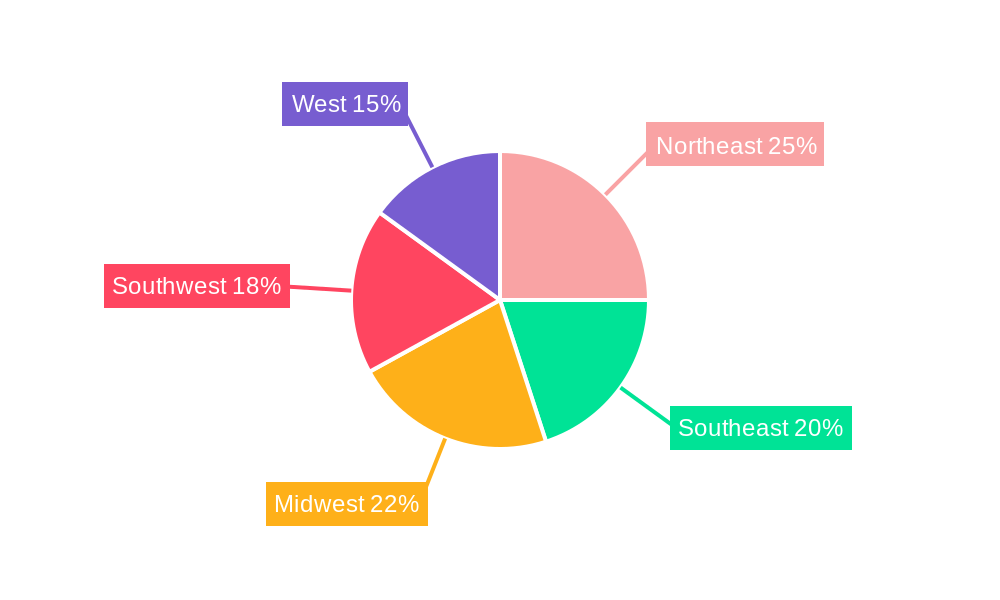

Competition in the US HVAC market is intense, with major players like Goodman Manufacturing Company, Carrier Corporation, and Lennox International Inc. vying for market share through technological innovation, strategic partnerships, and expansion efforts. The Northeast and West regions currently hold larger market shares due to higher population density and building activity. However, growth potential is substantial in the Southwest and Southeast, propelled by population growth and robust construction sectors in those areas. The forecast period (2025-2033) anticipates a continuous expansion of the market, with a compounded annual growth rate (CAGR) of 6.60%, indicating strong future prospects for the industry. This growth trajectory reflects both the inherent need for climate control and the growing adoption of more efficient and technologically advanced HVAC systems.

USA HVAC Industry Company Market Share

USA HVAC Industry Market Report: 2019-2033

This comprehensive report provides an in-depth analysis of the USA HVAC industry, offering valuable insights for industry professionals, investors, and strategic decision-makers. With a study period spanning 2019-2033, a base year of 2025, and a forecast period of 2025-2033, this report delivers a detailed overview of market size (in Millions), growth drivers, challenges, and future opportunities. The report leverages extensive data analysis and expert insights to paint a clear picture of the dynamic USA HVAC landscape. The market is segmented by end-user (Residential, Industrial, Commercial) and by type (New Installations, Retrofits).

USA HVAC Industry Market Structure & Innovation Trends

The USA HVAC market exhibits a moderately concentrated structure, with key players like Carrier Corporation and Lennox International Inc holding significant market share. However, a substantial number of smaller, regional players also contribute to the overall market volume. Innovation is driven by stringent energy efficiency regulations, increasing consumer demand for smart and sustainable HVAC solutions, and advancements in refrigerants and control systems. The regulatory framework, including the EPA's regulations on refrigerants, significantly influences product development and adoption. Product substitutes, such as geothermal systems, are gaining traction, albeit slowly, driven by environmental concerns. The end-user demographic is diversifying, with a growing demand from both residential and commercial sectors. Mergers and acquisitions (M&A) activity has been notable, with deal values exceeding $xx Million in recent years. For example, Marcone's acquisition of Munch in January 2022 significantly strengthened its market position.

- Market Concentration: Moderately concentrated, with major players holding xx% of the market share.

- Innovation Drivers: Stringent energy efficiency regulations, demand for smart HVAC, refrigerant advancements.

- M&A Activity: Significant activity observed, with deal values exceeding $xx Million. Notable examples include Marcone's acquisition of Munch.

- Regulatory Framework: EPA regulations on refrigerants significantly impact product development.

USA HVAC Industry Market Dynamics & Trends

The US HVAC market is poised for substantial growth, projected to achieve a Compound Annual Growth Rate (CAGR) of [Insert Updated CAGR Percentage]% during the forecast period (2025-2033). This expansion is fueled by several key factors: a surging demand for energy-efficient systems, robust construction activity in both residential and commercial sectors, and attractive government incentives promoting energy-conscious upgrades. The integration of smart technologies is revolutionizing the landscape, with advanced connectivity and control features reshaping consumer preferences and driving market demand for smart HVAC systems. While market penetration of smart HVAC systems was estimated at [Insert Updated 2025 Percentage]% in 2025, projections indicate a significant increase to [Insert Updated 2033 Percentage]% by 2033. Competitive pressures remain intense, particularly among smaller players, prompting larger companies to focus on product differentiation through advanced features, comprehensive service packages, and robust warranties. This competitive environment is fostering innovation and driving down prices for consumers. Furthermore, increasing concerns about climate change are pushing the market towards more sustainable solutions.

Dominant Regions & Segments in USA HVAC Industry

The Southern and Western regions of the US are experiencing the most dynamic growth in the HVAC market. This surge is attributable to factors such as rapid population growth, a construction boom, and the critical need for effective climate control in these warmer climates. The Residential segment currently holds the largest market share, followed closely by the Commercial sector. New installations represent the largest segment by type, mirroring the robust construction industry, with retrofits and replacements following closely behind. The increasing demand for energy-efficient solutions is also driving growth in the retrofit segment.

- Key Drivers (Southern & Western Regions): High population growth, booming construction activity, escalating demand for climate control in hot and increasingly arid climates, and rising disposable incomes.

- Dominant Segment (By End User): Residential (with significant growth in multi-family dwellings)

- Dominant Segment (By Type): New Installations (followed by a growing retrofit and replacement market)

USA HVAC Industry Product Innovations

The HVAC industry is witnessing a wave of innovation, driven by the need for improved efficiency, sustainability, and smart home integration. Key advancements include the development of highly efficient heat pumps with improved performance in both heating and cooling modes, sophisticated smart technology for seamless remote control and proactive energy management, and the wider adoption of eco-friendly refrigerants with reduced environmental impact. These innovations directly address growing consumer demand for energy savings, enhanced convenience, and environmentally responsible solutions. Manufacturers are fiercely competing to improve efficiency ratings (SEER and HSPF) and provide user-friendly interfaces and intuitive mobile applications for optimal control and monitoring.

Report Scope & Segmentation Analysis

The report segments the USA HVAC market by end-user (Residential, Commercial, Industrial) and by type (New Installations, Retrofits). The Residential segment is characterized by a high volume of smaller installations, with significant competition among smaller players. The Commercial segment is characterized by larger projects and more complex system designs. The Industrial segment focuses on specialized applications and large scale operations. The new installations segment exhibits stronger growth due to construction activity, while the retrofit segment is driven by upgrades and replacements in existing infrastructure.

Key Drivers of USA HVAC Industry Growth

The growth trajectory of the US HVAC industry is propelled by several interconnected factors: increased construction activity in both residential and commercial sectors, heightened awareness of energy efficiency and its economic benefits, substantial government incentives encouraging the adoption of energy-efficient HVAC systems, rapid technological advancements (including smart HVAC systems and improved refrigerants), and the escalating impact of climate change demanding more sophisticated heating and cooling solutions. The aging housing stock in many regions is also contributing to replacement demand.

Challenges in the USA HVAC Industry Sector

Despite the promising outlook, the US HVAC industry faces several significant challenges. Fluctuations in raw material prices, persistent supply chain disruptions impacting component availability, intense competition among manufacturers, a shortage of skilled labor, and increasingly stringent environmental regulations all pose considerable obstacles. These factors can significantly impact production costs and profitability, with estimated annual losses of [Insert Updated Loss Amount] million attributed to supply chain issues alone. Furthermore, navigating complex regulatory landscapes and ensuring compliance with evolving environmental standards adds another layer of complexity.

Emerging Opportunities in USA HVAC Industry

Emerging opportunities include the growth of smart home integration, increasing demand for energy-efficient solutions, expanding adoption of heat pumps and geothermal systems, and the development of specialized HVAC systems for data centers and other specialized applications.

Leading Players in the USA HVAC Industry Market

- Goodman Manufacturing Company

- ACCO Engineered Systems

- United Mechanical

- Lennox International Inc

- Nortek Global HVAC

- EMCOR Services

- Carrier Corporation

- Southland Industrial Energy

- National HVAC Services

- J&J Air Conditioning Services

Key Developments in USA HVAC Industry

- May 2022: NearU Services partnered with Bullman Heating and Air and Mountain Air Mechanical Contractors, expanding service capabilities in Asheville, NC.

- January 2022: Marcone acquired Munch, strengthening its position as a leading HVAC parts distributor.

Future Outlook for USA HVAC Industry Market

The USA HVAC market is poised for continued growth, driven by ongoing construction, increasing demand for energy-efficient and smart systems, and supportive government policies. Strategic opportunities lie in innovation, expansion into underserved markets, and the development of sustainable and cost-effective solutions. The market is expected to reach $xx Million by 2033.

USA HVAC Industry Segmentation

-

1. End User

- 1.1. Residential

- 1.2. Industrial and Commercial

-

2. Type

- 2.1. New Installations

- 2.2. Retrofits

USA HVAC Industry Segmentation By Geography

- 1. United States

USA HVAC Industry Regional Market Share

Geographic Coverage of USA HVAC Industry

USA HVAC Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.60% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Growth in Construction Activity; Higher Awareness on Energy Awareness Systems; Large Installed Base of HVAC Equipment in the Country

- 3.3. Market Restrains

- 3.3.1. Stringent Regulations in the Middle East Have Been a Challenge for Vendors; Traditional Forms of Advertising Continue to Dominate in a Few Countries

- 3.4. Market Trends

- 3.4.1. Industrial and Commercial Segment to Grow Significantly

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. USA HVAC Industry Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by End User

- 5.1.1. Residential

- 5.1.2. Industrial and Commercial

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. New Installations

- 5.2.2. Retrofits

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. United States

- 5.1. Market Analysis, Insights and Forecast - by End User

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2025

- 6.2. Company Profiles

- 6.2.1 Goodman Manufacturing Company

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 ACCO Engineered Systems

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 United Mechanical

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Lennox International Inc

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 Nortek Global HVAC

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 EMCOR Services

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 Carrier Corporation

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 Southland Industrial Energy

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 National HVAC Services

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 J&J Air Conditioning Services

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.1 Goodman Manufacturing Company

List of Figures

- Figure 1: USA HVAC Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: USA HVAC Industry Share (%) by Company 2025

List of Tables

- Table 1: USA HVAC Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 2: USA HVAC Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 3: USA HVAC Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: USA HVAC Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 5: USA HVAC Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 6: USA HVAC Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the USA HVAC Industry?

The projected CAGR is approximately 6.60%.

2. Which companies are prominent players in the USA HVAC Industry?

Key companies in the market include Goodman Manufacturing Company, ACCO Engineered Systems, United Mechanical, Lennox International Inc, Nortek Global HVAC, EMCOR Services, Carrier Corporation, Southland Industrial Energy, National HVAC Services, J&J Air Conditioning Services.

3. What are the main segments of the USA HVAC Industry?

The market segments include End User, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 19.85 Million as of 2022.

5. What are some drivers contributing to market growth?

Growth in Construction Activity; Higher Awareness on Energy Awareness Systems; Large Installed Base of HVAC Equipment in the Country.

6. What are the notable trends driving market growth?

Industrial and Commercial Segment to Grow Significantly.

7. Are there any restraints impacting market growth?

Stringent Regulations in the Middle East Have Been a Challenge for Vendors; Traditional Forms of Advertising Continue to Dominate in a Few Countries.

8. Can you provide examples of recent developments in the market?

May 2022: NearU Services announced its partnership with Bullman Heating and Air, an HVAC service provider in North Carolina. The collaboration with Bullman and NearU's May partnership with Mountain Air Mechanical Contractors will boost NearU's service capabilities in the rapidly-growing Asheville area.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "USA HVAC Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the USA HVAC Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the USA HVAC Industry?

To stay informed about further developments, trends, and reports in the USA HVAC Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence