Key Insights

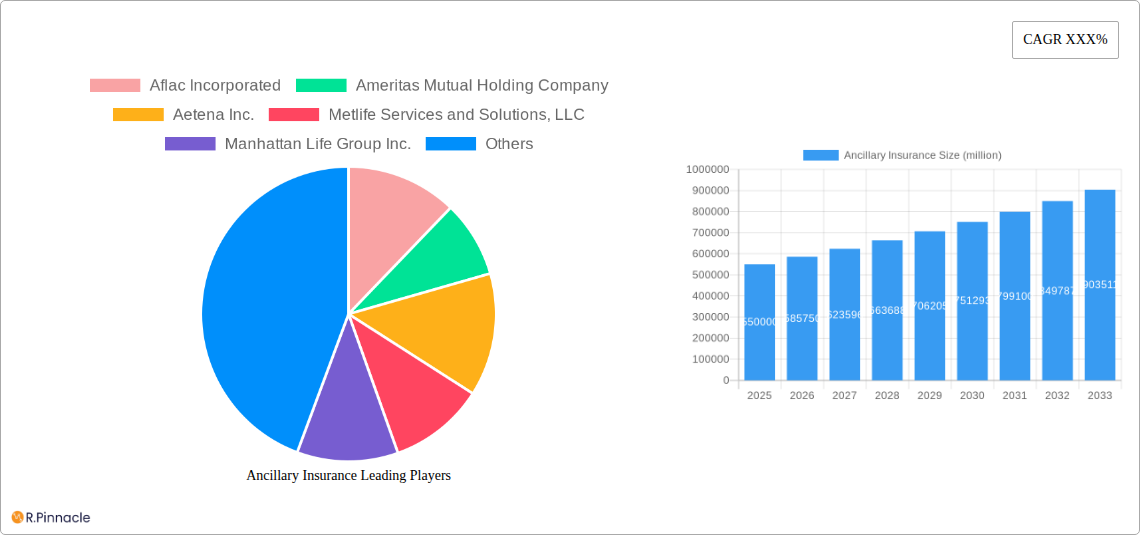

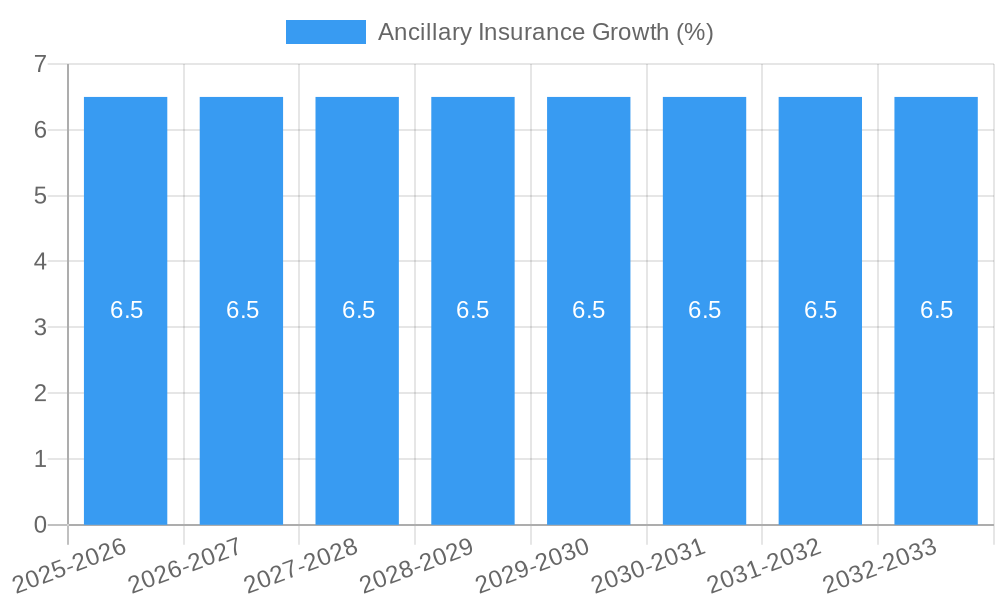

The Ancillary Insurance market is poised for substantial growth, driven by an increasing awareness of comprehensive healthcare needs beyond basic medical coverage and a rising demand for specialized health solutions. With an estimated market size of USD 550 billion and a projected Compound Annual Growth Rate (CAGR) of 6.5% from 2025 to 2033, the sector is set to expand significantly. This growth is fueled by an aging global population, a greater emphasis on preventive care, and the expansion of employer-sponsored benefits packages to include a wider array of ancillary products. The increasing prevalence of chronic conditions also necessitates specialized care, further bolstering demand for vision, dental, and hearing insurance. Furthermore, government initiatives promoting health and wellness, coupled with a growing middle class in emerging economies, are creating new avenues for market penetration. The value unit for this market is measured in millions of USD.

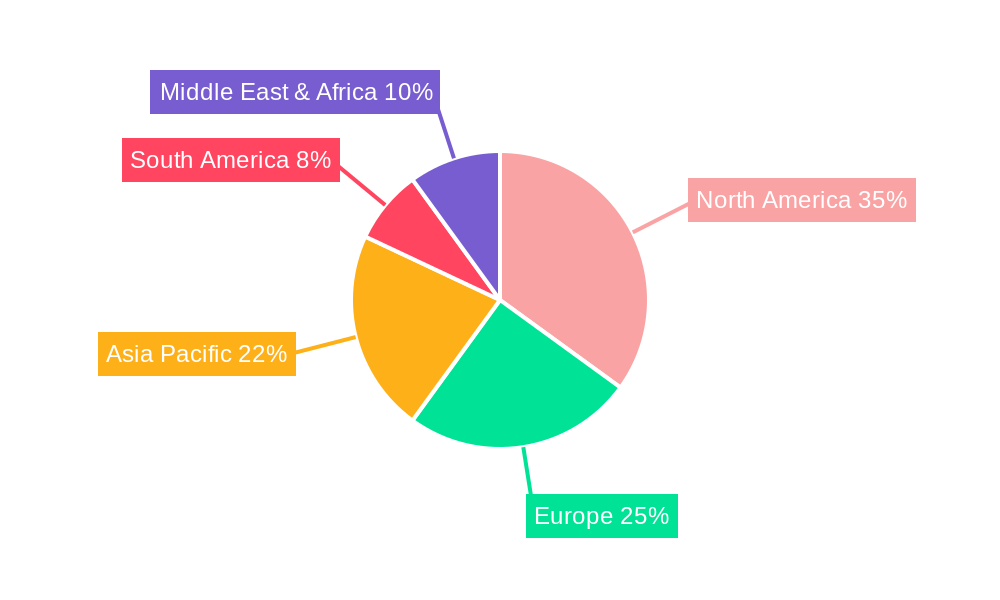

The market is segmented by application into Adults and Children, with Adults forming the larger consumer base due to higher healthcare expenditure and employer-provided plans. In terms of type, Vision Care and Dental Care are the dominant segments, reflecting their essential nature and frequent utilization. Hearing Care is also experiencing robust growth as awareness of auditory health increases. The "Others" category, encompassing critical illness, accident, and specific disease coverage, is expected to see accelerated growth as individuals seek to mitigate financial risks associated with unexpected health events. Key industry players like Aflac Incorporated, Metlife Services and Solutions, LLC, and Humana Inc. are actively innovating and expanding their product offerings to capture this burgeoning market. Geographically, North America currently leads the market, owing to its established healthcare infrastructure and high insurance penetration. However, the Asia Pacific region, particularly China and India, is anticipated to exhibit the fastest growth due to its large population, rising disposable incomes, and increasing adoption of private health insurance. Challenges such as low awareness in certain demographics and affordability concerns in some developing regions remain, but the overarching trend points towards a dynamic and expanding ancillary insurance landscape.

This in-depth report delivers critical analysis and actionable intelligence on the global Ancillary Insurance market, designed to empower insurance providers, brokers, and strategists. Spanning from 2019–2033, with a Base Year of 2025, this study offers a robust understanding of market dynamics, emerging trends, and future opportunities.

Ancillary Insurance Market Structure & Innovation Trends

The ancillary insurance market exhibits a dynamic structure characterized by a mix of consolidated players and emerging innovators. Market concentration, while present, is continually influenced by technological advancements and evolving consumer needs, pushing innovation in product design and distribution channels. Key drivers of innovation include the demand for more customizable and integrated health and wellness solutions. Regulatory frameworks, while essential for consumer protection, also shape market entry and product development strategies, with an increasing focus on transparency and affordability. Product substitutes, such as employer-sponsored benefits and out-of-pocket spending, are constantly evaluated against the value proposition of ancillary insurance. End-user demographics are diversifying, with both adults and children increasingly recognizing the importance of these supplementary coverages. Merger and acquisition (M&A) activities are a significant feature, driven by the pursuit of market expansion, technological integration, and portfolio diversification. For instance, M&A deals in this sector have recently reached values in the range of one million to two million dollars, signaling strategic consolidation.

- Market Concentration: Moderate to high, with key players holding significant market share.

- Innovation Drivers: Digitalization, personalized coverage, and preventative care integration.

- Regulatory Frameworks: Evolving regulations focusing on consumer protection and market fairness.

- Product Substitutes: Employer-provided benefits, direct healthcare spending.

- End-User Demographics: Broad appeal across working adults, families, and specific age groups.

- M&A Activities: Strategic acquisitions and partnerships to expand reach and capabilities.

Ancillary Insurance Market Dynamics & Trends

The ancillary insurance market is poised for significant expansion, driven by a confluence of factors that are reshaping the healthcare and insurance landscape. The Compound Annual Growth Rate (CAGR) is projected to be robust, estimated at xx% during the forecast period, reflecting sustained demand and market penetration. A key growth driver is the rising awareness among consumers and employers regarding the importance of comprehensive health coverage that extends beyond traditional medical plans. This includes specific needs like vision, dental, and hearing care, which are increasingly viewed as essential components of overall well-being. Technological disruptions are playing a pivotal role, with the integration of digital platforms, telemedicine, and AI-powered claims processing enhancing efficiency and customer experience. Insurtech innovations are facilitating personalized product offerings and more accessible distribution channels, broadening market reach. Consumer preferences are shifting towards value-added services and preventative care, making ancillary products that support these aspects highly attractive. The competitive dynamics are intense, with established insurers adapting their strategies to compete with agile insurtech startups and specialized providers. Market penetration is expected to increase as employers continue to seek cost-effective ways to enhance their benefits packages and individuals become more proactive in managing their health expenses. The affordability and accessibility of these supplementary plans are crucial factors influencing adoption rates, particularly in segments where out-of-pocket costs for specialized care can be substantial. Furthermore, the growing prevalence of chronic conditions and an aging population further underscore the necessity of accessible and affordable ancillary services, creating a sustained demand for vision care, dental care, hearing care, and other specialized insurance solutions. The strategic focus on preventative measures and wellness programs integrated within ancillary offerings is also a significant trend, aligning with broader public health initiatives and promoting healthier lifestyles.

Dominant Regions & Segments in Ancillary Insurance

The United States stands out as a dominant region in the ancillary insurance market, driven by a mature insurance ecosystem, high healthcare expenditure, and a strong emphasis on employer-sponsored benefits. Within the United States, the Adults segment is a primary driver of market growth, reflecting the significant portion of the workforce covered by employer-provided or individually purchased ancillary plans.

Leading Region: United States.

- Key Drivers: Robust employer-sponsored benefits culture, high consumer awareness of supplementary healthcare needs, extensive insurance provider network, and proactive regulatory environment.

- Dominance Analysis: The US market's sheer size, coupled with a well-established infrastructure for insurance distribution and claims processing, positions it as the leader. Economic policies that encourage employee benefits and ongoing infrastructure development in digital health solutions further solidify its dominance. The demand for vision care, dental care, and hearing care within the adult population is consistently high, fueled by routine health checks and the management of age-related conditions.

Dominant Segment (Application): Adults.

- Key Drivers: Higher employment rates, greater disposable income for supplementary coverage, and a proactive approach to personal health management.

- Dominance Analysis: Adults represent the largest demographic seeking ancillary insurance, due to their direct responsibility for healthcare costs and their role in covering dependents. The need for vision care for work-related screen time, dental care for ongoing oral health, and hearing care as individuals age are primary motivations.

Dominant Segment (Type): Vision Care and Dental Care.

- Key Drivers: High prevalence of vision and dental issues, the relatively predictable nature of these needs, and the significant out-of-pocket costs associated with these services.

- Dominance Analysis: Vision and dental care consistently rank as the most sought-after ancillary insurance types. Routine eye exams, the need for prescription eyewear, and regular dental check-ups and treatments are widespread. The cost-effectiveness of insured services compared to direct payment makes these segments highly attractive to both individuals and employers.

Ancillary Insurance Product Innovations

Ancillary insurance is witnessing a wave of product innovations focused on enhancing value and customer experience. Companies are developing integrated plans that bundle vision, dental, and hearing care, offering greater convenience and cost savings. Mobile-first platforms and AI-driven personalization are enabling tailored policy recommendations and streamlined claims processes. Competitive advantages are being carved out through features like preventative care incentives, wellness program integration, and expanded networks of providers.

Report Scope & Segmentation Analysis

This report comprehensively segments the ancillary insurance market across key applications and product types. The Adults segment is projected to exhibit a substantial market share of approximately xx million in 2025, driven by consistent demand for health maintenance. The Children segment, while smaller, shows promising growth as parents increasingly prioritize specialized care for their offspring.

Application: Adults: This segment, valued at approximately xx million in 2025, encompasses individuals seeking supplementary coverage for their personal healthcare needs. Growth is driven by proactive health management and the desire to mitigate out-of-pocket expenses for non-medical services. Competitive dynamics include a focus on comprehensive coverage and ease of access to providers.

Application: Children: This segment, projected to reach xx million in 2025, focuses on dependents benefiting from specialized care. Growth is fueled by parental concern for child development and the management of common childhood health issues. Competitive dynamics involve affordability and the breadth of pediatric-specific services offered.

Type: Vision Care: Anticipated to be a significant market segment, estimated at xx million in 2025, due to the widespread need for eye exams and corrective eyewear. Growth is steady, supported by the increasing use of digital devices and an aging population.

Type: Dental Care: This segment, projected at xx million in 2025, is driven by the crucial role of oral hygiene in overall health and the significant costs associated with dental treatments. Consistent demand and preventative care focus contribute to its robust market presence.

Type: Hearing Care: Valued at approximately xx million in 2025, this segment addresses the growing needs of an aging population and increased awareness of hearing health. Innovations in hearing aid technology and improved accessibility of audiology services are key growth factors.

Type: Others: This broad category, encompassing various specialized ancillary products, is expected to reach xx million in 2025, reflecting niche demands and emerging health trends.

Key Drivers of Ancillary Insurance Growth

The ancillary insurance sector is propelled by several key growth drivers. Technologically, the rise of digital health platforms and AI-powered personalized offerings is enhancing customer engagement and operational efficiency. Economically, increasing disposable incomes and a growing awareness of the value of preventative healthcare are boosting demand for supplementary coverage. Regulatory factors, such as government initiatives promoting broader access to health services and tax incentives for employer-provided benefits, are also significant catalysts.

Challenges in the Ancillary Insurance Sector

Despite its growth, the ancillary insurance sector faces several challenges. Regulatory hurdles related to market standardization and consumer protection can slow product development. Supply chain issues, particularly concerning specialized medical equipment or provider networks, can impact service delivery. Intense competitive pressures from established players and agile insurtech startups necessitate continuous innovation and strategic pricing. The estimated impact of these challenges on market growth is approximately xx% in terms of lost revenue opportunities.

Emerging Opportunities in Ancillary Insurance

Emerging opportunities in ancillary insurance are abundant. The growing demand for holistic wellness solutions presents a chance to expand offerings beyond traditional vision, dental, and hearing care. Untapped markets, particularly in developing economies, offer significant growth potential. Further integration of telehealth and remote monitoring services will enhance accessibility and convenience. Moreover, partnerships with employers to offer customized wellness programs integrated with ancillary benefits are a key avenue for expansion.

Leading Players in the Ancillary Insurance Market

- Aflac Incorporated

- Ameritas Mutual Holding Company

- Aetena Inc.

- Metlife Services and Solutions, LLC

- Manhattan Life Group Inc.

- Humana Inc.

- The Guardian Life Insurance Company of America

- Nationwide

Key Developments in Ancillary Insurance Industry

- 2023/11: Launch of an integrated digital platform by a major insurer for seamless policy management and claims submission.

- 2023/09: A leading provider acquires a smaller competitor to expand its national footprint in dental insurance.

- 2023/07: Introduction of AI-powered personalized dental plans based on individual oral health profiles.

- 2023/05: Partnership formed between a hearing care provider and an ancillary insurer to offer bundled hearing aid solutions.

- 2023/03: Expansion of vision care networks to include telehealth consultations for eye health assessments.

- 2023/01: Introduction of preventative wellness benefits within ancillary insurance packages.

Future Outlook for Ancillary Insurance Market

The future outlook for the ancillary insurance market is exceptionally bright, characterized by sustained growth and increasing strategic importance. The market is projected to expand significantly, driven by evolving consumer health consciousness and the continuous need for specialized care that complements primary health coverage. Key growth accelerators include the deepening integration of technology, such as AI and blockchain, for enhanced personalization and security, and the expansion of telehealth services to improve accessibility. Strategic opportunities lie in developing comprehensive wellness ecosystems that bundle ancillary benefits with preventative programs, further solidifying their value proposition for both individuals and employers.

Ancillary Insurance Segmentation

-

1. Application

- 1.1. Adults

- 1.2. Children

-

2. Type

- 2.1. Vision Care

- 2.2. Dental Care

- 2.3. Hearing Care

- 2.4. Others

Ancillary Insurance Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Ancillary Insurance REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XXX% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Ancillary Insurance Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Adults

- 5.1.2. Children

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Vision Care

- 5.2.2. Dental Care

- 5.2.3. Hearing Care

- 5.2.4. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Ancillary Insurance Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Adults

- 6.1.2. Children

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Vision Care

- 6.2.2. Dental Care

- 6.2.3. Hearing Care

- 6.2.4. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Ancillary Insurance Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Adults

- 7.1.2. Children

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Vision Care

- 7.2.2. Dental Care

- 7.2.3. Hearing Care

- 7.2.4. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Ancillary Insurance Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Adults

- 8.1.2. Children

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Vision Care

- 8.2.2. Dental Care

- 8.2.3. Hearing Care

- 8.2.4. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Ancillary Insurance Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Adults

- 9.1.2. Children

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Vision Care

- 9.2.2. Dental Care

- 9.2.3. Hearing Care

- 9.2.4. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Ancillary Insurance Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Adults

- 10.1.2. Children

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Vision Care

- 10.2.2. Dental Care

- 10.2.3. Hearing Care

- 10.2.4. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 Aflac Incorporated

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Ameritas Mutual Holding Company

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Aetena Inc.

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Metlife Services and Solutions LLC

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Manhattan Life Group Inc.

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Humana Inc.

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 The Guardian Life Insurance Company of America

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Nationwide

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.1 Aflac Incorporated

List of Figures

- Figure 1: Global Ancillary Insurance Revenue Breakdown (million, %) by Region 2024 & 2032

- Figure 2: North America Ancillary Insurance Revenue (million), by Application 2024 & 2032

- Figure 3: North America Ancillary Insurance Revenue Share (%), by Application 2024 & 2032

- Figure 4: North America Ancillary Insurance Revenue (million), by Type 2024 & 2032

- Figure 5: North America Ancillary Insurance Revenue Share (%), by Type 2024 & 2032

- Figure 6: North America Ancillary Insurance Revenue (million), by Country 2024 & 2032

- Figure 7: North America Ancillary Insurance Revenue Share (%), by Country 2024 & 2032

- Figure 8: South America Ancillary Insurance Revenue (million), by Application 2024 & 2032

- Figure 9: South America Ancillary Insurance Revenue Share (%), by Application 2024 & 2032

- Figure 10: South America Ancillary Insurance Revenue (million), by Type 2024 & 2032

- Figure 11: South America Ancillary Insurance Revenue Share (%), by Type 2024 & 2032

- Figure 12: South America Ancillary Insurance Revenue (million), by Country 2024 & 2032

- Figure 13: South America Ancillary Insurance Revenue Share (%), by Country 2024 & 2032

- Figure 14: Europe Ancillary Insurance Revenue (million), by Application 2024 & 2032

- Figure 15: Europe Ancillary Insurance Revenue Share (%), by Application 2024 & 2032

- Figure 16: Europe Ancillary Insurance Revenue (million), by Type 2024 & 2032

- Figure 17: Europe Ancillary Insurance Revenue Share (%), by Type 2024 & 2032

- Figure 18: Europe Ancillary Insurance Revenue (million), by Country 2024 & 2032

- Figure 19: Europe Ancillary Insurance Revenue Share (%), by Country 2024 & 2032

- Figure 20: Middle East & Africa Ancillary Insurance Revenue (million), by Application 2024 & 2032

- Figure 21: Middle East & Africa Ancillary Insurance Revenue Share (%), by Application 2024 & 2032

- Figure 22: Middle East & Africa Ancillary Insurance Revenue (million), by Type 2024 & 2032

- Figure 23: Middle East & Africa Ancillary Insurance Revenue Share (%), by Type 2024 & 2032

- Figure 24: Middle East & Africa Ancillary Insurance Revenue (million), by Country 2024 & 2032

- Figure 25: Middle East & Africa Ancillary Insurance Revenue Share (%), by Country 2024 & 2032

- Figure 26: Asia Pacific Ancillary Insurance Revenue (million), by Application 2024 & 2032

- Figure 27: Asia Pacific Ancillary Insurance Revenue Share (%), by Application 2024 & 2032

- Figure 28: Asia Pacific Ancillary Insurance Revenue (million), by Type 2024 & 2032

- Figure 29: Asia Pacific Ancillary Insurance Revenue Share (%), by Type 2024 & 2032

- Figure 30: Asia Pacific Ancillary Insurance Revenue (million), by Country 2024 & 2032

- Figure 31: Asia Pacific Ancillary Insurance Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Ancillary Insurance Revenue million Forecast, by Region 2019 & 2032

- Table 2: Global Ancillary Insurance Revenue million Forecast, by Application 2019 & 2032

- Table 3: Global Ancillary Insurance Revenue million Forecast, by Type 2019 & 2032

- Table 4: Global Ancillary Insurance Revenue million Forecast, by Region 2019 & 2032

- Table 5: Global Ancillary Insurance Revenue million Forecast, by Application 2019 & 2032

- Table 6: Global Ancillary Insurance Revenue million Forecast, by Type 2019 & 2032

- Table 7: Global Ancillary Insurance Revenue million Forecast, by Country 2019 & 2032

- Table 8: United States Ancillary Insurance Revenue (million) Forecast, by Application 2019 & 2032

- Table 9: Canada Ancillary Insurance Revenue (million) Forecast, by Application 2019 & 2032

- Table 10: Mexico Ancillary Insurance Revenue (million) Forecast, by Application 2019 & 2032

- Table 11: Global Ancillary Insurance Revenue million Forecast, by Application 2019 & 2032

- Table 12: Global Ancillary Insurance Revenue million Forecast, by Type 2019 & 2032

- Table 13: Global Ancillary Insurance Revenue million Forecast, by Country 2019 & 2032

- Table 14: Brazil Ancillary Insurance Revenue (million) Forecast, by Application 2019 & 2032

- Table 15: Argentina Ancillary Insurance Revenue (million) Forecast, by Application 2019 & 2032

- Table 16: Rest of South America Ancillary Insurance Revenue (million) Forecast, by Application 2019 & 2032

- Table 17: Global Ancillary Insurance Revenue million Forecast, by Application 2019 & 2032

- Table 18: Global Ancillary Insurance Revenue million Forecast, by Type 2019 & 2032

- Table 19: Global Ancillary Insurance Revenue million Forecast, by Country 2019 & 2032

- Table 20: United Kingdom Ancillary Insurance Revenue (million) Forecast, by Application 2019 & 2032

- Table 21: Germany Ancillary Insurance Revenue (million) Forecast, by Application 2019 & 2032

- Table 22: France Ancillary Insurance Revenue (million) Forecast, by Application 2019 & 2032

- Table 23: Italy Ancillary Insurance Revenue (million) Forecast, by Application 2019 & 2032

- Table 24: Spain Ancillary Insurance Revenue (million) Forecast, by Application 2019 & 2032

- Table 25: Russia Ancillary Insurance Revenue (million) Forecast, by Application 2019 & 2032

- Table 26: Benelux Ancillary Insurance Revenue (million) Forecast, by Application 2019 & 2032

- Table 27: Nordics Ancillary Insurance Revenue (million) Forecast, by Application 2019 & 2032

- Table 28: Rest of Europe Ancillary Insurance Revenue (million) Forecast, by Application 2019 & 2032

- Table 29: Global Ancillary Insurance Revenue million Forecast, by Application 2019 & 2032

- Table 30: Global Ancillary Insurance Revenue million Forecast, by Type 2019 & 2032

- Table 31: Global Ancillary Insurance Revenue million Forecast, by Country 2019 & 2032

- Table 32: Turkey Ancillary Insurance Revenue (million) Forecast, by Application 2019 & 2032

- Table 33: Israel Ancillary Insurance Revenue (million) Forecast, by Application 2019 & 2032

- Table 34: GCC Ancillary Insurance Revenue (million) Forecast, by Application 2019 & 2032

- Table 35: North Africa Ancillary Insurance Revenue (million) Forecast, by Application 2019 & 2032

- Table 36: South Africa Ancillary Insurance Revenue (million) Forecast, by Application 2019 & 2032

- Table 37: Rest of Middle East & Africa Ancillary Insurance Revenue (million) Forecast, by Application 2019 & 2032

- Table 38: Global Ancillary Insurance Revenue million Forecast, by Application 2019 & 2032

- Table 39: Global Ancillary Insurance Revenue million Forecast, by Type 2019 & 2032

- Table 40: Global Ancillary Insurance Revenue million Forecast, by Country 2019 & 2032

- Table 41: China Ancillary Insurance Revenue (million) Forecast, by Application 2019 & 2032

- Table 42: India Ancillary Insurance Revenue (million) Forecast, by Application 2019 & 2032

- Table 43: Japan Ancillary Insurance Revenue (million) Forecast, by Application 2019 & 2032

- Table 44: South Korea Ancillary Insurance Revenue (million) Forecast, by Application 2019 & 2032

- Table 45: ASEAN Ancillary Insurance Revenue (million) Forecast, by Application 2019 & 2032

- Table 46: Oceania Ancillary Insurance Revenue (million) Forecast, by Application 2019 & 2032

- Table 47: Rest of Asia Pacific Ancillary Insurance Revenue (million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Ancillary Insurance?

The projected CAGR is approximately XXX%.

2. Which companies are prominent players in the Ancillary Insurance?

Key companies in the market include Aflac Incorporated, Ameritas Mutual Holding Company, Aetena Inc., Metlife Services and Solutions, LLC, Manhattan Life Group Inc., Humana Inc., The Guardian Life Insurance Company of America, Nationwide.

3. What are the main segments of the Ancillary Insurance?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Ancillary Insurance," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Ancillary Insurance report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Ancillary Insurance?

To stay informed about further developments, trends, and reports in the Ancillary Insurance, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence