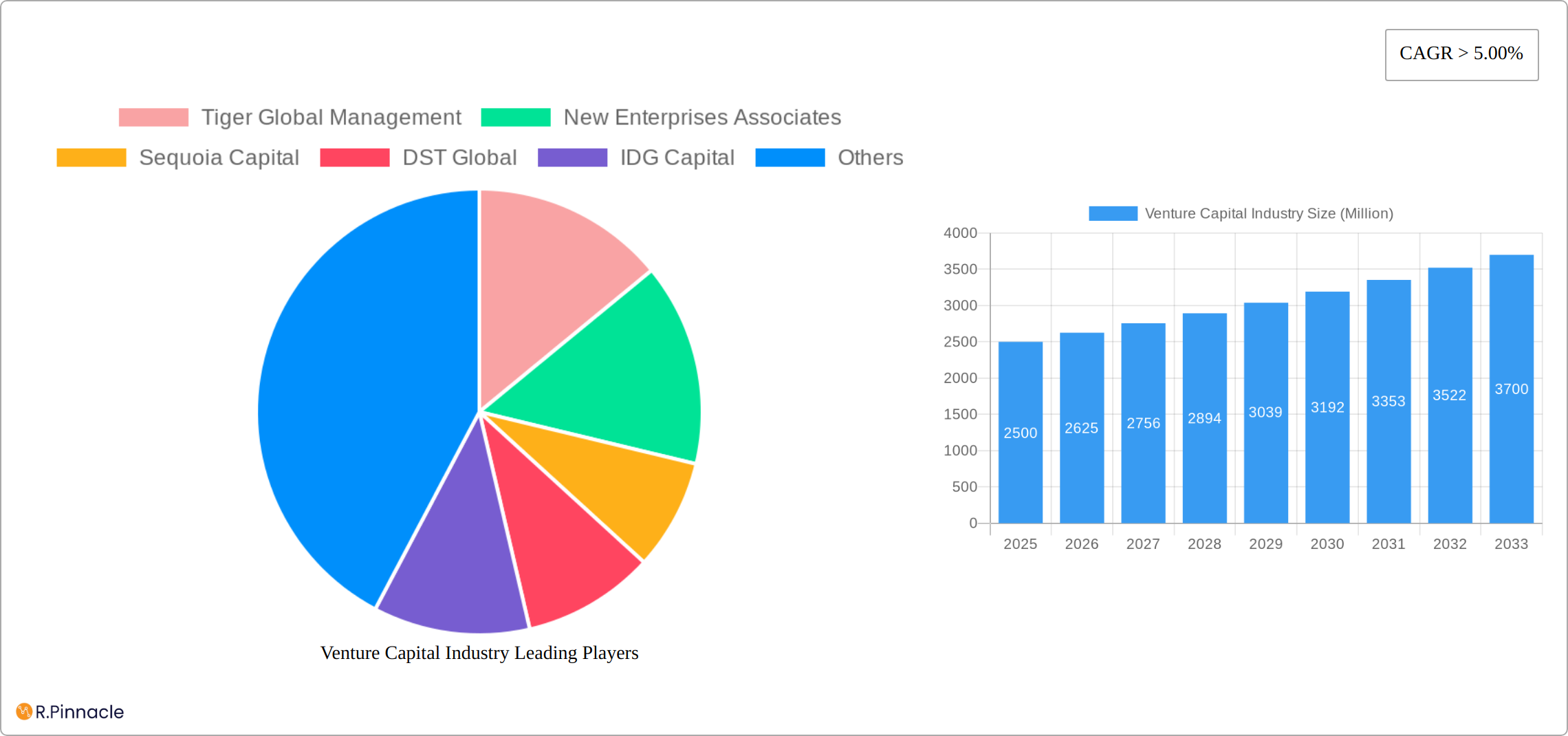

Key Insights

The venture capital (VC) industry is experiencing robust growth, fueled by a confluence of factors. A compound annual growth rate (CAGR) exceeding 5% suggests a consistently expanding market, projected to reach significant valuations within the forecast period (2025-2033). This expansion is driven by several key trends: the increasing number of high-growth startups across diverse sectors (technology, healthcare, and others), a rise in the availability of capital from both traditional VC firms and alternative sources like corporate venture capital, and a growing appetite for high-risk, high-reward investments. The presence of prominent firms like Tiger Global Management, Sequoia Capital, and DST Global underscores the industry's maturity and competitiveness. While challenges exist, such as economic downturns that can impact investment cycles and the inherent risks associated with early-stage investments, the overall market outlook remains positive, particularly given ongoing innovation and the constant emergence of disruptive technologies.

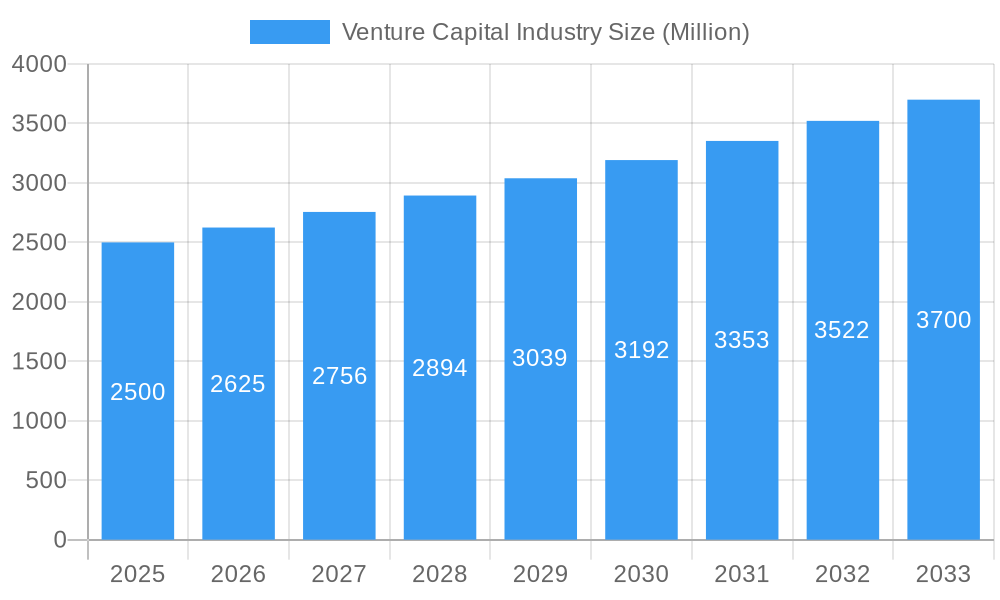

Venture Capital Industry Market Size (In Billion)

Further analysis reveals that the segmentation within the VC industry (although not detailed in the provided data) likely includes distinctions based on investment stage (seed, Series A, etc.), industry focus, and geographical region. The geographic distribution of investments will vary, with North America and Europe likely commanding significant shares, reflecting established ecosystems and investor activity. However, emerging markets are also witnessing increasing VC activity, further contributing to the overall market expansion. While precise market size figures are not provided, a CAGR of over 5% applied to a base year 2025 value, even with a conservative estimate, points towards substantial market expansion throughout the forecast period. The industry's continued success hinges upon maintaining access to capital, fostering innovation, and adapting to evolving economic and technological landscapes.

Venture Capital Industry Company Market Share

Venture Capital Industry: A Comprehensive Market Report (2019-2033)

This comprehensive report provides an in-depth analysis of the Venture Capital (VC) industry, offering actionable insights for investors, entrepreneurs, and industry professionals. With a study period spanning 2019-2033, a base year of 2025, and an estimated and forecast period of 2025-2033, this report leverages historical data (2019-2024) to project future trends and opportunities within this dynamic market. The report covers key players like Tiger Global Management, New Enterprises Associates, Sequoia Capital, DST Global, IDG Capital, Index Ventures, Healthcare Royalty Partners, GGV Capital, Nanjing Zijin Investment, and Greylock Partners (list not exhaustive), analyzing market dynamics and future potential. Projected market values are in Millions of USD.

Venture Capital Industry Market Structure & Innovation Trends

This section delves into the dynamic landscape of the venture capital (VC) industry, analyzing market concentration, key innovation drivers, regulatory influences, and the impact of mergers and acquisitions (M&A) activity. We examine the market share distribution among leading players and assess the financial value of significant M&A transactions. The competitive environment is notably fragmented, featuring a few dominant firms alongside numerous smaller players vying for investment opportunities. The industry's growth is fueled by significant innovation spurred by rapid technological advancements and the evolving preferences of investors. Regulatory frameworks vary substantially across different regions, directly affecting investment strategies and the overall deal flow.

- Market Concentration: While precise figures fluctuate, a small number of leading firms exert considerable influence over the global VC market. Ongoing consolidation is anticipated, suggesting further concentration in the coming years. Detailed market share data requires further investigation and will be updated as data becomes available.

- Innovation Drivers: Transformative technologies such as artificial intelligence (AI), blockchain technology, and the increasing focus on sustainable and impact investing are reshaping investment strategies and portfolio composition within the VC industry. These drivers are attracting significant capital and fostering the development of new technologies and business models.

- Regulatory Frameworks: The diverse regulatory landscape across various jurisdictions presents both challenges and opportunities. Understanding and navigating these varying rules and regulations is crucial for effective deal structuring and ensuring regulatory compliance. This complexity necessitates a sophisticated approach to international investment.

- Product Substitutes: Alternative funding sources, including crowdfunding and angel investing, provide complementary financing options. However, these alternatives have not yet significantly eroded the dominance of traditional VC firms, which continue to play a crucial role in funding high-growth startups.

- End-User Demographics: The primary end-users are high-growth startups across a range of sectors. However, there's a notable and growing emphasis on technology, healthcare, and renewable energy, reflecting broader societal priorities and technological advancements.

- M&A Activities: The annual value of M&A transactions within the VC industry exhibits considerable variation. While precise figures for past averages and future projections require further research and data analysis, the trend indicates potential for increased activity in the coming years driven by industry consolidation and strategic acquisitions.

Venture Capital Industry Market Dynamics & Trends

This section delves into the market growth drivers, technological disruptions, consumer preferences, and competitive dynamics within the VC industry. We examine the Compound Annual Growth Rate (CAGR) and market penetration across various segments.

The VC market is experiencing rapid growth, fueled by factors such as increased availability of capital, a rise in high-growth startups, and the continuous evolution of technology. Technological disruptions, such as artificial intelligence and blockchain, are reshaping the investment landscape, creating both challenges and opportunities for traditional VC firms. Investor preferences are shifting towards sustainable and impact investing, driving the growth of environmentally and socially responsible ventures. Competitive dynamics are intensifying, with increasing competition from both established players and new entrants. We project a CAGR of xx% for the global VC market during the forecast period, with market penetration expected to reach xx% by 2033.

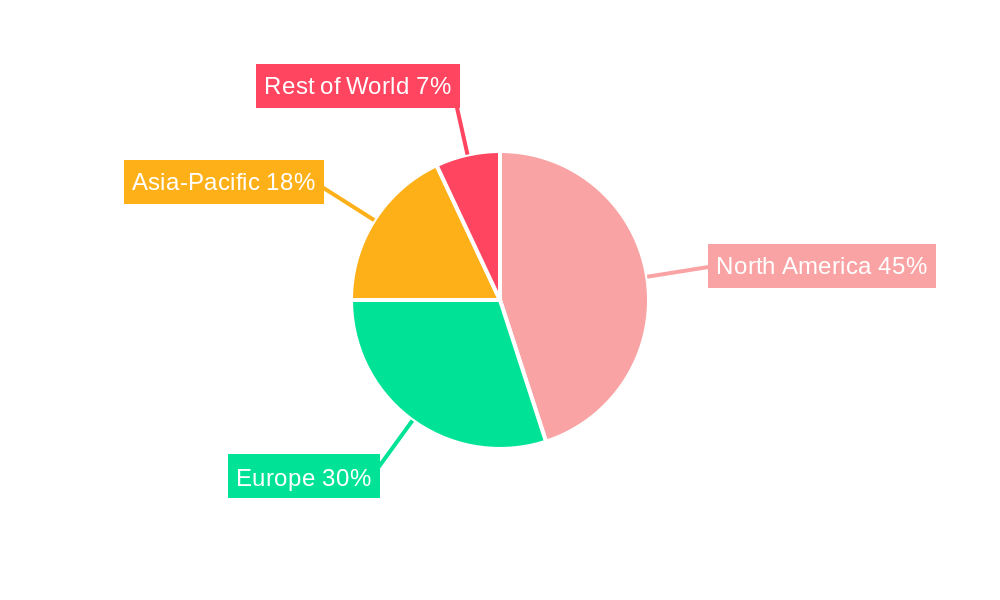

Dominant Regions & Segments in Venture Capital Industry

This section identifies the leading regions and segments within the VC industry. Key drivers for dominance are analyzed using bullet points, while in-depth analysis is provided in paragraph form.

The Americas (primarily the US) and Asia (particularly China) have emerged as dominant regions, attracting significant investment. Europe is also witnessing substantial growth. Within these regions, the technology sector consistently attracts the largest share of VC funding.

- Key Drivers for the Americas: Strong entrepreneurial ecosystem, access to capital, favorable regulatory environment, and a mature technology industry.

- Key Drivers for Asia: Rapid economic growth, increasing government support, a large pool of talented entrepreneurs, and a growing middle class.

- Key Drivers for Europe: A supportive regulatory environment, growing technological capabilities, and increased cross-border investment.

Venture Capital Industry Product Innovations

This section summarizes product developments, applications, and competitive advantages, highlighting technological trends and market fit. The VC industry itself doesn't produce a tangible "product," but rather provides funding and expertise to startups. Recent innovation focuses on improved due diligence processes, the use of AI-powered investment tools, and the expansion into new asset classes like cryptocurrencies and NFTs. These innovations enhance efficiency, risk assessment, and investment returns, fostering a competitive advantage for firms adopting them.

Report Scope & Segmentation Analysis

This section details the market segmentations including growth projections, market sizes, and competitive dynamics. The report segments the market by geography (North America, Europe, Asia-Pacific, Rest of the World), investment stage (seed, early-stage, late-stage), and industry sector (technology, healthcare, consumer goods, etc.). Growth projections are provided for each segment, along with an analysis of market size and competitive landscape. For instance, the technology sector is expected to maintain the largest market share throughout the forecast period, while the healthcare sector is poised for substantial growth due to increasing demand for innovative medical solutions.

Key Drivers of Venture Capital Industry Growth

This section outlines the key drivers of the VC industry's growth, focusing on technological, economic, and regulatory factors. Technological advancements continuously create new investment opportunities and enhance operational efficiency. Strong economic growth fuels entrepreneurial activity and attracts increased investments. Supportive regulatory environments, though varying regionally, encourage investment and innovation.

Challenges in the Venture Capital Industry Sector

This section addresses barriers and restraints in the VC industry, such as regulatory hurdles, supply chain issues (less directly relevant but impacting portfolio companies), and intensifying competitive pressures. The impact of these challenges on investment decisions and returns is quantified wherever possible.

Emerging Opportunities in Venture Capital Industry

This section highlights promising trends and opportunities, encompassing new markets, disruptive technologies, and evolving consumer preferences. The increasing prominence of impact investing, the expansion into alternative asset classes (such as cryptocurrencies), and the exploration of new geographic markets present significant opportunities for agile VC firms willing to embrace innovation and adapt to a dynamic global landscape. This includes focusing on sectors such as fintech, biotech, and sustainable technologies, which are experiencing rapid growth and attracting significant investor interest.

Leading Players in the Venture Capital Industry Market

Key Developments in Venture Capital Industry

- 2020 Q4: The Americas dominated VC investment, with the US accounting for a significant portion of the total. Europe also witnessed substantial investment activity, highlighting the global reach of the VC industry.

- 2022: IDG Capital Vietnam's investment in METAIN exemplifies the growing interest in blockchain and NFT technologies within the VC industry, showcasing how emerging trends are shaping investment decisions.

- Ongoing Developments: [Add other significant key developments and quantify where possible, e.g., mention specific funding rounds for prominent startups, shifts in investment focus by major players, or significant regulatory changes. ]

Future Outlook for Venture Capital Industry Market

The future of the VC industry remains dynamic and promising. Continued technological innovation, the expansion into new global markets, and a growing emphasis on sustainable and impact investments are key drivers of growth. Success in the coming years will depend on strategic partnerships, the diversification of investment strategies, and the ability to adapt to the ever-evolving regulatory landscape. Favorable economic conditions in key regions, coupled with the emergence of innovative startups and increasing venture capital funding, are expected to fuel continued market expansion. However, economic downturns and shifts in investor sentiment represent significant potential risks.

Venture Capital Industry Segmentation

-

1. Type

- 1.1. Local Investors

- 1.2. International Investors

-

2. Industry

- 2.1. Real Estate

- 2.2. Financial Services

- 2.3. Food & Beverages

- 2.4. Healthcare

- 2.5. Transport & Logistics

- 2.6. IT & ITeS

- 2.7. Education

- 2.8. Other Industries

Venture Capital Industry Segmentation By Geography

- 1. North America

- 2. Latin America

- 3. Europe

- 4. Asia Pacific

- 5. Middle East and Africa

Venture Capital Industry Regional Market Share

Geographic Coverage of Venture Capital Industry

Venture Capital Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 16.68% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. PRI Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Local Investors

- 5.1.2. International Investors

- 5.2. Market Analysis, Insights and Forecast - by Industry

- 5.2.1. Real Estate

- 5.2.2. Financial Services

- 5.2.3. Food & Beverages

- 5.2.4. Healthcare

- 5.2.5. Transport & Logistics

- 5.2.6. IT & ITeS

- 5.2.7. Education

- 5.2.8. Other Industries

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Latin America

- 5.3.3. Europe

- 5.3.4. Asia Pacific

- 5.3.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Global Venture Capital Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Local Investors

- 6.1.2. International Investors

- 6.2. Market Analysis, Insights and Forecast - by Industry

- 6.2.1. Real Estate

- 6.2.2. Financial Services

- 6.2.3. Food & Beverages

- 6.2.4. Healthcare

- 6.2.5. Transport & Logistics

- 6.2.6. IT & ITeS

- 6.2.7. Education

- 6.2.8. Other Industries

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. North America Venture Capital Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Local Investors

- 7.1.2. International Investors

- 7.2. Market Analysis, Insights and Forecast - by Industry

- 7.2.1. Real Estate

- 7.2.2. Financial Services

- 7.2.3. Food & Beverages

- 7.2.4. Healthcare

- 7.2.5. Transport & Logistics

- 7.2.6. IT & ITeS

- 7.2.7. Education

- 7.2.8. Other Industries

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Latin America Venture Capital Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Local Investors

- 8.1.2. International Investors

- 8.2. Market Analysis, Insights and Forecast - by Industry

- 8.2.1. Real Estate

- 8.2.2. Financial Services

- 8.2.3. Food & Beverages

- 8.2.4. Healthcare

- 8.2.5. Transport & Logistics

- 8.2.6. IT & ITeS

- 8.2.7. Education

- 8.2.8. Other Industries

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Europe Venture Capital Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Local Investors

- 9.1.2. International Investors

- 9.2. Market Analysis, Insights and Forecast - by Industry

- 9.2.1. Real Estate

- 9.2.2. Financial Services

- 9.2.3. Food & Beverages

- 9.2.4. Healthcare

- 9.2.5. Transport & Logistics

- 9.2.6. IT & ITeS

- 9.2.7. Education

- 9.2.8. Other Industries

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Asia Pacific Venture Capital Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Local Investors

- 10.1.2. International Investors

- 10.2. Market Analysis, Insights and Forecast - by Industry

- 10.2.1. Real Estate

- 10.2.2. Financial Services

- 10.2.3. Food & Beverages

- 10.2.4. Healthcare

- 10.2.5. Transport & Logistics

- 10.2.6. IT & ITeS

- 10.2.7. Education

- 10.2.8. Other Industries

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Middle East and Africa Venture Capital Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Type

- 11.1.1. Local Investors

- 11.1.2. International Investors

- 11.2. Market Analysis, Insights and Forecast - by Industry

- 11.2.1. Real Estate

- 11.2.2. Financial Services

- 11.2.3. Food & Beverages

- 11.2.4. Healthcare

- 11.2.5. Transport & Logistics

- 11.2.6. IT & ITeS

- 11.2.7. Education

- 11.2.8. Other Industries

- 11.1. Market Analysis, Insights and Forecast - by Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Tiger Global Management

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 New Enterprises Associates

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Sequoia Capital

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 DST Global

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 IDG Capital

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Index Ventures

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Healthcare Royalty Partners

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 GGV Capital

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Nanjing Zijin Investment

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Greylock Partners**List Not Exhaustive

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Tiger Global Management

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Venture Capital Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Venture Capital Industry Revenue (billion), by Type 2025 & 2033

- Figure 3: North America Venture Capital Industry Revenue Share (%), by Type 2025 & 2033

- Figure 4: North America Venture Capital Industry Revenue (billion), by Industry 2025 & 2033

- Figure 5: North America Venture Capital Industry Revenue Share (%), by Industry 2025 & 2033

- Figure 6: North America Venture Capital Industry Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Venture Capital Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: Latin America Venture Capital Industry Revenue (billion), by Type 2025 & 2033

- Figure 9: Latin America Venture Capital Industry Revenue Share (%), by Type 2025 & 2033

- Figure 10: Latin America Venture Capital Industry Revenue (billion), by Industry 2025 & 2033

- Figure 11: Latin America Venture Capital Industry Revenue Share (%), by Industry 2025 & 2033

- Figure 12: Latin America Venture Capital Industry Revenue (billion), by Country 2025 & 2033

- Figure 13: Latin America Venture Capital Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Venture Capital Industry Revenue (billion), by Type 2025 & 2033

- Figure 15: Europe Venture Capital Industry Revenue Share (%), by Type 2025 & 2033

- Figure 16: Europe Venture Capital Industry Revenue (billion), by Industry 2025 & 2033

- Figure 17: Europe Venture Capital Industry Revenue Share (%), by Industry 2025 & 2033

- Figure 18: Europe Venture Capital Industry Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Venture Capital Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Asia Pacific Venture Capital Industry Revenue (billion), by Type 2025 & 2033

- Figure 21: Asia Pacific Venture Capital Industry Revenue Share (%), by Type 2025 & 2033

- Figure 22: Asia Pacific Venture Capital Industry Revenue (billion), by Industry 2025 & 2033

- Figure 23: Asia Pacific Venture Capital Industry Revenue Share (%), by Industry 2025 & 2033

- Figure 24: Asia Pacific Venture Capital Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: Asia Pacific Venture Capital Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Middle East and Africa Venture Capital Industry Revenue (billion), by Type 2025 & 2033

- Figure 27: Middle East and Africa Venture Capital Industry Revenue Share (%), by Type 2025 & 2033

- Figure 28: Middle East and Africa Venture Capital Industry Revenue (billion), by Industry 2025 & 2033

- Figure 29: Middle East and Africa Venture Capital Industry Revenue Share (%), by Industry 2025 & 2033

- Figure 30: Middle East and Africa Venture Capital Industry Revenue (billion), by Country 2025 & 2033

- Figure 31: Middle East and Africa Venture Capital Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Venture Capital Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 2: Global Venture Capital Industry Revenue billion Forecast, by Industry 2020 & 2033

- Table 3: Global Venture Capital Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Venture Capital Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 5: Global Venture Capital Industry Revenue billion Forecast, by Industry 2020 & 2033

- Table 6: Global Venture Capital Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: Global Venture Capital Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 8: Global Venture Capital Industry Revenue billion Forecast, by Industry 2020 & 2033

- Table 9: Global Venture Capital Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 10: Global Venture Capital Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 11: Global Venture Capital Industry Revenue billion Forecast, by Industry 2020 & 2033

- Table 12: Global Venture Capital Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Global Venture Capital Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 14: Global Venture Capital Industry Revenue billion Forecast, by Industry 2020 & 2033

- Table 15: Global Venture Capital Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 16: Global Venture Capital Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 17: Global Venture Capital Industry Revenue billion Forecast, by Industry 2020 & 2033

- Table 18: Global Venture Capital Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Venture Capital Industry?

The projected CAGR is approximately 16.68%.

2. Which companies are prominent players in the Venture Capital Industry?

Key companies in the market include Tiger Global Management, New Enterprises Associates, Sequoia Capital, DST Global, IDG Capital, Index Ventures, Healthcare Royalty Partners, GGV Capital, Nanjing Zijin Investment, Greylock Partners**List Not Exhaustive.

3. What are the main segments of the Venture Capital Industry?

The market segments include Type, Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 396.7 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

Distribution of Start-Ups Witnessing Venture Capital Industry Globally.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

In 2022, IDG Capital Vietnam Confirms Investment in METAIN to Lead NFT-Empowered Real Estate Trend in Vietnam. IDG Capital also shows its ambition to lead the NFT Real estate trend and reveals its plan to proactively engage with global investors to attract investment into the Vietnam real estate market. With the high security, instantaneous settlement, transparent, seamless transaction process, blockchain, smart contract, and NFT (Non-fungible token) technology is transforming the real estate industry and will become the key trend in the next decades.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Venture Capital Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Venture Capital Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Venture Capital Industry?

To stay informed about further developments, trends, and reports in the Venture Capital Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence