Key Insights

The global market for Incontinence Devices and Ostomy is poised for substantial growth, driven by an aging population worldwide and an increasing prevalence of conditions leading to incontinence and ostomy requirements. The market size is estimated to be in the billions of dollars, with a significant Compound Annual Growth Rate (CAGR) projected over the forecast period. This expansion is fueled by rising awareness of advanced ostomy and incontinence management products, improved healthcare infrastructure, and a growing demand for discreet and user-friendly solutions. Key applications within this market encompass hospitals and clinics, where these devices are critical for patient care, as well as broader home-use scenarios driven by an aging demographic and individuals managing chronic conditions. The market segmentation highlights two primary product types: Incontinence Care Products, addressing a wide spectrum of urinary and fecal incontinence, and Ostomy Care Products, essential for individuals with surgically created ostomies.

The market's growth trajectory is supported by several key drivers, including technological advancements leading to more comfortable and effective products, a greater focus on patient quality of life, and increasing reimbursement policies in various regions. However, potential restraints such as the high cost of some advanced devices and limited access to specialized care in developing economies may pose challenges. Geographically, North America and Europe are expected to maintain a dominant market share due to their advanced healthcare systems and high adoption rates of innovative medical devices. The Asia Pacific region, however, presents a rapidly growing opportunity, propelled by rising disposable incomes, increasing healthcare expenditure, and a growing awareness of ostomy and incontinence management solutions. Major companies like Coloplast Corporation, Hollister Inc., and Kimberly-Clark Corporation are at the forefront of innovation, continuously launching new products to meet the evolving needs of patients and healthcare providers, thereby shaping the competitive landscape.

This in-depth market research report offers a comprehensive analysis of the global Incontinence Devices and Ostomy market, providing critical insights for industry professionals. Covering the historical period from 2019 to 2024 and projecting forward to 2033, with a base and estimated year of 2025 and a forecast period from 2025 to 2033, this report is an essential resource for understanding market dynamics, innovation trends, and growth opportunities. With an estimated market value of over a million dollars, this report delves into every facet of the industry, from key players to emerging technologies.

Incontinence Devices And Ostomy Market Structure & Innovation Trends

The Incontinence Devices and Ostomy market exhibits a moderately concentrated structure, with a few key players holding significant market share, estimated at over 50% collectively. Innovation is primarily driven by advancements in material science, product design for enhanced comfort and discretion, and the development of smart devices for remote monitoring. Regulatory frameworks, while varying by region, are generally focused on ensuring product safety and efficacy. Product substitutes, such as absorbent pads and reusable products, present a competitive challenge to traditional devices. End-user demographics are increasingly characterized by an aging global population and a rising prevalence of chronic diseases, driving demand across the Hospital, Clinic, and Others applications. Mergers and acquisitions (M&A) activities have been observed, with an estimated aggregate deal value in the millions, aimed at consolidating market presence and expanding product portfolios. Key M&A targets often include innovative startups and companies with complementary product lines, further shaping the competitive landscape.

Incontinence Devices And Ostomy Market Dynamics & Trends

The Incontinence Devices and Ostomy market is experiencing robust growth, propelled by a confluence of favorable market dynamics and evolving trends. A primary growth driver is the escalating prevalence of urinary and fecal incontinence globally, attributed to an aging population, rising rates of chronic conditions like diabetes and neurological disorders, and increased survival rates from medical procedures that can lead to ostomy formation. Technological disruptions are playing a pivotal role, with significant investments in research and development yielding next-generation products. These include advanced absorbent materials offering superior leakage protection and odor control, discreet and comfortable ostomy pouches with enhanced adhesion and reduced skin irritation, and innovative application systems designed for ease of use. The integration of smart technologies, such as sensors that monitor fluid levels and alert users or caregivers, is also gaining traction, enhancing the quality of life for individuals managing these conditions.

Consumer preferences are shifting towards products that offer greater comfort, discretion, and a sense of normalcy. This demand is fueling innovation in materials, designs, and packaging, moving away from purely functional solutions towards user-centric designs that empower individuals. The increasing awareness and reduced stigma surrounding incontinence and ostomy care are also contributing to higher market penetration. Healthcare professionals are playing a crucial role in patient education and product recommendation, further influencing consumer choices.

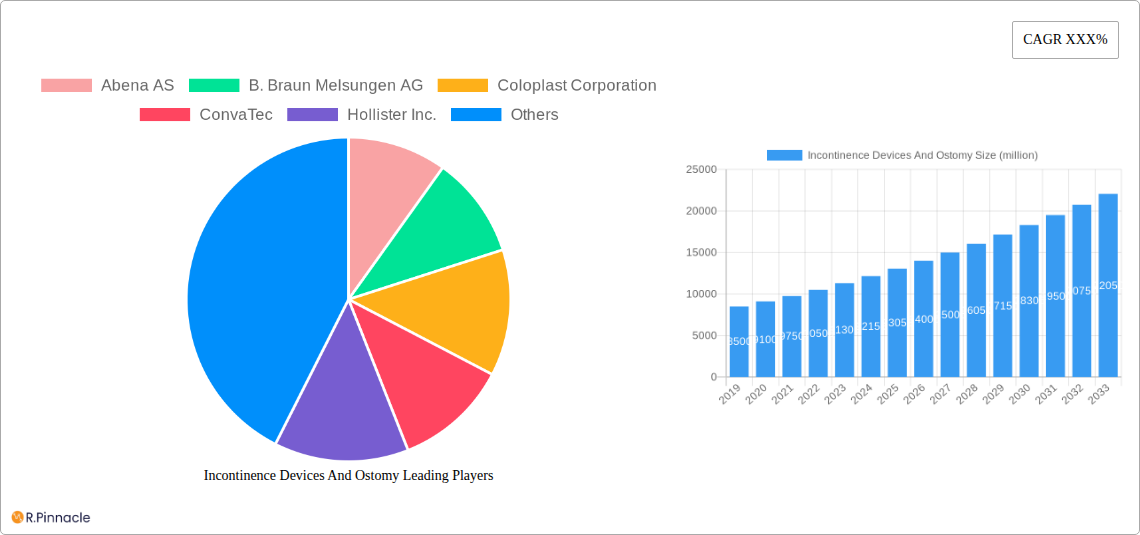

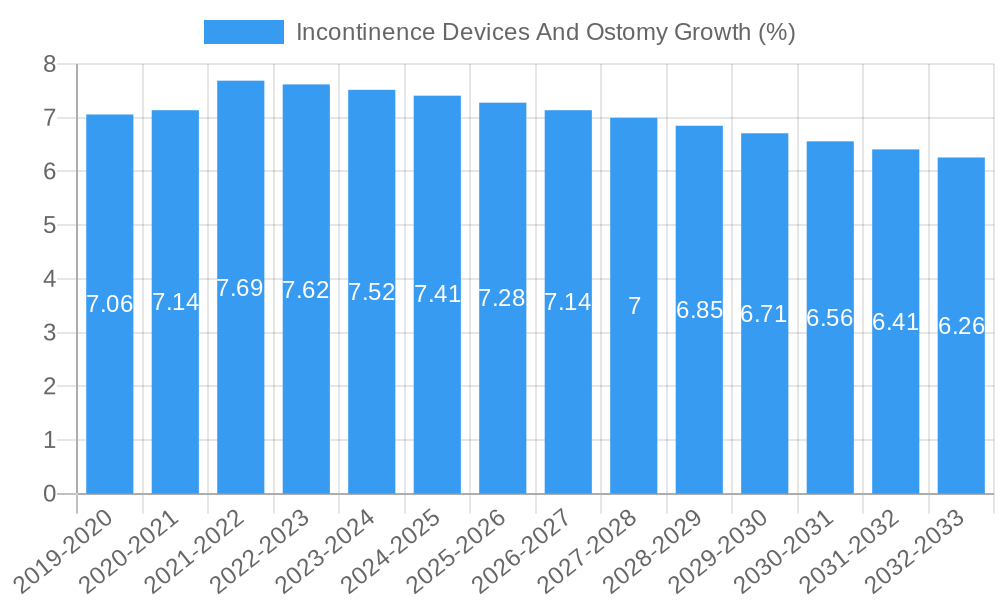

Competitive dynamics within the market are characterized by intense rivalry, with established players continually innovating and expanding their product offerings to maintain market share. Emerging companies are focusing on niche segments and disruptive technologies, creating a dynamic and evolving competitive landscape. Strategic partnerships and collaborations between manufacturers, healthcare providers, and technology companies are becoming more prevalent, aimed at developing integrated solutions and expanding market reach. The overall market penetration is estimated to be in the tens of percent, with significant room for further growth, especially in emerging economies. The Compound Annual Growth Rate (CAGR) for the forecast period is projected to be in the high single digits, underscoring the significant growth potential of this sector.

Dominant Regions & Segments in Incontinence Devices And Ostomy

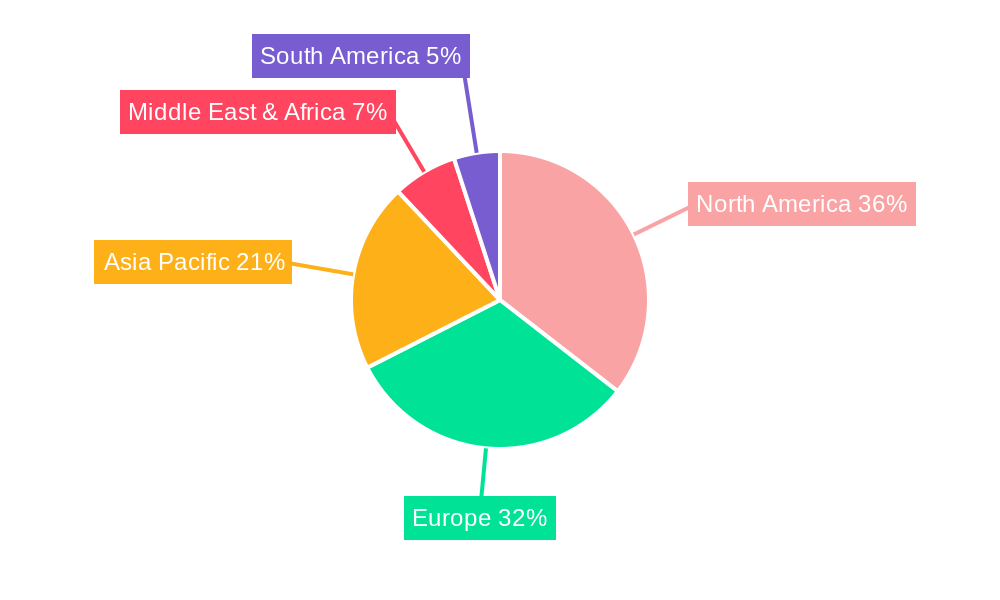

North America currently dominates the Incontinence Devices and Ostomy market, driven by a confluence of factors including a well-established healthcare infrastructure, high disposable incomes, and a greater emphasis on patient quality of life. The United States, in particular, leads in market share due to its advanced medical facilities and a significant elderly population. Economic policies favoring healthcare spending and robust reimbursement frameworks for medical devices further bolster market dominance.

Within the segment analysis, Incontinence Care Products represent the larger market share compared to Ostomy Care Products, owing to the broader applicability of incontinence management across various age groups and conditions. The Hospital application segment demonstrates substantial growth, fueled by increasing hospital admissions for conditions requiring incontinence management and post-surgical ostomy care. The Clinic segment also plays a vital role, offering specialized care and product fitting services. The Others segment, encompassing home healthcare and retail sales, is also experiencing significant expansion as individuals seek convenient and accessible solutions.

Key drivers of dominance in this region and these segments include:

- Aging Population: A substantial demographic of individuals aged 65 and above, a key consumer group for both incontinence and ostomy products.

- High Disease Prevalence: The high incidence of chronic diseases such as diabetes, neurological disorders, and inflammatory bowel diseases contributes significantly to the demand.

- Technological Advancements: Continuous innovation in product materials and design leading to more effective and user-friendly solutions.

- Healthcare Expenditure: Robust government and private healthcare spending ensures access to advanced medical devices and treatments.

- Reimbursement Policies: Favorable reimbursement policies for incontinence and ostomy supplies facilitate wider adoption.

- Awareness and Education: Increased public awareness and educational initiatives reduce stigma and encourage seeking appropriate care.

Incontinence Devices And Ostomy Product Innovations

Product innovations in the Incontinence Devices and Ostomy market are centered on enhancing user comfort, discretion, and effectiveness. Advancements in superabsorbent polymers have led to thinner, more absorbent pads with superior odor control. Ostomy pouches are featuring improved skin barrier technology for reduced irritation and enhanced adhesion, along with quieter, more discreet materials. Smart devices are emerging, incorporating sensors for fluid level monitoring and connectivity for remote patient management, offering a significant competitive advantage by improving patient autonomy and caregiver efficiency. These innovations cater to a growing demand for personalized and less intrusive solutions.

Report Scope & Segmentation Analysis

This report segments the Incontinence Devices and Ostomy market by Application and Type. The Application segments include Hospital, Clinic, and Others. The Hospital segment, projected to reach a market size in the hundreds of millions, is driven by increasing patient volumes and post-operative care needs. The Clinic segment, with an estimated market size in the tens of millions, focuses on specialized care and patient education. The Others segment, encompassing home healthcare and retail, is expected to witness robust growth in the hundreds of millions, driven by convenience and patient preference.

The Type segments are Incontinence Care Products and Ostomy Care Products. Incontinence Care Products, the larger segment with a projected market size in the billions, encompasses adult diapers, pads, and catheters. Ostomy Care Products, with an estimated market size in the hundreds of millions, includes ostomy bags, barriers, and accessories. Competitive dynamics within these segments are influenced by product innovation, brand loyalty, and distribution networks.

Key Drivers of Incontinence Devices And Ostomy Growth

Several key drivers are propelling the growth of the Incontinence Devices and Ostomy market. The escalating global prevalence of incontinence, exacerbated by an aging population and a rise in chronic diseases, is a primary factor. Technological advancements in material science and product design are leading to more comfortable, discreet, and effective solutions, such as advanced absorbent cores and improved skin-friendly adhesives. Increased awareness and reduced stigma surrounding these conditions are encouraging more individuals to seek appropriate management options. Furthermore, favorable reimbursement policies in many developed nations ensure greater accessibility to these essential medical devices. The growing trend towards home healthcare and remote patient monitoring also presents significant opportunities for market expansion.

Challenges in the Incontinence Devices And Ostomy Sector

Despite robust growth, the Incontinence Devices and Ostomy sector faces several challenges. Stringent regulatory approval processes for new medical devices can lead to extended development timelines and increased costs. Supply chain disruptions, as witnessed in recent global events, can impact the availability and pricing of raw materials and finished products. Intense competitive pressure from both established brands and emerging players can lead to price wars and necessitate continuous innovation to maintain market share. Palpable challenges also include the cost of advanced products, which can be a barrier for some consumer segments, and the need for ongoing patient and caregiver education to ensure optimal product utilization and adherence.

Emerging Opportunities in Incontinence Devices And Ostomy

Emerging opportunities in the Incontinence Devices and Ostomy market are diverse and promising. The development of smart and connected devices, offering real-time monitoring and data analytics for personalized care, represents a significant avenue for growth. Expansion into emerging economies with growing middle classes and increasing healthcare awareness offers substantial untapped market potential. The niche segment of pediatric incontinence management is also ripe for innovation and market penetration. Furthermore, the demand for sustainable and eco-friendly products is creating opportunities for manufacturers to develop biodegradable or reusable incontinence and ostomy solutions. Partnerships with telehealth providers and home care agencies can further enhance market reach and service delivery.

Leading Players in the Incontinence Devices And Ostomy Market

- Abena AS

- B. Braun Melsungen AG

- Coloplast Corporation

- ConvaTec

- Hollister Inc.

- Kimberly-Clark Corporation

- Salts Healthcare

- Unicharm Corporation

Key Developments in Incontinence Devices And Ostomy Industry

- 2023/11: Launch of a new generation of ultra-thin, high-absorbency incontinence pads by a leading manufacturer, focusing on discreetness and comfort.

- 2023/09: Acquisition of a medical technology startup specializing in wearable ostomy monitoring devices by a major player, signaling a move towards smart health solutions.

- 2023/07: Introduction of a novel skin barrier formulation for ostomy products, designed to minimize irritation and improve adherence for sensitive skin.

- 2023/05: Expansion of a prominent company's manufacturing capabilities in Asia to meet growing demand in emerging markets.

- 2022/12: Development of a biodegradable ostomy pouch, addressing growing consumer demand for sustainable healthcare products.

- 2022/10: Strategic partnership formed between an incontinence device manufacturer and a telehealth platform to enhance remote patient support.

Future Outlook for Incontinence Devices And Ostomy Market

- 2023/11: Launch of a new generation of ultra-thin, high-absorbency incontinence pads by a leading manufacturer, focusing on discreetness and comfort.

- 2023/09: Acquisition of a medical technology startup specializing in wearable ostomy monitoring devices by a major player, signaling a move towards smart health solutions.

- 2023/07: Introduction of a novel skin barrier formulation for ostomy products, designed to minimize irritation and improve adherence for sensitive skin.

- 2023/05: Expansion of a prominent company's manufacturing capabilities in Asia to meet growing demand in emerging markets.

- 2022/12: Development of a biodegradable ostomy pouch, addressing growing consumer demand for sustainable healthcare products.

- 2022/10: Strategic partnership formed between an incontinence device manufacturer and a telehealth platform to enhance remote patient support.

Future Outlook for Incontinence Devices And Ostomy Market

The future outlook for the Incontinence Devices and Ostomy market is exceptionally positive, driven by a sustained increase in demand and continuous innovation. The aging global population, coupled with advancements in medical treatments leading to longer lifespans and higher incidences of chronic conditions, will continue to fuel market expansion. The integration of smart technologies, such as AI-powered predictive analytics and wearable sensors, is set to revolutionize patient care, offering unprecedented levels of autonomy and improved health outcomes. Emerging markets, with their rapidly growing economies and increasing healthcare expenditure, represent significant untapped potential. Strategic investments in research and development, focusing on user-centric designs, advanced materials, and sustainable solutions, will be crucial for market players to maintain a competitive edge and capitalize on the burgeoning opportunities. The market is poised for sustained growth in the hundreds of millions, with an estimated market size in the tens of billions by the end of the forecast period.

Incontinence Devices And Ostomy Segmentation

-

1. Application

- 1.1. Hospital

- 1.2. Clinic

- 1.3. Others

-

2. Type

- 2.1. Incontinence Care Products

- 2.2. Ostomy Care Products

Incontinence Devices And Ostomy Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Incontinence Devices And Ostomy REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XXX% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Incontinence Devices And Ostomy Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Hospital

- 5.1.2. Clinic

- 5.1.3. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Incontinence Care Products

- 5.2.2. Ostomy Care Products

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Incontinence Devices And Ostomy Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Hospital

- 6.1.2. Clinic

- 6.1.3. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Incontinence Care Products

- 6.2.2. Ostomy Care Products

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Incontinence Devices And Ostomy Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Hospital

- 7.1.2. Clinic

- 7.1.3. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Incontinence Care Products

- 7.2.2. Ostomy Care Products

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Incontinence Devices And Ostomy Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Hospital

- 8.1.2. Clinic

- 8.1.3. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Incontinence Care Products

- 8.2.2. Ostomy Care Products

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Incontinence Devices And Ostomy Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Hospital

- 9.1.2. Clinic

- 9.1.3. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Incontinence Care Products

- 9.2.2. Ostomy Care Products

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Incontinence Devices And Ostomy Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Hospital

- 10.1.2. Clinic

- 10.1.3. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Incontinence Care Products

- 10.2.2. Ostomy Care Products

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 Abena AS

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 B. Braun Melsungen AG

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Coloplast Corporation

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 ConvaTec

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Hollister Inc.

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Kimberly-Clark Corporation

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Salts Healthcare

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Unicharm Corporation

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.1 Abena AS

List of Figures

- Figure 1: Global Incontinence Devices And Ostomy Revenue Breakdown (million, %) by Region 2024 & 2032

- Figure 2: North America Incontinence Devices And Ostomy Revenue (million), by Application 2024 & 2032

- Figure 3: North America Incontinence Devices And Ostomy Revenue Share (%), by Application 2024 & 2032

- Figure 4: North America Incontinence Devices And Ostomy Revenue (million), by Type 2024 & 2032

- Figure 5: North America Incontinence Devices And Ostomy Revenue Share (%), by Type 2024 & 2032

- Figure 6: North America Incontinence Devices And Ostomy Revenue (million), by Country 2024 & 2032

- Figure 7: North America Incontinence Devices And Ostomy Revenue Share (%), by Country 2024 & 2032

- Figure 8: South America Incontinence Devices And Ostomy Revenue (million), by Application 2024 & 2032

- Figure 9: South America Incontinence Devices And Ostomy Revenue Share (%), by Application 2024 & 2032

- Figure 10: South America Incontinence Devices And Ostomy Revenue (million), by Type 2024 & 2032

- Figure 11: South America Incontinence Devices And Ostomy Revenue Share (%), by Type 2024 & 2032

- Figure 12: South America Incontinence Devices And Ostomy Revenue (million), by Country 2024 & 2032

- Figure 13: South America Incontinence Devices And Ostomy Revenue Share (%), by Country 2024 & 2032

- Figure 14: Europe Incontinence Devices And Ostomy Revenue (million), by Application 2024 & 2032

- Figure 15: Europe Incontinence Devices And Ostomy Revenue Share (%), by Application 2024 & 2032

- Figure 16: Europe Incontinence Devices And Ostomy Revenue (million), by Type 2024 & 2032

- Figure 17: Europe Incontinence Devices And Ostomy Revenue Share (%), by Type 2024 & 2032

- Figure 18: Europe Incontinence Devices And Ostomy Revenue (million), by Country 2024 & 2032

- Figure 19: Europe Incontinence Devices And Ostomy Revenue Share (%), by Country 2024 & 2032

- Figure 20: Middle East & Africa Incontinence Devices And Ostomy Revenue (million), by Application 2024 & 2032

- Figure 21: Middle East & Africa Incontinence Devices And Ostomy Revenue Share (%), by Application 2024 & 2032

- Figure 22: Middle East & Africa Incontinence Devices And Ostomy Revenue (million), by Type 2024 & 2032

- Figure 23: Middle East & Africa Incontinence Devices And Ostomy Revenue Share (%), by Type 2024 & 2032

- Figure 24: Middle East & Africa Incontinence Devices And Ostomy Revenue (million), by Country 2024 & 2032

- Figure 25: Middle East & Africa Incontinence Devices And Ostomy Revenue Share (%), by Country 2024 & 2032

- Figure 26: Asia Pacific Incontinence Devices And Ostomy Revenue (million), by Application 2024 & 2032

- Figure 27: Asia Pacific Incontinence Devices And Ostomy Revenue Share (%), by Application 2024 & 2032

- Figure 28: Asia Pacific Incontinence Devices And Ostomy Revenue (million), by Type 2024 & 2032

- Figure 29: Asia Pacific Incontinence Devices And Ostomy Revenue Share (%), by Type 2024 & 2032

- Figure 30: Asia Pacific Incontinence Devices And Ostomy Revenue (million), by Country 2024 & 2032

- Figure 31: Asia Pacific Incontinence Devices And Ostomy Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Incontinence Devices And Ostomy Revenue million Forecast, by Region 2019 & 2032

- Table 2: Global Incontinence Devices And Ostomy Revenue million Forecast, by Application 2019 & 2032

- Table 3: Global Incontinence Devices And Ostomy Revenue million Forecast, by Type 2019 & 2032

- Table 4: Global Incontinence Devices And Ostomy Revenue million Forecast, by Region 2019 & 2032

- Table 5: Global Incontinence Devices And Ostomy Revenue million Forecast, by Application 2019 & 2032

- Table 6: Global Incontinence Devices And Ostomy Revenue million Forecast, by Type 2019 & 2032

- Table 7: Global Incontinence Devices And Ostomy Revenue million Forecast, by Country 2019 & 2032

- Table 8: United States Incontinence Devices And Ostomy Revenue (million) Forecast, by Application 2019 & 2032

- Table 9: Canada Incontinence Devices And Ostomy Revenue (million) Forecast, by Application 2019 & 2032

- Table 10: Mexico Incontinence Devices And Ostomy Revenue (million) Forecast, by Application 2019 & 2032

- Table 11: Global Incontinence Devices And Ostomy Revenue million Forecast, by Application 2019 & 2032

- Table 12: Global Incontinence Devices And Ostomy Revenue million Forecast, by Type 2019 & 2032

- Table 13: Global Incontinence Devices And Ostomy Revenue million Forecast, by Country 2019 & 2032

- Table 14: Brazil Incontinence Devices And Ostomy Revenue (million) Forecast, by Application 2019 & 2032

- Table 15: Argentina Incontinence Devices And Ostomy Revenue (million) Forecast, by Application 2019 & 2032

- Table 16: Rest of South America Incontinence Devices And Ostomy Revenue (million) Forecast, by Application 2019 & 2032

- Table 17: Global Incontinence Devices And Ostomy Revenue million Forecast, by Application 2019 & 2032

- Table 18: Global Incontinence Devices And Ostomy Revenue million Forecast, by Type 2019 & 2032

- Table 19: Global Incontinence Devices And Ostomy Revenue million Forecast, by Country 2019 & 2032

- Table 20: United Kingdom Incontinence Devices And Ostomy Revenue (million) Forecast, by Application 2019 & 2032

- Table 21: Germany Incontinence Devices And Ostomy Revenue (million) Forecast, by Application 2019 & 2032

- Table 22: France Incontinence Devices And Ostomy Revenue (million) Forecast, by Application 2019 & 2032

- Table 23: Italy Incontinence Devices And Ostomy Revenue (million) Forecast, by Application 2019 & 2032

- Table 24: Spain Incontinence Devices And Ostomy Revenue (million) Forecast, by Application 2019 & 2032

- Table 25: Russia Incontinence Devices And Ostomy Revenue (million) Forecast, by Application 2019 & 2032

- Table 26: Benelux Incontinence Devices And Ostomy Revenue (million) Forecast, by Application 2019 & 2032

- Table 27: Nordics Incontinence Devices And Ostomy Revenue (million) Forecast, by Application 2019 & 2032

- Table 28: Rest of Europe Incontinence Devices And Ostomy Revenue (million) Forecast, by Application 2019 & 2032

- Table 29: Global Incontinence Devices And Ostomy Revenue million Forecast, by Application 2019 & 2032

- Table 30: Global Incontinence Devices And Ostomy Revenue million Forecast, by Type 2019 & 2032

- Table 31: Global Incontinence Devices And Ostomy Revenue million Forecast, by Country 2019 & 2032

- Table 32: Turkey Incontinence Devices And Ostomy Revenue (million) Forecast, by Application 2019 & 2032

- Table 33: Israel Incontinence Devices And Ostomy Revenue (million) Forecast, by Application 2019 & 2032

- Table 34: GCC Incontinence Devices And Ostomy Revenue (million) Forecast, by Application 2019 & 2032

- Table 35: North Africa Incontinence Devices And Ostomy Revenue (million) Forecast, by Application 2019 & 2032

- Table 36: South Africa Incontinence Devices And Ostomy Revenue (million) Forecast, by Application 2019 & 2032

- Table 37: Rest of Middle East & Africa Incontinence Devices And Ostomy Revenue (million) Forecast, by Application 2019 & 2032

- Table 38: Global Incontinence Devices And Ostomy Revenue million Forecast, by Application 2019 & 2032

- Table 39: Global Incontinence Devices And Ostomy Revenue million Forecast, by Type 2019 & 2032

- Table 40: Global Incontinence Devices And Ostomy Revenue million Forecast, by Country 2019 & 2032

- Table 41: China Incontinence Devices And Ostomy Revenue (million) Forecast, by Application 2019 & 2032

- Table 42: India Incontinence Devices And Ostomy Revenue (million) Forecast, by Application 2019 & 2032

- Table 43: Japan Incontinence Devices And Ostomy Revenue (million) Forecast, by Application 2019 & 2032

- Table 44: South Korea Incontinence Devices And Ostomy Revenue (million) Forecast, by Application 2019 & 2032

- Table 45: ASEAN Incontinence Devices And Ostomy Revenue (million) Forecast, by Application 2019 & 2032

- Table 46: Oceania Incontinence Devices And Ostomy Revenue (million) Forecast, by Application 2019 & 2032

- Table 47: Rest of Asia Pacific Incontinence Devices And Ostomy Revenue (million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Incontinence Devices And Ostomy?

The projected CAGR is approximately XXX%.

2. Which companies are prominent players in the Incontinence Devices And Ostomy?

Key companies in the market include Abena AS, B. Braun Melsungen AG, Coloplast Corporation, ConvaTec, Hollister Inc., Kimberly-Clark Corporation, Salts Healthcare, Unicharm Corporation.

3. What are the main segments of the Incontinence Devices And Ostomy?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Incontinence Devices And Ostomy," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Incontinence Devices And Ostomy report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Incontinence Devices And Ostomy?

To stay informed about further developments, trends, and reports in the Incontinence Devices And Ostomy, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence