Key Insights

The global Grade I Polysilicon for Electronics market is poised for significant expansion, driven by the insatiable demand for semiconductors powering everything from smartphones to advanced computing. While specific market size figures were not provided, a healthy CAGR of approximately 8-10% (estimated based on industry trends and growth drivers) suggests a robust market worth in the billions of USD. This growth is fundamentally fueled by the escalating adoption of electronic devices across diverse sectors, including consumer electronics, automotive, and telecommunications, all of which rely heavily on high-purity polysilicon for wafer fabrication. The increasing complexity and miniaturization of semiconductor components further necessitate the use of superior-quality polysilicon, directly impacting market demand. Furthermore, the ongoing digitalization initiatives worldwide, coupled with advancements in AI and 5G technology, are creating an unprecedented need for more powerful and efficient chips, thereby propelling the Grade I Polysilicon market forward.

Key trends shaping this market include a strong emphasis on sustainable manufacturing practices and the development of more efficient polysilicon production methods. Companies are investing in cleaner technologies to reduce the environmental footprint associated with polysilicon manufacturing. The market is also witnessing a strategic shift towards localized production and supply chain resilience, particularly in response to geopolitical factors and the desire to mitigate risks. While the market is characterized by substantial growth, certain restraints could emerge. These may include the volatility in raw material prices, particularly for silicon metal, and the high capital expenditure required for setting up and maintaining polysilicon manufacturing facilities. Additionally, stringent environmental regulations in some regions could pose challenges for new entrants and existing players alike. Despite these potential headwinds, the overarching demand from the electronics industry, coupled with technological advancements in polysilicon purification and production, paints a very positive outlook for market participants.

Grade I Polysilicon for Electronics Market Analysis: Driving Semiconductor Innovation (2019-2033)

This comprehensive report delves into the Grade I Polysilicon for Electronics market, a critical component underpinning the global semiconductor industry. Analyzing from 2019 to 2033, with a base year of 2025, this study provides in-depth insights into market dynamics, innovation trends, regional dominance, and future growth potential. We examine key players, technological advancements, and the intricate segmentation of this vital market.

Grade I Polysilicon for Electronics Market Structure & Innovation Trends

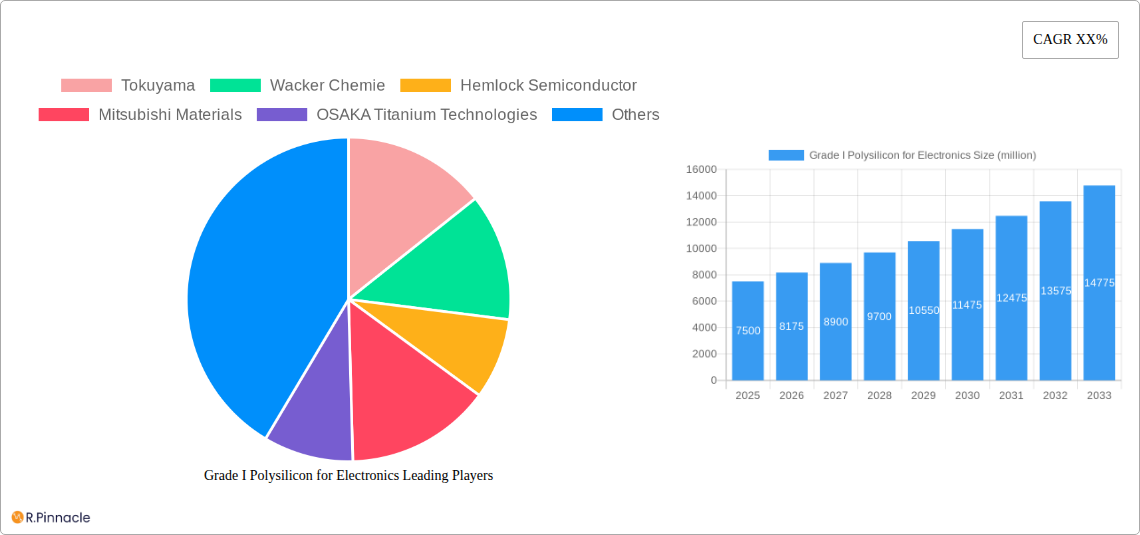

The Grade I Polysilicon for Electronics market is characterized by a moderate level of concentration, with key players like Tokuyama, Wacker Chemie, Hemlock Semiconductor, Mitsubishi Materials, OSAKA Titanium Technologies, OCI, REC Silicon, GCL-Poly Energy, Huanghe Hydropower, and Yichang CSG holding significant market shares, estimated at over 70% collectively in the base year of 2025. Innovation is primarily driven by the relentless demand for higher purity polysilicon to enable smaller, faster, and more power-efficient semiconductor devices, particularly for 300mm wafer applications. Regulatory frameworks, such as environmental compliance and trade policies, play a crucial role in shaping market access and production costs. Product substitutes are limited due to the stringent purity requirements for electronics-grade polysilicon. End-user demographics are dominated by semiconductor manufacturers and foundries. Mergers and acquisitions (M&A) activity, while present, has been strategic, with estimated deal values in the range of hundreds of millions of dollars, aimed at consolidating production capabilities and securing raw material supply chains.

- Market Concentration: Dominated by a few key global suppliers.

- Innovation Drivers: Demand for increased purity, smaller chip geometries, and advanced semiconductor nodes.

- Regulatory Frameworks: Environmental regulations and trade policies influencing production and pricing.

- Product Substitutes: Limited due to high purity demands.

- End-User Demographics: Primarily semiconductor manufacturers and foundries.

- M&A Activities: Strategic consolidation, with deal values in the hundreds of millions.

Grade I Polysilicon for Electronics Market Dynamics & Trends

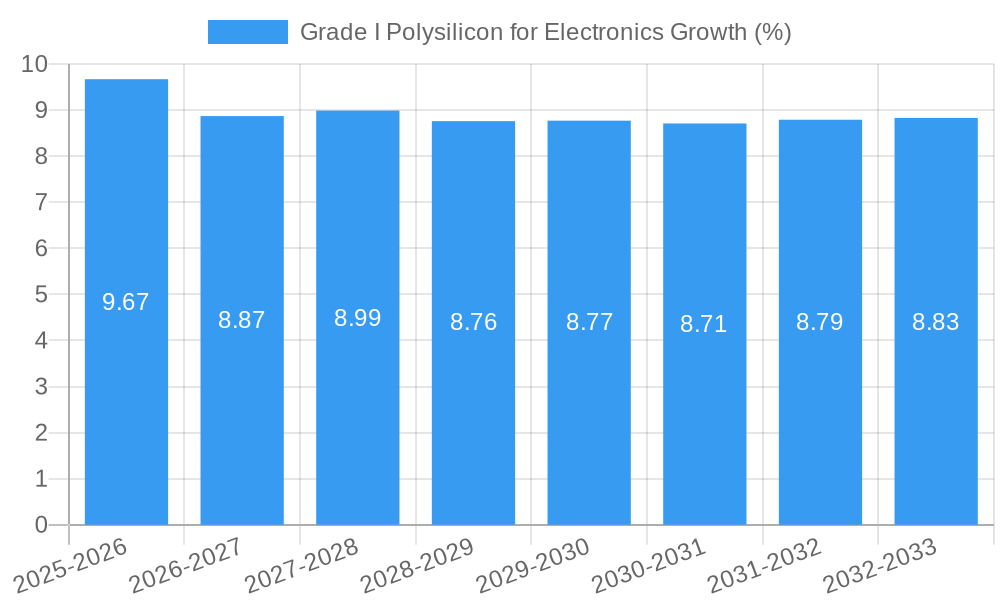

The Grade I Polysilicon for Electronics market is poised for significant growth, projected to experience a Compound Annual Growth Rate (CAGR) of approximately 6.5% during the forecast period of 2025–2033. This expansion is fueled by the escalating demand for advanced electronic devices, including smartphones, high-performance computing, artificial intelligence (AI) hardware, and the burgeoning Internet of Things (IoT) ecosystem. Technological disruptions, such as advancements in the Trichlorosilane (TCS) method and the development of more energy-efficient production processes like the Silane method, are continuously improving purity levels and cost-effectiveness. Consumer preferences for smaller, more powerful, and energy-efficient electronics directly translate into an increased need for high-purity polysilicon. The competitive dynamics within the market are intense, with established players investing heavily in capacity expansion and research and development to maintain their market penetration. Emerging economies are also showing increased market penetration as their domestic semiconductor industries mature. Supply chain resilience and geopolitical factors are becoming increasingly important considerations. The market penetration for 300mm wafer applications is expected to grow substantially due to its dominance in advanced node manufacturing. The shift towards sustainable manufacturing practices is also influencing production methods and raw material sourcing. The historical period (2019–2024) witnessed steady growth, driven by the increasing adoption of advanced technologies. The estimated market size for Grade I Polysilicon for Electronics in 2025 is projected to be in the billions of dollars, with significant contributions from wafer fabrication and semiconductor manufacturing. The report details specific market penetration rates and growth trajectories for various segments and regions.

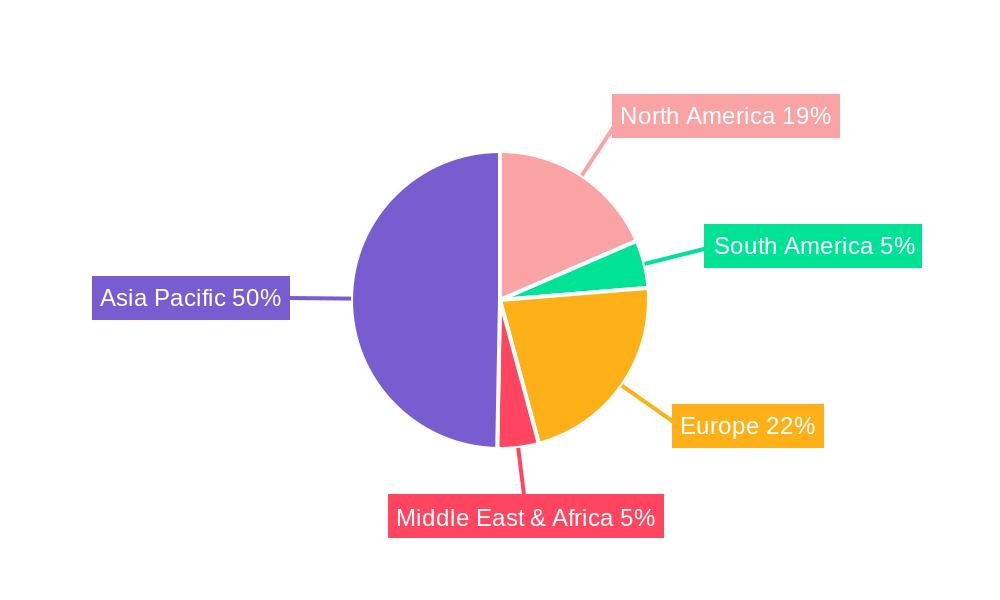

Dominant Regions & Segments in Grade I Polysilicon for Electronics

Asia Pacific, particularly China and South Korea, stands out as the dominant region in the Grade I Polysilicon for Electronics market. This dominance is propelled by strong government support for the semiconductor industry, substantial investments in wafer fabrication facilities, and a robust ecosystem of electronics manufacturing. The country-specific drivers include extensive economic policies encouraging domestic production, significant infrastructure development for advanced manufacturing, and a rapidly growing consumer electronics market.

In terms of application, the 300mm Wafer segment is leading the market and is expected to continue its trajectory of dominance throughout the forecast period. This is directly attributed to the global shift towards larger wafer sizes, which enable higher wafer yields and reduced manufacturing costs for advanced semiconductor chips. Foundries are increasingly adopting 300mm wafer technology for the production of next-generation processors, memory chips, and AI accelerators.

Among the types, the Trichlorosilane (TCS) Method remains the most prevalent and widely adopted production process for Grade I Polysilicon. Its established efficiency and scalability contribute to its market leadership. However, ongoing research and development are focusing on optimizing and refining the Silane Method and Dichlorodihydro Silicon Method for enhanced purity and energy efficiency, suggesting potential future shifts in dominance.

- Leading Region: Asia Pacific (China, South Korea)

- Key Drivers: Government support, wafer fabrication investment, electronics manufacturing ecosystem, economic policies, infrastructure development, consumer electronics demand.

- Dominant Application Segment: 300mm Wafer

- Key Drivers: Higher wafer yields, reduced manufacturing costs, production of advanced semiconductor chips, adoption by foundries for next-gen processors, memory, and AI accelerators.

- Dominant Type: Trichlorosilane (TCS) Method

- Key Drivers: Established efficiency, scalability, widespread adoption.

- Emerging Trends: Advancements in Silane Method and Dichlorodihydro Silicon Method for improved purity and energy efficiency.

Grade I Polysilicon for Electronics Product Innovations

Product innovations in Grade I Polysilicon for Electronics are centered on achieving ultra-high purity levels (exceeding 9N, or 99.9999999% purity) to meet the demands of sub-10nm semiconductor nodes. Manufacturers are investing in advanced purification techniques and proprietary processes to reduce metallic impurities and other contaminants to parts per trillion (ppt) levels. This drive for higher purity translates into improved device performance, lower defect rates, and enhanced reliability in advanced integrated circuits. Competitive advantages are derived from consistent product quality, cost-effective production, and the ability to tailor polysilicon specifications to meet the unique requirements of different semiconductor applications. Technological trends favor continuous improvement in silicon crystal growth and refining processes.

Report Scope & Segmentation Analysis

This report segments the Grade I Polysilicon for Electronics market across key applications and production types. The 300mm Wafer segment is projected to exhibit the highest growth rate due to its widespread adoption in cutting-edge semiconductor manufacturing. The 200mm Wafer segment, while mature, continues to be relevant for specific applications and legacy manufacturing. The Others application segment encompasses specialized uses and emerging technologies. In terms of production types, the Trichlorosilane Method dominates the current market, but the Silane Method and Dichlorodihydro Silicon Method are gaining traction due to their potential for improved efficiency and purity. The Silicon Tetrachloride and Other methods represent niche or less prevalent production routes. Detailed market size projections and competitive dynamics are provided for each segment.

- Application Segmentation:

- 300mm Wafer: Expected to lead in growth due to advanced node manufacturing.

- 200mm Wafer: Continues to be significant for specific applications.

- Others: Includes specialized uses and emerging technologies.

- Type Segmentation:

- Trichlorosilane Method: Current market leader.

- Silicon Tetrachloride: Niche or less prevalent.

- Dichlorodihydro Silicon Method: Emerging with potential improvements.

- Silane Method: Gaining traction for efficiency and purity.

- Other: Represents other less common production methods.

Key Drivers of Grade I Polysilicon for Electronics Growth

The growth of the Grade I Polysilicon for Electronics market is propelled by several interconnected factors. The exponential increase in demand for semiconductors driven by AI, 5G, IoT, and advanced computing applications is the primary catalyst. Technological advancements in semiconductor manufacturing, enabling smaller feature sizes and higher transistor densities, necessitate the use of increasingly pure polysilicon. Government initiatives and investments in domestic semiconductor manufacturing capabilities in various regions also contribute significantly. Economic growth and the increasing disposable income in developing nations further fuel the demand for consumer electronics, indirectly boosting polysilicon consumption.

- Demand for Advanced Electronics: AI, 5G, IoT, HPC.

- Semiconductor Technology Advancements: Smaller nodes, higher densities.

- Government Initiatives: Support for domestic semiconductor production.

- Global Economic Growth: Increased consumer electronics demand.

Challenges in the Grade I Polysilicon for Electronics Sector

Despite robust growth prospects, the Grade I Polysilicon for Electronics sector faces several challenges. The high capital intensity and energy consumption associated with polysilicon production create significant barriers to entry and necessitate substantial operational investments. Stringent environmental regulations concerning emissions and waste management add to production costs and complexity. Geopolitical tensions and trade disputes can disrupt global supply chains, leading to price volatility and material shortages. Intense competition among established players and emerging producers can lead to price pressures and margin erosion. Furthermore, the continuous need for R&D to achieve higher purity levels requires ongoing technological innovation and significant investment.

- High Capital and Energy Intensity: Significant upfront and operational costs.

- Environmental Regulations: Compliance adds to production costs.

- Supply Chain Vulnerabilities: Geopolitical risks and trade disputes.

- Intense Competition: Price pressures and margin erosion.

- Continuous R&D Demands: Need for innovation to achieve ultra-high purity.

Emerging Opportunities in Grade I Polysilicon for Electronics

Emerging opportunities within the Grade I Polysilicon for Electronics market are diverse and promising. The rapid expansion of the electric vehicle (EV) market and the increasing adoption of advanced driver-assistance systems (ADAS) are creating new demand for specialized semiconductor components requiring high-purity polysilicon. The growth of renewable energy technologies, particularly solar power, also presents opportunities for polysilicon manufacturers, although the quality requirements may differ. Advancements in quantum computing and other next-generation technologies are expected to drive demand for novel semiconductor materials, including ultra-pure polysilicon. Furthermore, the development of more sustainable and energy-efficient polysilicon production methods offers opportunities for companies to gain a competitive edge and meet increasing environmental concerns. The growing demand for wafer-level manufacturing in emerging markets presents a significant opportunity for market expansion.

- Electric Vehicles (EVs) and ADAS: Growing demand for specialized semiconductors.

- Renewable Energy: Opportunities in solar power (though with different purity needs).

- Next-Generation Technologies: Quantum computing, advanced sensors.

- Sustainable Production Methods: Meeting environmental demands and gaining competitive advantage.

- Emerging Markets: Growth in wafer-level manufacturing.

Leading Players in the Grade I Polysilicon for Electronics Market

- Tokuyama

- Wacker Chemie

- Hemlock Semiconductor

- Mitsubishi Materials

- OSAKA Titanium Technologies

- OCI

- REC Silicon

- GCL-Poly Energy

- Huanghe Hydropower

- Yichang CSG

Key Developments in Grade I Polysilicon for Electronics Industry

- 2023 March: GCL-Poly Energy announces expansion of its polysilicon production capacity by 100,000 metric tons to meet growing demand for solar and semiconductor applications.

- 2022 December: Wacker Chemie completes acquisition of a minority stake in a polysilicon joint venture in China, strengthening its market presence.

- 2022 July: Hemlock Semiconductor announces significant investment in expanding its polysilicon production capacity in the United States.

- 2021 September: Tokuyama develops a new purification technology that achieves record-high purity levels for Grade I polysilicon.

- 2020 May: REC Silicon secures a multi-year supply agreement with a major US-based semiconductor manufacturer.

Future Outlook for Grade I Polysilicon for Electronics Market

The future outlook for the Grade I Polysilicon for Electronics market is exceptionally bright, driven by the sustained and accelerating demand for advanced semiconductors. The continuous miniaturization of electronic components and the proliferation of data-intensive applications, such as AI, autonomous driving, and the metaverse, will necessitate a corresponding increase in the production and purity of polysilicon. Strategic investments in capacity expansion, coupled with ongoing innovation in production technologies aimed at improving efficiency and reducing environmental impact, will be crucial for market players. Emerging markets will offer significant growth potential as their semiconductor industries mature. Companies that can demonstrate a strong commitment to sustainability and supply chain resilience will be well-positioned for long-term success. The increasing importance of domestic semiconductor manufacturing in various countries will also create new avenues for growth and strategic partnerships.

Grade I Polysilicon for Electronics Segmentation

-

1. Application

- 1.1. 300mm Wafer

- 1.2. 200mm Wafer

- 1.3. Others

-

2. Types

- 2.1. Trichlorosilane Method

- 2.2. Silicon Tetrachloride

- 2.3. Dichlorodihydro Silicon Method

- 2.4. Silane Method

- 2.5. Other

Grade I Polysilicon for Electronics Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Grade I Polysilicon for Electronics REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Grade I Polysilicon for Electronics Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. 300mm Wafer

- 5.1.2. 200mm Wafer

- 5.1.3. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Trichlorosilane Method

- 5.2.2. Silicon Tetrachloride

- 5.2.3. Dichlorodihydro Silicon Method

- 5.2.4. Silane Method

- 5.2.5. Other

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Grade I Polysilicon for Electronics Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. 300mm Wafer

- 6.1.2. 200mm Wafer

- 6.1.3. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Trichlorosilane Method

- 6.2.2. Silicon Tetrachloride

- 6.2.3. Dichlorodihydro Silicon Method

- 6.2.4. Silane Method

- 6.2.5. Other

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Grade I Polysilicon for Electronics Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. 300mm Wafer

- 7.1.2. 200mm Wafer

- 7.1.3. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Trichlorosilane Method

- 7.2.2. Silicon Tetrachloride

- 7.2.3. Dichlorodihydro Silicon Method

- 7.2.4. Silane Method

- 7.2.5. Other

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Grade I Polysilicon for Electronics Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. 300mm Wafer

- 8.1.2. 200mm Wafer

- 8.1.3. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Trichlorosilane Method

- 8.2.2. Silicon Tetrachloride

- 8.2.3. Dichlorodihydro Silicon Method

- 8.2.4. Silane Method

- 8.2.5. Other

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Grade I Polysilicon for Electronics Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. 300mm Wafer

- 9.1.2. 200mm Wafer

- 9.1.3. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Trichlorosilane Method

- 9.2.2. Silicon Tetrachloride

- 9.2.3. Dichlorodihydro Silicon Method

- 9.2.4. Silane Method

- 9.2.5. Other

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Grade I Polysilicon for Electronics Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. 300mm Wafer

- 10.1.2. 200mm Wafer

- 10.1.3. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Trichlorosilane Method

- 10.2.2. Silicon Tetrachloride

- 10.2.3. Dichlorodihydro Silicon Method

- 10.2.4. Silane Method

- 10.2.5. Other

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 Tokuyama

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Wacker Chemie

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Hemlock Semiconductor

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Mitsubishi Materials

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 OSAKA Titanium Technologies

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 OCI

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 REC Silicon

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 GCL-Poly Energy

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Huanghe Hydropower

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Yichang CSG

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.1 Tokuyama

List of Figures

- Figure 1: Global Grade I Polysilicon for Electronics Revenue Breakdown (million, %) by Region 2024 & 2032

- Figure 2: North America Grade I Polysilicon for Electronics Revenue (million), by Application 2024 & 2032

- Figure 3: North America Grade I Polysilicon for Electronics Revenue Share (%), by Application 2024 & 2032

- Figure 4: North America Grade I Polysilicon for Electronics Revenue (million), by Types 2024 & 2032

- Figure 5: North America Grade I Polysilicon for Electronics Revenue Share (%), by Types 2024 & 2032

- Figure 6: North America Grade I Polysilicon for Electronics Revenue (million), by Country 2024 & 2032

- Figure 7: North America Grade I Polysilicon for Electronics Revenue Share (%), by Country 2024 & 2032

- Figure 8: South America Grade I Polysilicon for Electronics Revenue (million), by Application 2024 & 2032

- Figure 9: South America Grade I Polysilicon for Electronics Revenue Share (%), by Application 2024 & 2032

- Figure 10: South America Grade I Polysilicon for Electronics Revenue (million), by Types 2024 & 2032

- Figure 11: South America Grade I Polysilicon for Electronics Revenue Share (%), by Types 2024 & 2032

- Figure 12: South America Grade I Polysilicon for Electronics Revenue (million), by Country 2024 & 2032

- Figure 13: South America Grade I Polysilicon for Electronics Revenue Share (%), by Country 2024 & 2032

- Figure 14: Europe Grade I Polysilicon for Electronics Revenue (million), by Application 2024 & 2032

- Figure 15: Europe Grade I Polysilicon for Electronics Revenue Share (%), by Application 2024 & 2032

- Figure 16: Europe Grade I Polysilicon for Electronics Revenue (million), by Types 2024 & 2032

- Figure 17: Europe Grade I Polysilicon for Electronics Revenue Share (%), by Types 2024 & 2032

- Figure 18: Europe Grade I Polysilicon for Electronics Revenue (million), by Country 2024 & 2032

- Figure 19: Europe Grade I Polysilicon for Electronics Revenue Share (%), by Country 2024 & 2032

- Figure 20: Middle East & Africa Grade I Polysilicon for Electronics Revenue (million), by Application 2024 & 2032

- Figure 21: Middle East & Africa Grade I Polysilicon for Electronics Revenue Share (%), by Application 2024 & 2032

- Figure 22: Middle East & Africa Grade I Polysilicon for Electronics Revenue (million), by Types 2024 & 2032

- Figure 23: Middle East & Africa Grade I Polysilicon for Electronics Revenue Share (%), by Types 2024 & 2032

- Figure 24: Middle East & Africa Grade I Polysilicon for Electronics Revenue (million), by Country 2024 & 2032

- Figure 25: Middle East & Africa Grade I Polysilicon for Electronics Revenue Share (%), by Country 2024 & 2032

- Figure 26: Asia Pacific Grade I Polysilicon for Electronics Revenue (million), by Application 2024 & 2032

- Figure 27: Asia Pacific Grade I Polysilicon for Electronics Revenue Share (%), by Application 2024 & 2032

- Figure 28: Asia Pacific Grade I Polysilicon for Electronics Revenue (million), by Types 2024 & 2032

- Figure 29: Asia Pacific Grade I Polysilicon for Electronics Revenue Share (%), by Types 2024 & 2032

- Figure 30: Asia Pacific Grade I Polysilicon for Electronics Revenue (million), by Country 2024 & 2032

- Figure 31: Asia Pacific Grade I Polysilicon for Electronics Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Grade I Polysilicon for Electronics Revenue million Forecast, by Region 2019 & 2032

- Table 2: Global Grade I Polysilicon for Electronics Revenue million Forecast, by Application 2019 & 2032

- Table 3: Global Grade I Polysilicon for Electronics Revenue million Forecast, by Types 2019 & 2032

- Table 4: Global Grade I Polysilicon for Electronics Revenue million Forecast, by Region 2019 & 2032

- Table 5: Global Grade I Polysilicon for Electronics Revenue million Forecast, by Application 2019 & 2032

- Table 6: Global Grade I Polysilicon for Electronics Revenue million Forecast, by Types 2019 & 2032

- Table 7: Global Grade I Polysilicon for Electronics Revenue million Forecast, by Country 2019 & 2032

- Table 8: United States Grade I Polysilicon for Electronics Revenue (million) Forecast, by Application 2019 & 2032

- Table 9: Canada Grade I Polysilicon for Electronics Revenue (million) Forecast, by Application 2019 & 2032

- Table 10: Mexico Grade I Polysilicon for Electronics Revenue (million) Forecast, by Application 2019 & 2032

- Table 11: Global Grade I Polysilicon for Electronics Revenue million Forecast, by Application 2019 & 2032

- Table 12: Global Grade I Polysilicon for Electronics Revenue million Forecast, by Types 2019 & 2032

- Table 13: Global Grade I Polysilicon for Electronics Revenue million Forecast, by Country 2019 & 2032

- Table 14: Brazil Grade I Polysilicon for Electronics Revenue (million) Forecast, by Application 2019 & 2032

- Table 15: Argentina Grade I Polysilicon for Electronics Revenue (million) Forecast, by Application 2019 & 2032

- Table 16: Rest of South America Grade I Polysilicon for Electronics Revenue (million) Forecast, by Application 2019 & 2032

- Table 17: Global Grade I Polysilicon for Electronics Revenue million Forecast, by Application 2019 & 2032

- Table 18: Global Grade I Polysilicon for Electronics Revenue million Forecast, by Types 2019 & 2032

- Table 19: Global Grade I Polysilicon for Electronics Revenue million Forecast, by Country 2019 & 2032

- Table 20: United Kingdom Grade I Polysilicon for Electronics Revenue (million) Forecast, by Application 2019 & 2032

- Table 21: Germany Grade I Polysilicon for Electronics Revenue (million) Forecast, by Application 2019 & 2032

- Table 22: France Grade I Polysilicon for Electronics Revenue (million) Forecast, by Application 2019 & 2032

- Table 23: Italy Grade I Polysilicon for Electronics Revenue (million) Forecast, by Application 2019 & 2032

- Table 24: Spain Grade I Polysilicon for Electronics Revenue (million) Forecast, by Application 2019 & 2032

- Table 25: Russia Grade I Polysilicon for Electronics Revenue (million) Forecast, by Application 2019 & 2032

- Table 26: Benelux Grade I Polysilicon for Electronics Revenue (million) Forecast, by Application 2019 & 2032

- Table 27: Nordics Grade I Polysilicon for Electronics Revenue (million) Forecast, by Application 2019 & 2032

- Table 28: Rest of Europe Grade I Polysilicon for Electronics Revenue (million) Forecast, by Application 2019 & 2032

- Table 29: Global Grade I Polysilicon for Electronics Revenue million Forecast, by Application 2019 & 2032

- Table 30: Global Grade I Polysilicon for Electronics Revenue million Forecast, by Types 2019 & 2032

- Table 31: Global Grade I Polysilicon for Electronics Revenue million Forecast, by Country 2019 & 2032

- Table 32: Turkey Grade I Polysilicon for Electronics Revenue (million) Forecast, by Application 2019 & 2032

- Table 33: Israel Grade I Polysilicon for Electronics Revenue (million) Forecast, by Application 2019 & 2032

- Table 34: GCC Grade I Polysilicon for Electronics Revenue (million) Forecast, by Application 2019 & 2032

- Table 35: North Africa Grade I Polysilicon for Electronics Revenue (million) Forecast, by Application 2019 & 2032

- Table 36: South Africa Grade I Polysilicon for Electronics Revenue (million) Forecast, by Application 2019 & 2032

- Table 37: Rest of Middle East & Africa Grade I Polysilicon for Electronics Revenue (million) Forecast, by Application 2019 & 2032

- Table 38: Global Grade I Polysilicon for Electronics Revenue million Forecast, by Application 2019 & 2032

- Table 39: Global Grade I Polysilicon for Electronics Revenue million Forecast, by Types 2019 & 2032

- Table 40: Global Grade I Polysilicon for Electronics Revenue million Forecast, by Country 2019 & 2032

- Table 41: China Grade I Polysilicon for Electronics Revenue (million) Forecast, by Application 2019 & 2032

- Table 42: India Grade I Polysilicon for Electronics Revenue (million) Forecast, by Application 2019 & 2032

- Table 43: Japan Grade I Polysilicon for Electronics Revenue (million) Forecast, by Application 2019 & 2032

- Table 44: South Korea Grade I Polysilicon for Electronics Revenue (million) Forecast, by Application 2019 & 2032

- Table 45: ASEAN Grade I Polysilicon for Electronics Revenue (million) Forecast, by Application 2019 & 2032

- Table 46: Oceania Grade I Polysilicon for Electronics Revenue (million) Forecast, by Application 2019 & 2032

- Table 47: Rest of Asia Pacific Grade I Polysilicon for Electronics Revenue (million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Grade I Polysilicon for Electronics?

The projected CAGR is approximately XX%.

2. Which companies are prominent players in the Grade I Polysilicon for Electronics?

Key companies in the market include Tokuyama, Wacker Chemie, Hemlock Semiconductor, Mitsubishi Materials, OSAKA Titanium Technologies, OCI, REC Silicon, GCL-Poly Energy, Huanghe Hydropower, Yichang CSG.

3. What are the main segments of the Grade I Polysilicon for Electronics?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Grade I Polysilicon for Electronics," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Grade I Polysilicon for Electronics report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Grade I Polysilicon for Electronics?

To stay informed about further developments, trends, and reports in the Grade I Polysilicon for Electronics, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence