Key Insights

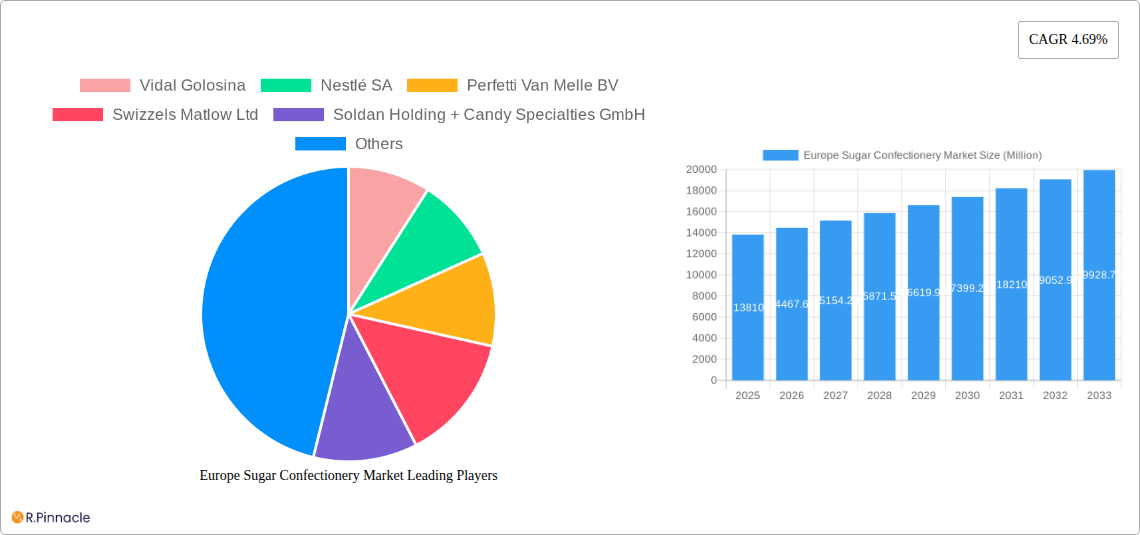

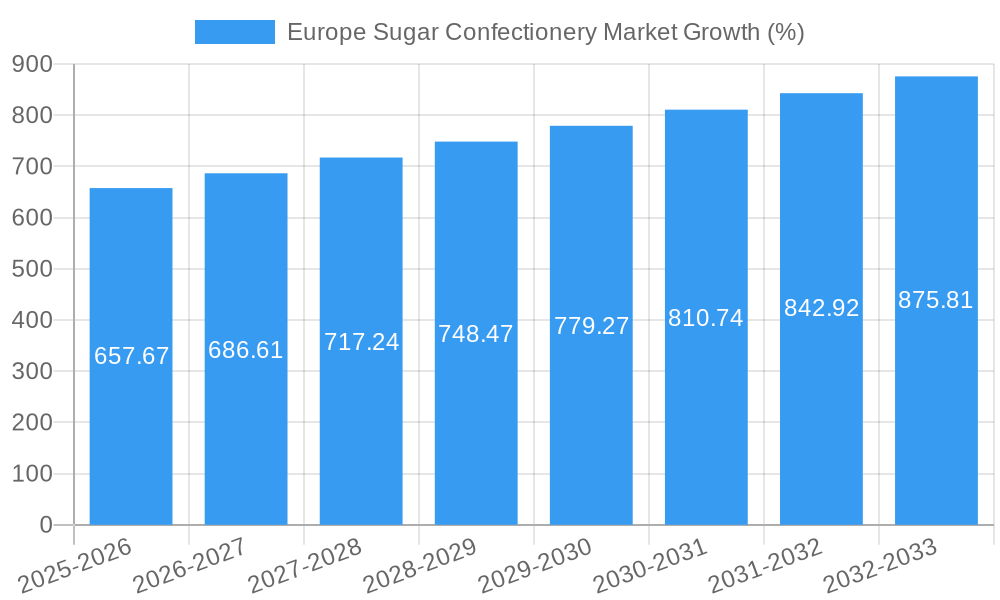

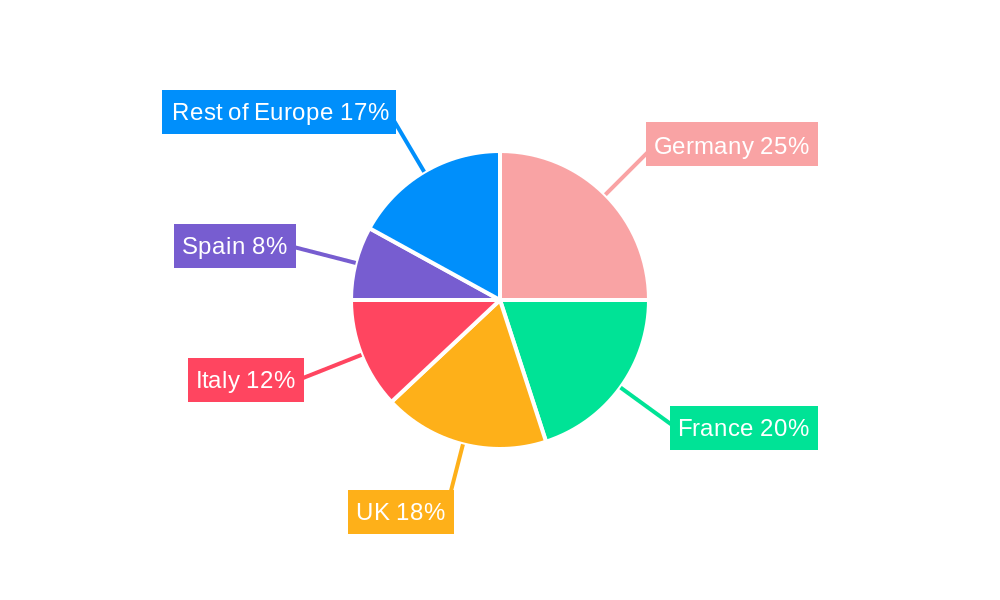

The European sugar confectionery market, valued at €13.81 billion in 2025, is projected to experience steady growth, driven by several key factors. Increased disposable incomes in several European countries, coupled with a rising preference for convenient and indulgent snacks, fuels demand for sugar confectionery products. The market is segmented by confectionery type, with hard candies, lollipops, and gummies holding significant market share due to their broad appeal across age groups. Growing health consciousness is a notable trend, leading to increased demand for sugar-reduced or healthier alternatives within the confectionery sector. Manufacturers are responding with innovative product launches featuring natural sweeteners and reduced sugar content. However, stringent regulations on sugar content and increasing health concerns pose challenges to the market’s growth. The online retail channel is experiencing robust growth, reflecting the evolving consumer preference for convenient purchasing options. Germany, France, and the UK remain the largest national markets within Europe, driven by high consumption rates and established distribution networks. Competitive intensity remains high, with established multinational players and regional brands vying for market share through product innovation and strategic partnerships. The market's growth trajectory is expected to continue, albeit at a moderated pace, reflecting the balance between consumer demand and evolving health-conscious preferences. The forecast period (2025-2033) anticipates a sustained expansion, albeit at a slightly slower pace than previous years, influenced by the aforementioned market dynamics.

The competitive landscape is characterized by a mix of multinational corporations and regional players. Major players such as Nestlé, Mars, and Ferrero leverage their established brands and extensive distribution networks to maintain their market positions. Smaller, regional companies focus on specialized confectionery types or cater to niche market segments with innovative flavors and unique product offerings. Product diversification, focusing on premiumization and healthier options, will be key for companies seeking to capture market share and enhance profitability. Successful strategies will involve aligning product offerings with evolving consumer preferences, adapting to regulatory changes, and leveraging effective marketing and distribution channels to reach target demographics. The projected CAGR of 4.69% indicates consistent albeit moderate growth over the forecast period, reflecting the market's resilience and adaptation to the ongoing shifts in consumer behavior and regulatory environments.

Europe Sugar Confectionery Market: A Comprehensive Report (2019-2033)

This in-depth report provides a comprehensive analysis of the Europe sugar confectionery market, offering invaluable insights for industry professionals, investors, and strategic decision-makers. We cover market structure, dynamics, key players, and future growth projections, leveraging data from 2019-2024 (historical period), with estimations for 2025 (base and estimated year) and forecasts extending to 2033 (forecast period). The market is segmented by country (Belgium, France, Germany, Italy, Netherlands, Russia, Spain, Switzerland, Turkey, United Kingdom, Rest of Europe), confectionery variant (Hard Candy, Lollipops, Mints, Pastilles, Gummies and Jellies, Toffees and Nougats, Others), and distribution channel (Convenience Store, Online Retail Store, Supermarket/Hypermarket, Others).

Europe Sugar Confectionery Market Structure & Innovation Trends

The European sugar confectionery market exhibits a moderately concentrated structure, with several multinational giants holding significant market share. Key players like Nestlé SA, Mars Incorporated, and Ferrero International SA command substantial portions, while regional and smaller players contribute to the overall market vibrancy. The market is characterized by continuous innovation, driven by evolving consumer preferences for healthier options, unique flavors, and sustainable packaging. Regulatory frameworks concerning sugar content and labeling influence product development, and intense competition necessitates constant product differentiation. The market is also susceptible to the emergence of substitute products, such as sugar-free confectionery, posing a challenge to traditional players. Mergers and acquisitions (M&A) activities play a considerable role in shaping the market landscape, with larger companies acquiring smaller brands to expand their portfolio and distribution reach. Recent M&A deal values have averaged xx Million, although this fluctuates significantly depending on the size and strategic importance of the target company.

Europe Sugar Confectionery Market Dynamics & Trends

The Europe sugar confectionery market is projected to witness a CAGR of xx% during the forecast period (2025-2033). Growth is primarily driven by factors such as rising disposable incomes, increasing consumer spending on treats, and the growing popularity of online retail channels. Technological advancements in manufacturing processes, flavor development, and packaging solutions contribute to market expansion. Consumer preferences are shifting towards healthier options and more indulgent experiences, fueling the demand for premium and specialized confectionery products. The rise of e-commerce is significantly altering the distribution landscape, creating new avenues for direct-to-consumer sales and enhancing convenience. Competitive dynamics are intense, with established players continually innovating and smaller companies emerging with niche products. The market penetration of online retail channels is currently estimated at xx%, expected to grow significantly by 2033.

Dominant Regions & Segments in Europe Sugar Confectionery Market

Leading Region: Western Europe (Germany, UK, France) accounts for the largest market share, driven by high consumption levels and established distribution networks.

Leading Country: Germany consistently holds a dominant position due to strong purchasing power, high consumption patterns, and a well-developed confectionery industry.

Leading Segment (Confectionery Variant): Gummies and Jellies currently hold the largest market share, driven by their versatility, popularity across age groups, and continuous innovation in flavors and textures.

Leading Segment (Distribution Channel): Supermarket/Hypermarkets continue to dominate the distribution channel, offering wide product selections and convenient accessibility. However, online retail is growing rapidly.

The dominance of Germany and Western Europe is rooted in higher per capita disposable incomes, well-established retail infrastructure, and mature consumer markets. The UK, while experiencing some economic uncertainty, maintains strong consumption of confectionery. France displays a healthy market, with diverse preferences for both traditional and novel confectionery items. These countries benefit from robust economies and efficient logistics networks, further bolstering their market share.

Europe Sugar Confectionery Market Product Innovations

Recent product innovations focus on healthier options, such as reduced sugar content and natural ingredients. New flavor combinations, unique textures, and visually appealing packaging are employed to attract consumers. Technological advancements in manufacturing improve production efficiency and reduce costs. The incorporation of smart packaging with augmented reality (AR) experiences is emerging as a key differentiator. Market fit is driven by consumer demand for novelty, healthier choices, and personalized experiences.

Report Scope & Segmentation Analysis

Country: The report comprehensively analyzes the market across Belgium, France, Germany, Italy, Netherlands, Russia, Spain, Switzerland, Turkey, United Kingdom, and Rest of Europe, projecting growth in each region based on consumption trends and economic factors. Market size varies considerably depending on the region, with Western Europe showing significant higher market value than Eastern Europe.

Confectionery Variant: Each confectionery variant (Hard Candy, Lollipops, Mints, Pastilles, Gummies and Jellies, Toffees and Nougats, Others) is analyzed for its market size, growth rate, and competitive landscape. Gummies and Jellies are expected to experience particularly strong growth, while traditional products face moderate challenges.

Distribution Channel: The report examines the market size and growth of each distribution channel, including Convenience Stores, Online Retail Stores, and Supermarket/Hypermarkets. E-commerce is expected to become a more significant channel for confectionery sales.

Key Drivers of Europe Sugar Confectionery Market Growth

Key drivers include increasing disposable incomes across several European countries, expanding online retail channels, and innovation in flavors and packaging. Government policies promoting domestic industries also influence market growth. The trend towards premiumization and indulgence also fuels demand for higher-quality confectionery products.

Challenges in the Europe Sugar Confectionery Market Sector

Fluctuations in raw material prices, increasing health consciousness leading to a shift towards healthier alternatives, and stringent regulations concerning sugar content pose significant challenges. Competition from both established players and emerging brands creates intense pressure on margins and market share. Supply chain disruptions caused by geopolitical events can significantly impact production and distribution.

Emerging Opportunities in Europe Sugar Confectionery Market

Emerging opportunities lie in the growing demand for functional confectionery (e.g., incorporating probiotics or vitamins), personalized products, and sustainable packaging options. The expansion into emerging markets within Europe and the increasing adoption of e-commerce platforms offer significant potential for growth.

Leading Players in the Europe Sugar Confectionery Market Market

- Vidal Golosina

- Nestlé SA

- Perfetti Van Melle BV

- Swizzels Matlow Ltd

- Soldan Holding + Candy Specialties GmbH

- Lavdas SA

- August Storck KG

- Katjes International GmbH & Co KG

- Ferrero International SA

- Cloetta AB

- Ricola AG

- Mars Incorporated

- HARIBO Holding GmbH & Co KG

- Mondelēz International Inc

- The Hershey Company

Key Developments in Europe Sugar Confectionery Market Industry

- March 2023: Hershey's introduced new Hershey's Kisses’ Milklicious candies.

- April 2023: Swizzels Sweets partnered with Applied Nutrition to launch sports nutrition products.

- May 2023: Swizzels expanded its Minions product range with a Sherbet Dip.

Future Outlook for Europe Sugar Confectionery Market Market

The Europe sugar confectionery market is poised for continued growth, driven by innovation, evolving consumer preferences, and the expansion of e-commerce. Strategic partnerships, product diversification, and a focus on sustainability will be crucial for success in this dynamic market. The market is expected to see significant growth in premium and healthier confectionery options, while traditional products may see moderate decline.

Europe Sugar Confectionery Market Segmentation

-

1. Confectionery Variant

- 1.1. Hard Candy

- 1.2. Lollipops

- 1.3. Mints

- 1.4. Pastilles, Gummies, and Jellies

- 1.5. Toffees and Nougats

- 1.6. Others

-

2. Distribution Channel

- 2.1. Convenience Store

- 2.2. Online Retail Store

- 2.3. Supermarket/Hypermarket

- 2.4. Others

Europe Sugar Confectionery Market Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Netherlands

- 1.7. Belgium

- 1.8. Sweden

- 1.9. Norway

- 1.10. Poland

- 1.11. Denmark

Europe Sugar Confectionery Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 4.69% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increased Consumption of Baked Goods; Demand for Indigenous Fermented Foods

- 3.3. Market Restrains

- 3.3.1. Potential Side-effects of Yeast

- 3.4. Market Trends

- 3.4.1. OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Europe Sugar Confectionery Market Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Confectionery Variant

- 5.1.1. Hard Candy

- 5.1.2. Lollipops

- 5.1.3. Mints

- 5.1.4. Pastilles, Gummies, and Jellies

- 5.1.5. Toffees and Nougats

- 5.1.6. Others

- 5.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.2.1. Convenience Store

- 5.2.2. Online Retail Store

- 5.2.3. Supermarket/Hypermarket

- 5.2.4. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by Confectionery Variant

- 6. Germany Europe Sugar Confectionery Market Analysis, Insights and Forecast, 2019-2031

- 7. France Europe Sugar Confectionery Market Analysis, Insights and Forecast, 2019-2031

- 8. Italy Europe Sugar Confectionery Market Analysis, Insights and Forecast, 2019-2031

- 9. United Kingdom Europe Sugar Confectionery Market Analysis, Insights and Forecast, 2019-2031

- 10. Netherlands Europe Sugar Confectionery Market Analysis, Insights and Forecast, 2019-2031

- 11. Sweden Europe Sugar Confectionery Market Analysis, Insights and Forecast, 2019-2031

- 12. Rest of Europe Europe Sugar Confectionery Market Analysis, Insights and Forecast, 2019-2031

- 13. Competitive Analysis

- 13.1. Market Share Analysis 2024

- 13.2. Company Profiles

- 13.2.1 Vidal Golosina

- 13.2.1.1. Overview

- 13.2.1.2. Products

- 13.2.1.3. SWOT Analysis

- 13.2.1.4. Recent Developments

- 13.2.1.5. Financials (Based on Availability)

- 13.2.2 Nestlé SA

- 13.2.2.1. Overview

- 13.2.2.2. Products

- 13.2.2.3. SWOT Analysis

- 13.2.2.4. Recent Developments

- 13.2.2.5. Financials (Based on Availability)

- 13.2.3 Perfetti Van Melle BV

- 13.2.3.1. Overview

- 13.2.3.2. Products

- 13.2.3.3. SWOT Analysis

- 13.2.3.4. Recent Developments

- 13.2.3.5. Financials (Based on Availability)

- 13.2.4 Swizzels Matlow Ltd

- 13.2.4.1. Overview

- 13.2.4.2. Products

- 13.2.4.3. SWOT Analysis

- 13.2.4.4. Recent Developments

- 13.2.4.5. Financials (Based on Availability)

- 13.2.5 Soldan Holding + Candy Specialties GmbH

- 13.2.5.1. Overview

- 13.2.5.2. Products

- 13.2.5.3. SWOT Analysis

- 13.2.5.4. Recent Developments

- 13.2.5.5. Financials (Based on Availability)

- 13.2.6 Lavdas SA

- 13.2.6.1. Overview

- 13.2.6.2. Products

- 13.2.6.3. SWOT Analysis

- 13.2.6.4. Recent Developments

- 13.2.6.5. Financials (Based on Availability)

- 13.2.7 August Storck KG

- 13.2.7.1. Overview

- 13.2.7.2. Products

- 13.2.7.3. SWOT Analysis

- 13.2.7.4. Recent Developments

- 13.2.7.5. Financials (Based on Availability)

- 13.2.8 Katjes International GmbH & Co KG

- 13.2.8.1. Overview

- 13.2.8.2. Products

- 13.2.8.3. SWOT Analysis

- 13.2.8.4. Recent Developments

- 13.2.8.5. Financials (Based on Availability)

- 13.2.9 Ferrero International SA

- 13.2.9.1. Overview

- 13.2.9.2. Products

- 13.2.9.3. SWOT Analysis

- 13.2.9.4. Recent Developments

- 13.2.9.5. Financials (Based on Availability)

- 13.2.10 Cloetta AB

- 13.2.10.1. Overview

- 13.2.10.2. Products

- 13.2.10.3. SWOT Analysis

- 13.2.10.4. Recent Developments

- 13.2.10.5. Financials (Based on Availability)

- 13.2.11 Ricola AG

- 13.2.11.1. Overview

- 13.2.11.2. Products

- 13.2.11.3. SWOT Analysis

- 13.2.11.4. Recent Developments

- 13.2.11.5. Financials (Based on Availability)

- 13.2.12 Mars Incorporated

- 13.2.12.1. Overview

- 13.2.12.2. Products

- 13.2.12.3. SWOT Analysis

- 13.2.12.4. Recent Developments

- 13.2.12.5. Financials (Based on Availability)

- 13.2.13 HARIBO Holding GmbH & Co KG

- 13.2.13.1. Overview

- 13.2.13.2. Products

- 13.2.13.3. SWOT Analysis

- 13.2.13.4. Recent Developments

- 13.2.13.5. Financials (Based on Availability)

- 13.2.14 Mondelēz International Inc

- 13.2.14.1. Overview

- 13.2.14.2. Products

- 13.2.14.3. SWOT Analysis

- 13.2.14.4. Recent Developments

- 13.2.14.5. Financials (Based on Availability)

- 13.2.15 The Hershey Company

- 13.2.15.1. Overview

- 13.2.15.2. Products

- 13.2.15.3. SWOT Analysis

- 13.2.15.4. Recent Developments

- 13.2.15.5. Financials (Based on Availability)

- 13.2.1 Vidal Golosina

List of Figures

- Figure 1: Europe Sugar Confectionery Market Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Europe Sugar Confectionery Market Share (%) by Company 2024

List of Tables

- Table 1: Europe Sugar Confectionery Market Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Europe Sugar Confectionery Market Volume K Tons Forecast, by Region 2019 & 2032

- Table 3: Europe Sugar Confectionery Market Revenue Million Forecast, by Confectionery Variant 2019 & 2032

- Table 4: Europe Sugar Confectionery Market Volume K Tons Forecast, by Confectionery Variant 2019 & 2032

- Table 5: Europe Sugar Confectionery Market Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 6: Europe Sugar Confectionery Market Volume K Tons Forecast, by Distribution Channel 2019 & 2032

- Table 7: Europe Sugar Confectionery Market Revenue Million Forecast, by Region 2019 & 2032

- Table 8: Europe Sugar Confectionery Market Volume K Tons Forecast, by Region 2019 & 2032

- Table 9: Europe Sugar Confectionery Market Revenue Million Forecast, by Country 2019 & 2032

- Table 10: Europe Sugar Confectionery Market Volume K Tons Forecast, by Country 2019 & 2032

- Table 11: Germany Europe Sugar Confectionery Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: Germany Europe Sugar Confectionery Market Volume (K Tons) Forecast, by Application 2019 & 2032

- Table 13: France Europe Sugar Confectionery Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: France Europe Sugar Confectionery Market Volume (K Tons) Forecast, by Application 2019 & 2032

- Table 15: Italy Europe Sugar Confectionery Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 16: Italy Europe Sugar Confectionery Market Volume (K Tons) Forecast, by Application 2019 & 2032

- Table 17: United Kingdom Europe Sugar Confectionery Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 18: United Kingdom Europe Sugar Confectionery Market Volume (K Tons) Forecast, by Application 2019 & 2032

- Table 19: Netherlands Europe Sugar Confectionery Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 20: Netherlands Europe Sugar Confectionery Market Volume (K Tons) Forecast, by Application 2019 & 2032

- Table 21: Sweden Europe Sugar Confectionery Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 22: Sweden Europe Sugar Confectionery Market Volume (K Tons) Forecast, by Application 2019 & 2032

- Table 23: Rest of Europe Europe Sugar Confectionery Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 24: Rest of Europe Europe Sugar Confectionery Market Volume (K Tons) Forecast, by Application 2019 & 2032

- Table 25: Europe Sugar Confectionery Market Revenue Million Forecast, by Confectionery Variant 2019 & 2032

- Table 26: Europe Sugar Confectionery Market Volume K Tons Forecast, by Confectionery Variant 2019 & 2032

- Table 27: Europe Sugar Confectionery Market Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 28: Europe Sugar Confectionery Market Volume K Tons Forecast, by Distribution Channel 2019 & 2032

- Table 29: Europe Sugar Confectionery Market Revenue Million Forecast, by Country 2019 & 2032

- Table 30: Europe Sugar Confectionery Market Volume K Tons Forecast, by Country 2019 & 2032

- Table 31: United Kingdom Europe Sugar Confectionery Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 32: United Kingdom Europe Sugar Confectionery Market Volume (K Tons) Forecast, by Application 2019 & 2032

- Table 33: Germany Europe Sugar Confectionery Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 34: Germany Europe Sugar Confectionery Market Volume (K Tons) Forecast, by Application 2019 & 2032

- Table 35: France Europe Sugar Confectionery Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 36: France Europe Sugar Confectionery Market Volume (K Tons) Forecast, by Application 2019 & 2032

- Table 37: Italy Europe Sugar Confectionery Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 38: Italy Europe Sugar Confectionery Market Volume (K Tons) Forecast, by Application 2019 & 2032

- Table 39: Spain Europe Sugar Confectionery Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 40: Spain Europe Sugar Confectionery Market Volume (K Tons) Forecast, by Application 2019 & 2032

- Table 41: Netherlands Europe Sugar Confectionery Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 42: Netherlands Europe Sugar Confectionery Market Volume (K Tons) Forecast, by Application 2019 & 2032

- Table 43: Belgium Europe Sugar Confectionery Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 44: Belgium Europe Sugar Confectionery Market Volume (K Tons) Forecast, by Application 2019 & 2032

- Table 45: Sweden Europe Sugar Confectionery Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 46: Sweden Europe Sugar Confectionery Market Volume (K Tons) Forecast, by Application 2019 & 2032

- Table 47: Norway Europe Sugar Confectionery Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 48: Norway Europe Sugar Confectionery Market Volume (K Tons) Forecast, by Application 2019 & 2032

- Table 49: Poland Europe Sugar Confectionery Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 50: Poland Europe Sugar Confectionery Market Volume (K Tons) Forecast, by Application 2019 & 2032

- Table 51: Denmark Europe Sugar Confectionery Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 52: Denmark Europe Sugar Confectionery Market Volume (K Tons) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Sugar Confectionery Market?

The projected CAGR is approximately 4.69%.

2. Which companies are prominent players in the Europe Sugar Confectionery Market?

Key companies in the market include Vidal Golosina, Nestlé SA, Perfetti Van Melle BV, Swizzels Matlow Ltd, Soldan Holding + Candy Specialties GmbH, Lavdas SA, August Storck KG, Katjes International GmbH & Co KG, Ferrero International SA, Cloetta AB, Ricola AG, Mars Incorporated, HARIBO Holding GmbH & Co KG, Mondelēz International Inc, The Hershey Company.

3. What are the main segments of the Europe Sugar Confectionery Market?

The market segments include Confectionery Variant, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 13810 Million as of 2022.

5. What are some drivers contributing to market growth?

Increased Consumption of Baked Goods; Demand for Indigenous Fermented Foods.

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

Potential Side-effects of Yeast.

8. Can you provide examples of recent developments in the market?

May 2023: British sweet manufacturer Swizzels expanded its popular range of Minions products with the addition of a Sherbet Dip. This Minions Sherbet Dip comprises three new flavors: Fizzy Orange, Sour Apple and Tangy Berry, and a classic Swizzelstick for dipping.April 2023: Swizzels Sweets has partnered with Applied Nutrition to launch a range of sports nutrition products in several of Swizzels’ well-known flavors. The sports brand Applied Nutrition announced Drumstick flavor lollies of both its bestselling hydration drink, BodyFuel, and a 60 ml shot variant of its popular pre-workout, A.B.E.March 2023: Hershey's introduced new Hershey's Kisses’ Milklicious candies, featuring a creamy chocolate milk filling packed into the delicious center of a rich, milk chocolate Hershey's Kisses candy.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Tons.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Sugar Confectionery Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Sugar Confectionery Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Sugar Confectionery Market?

To stay informed about further developments, trends, and reports in the Europe Sugar Confectionery Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence